It was Mar 23, 2020. The COVID pandemic had scared the crap out of markets. The S&P 500 had dropped 35% in about a month and, to make things worse, a dreaded death cross was only 50 points away.

Death crosses, where the 50-day moving average drops below the 200-day, are well known to investors – technicians or not.They often usher in dramatically lower prices such as in 2007-2009 when SPX shed 54%.

Death crosses, where the 50-day moving average drops below the 200-day, are well known to investors – technicians or not.They often usher in dramatically lower prices such as in 2007-2009 when SPX shed 54%.

On Mar 23, 2020, SPX’s approaching death cross promised to add to the pain already experienced by markets roiled by the pandemic. The Trump administration, which had badly fumbled its public health response with such brilliant advice as injecting bleach, was paying much more attention to the stock market than the health crisis.

Congress and the Fed sat on their hands as Trump press conferences and tweets were increasingly frantic. Finally, with the Dow back to the lows last experienced on election night 2016, the market bottomed in response to a concerted effort to prop up stocks.

It started in the after-hours on a Sunday night with a press release by Treasury secretary Mnuchin that promised $4 trillion in financial stimulus. The Dow gapped higher, closing +13.4% off its Friday lows. The S&P 500 gained almost 12%.

It started in the after-hours on a Sunday night with a press release by Treasury secretary Mnuchin that promised $4 trillion in financial stimulus. The Dow gapped higher, closing +13.4% off its Friday lows. The S&P 500 gained almost 12%.

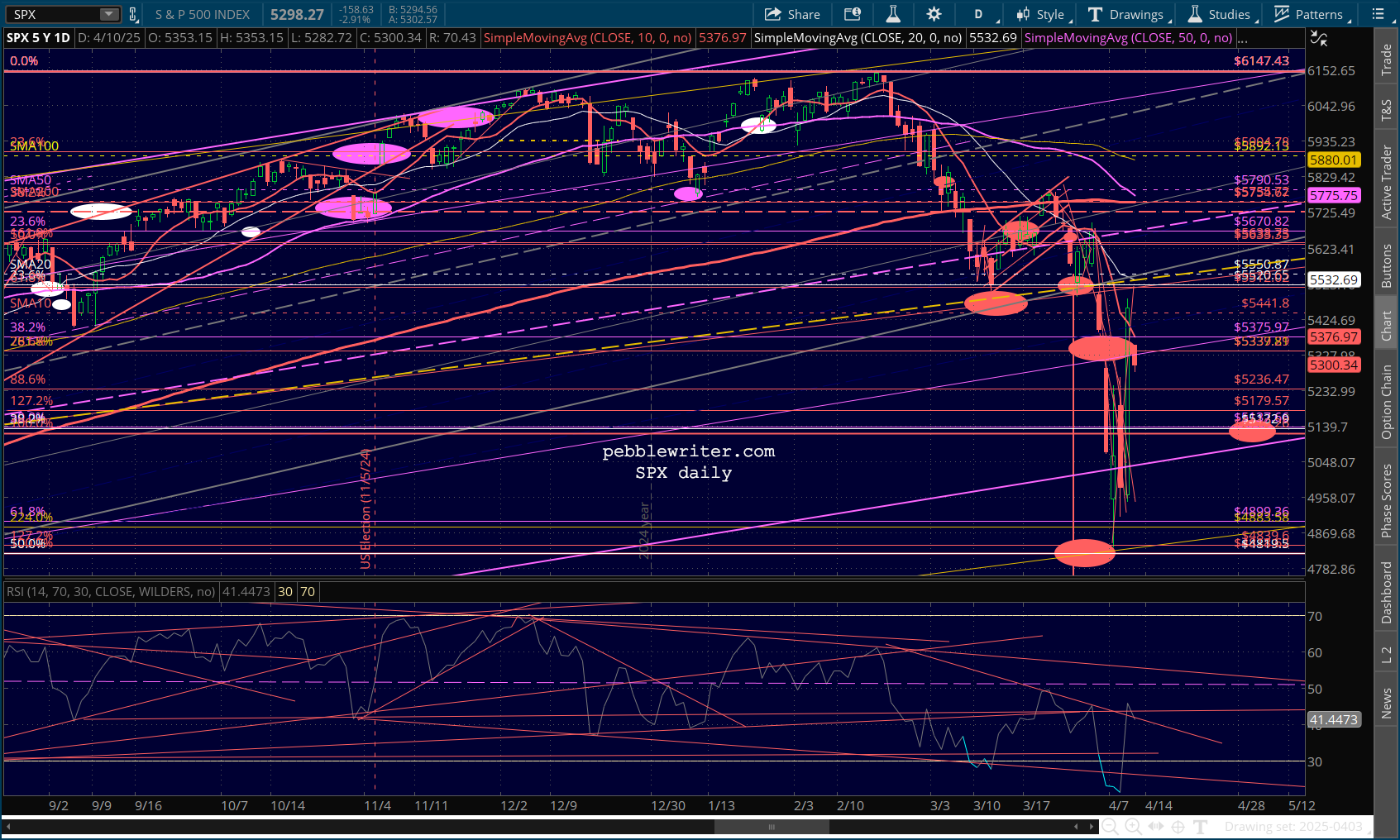

By the time the death cross occurred on the 27th, SPX had rebounded a stunning 20%. It was a remarkable rally that any active investor will remember well. Many of us were reminded of it yesterday when the S&P 500, which had already dropped more than 20% from recent highs (the definition of a bear market) was so close to completing another death cross.

I imagine there were very few active investors who weren’t thinking about the death cross, with many of them recalling the 2020 incident and some of us anticipating a repeat. As we wrote yesterday:

Note that SPX/SPY are about to experience a death cross – where the SMA50 drops below the SMA200. In a manipulated stock market such as we have, this is often a point at which the manipulators jump in to avoid the downside such a move entails.

It came as little surprise yesterday when Trump announced that he was going to pause some of the tariffs which had set the financial world on fire last week. Oh, and it would be nice if investors would thank him for putting out the fire that he set.

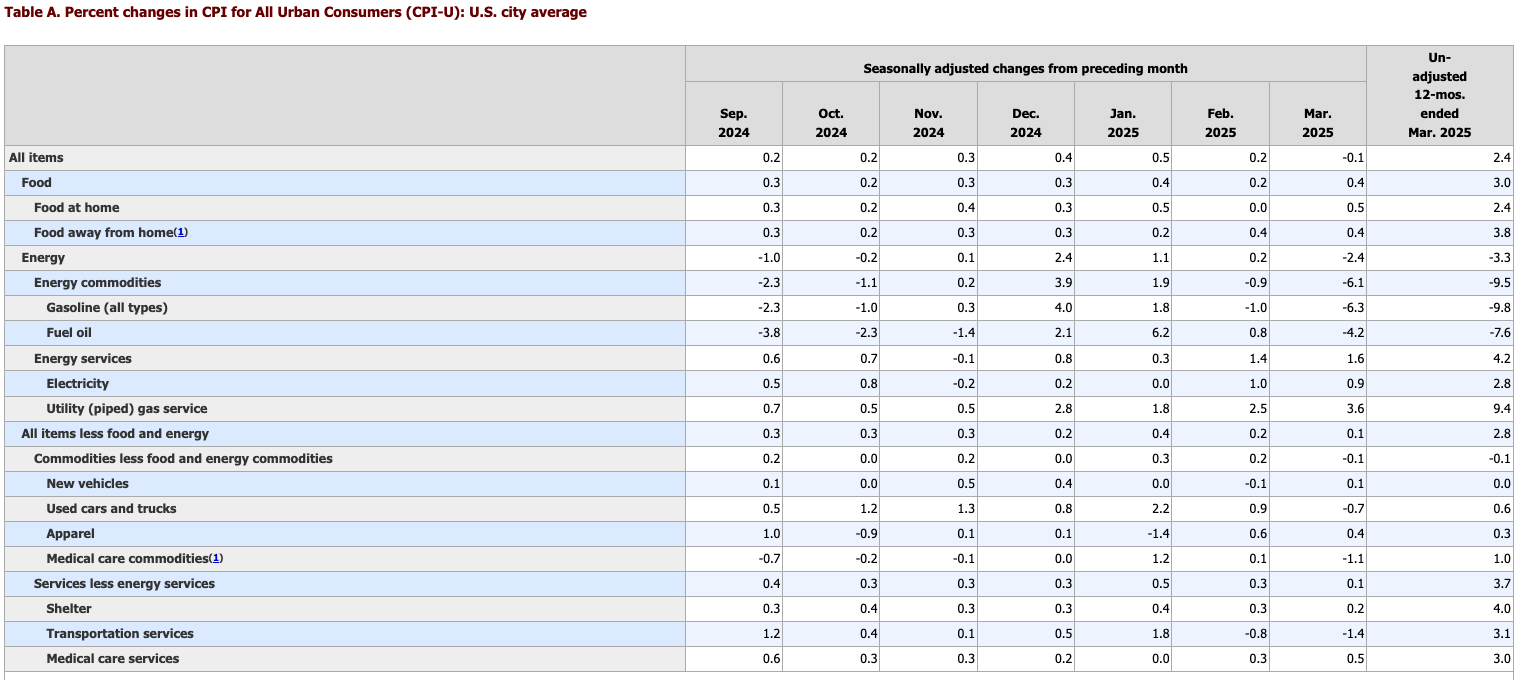

Only, the fire isn’t out. Despite March’s rather tame CPI print released this morning, the tariffs still in place will undoubtedly increase inflation. Despite the phalanx of foreign trade representatives supposedly lining up to kiss Trump’s ass, the average effective US tariff rate is still over 25%.

As we’ve pointed out many times, tariffs are a tax on the American people. They are also regressive, affecting lower income Americans more than the wealthy Americans who will benefit most from the $2 trillion in tax cuts theoretically financed by tariff income (with assistance from $880 billion in Medicaid cuts.)

It’s such an outrageous “steal from the poor and give to the rich” scheme that Republicans can’t figure out how to sell it to their constituents who are increasingly alarmed. Give the American people credit for recognizing the coming wave of inflation (and bothering to read their 401(k) statements.)

Speaking of which, it seems at least a few investors have noticed that the tariff fire is still smoldering. Futures are off almost 2%.

continued for members…

continued for members…

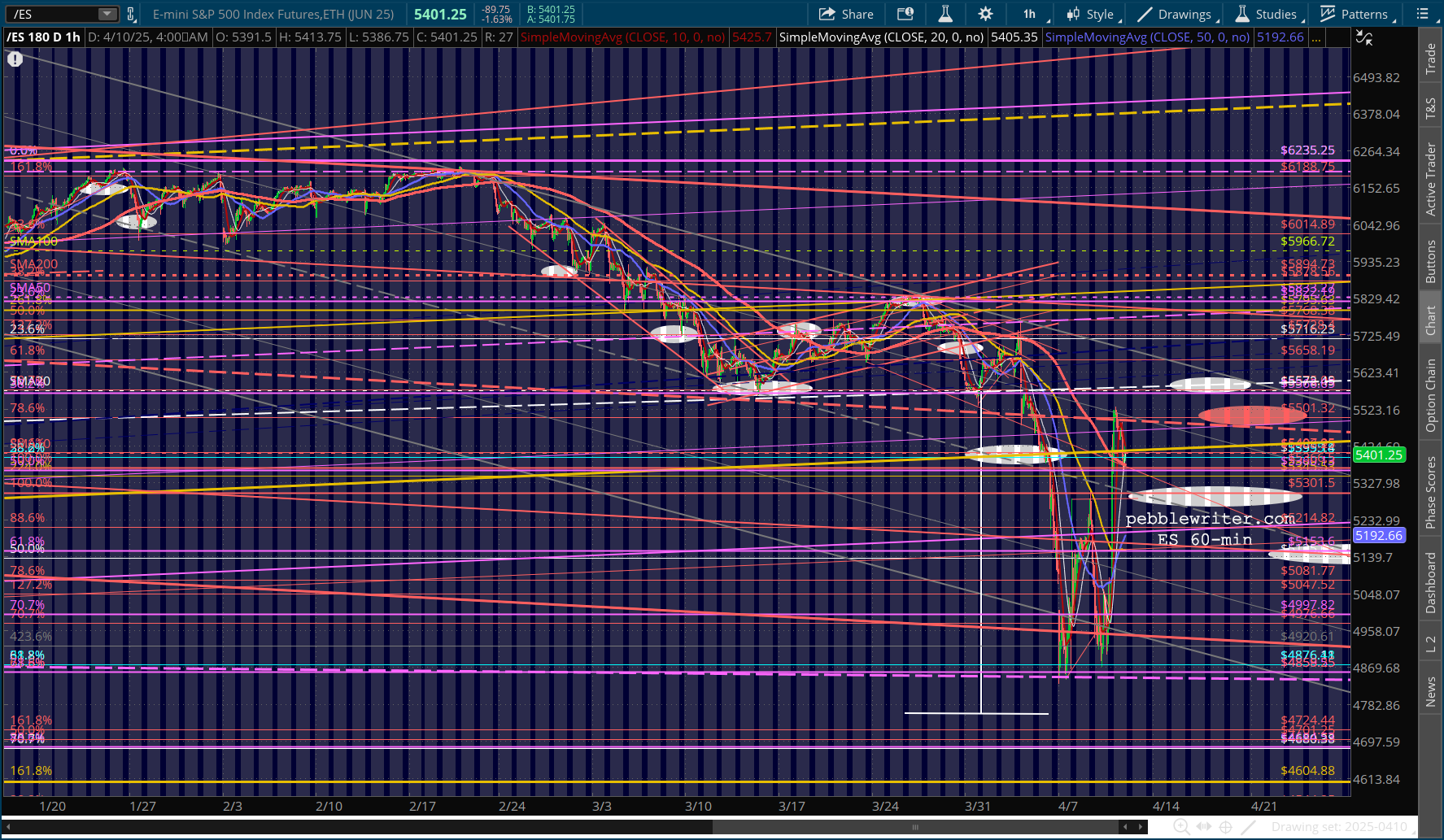

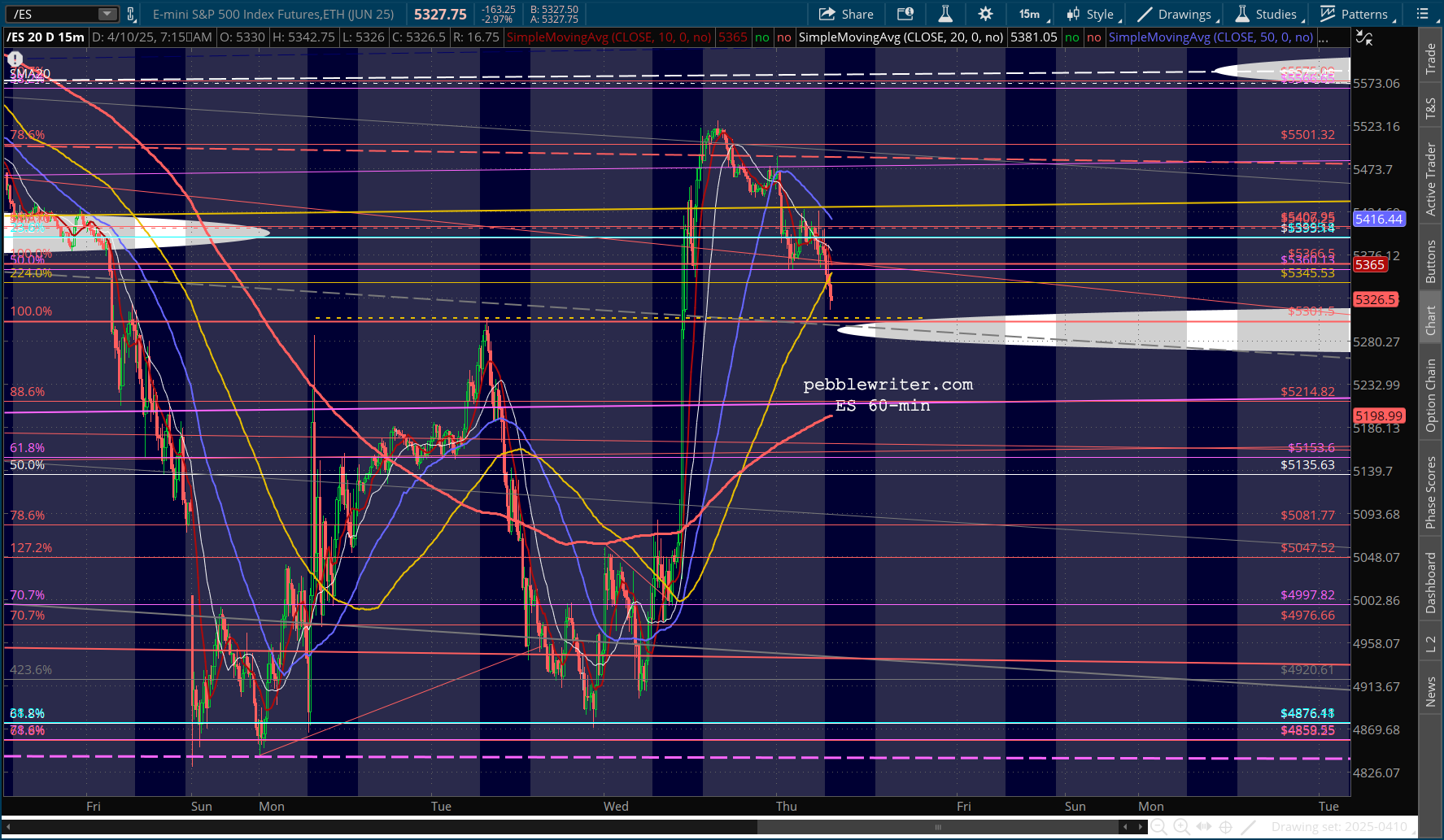

There are still a few technical issues that could bother the algos. ES has already experienced a death cross. It is approaching yesterday’s highs at 5305.25, which bulls would theorize represents support – the wave 1 high that a wave 4 decline shouldn’t drop below.

It is approaching yesterday’s highs at 5305.25, which bulls would theorize represents support – the wave 1 high that a wave 4 decline shouldn’t drop below.

The gap at SPX 5390 from Apr 3 has obviously been closed, but SPX remains below its SMA10, which is still falling.

The gap at SPX 5390 from Apr 3 has obviously been closed, but SPX remains below its SMA10, which is still falling.

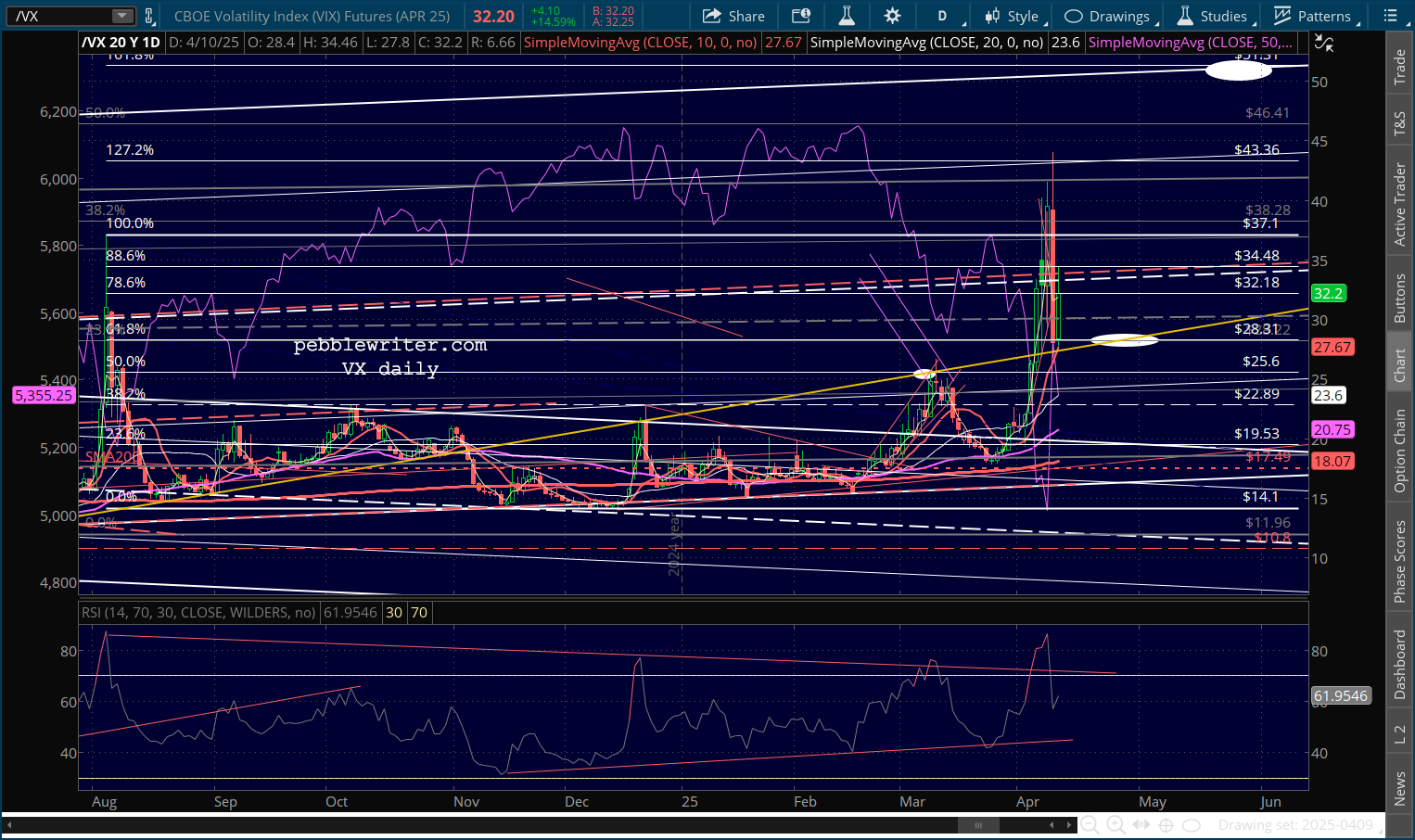

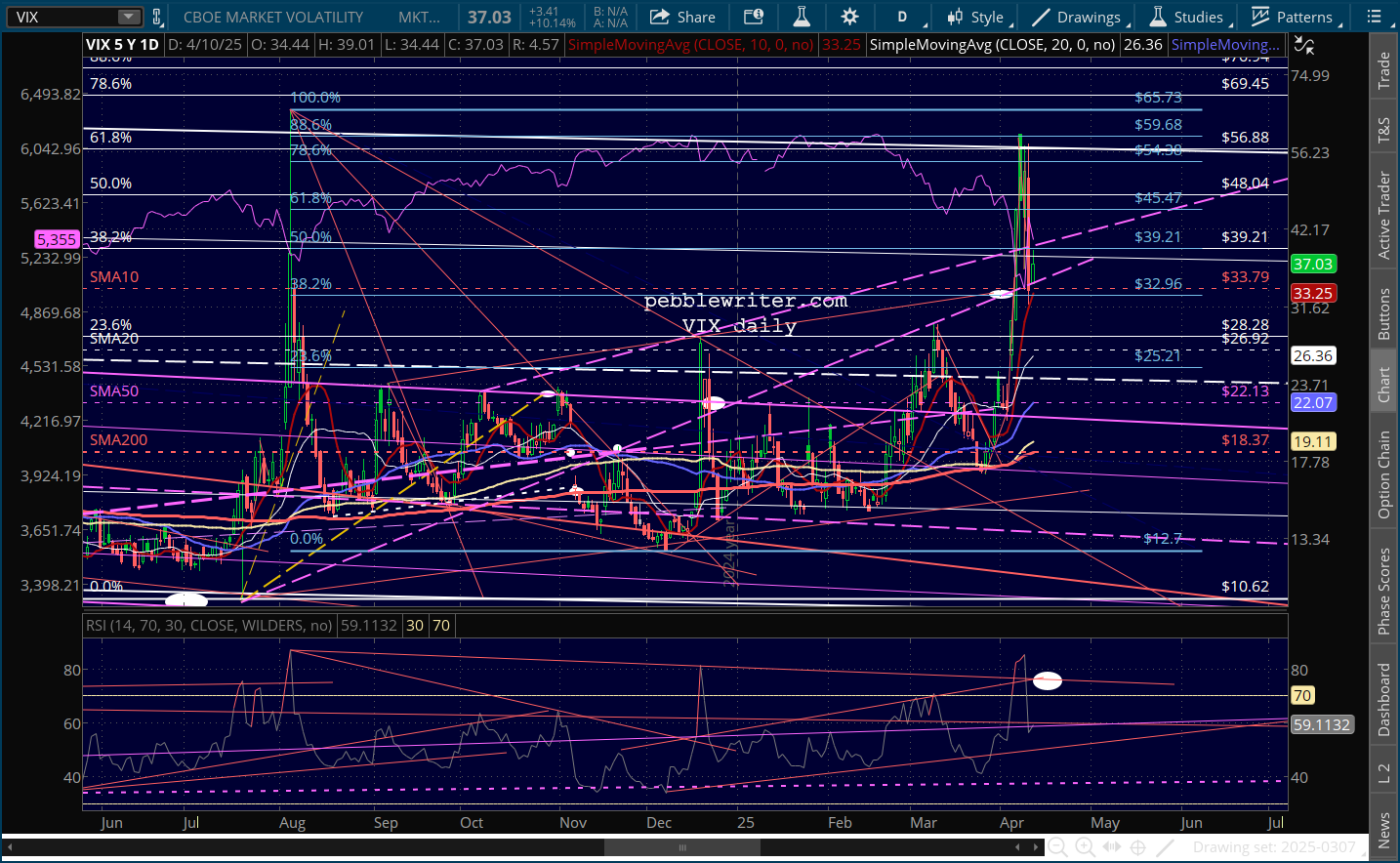

VIX and VX are no longer overbought, but they are currently bouncing off TL support.

VIX and VX are no longer overbought, but they are currently bouncing off TL support.

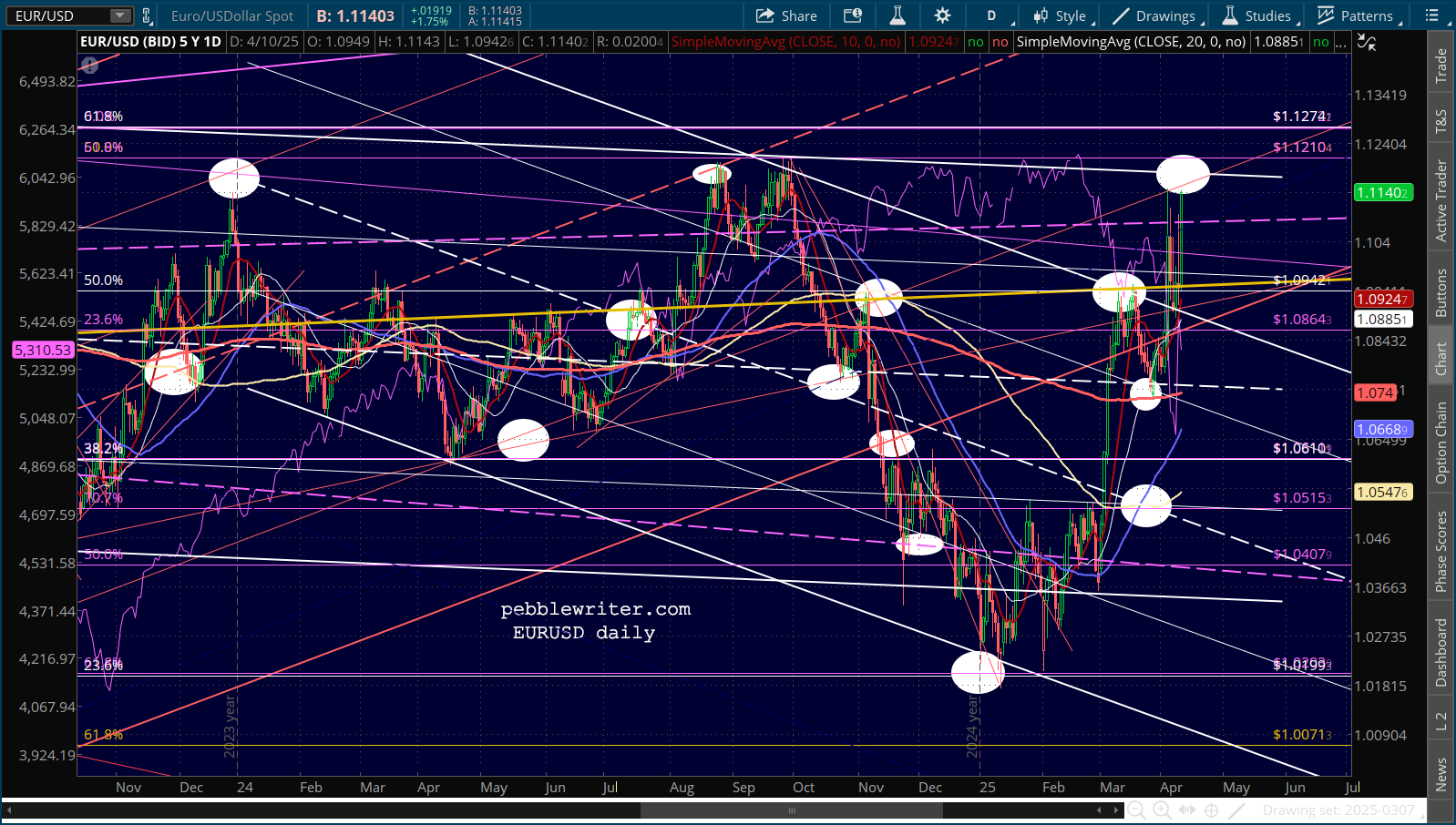

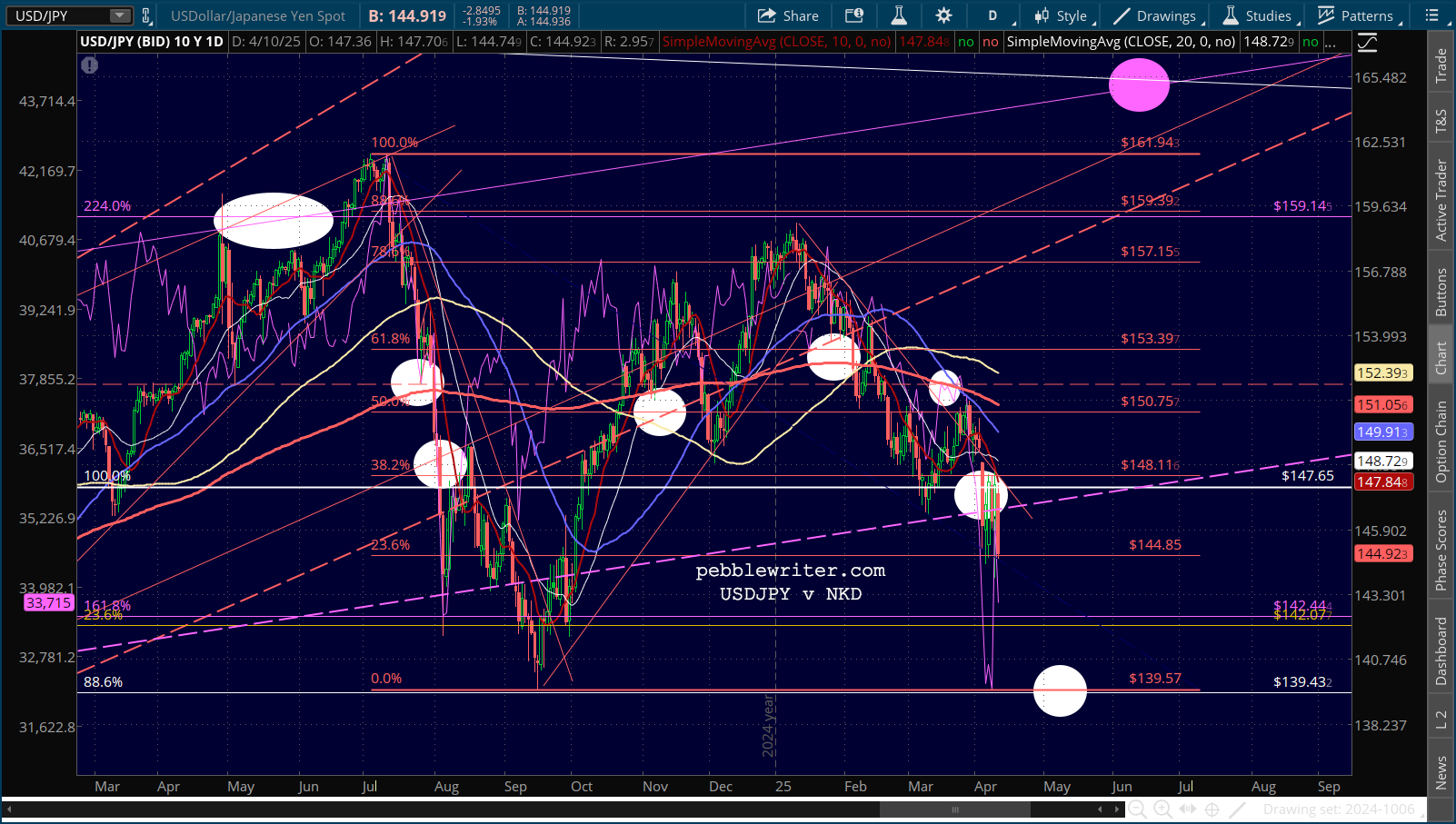

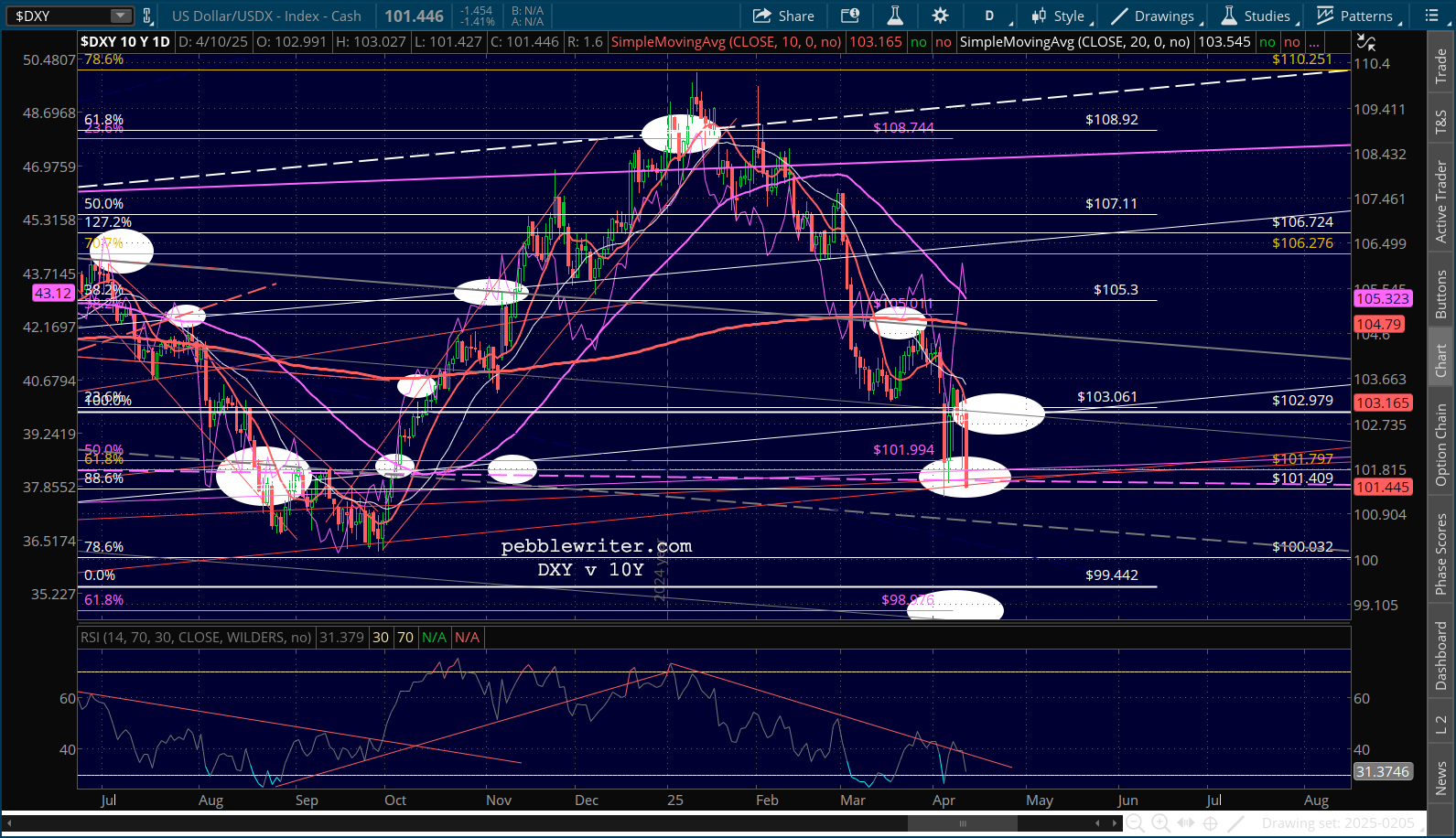

The USD is still under pressure, with the yen gaining the kind of strength it usually does when equities are tumbling.

The USD is still under pressure, with the yen gaining the kind of strength it usually does when equities are tumbling.

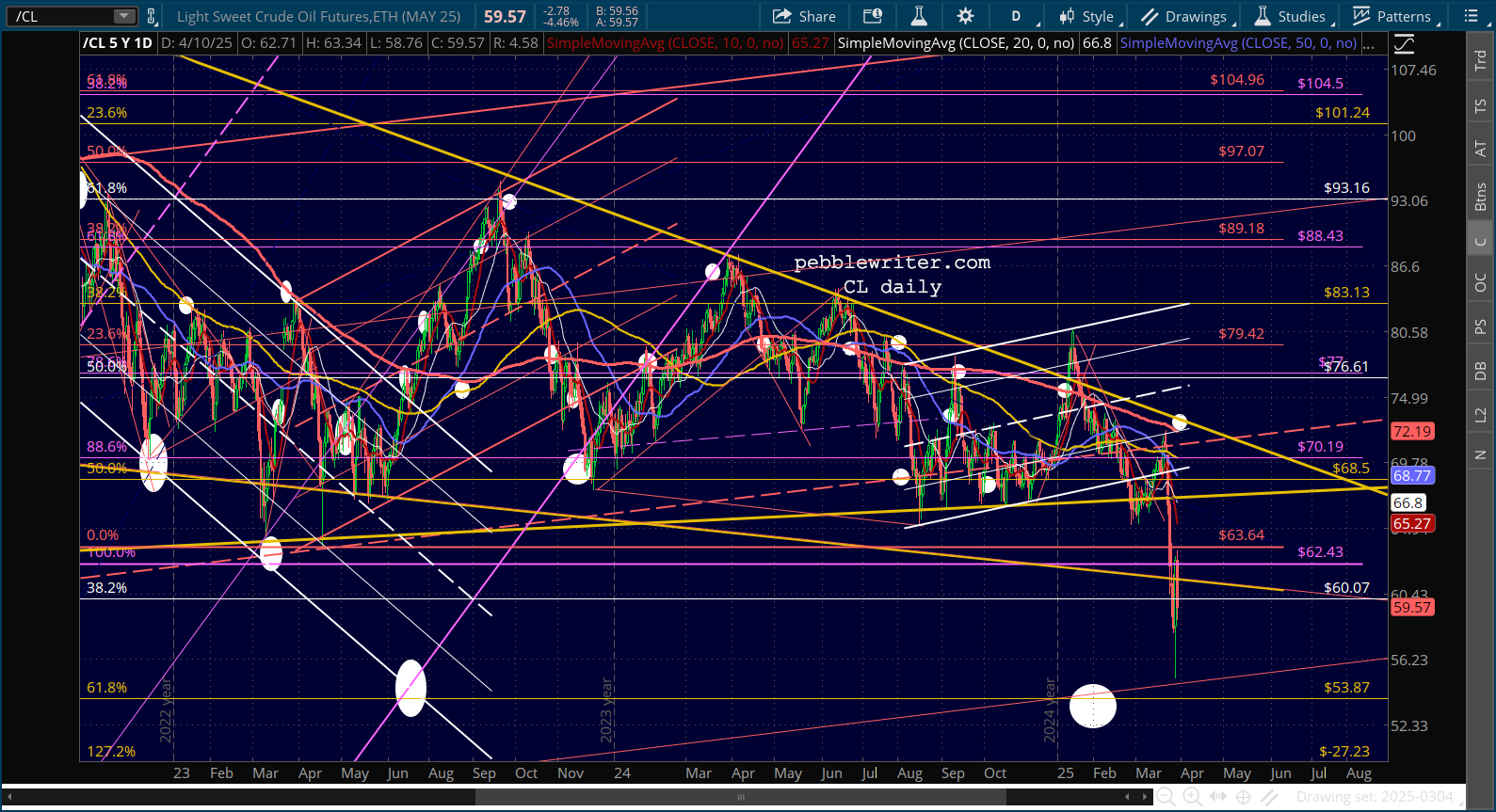

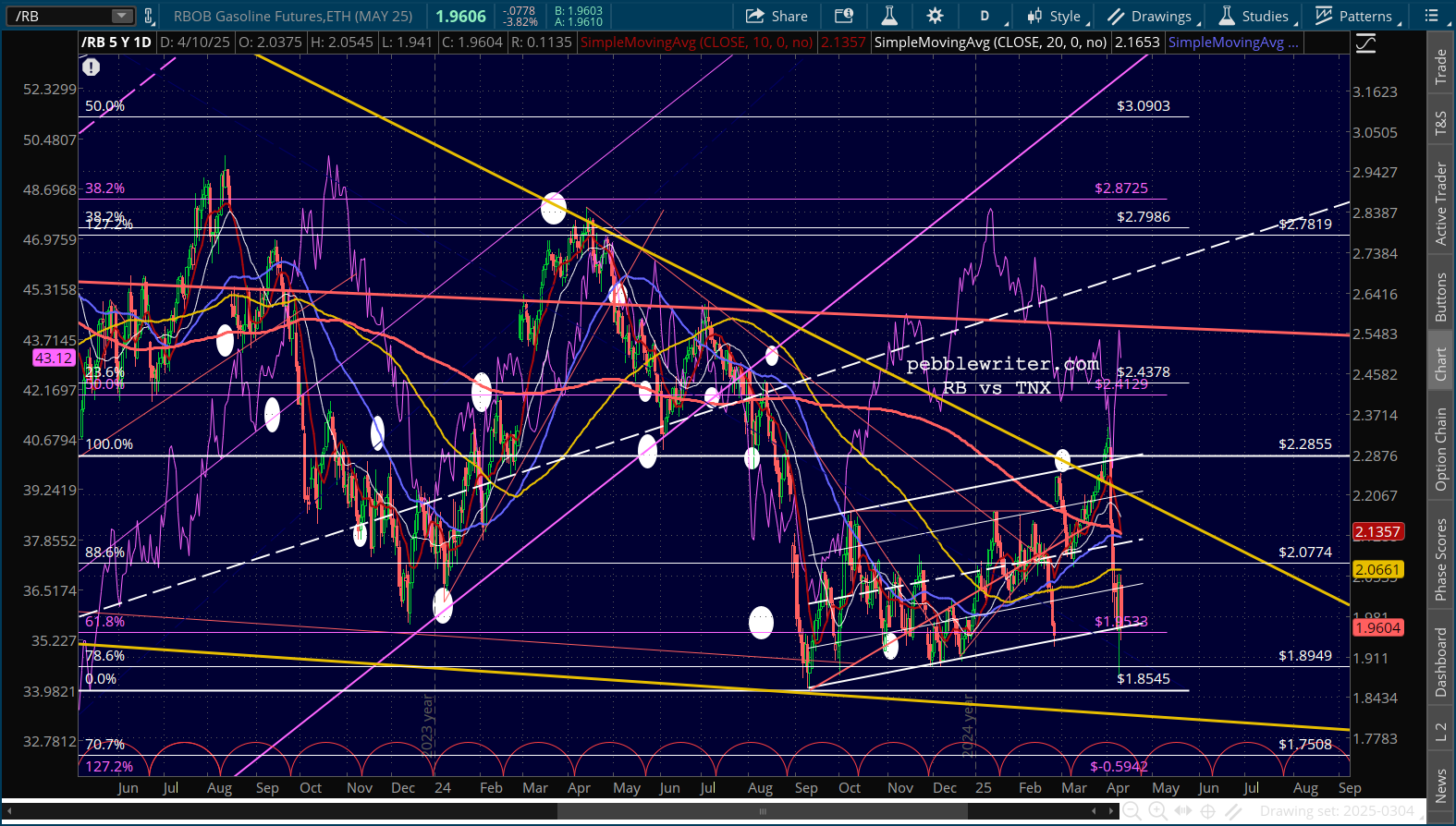

And, although CL and RB are bouncing nicely, this rebound won’t help tamp down inflation…

And, although CL and RB are bouncing nicely, this rebound won’t help tamp down inflation…

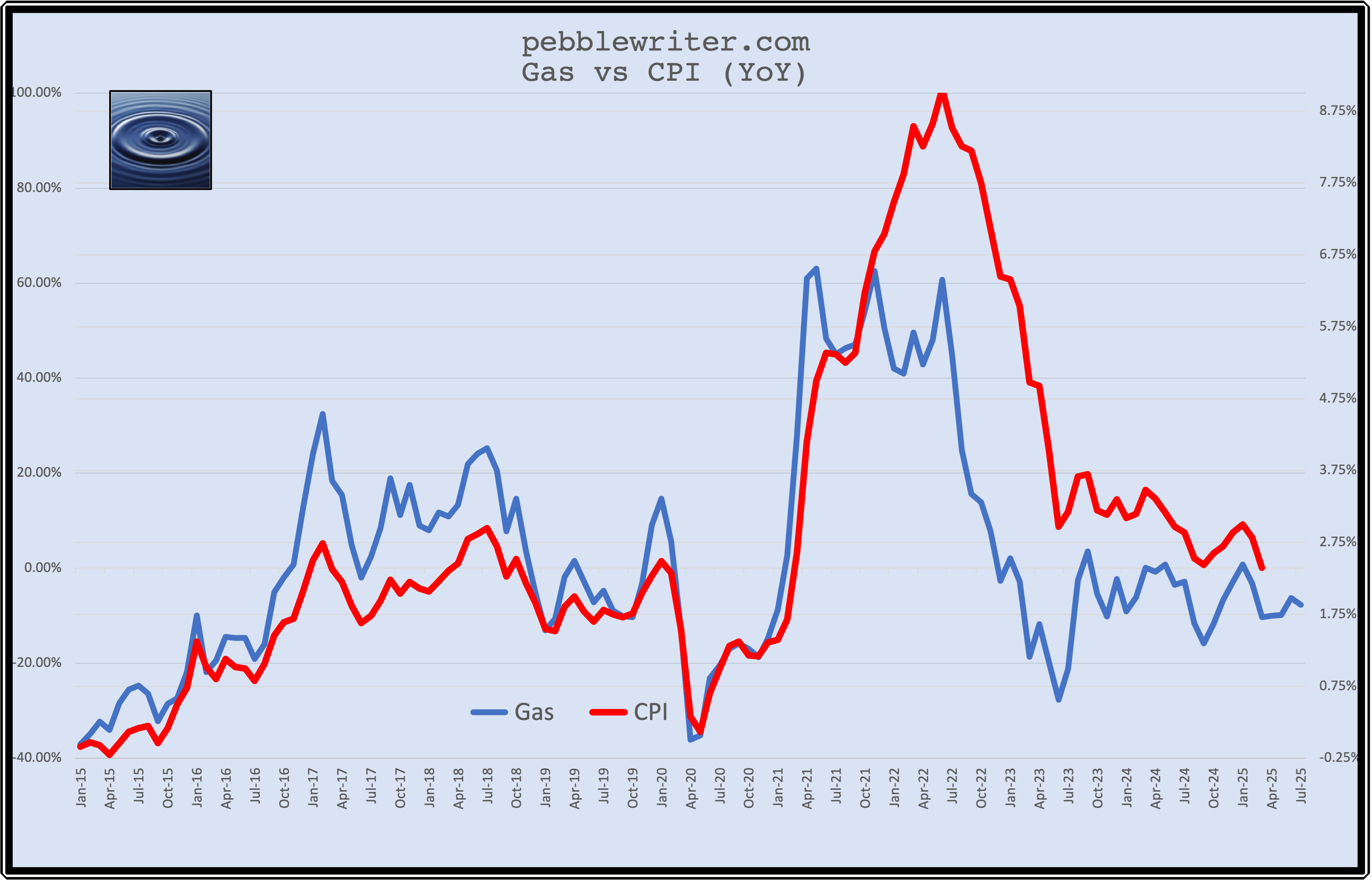

…as it did last month.

…as it did last month.

The effects of gas’ YoY decline are already waning, with a 4.7% increase indicated over March’s levels before this rebound.

The effects of gas’ YoY decline are already waning, with a 4.7% increase indicated over March’s levels before this rebound.

Combined with tariff-induced inflation, it’s not surprising that the 10Y’s increase shows positive divergence from oil/gas prices.

Combined with tariff-induced inflation, it’s not surprising that the 10Y’s increase shows positive divergence from oil/gas prices.

As we’ve discussed before, China is selling treasuries. Japan probably is, too.

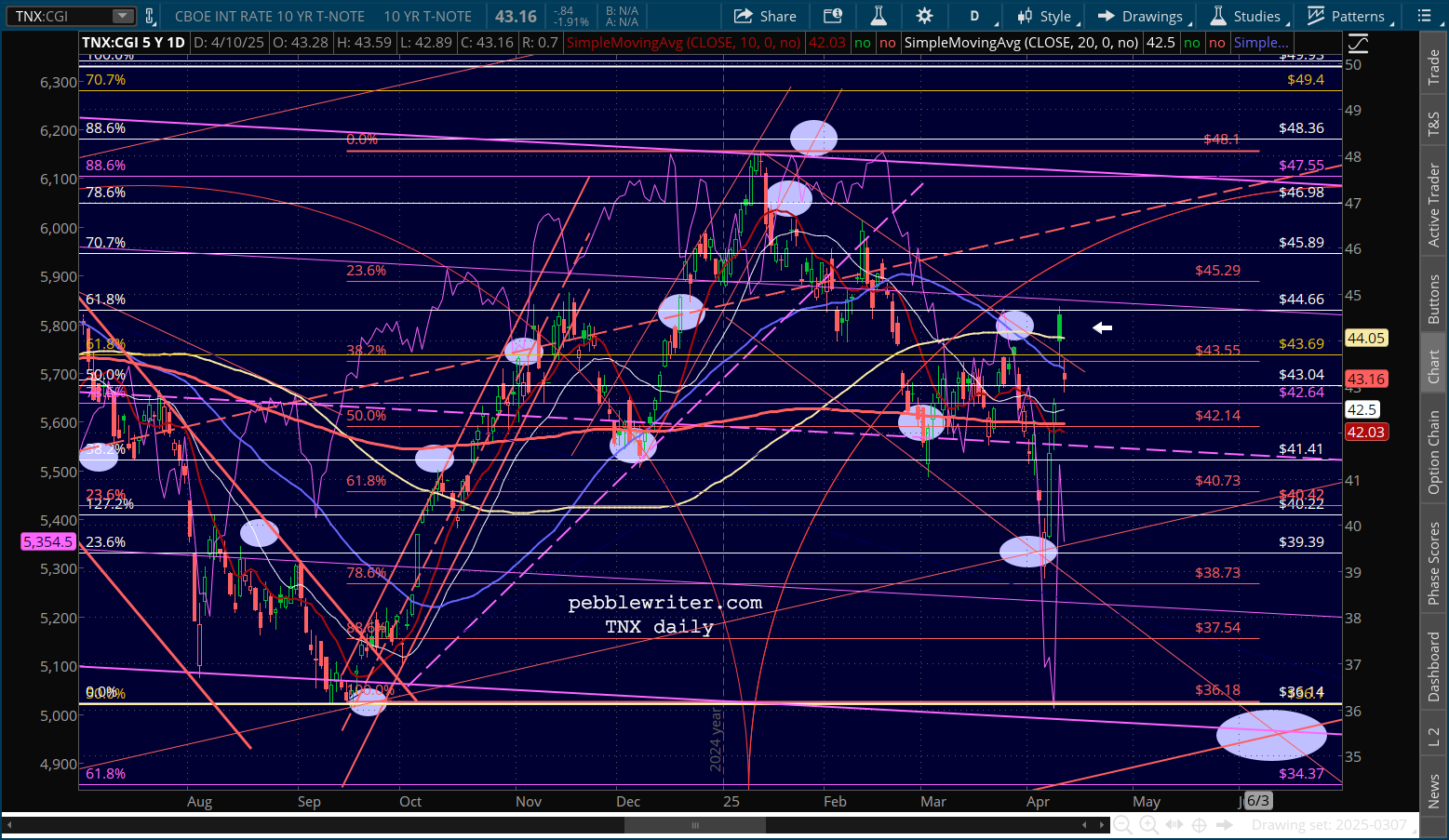

Although TNX’s breakout has abated, it’s still elevated considering that CPI is printing lower. Inflation expectations sure don’t help.

Although TNX’s breakout has abated, it’s still elevated considering that CPI is printing lower. Inflation expectations sure don’t help.

Bottom line, the market is hardly out of the woods. If SPX can’t remain above 5267 (ES 5305) we still have a very good chance of reaching SPX 4,506. We still have a 145% tariff in place against China. Stay frosty.