What a difference a week makes. I was hoping that taking a week off would see some semblance of sanity return to the markets. Apparently, that was too much to expect.

A week ago, the US dollar pairs had reached long-term objectives, SPX was running out of steam and VIX’s all-time low was set way back in 1993.

Today, the dollar is running for cover, SPX has broken out yet again, and VIX set new all-time lows — having spent all but 4 sessions of the past three months below the bottom of our long-term rising yellow channel. We’ll look at the repercussions of all the above, and what to expect next.

We’ll look at the repercussions of all the above, and what to expect next.

continued for members…First, the DXY has broken down below the purple channel midline as well as the falling white channel. If it doesn’t bounce at the upcoming .886 at 93.276, when it’s likely to test the 91.919 lows and the purple channel .236 line.

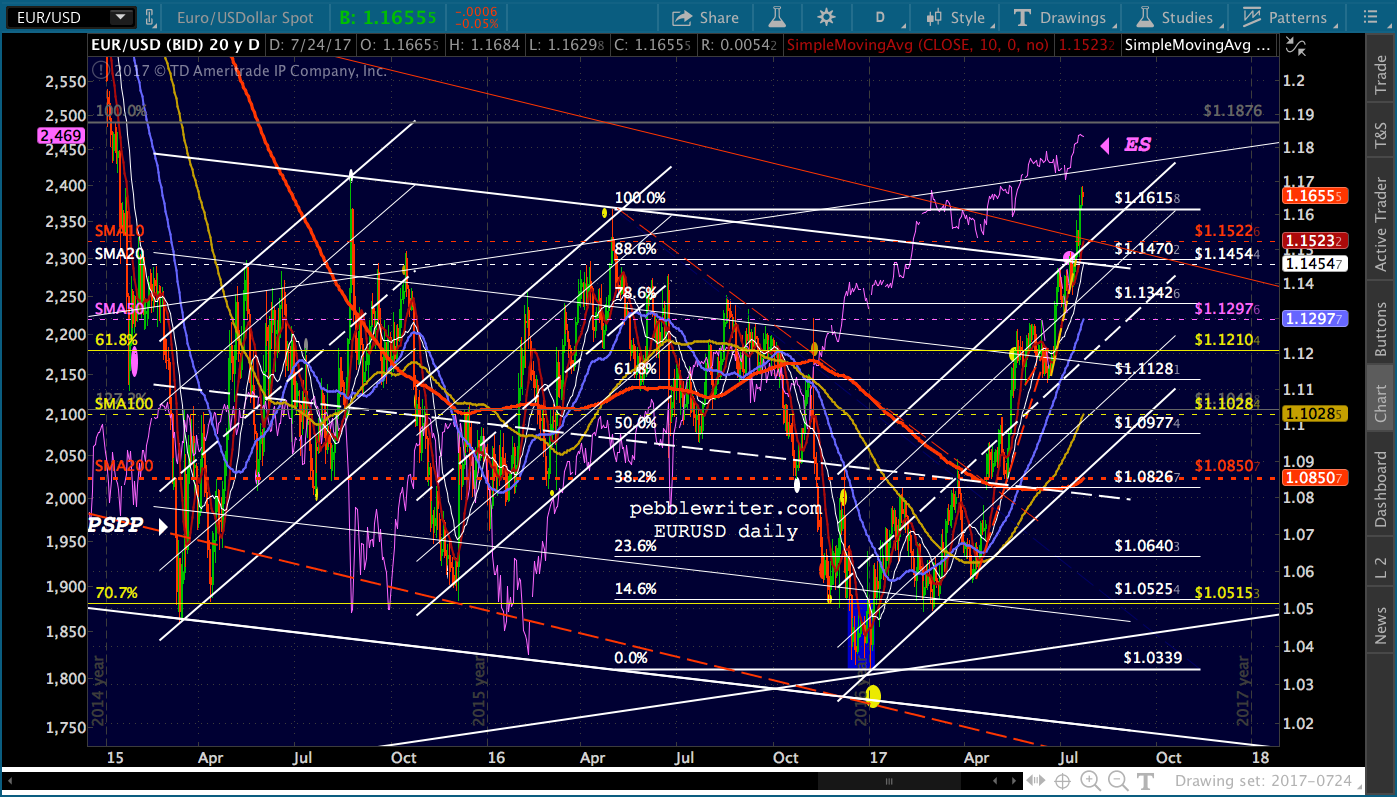

The culprit, of course, the euro — which has broken out above the falling white channel line and its 2016 highs and is testing the 2015 highs.

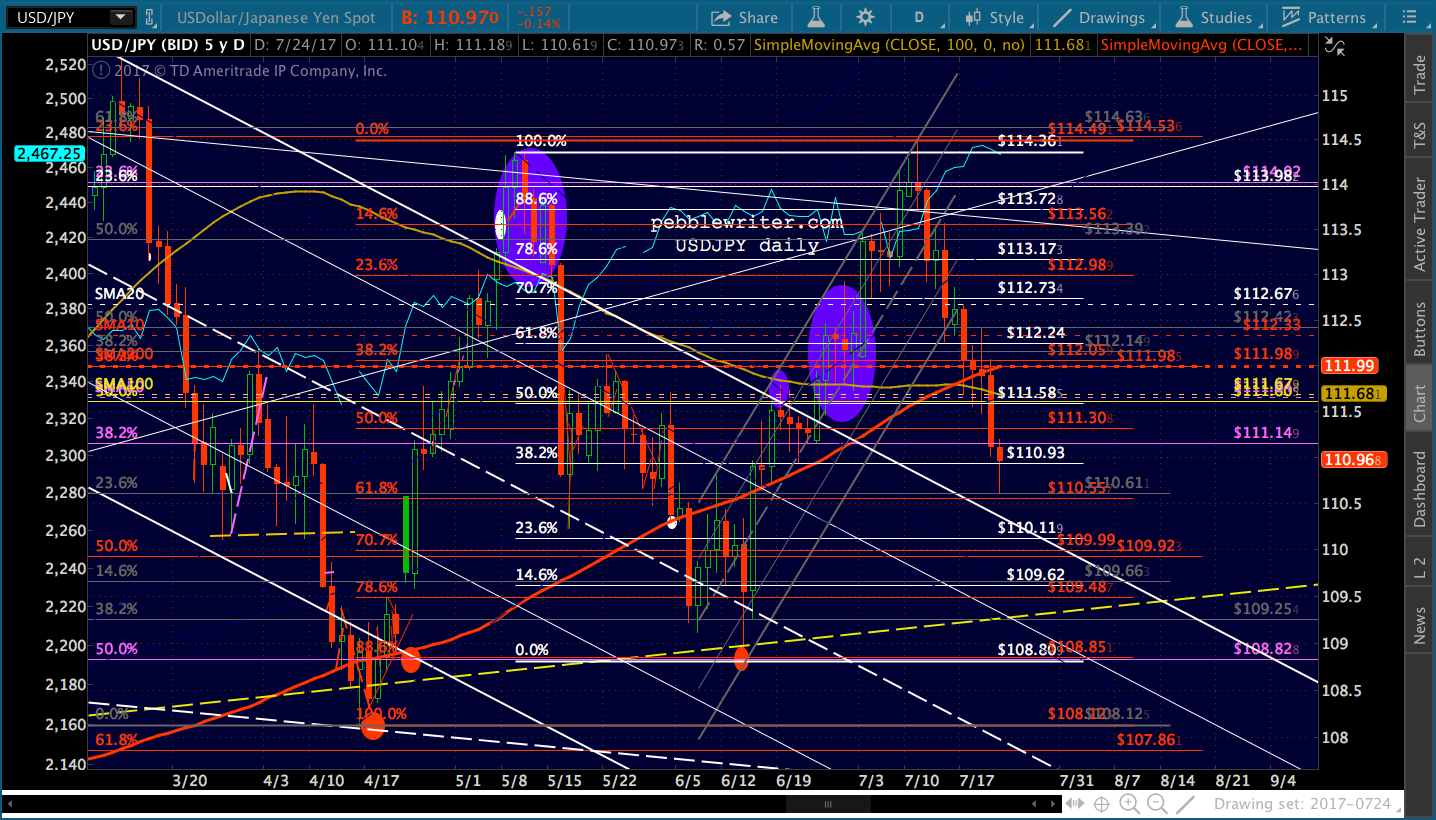

The culprit, of course, the euro — which has broken out above the falling white channel line and its 2016 highs and is testing the 2015 highs. This has also sent USDJPY plunging, with a backtest of the falling white channel quite likely.

This has also sent USDJPY plunging, with a backtest of the falling white channel quite likely.  All this might normally be expected to send stocks tumbling. But, the VIX has managed to keep it all afloat…

All this might normally be expected to send stocks tumbling. But, the VIX has managed to keep it all afloat… …producing new highs, instead.

…producing new highs, instead.

CL is minding its own business, still on track for our 49.82 objective.

CL is minding its own business, still on track for our 49.82 objective.  If it has truly backtested and will bounce off the purple .236 channel line and SMA20, and the DXY catches support at the .886 as described above, then VIX can bounce back to “normal” without affecting stocks too much.

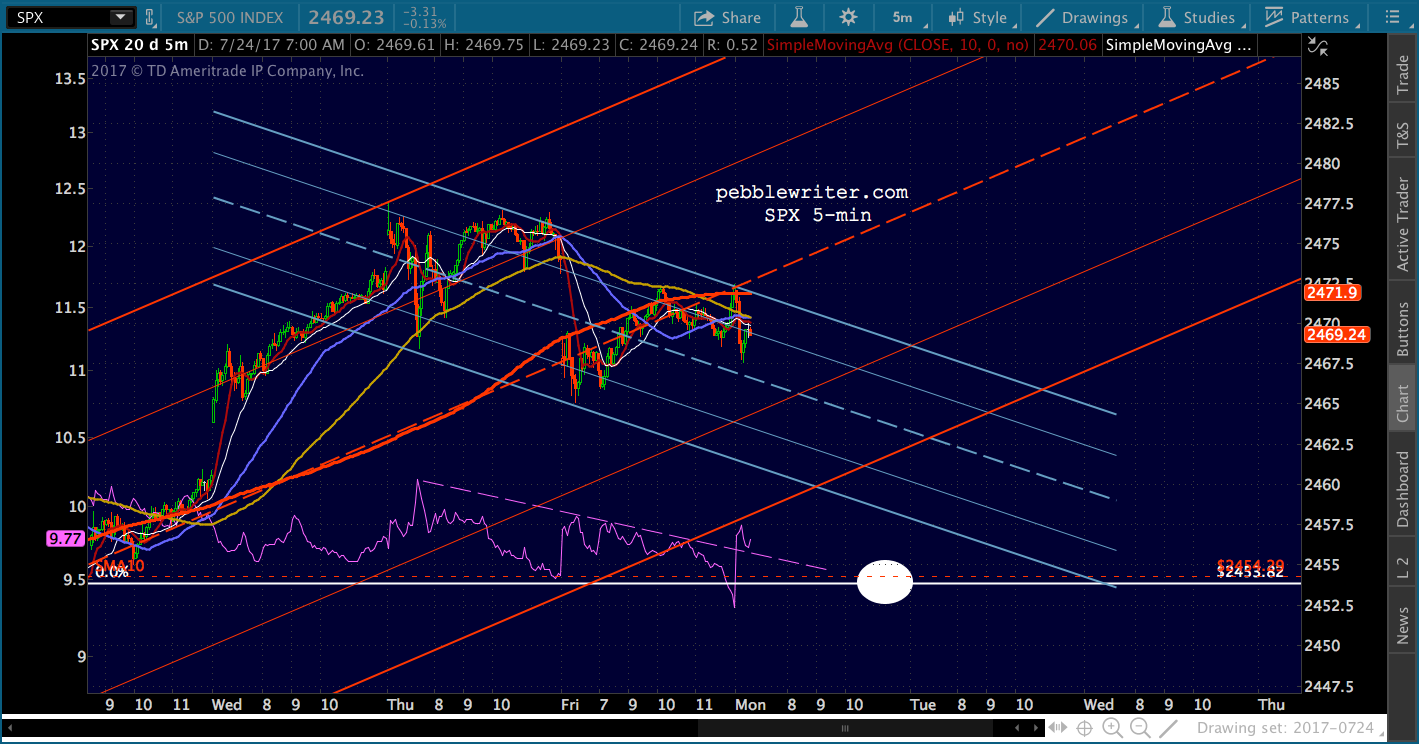

If it has truly backtested and will bounce off the purple .236 channel line and SMA20, and the DXY catches support at the .886 as described above, then VIX can bounce back to “normal” without affecting stocks too much.  But, a bounce in VIX without a recovery in the dollar or continuing bounce in CL would likely mean at least a backtest of the recent 2453.82 highs for SPX. Note that the SMA10 has reached 2454, meaning even a 23-pt drop could be taken as a positive. I’d want to be short going into today’s session.

But, a bounce in VIX without a recovery in the dollar or continuing bounce in CL would likely mean at least a backtest of the recent 2453.82 highs for SPX. Note that the SMA10 has reached 2454, meaning even a 23-pt drop could be taken as a positive. I’d want to be short going into today’s session.

The last two times USDJPY fell below its SMA200, SPX either dropped outright or at least flattened, threatening to roll over.  The dramatic recovery in mid-June prevented it. With USDJPY back below its SMA200, I suspect we’ll see it bounce on the white channel top and continue sideways, removing this particular headwind for stocks.

The dramatic recovery in mid-June prevented it. With USDJPY back below its SMA200, I suspect we’ll see it bounce on the white channel top and continue sideways, removing this particular headwind for stocks.

The small, falling purple channel which has set up over the last two sessions doesn’t reach 2454 for another day or two. But, by then, the SMA10 would up even higher. Thus, I think there’s a decent chance the decline will accelerate as today’s session unfolds. It’s worth considering the implications of a rise in CL concurrent with a drop in the value of the DXY. The most important is a rise in inflation, which lately has failed to match up with the Fed’s rate hike narrative.

It’s worth considering the implications of a rise in CL concurrent with a drop in the value of the DXY. The most important is a rise in inflation, which lately has failed to match up with the Fed’s rate hike narrative. As a result, the yield curve is looking more and more like one that signals an impending recession.

As a result, the yield curve is looking more and more like one that signals an impending recession.

What’s the Fed more concerned with: a recession or a market correction? At this point, I’d have to say a recession. There has been plenty of Fedspeak, lately, about exuberant markets that could use a little off the top.

The US can scarcely afford higher interest rates, but it can ill afford a recession. CPI is artificially suppressed via the reporting process (especially food and housing.) Higher oil prices will help to some extent, reinforcing my expectation for continued appreciation. A lower USD will also help, as the US is a net importer.

So, the Fed is in the impossible position of trying to increase “reported” inflation without affecting actual consumers. At the same time, they’d like to build a little more cushion into interest rates (for future QE) without leaving gov’t/corp interest expense at a level which would decimate the economy and without increasing the USD to a level which works against their inflation goals.

The next few days/weeks will hopefully provide some clarity.

More later.