We’ve heard the Fed’s pitches about inflation being transitory, the overriding need to keep stimulus flowing and interest rates at all-time lows, etc. But, as we witness the ongoing Gamestopification of the market, will investors be able to ignore next week’s evidence of persistent inflation that the Fed’s own actions has produced? I think they might need some new slogans.

Futures are off moderately on – drumroll please – better than expected ADP employment and initial claims.

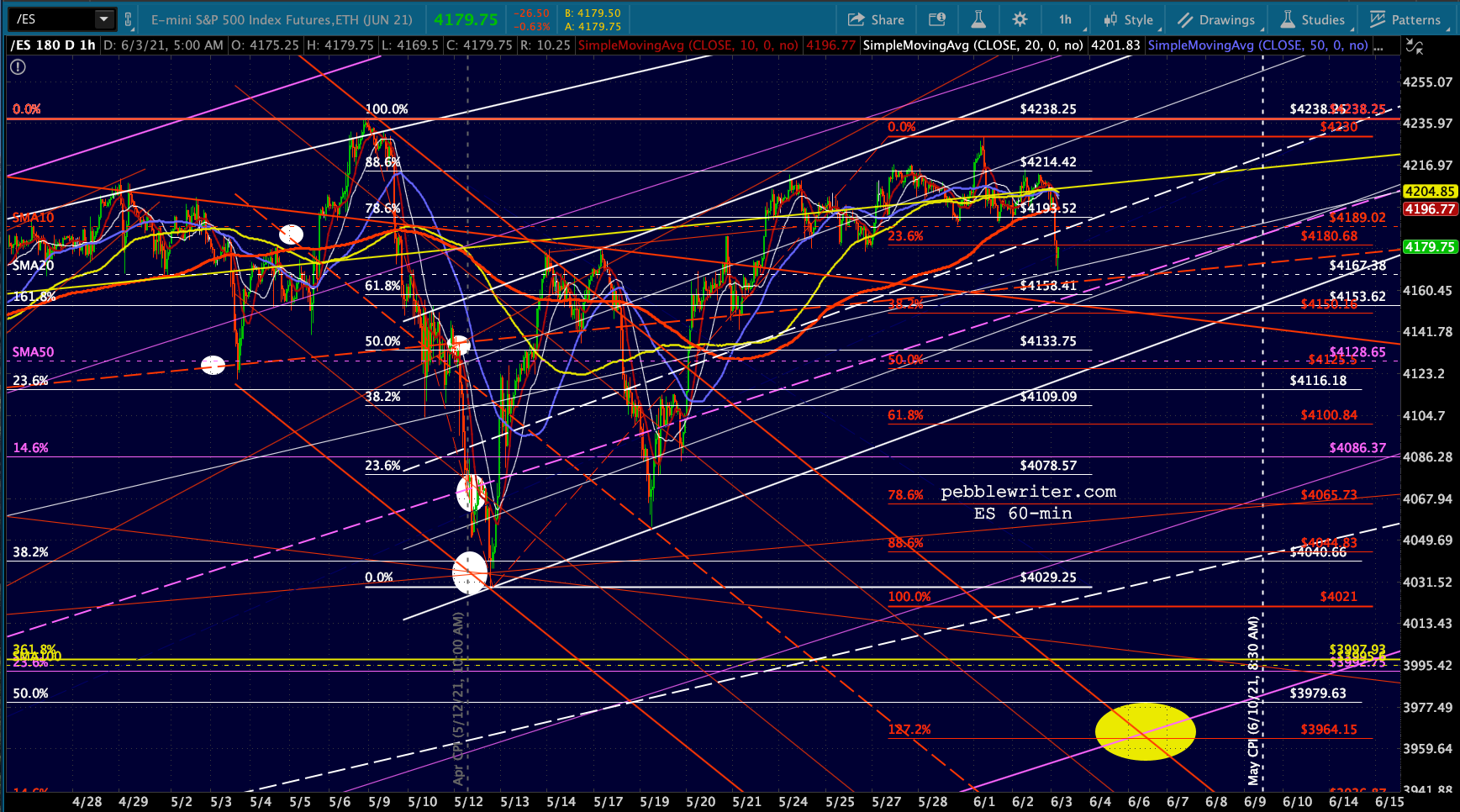

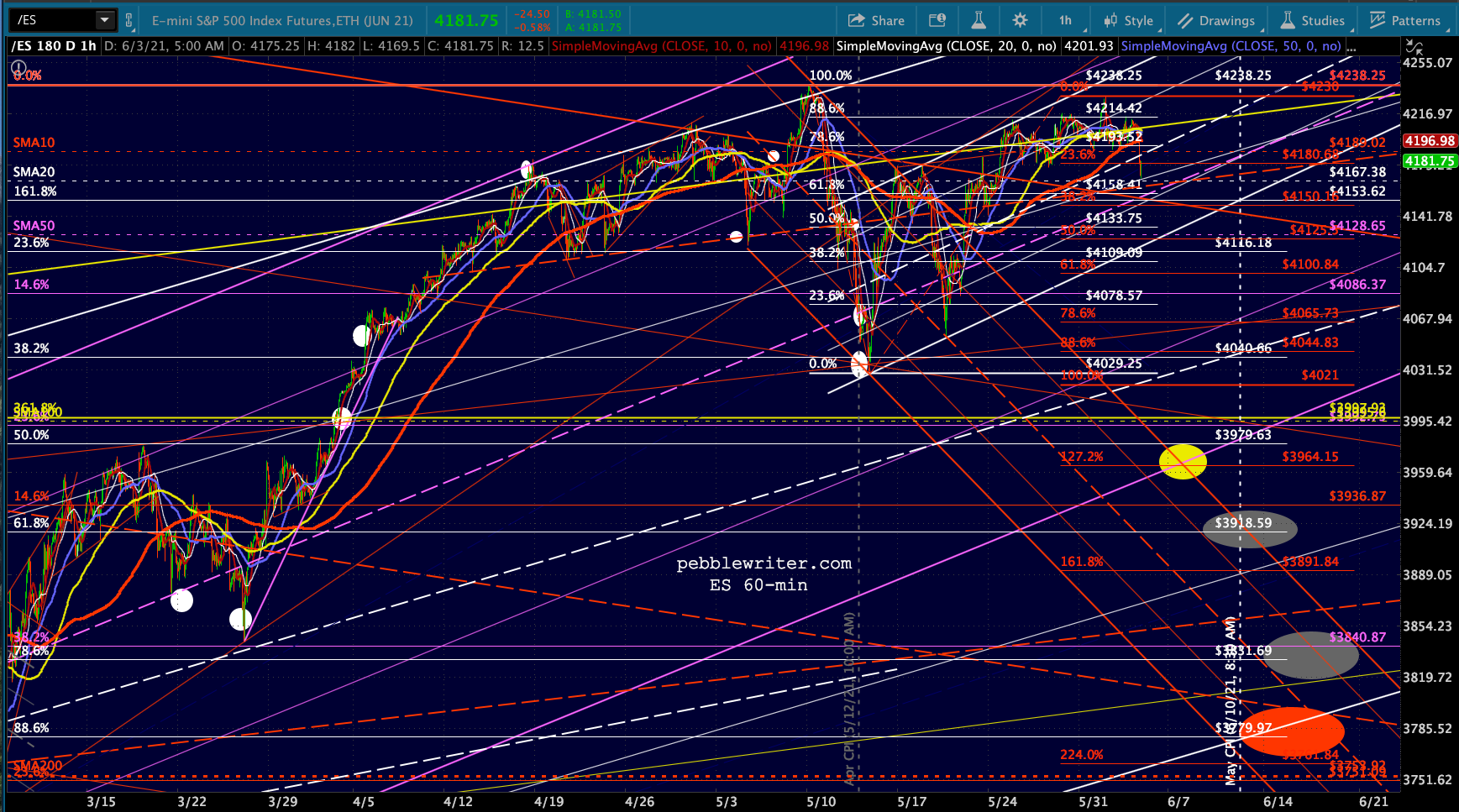

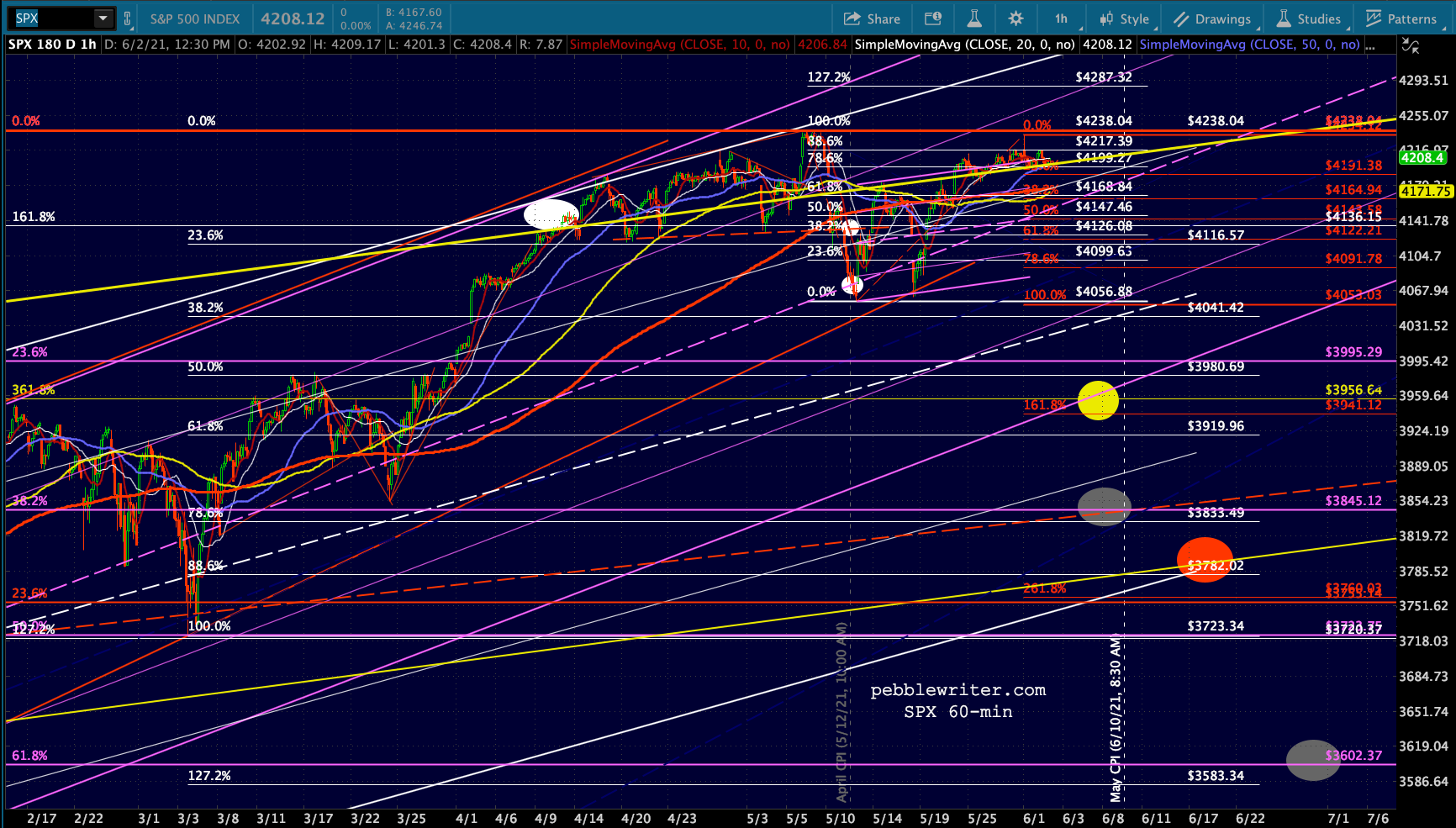

continued for members…The big picture hasn’t changed. Is it time to let the market take a pause and take advantage of its now much higher moving averages?

continued for members…The big picture hasn’t changed. Is it time to let the market take a pause and take advantage of its now much higher moving averages?

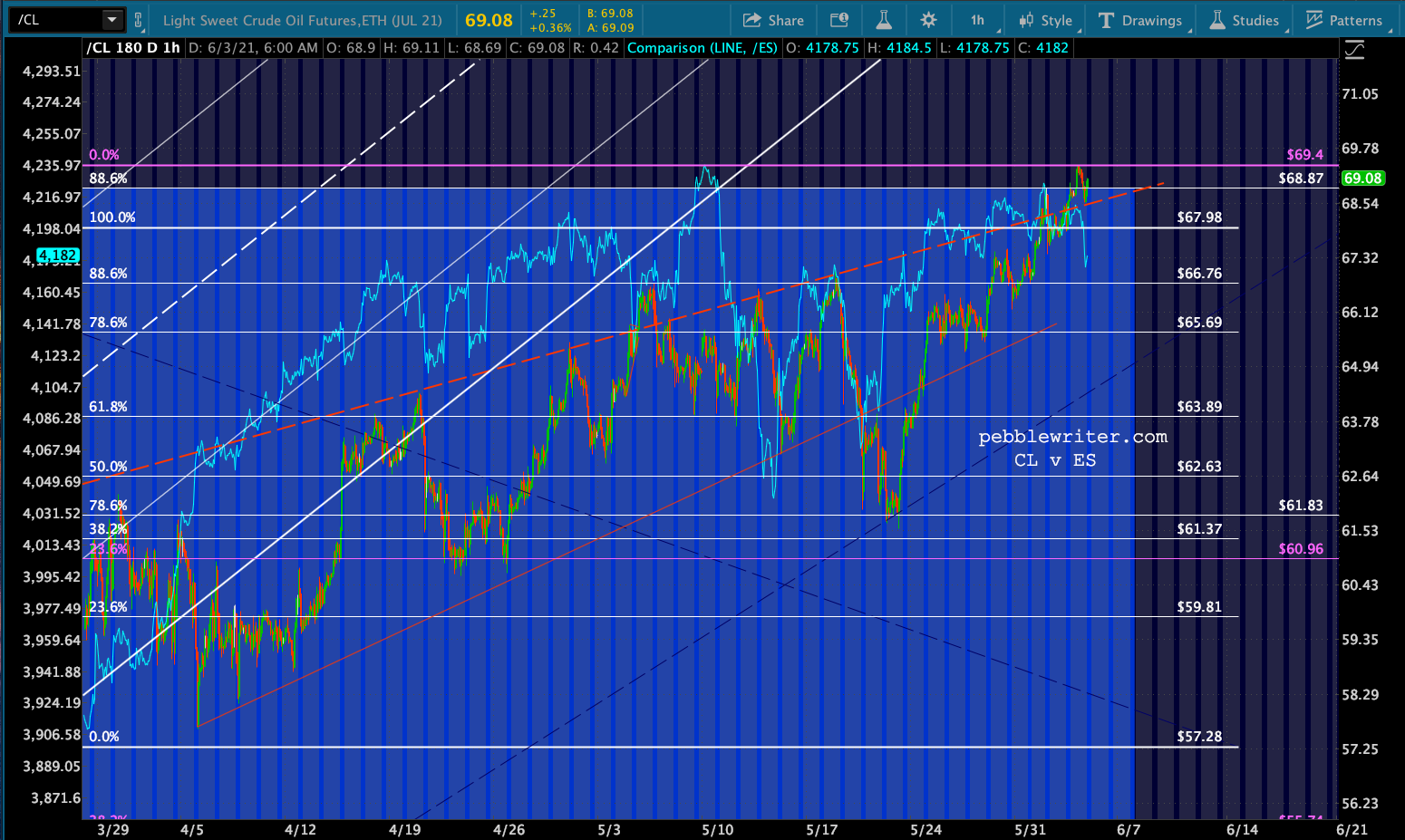

CL has an important decision to make here. It has pushed above its .886, which is connected to higher interest rates – which the Fed obviously does not want – as well as higher stock prices. EIA inventories are due out at 11am this morning.

CL has an important decision to make here. It has pushed above its .886, which is connected to higher interest rates – which the Fed obviously does not want – as well as higher stock prices. EIA inventories are due out at 11am this morning.

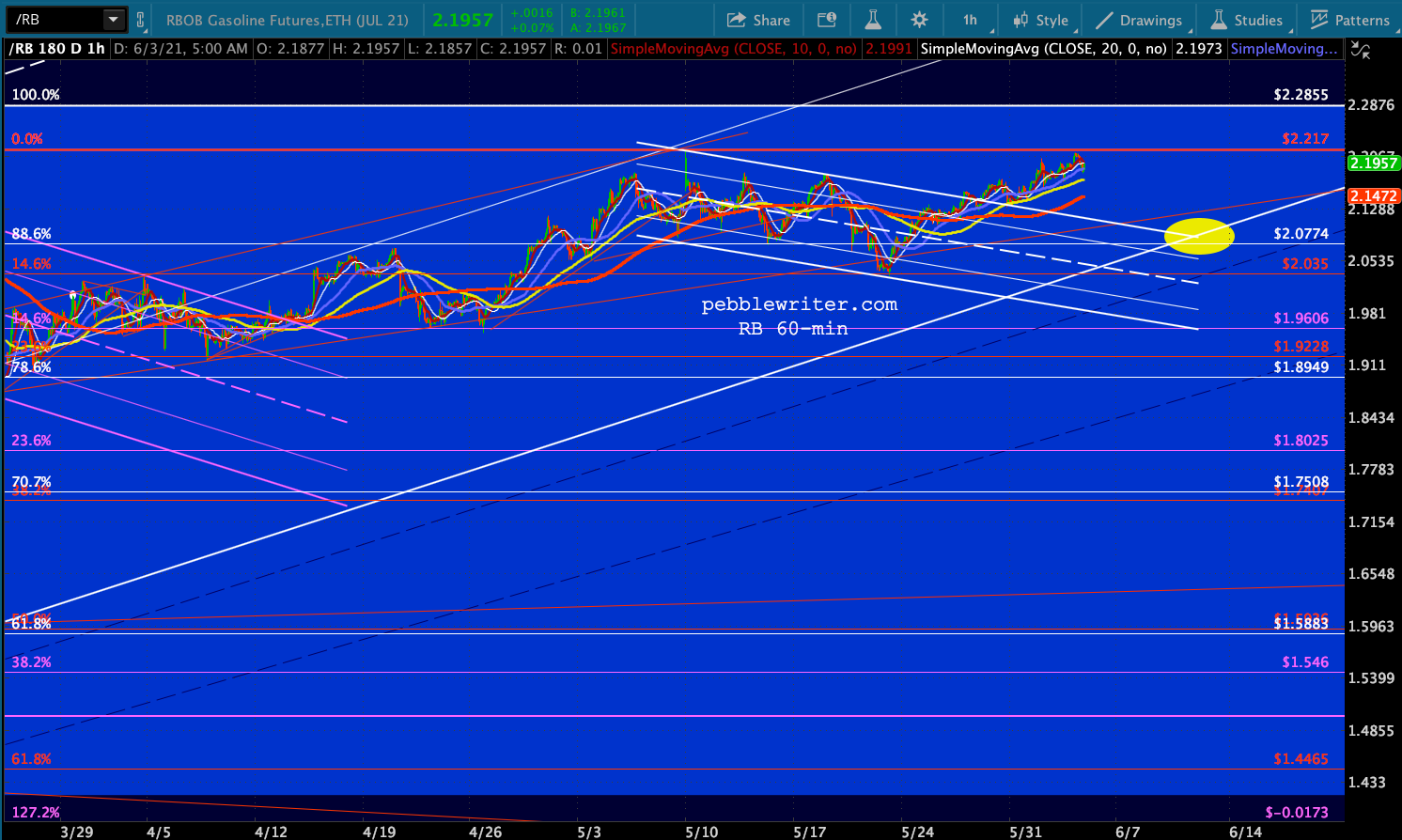

RB is already nudging up against its 2018 highs.

RB is already nudging up against its 2018 highs.

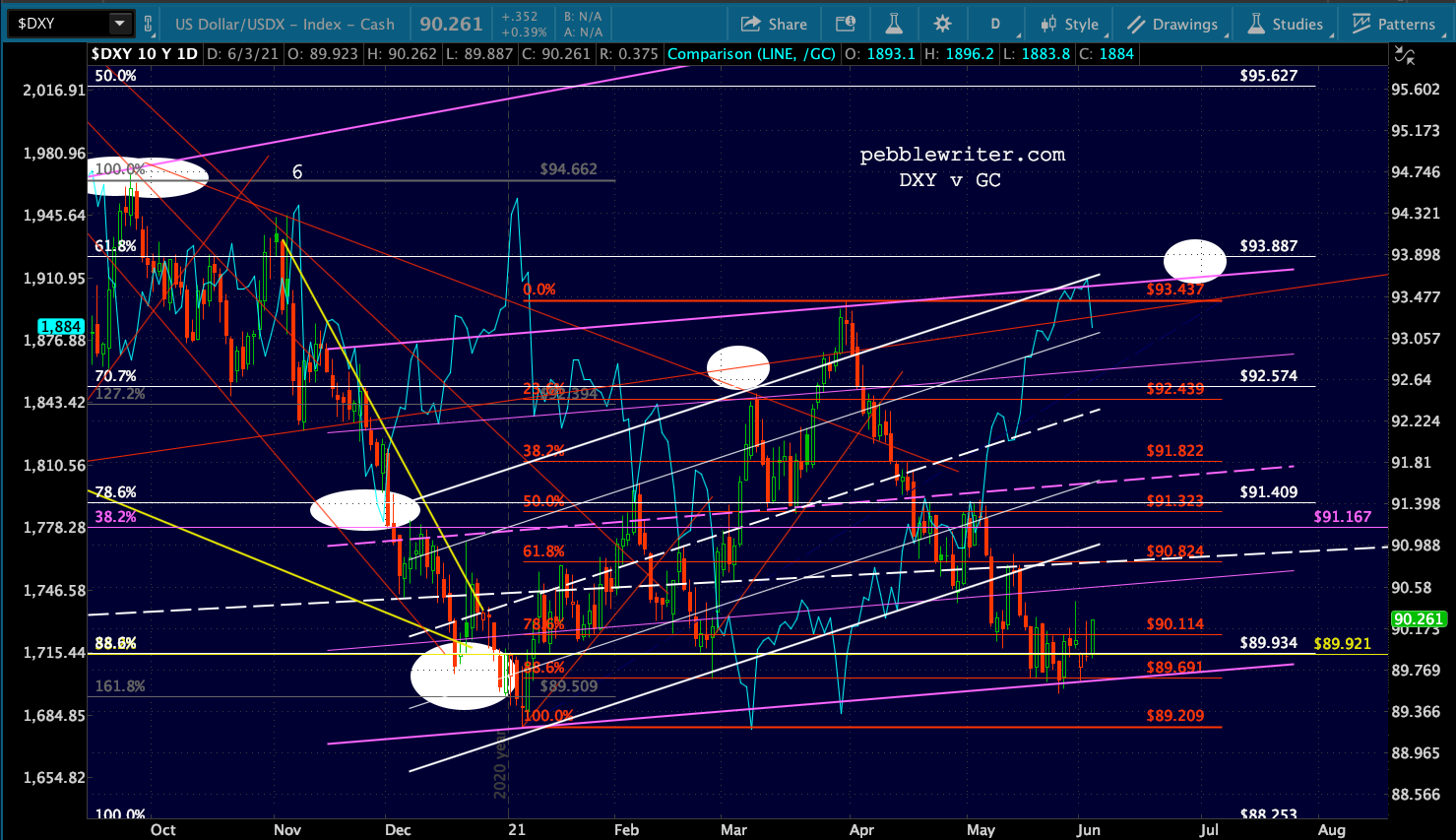

If, as I expect, stocks are going to be allowed to correct, we’ll need to see some giveup on USDJPY’s “breakout.”

If, as I expect, stocks are going to be allowed to correct, we’ll need to see some giveup on USDJPY’s “breakout.”

The yen’s strength should be offset by dollar strength versus the euro…

The yen’s strength should be offset by dollar strength versus the euro…  …resulting in a net gain for DXY…

…resulting in a net gain for DXY… …even as TNX is likely to nosedive.

…even as TNX is likely to nosedive.

Remember, declining rates means higher ZN, which should mean higher GC prices.

Remember, declining rates means higher ZN, which should mean higher GC prices.

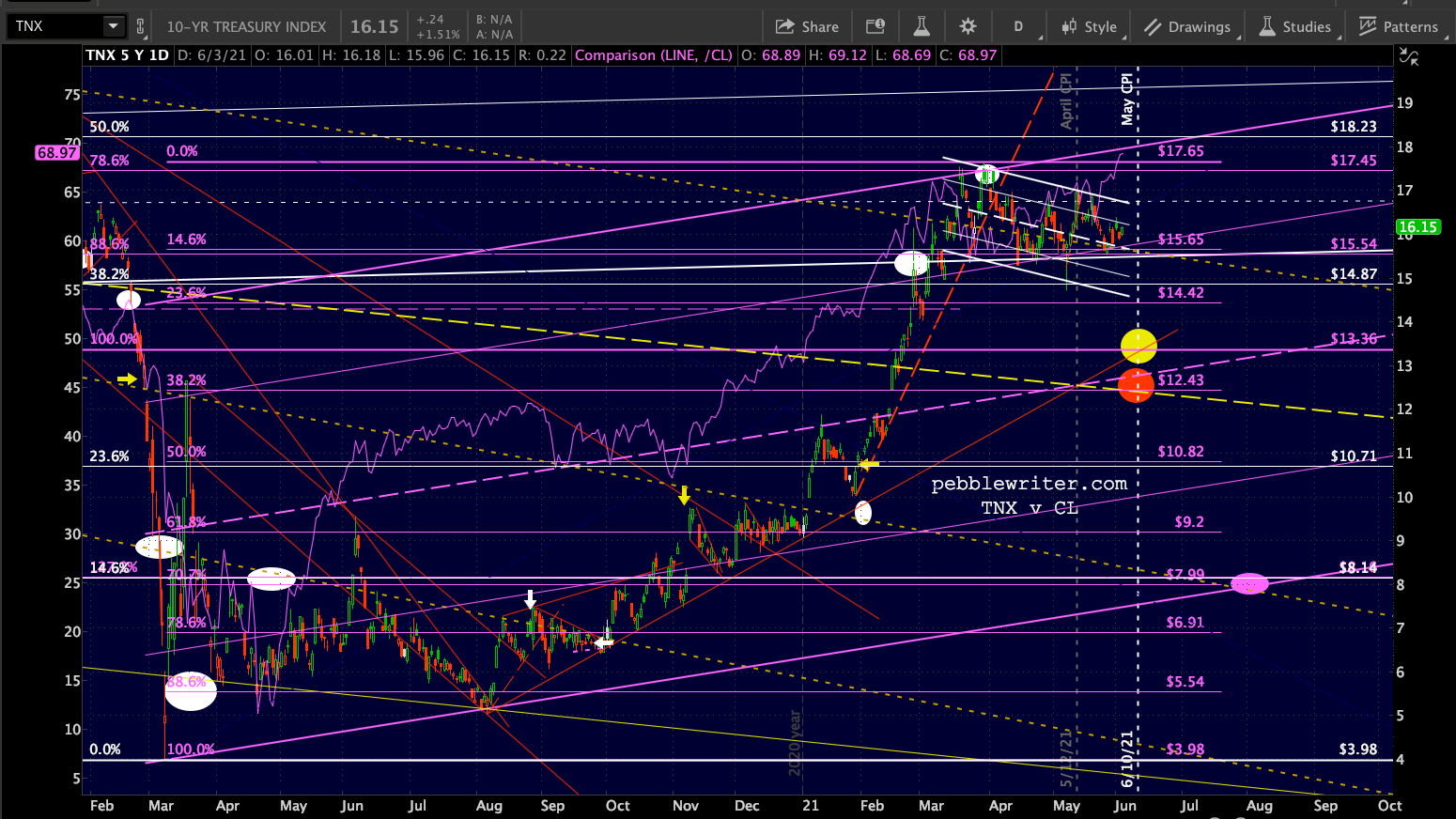

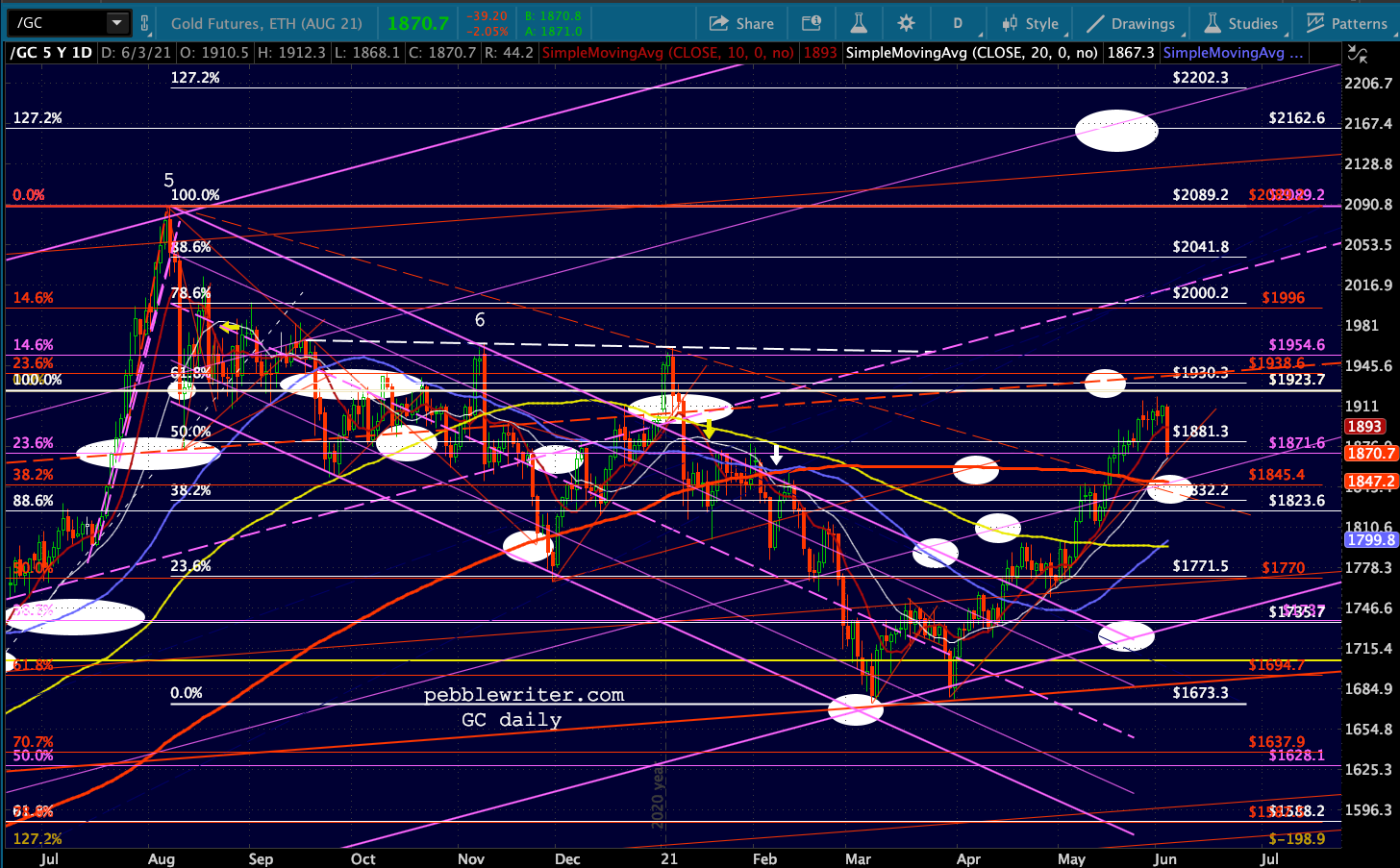

So, why are GC and SI getting whacked? Note that GC is testing a TL off its March lows and is likely to finally backtest its SMA200 after coming up just short of our .618 target.

SI is just plain getting creamed with a SMA200 backtest well below current levels.

SI is just plain getting creamed with a SMA200 backtest well below current levels.  There are three potential explanations:

There are three potential explanations:

- the correlation between ZN and GC is breaking down

- rates are about to move substantially higher

- the Fed is pressuring GC/SI lower in order to shape inflationary expectations

Tomorrow’s jobs report should help clarify things.