As enjoyable as it is filling up the Family Truckster for only $2.36/gallon, what if it meant the the death of thousands of Kurds? Here’s what we know.

For months, OPEC ignored Trump’s demands to bring down the price of oil. Trump was correctly concerned that spiking oil prices would push inflation to new highs (they did) and thus cause interest rates to reach unsustainable levels (they did.)

Trump’s tweets began in April…

Looks like OPEC is at it again. With record amounts of Oil all over the place, including the fully loaded ships at sea, Oil prices are artificially Very High! No good and will not be accepted!

— Donald J. Trump (@realDonaldTrump) April 20, 2018

…but, oil prices continued to climb until October 3 — which just happened to be the very day headlines proclaimed that Jamal Khashoggi was murdered in the Saudi embassy in Turkey, presumably at the direction of Saudi Crown Prince Mohammad bin Salman.

Since October 3, oil prices have dropped over 40%. Coincidence?

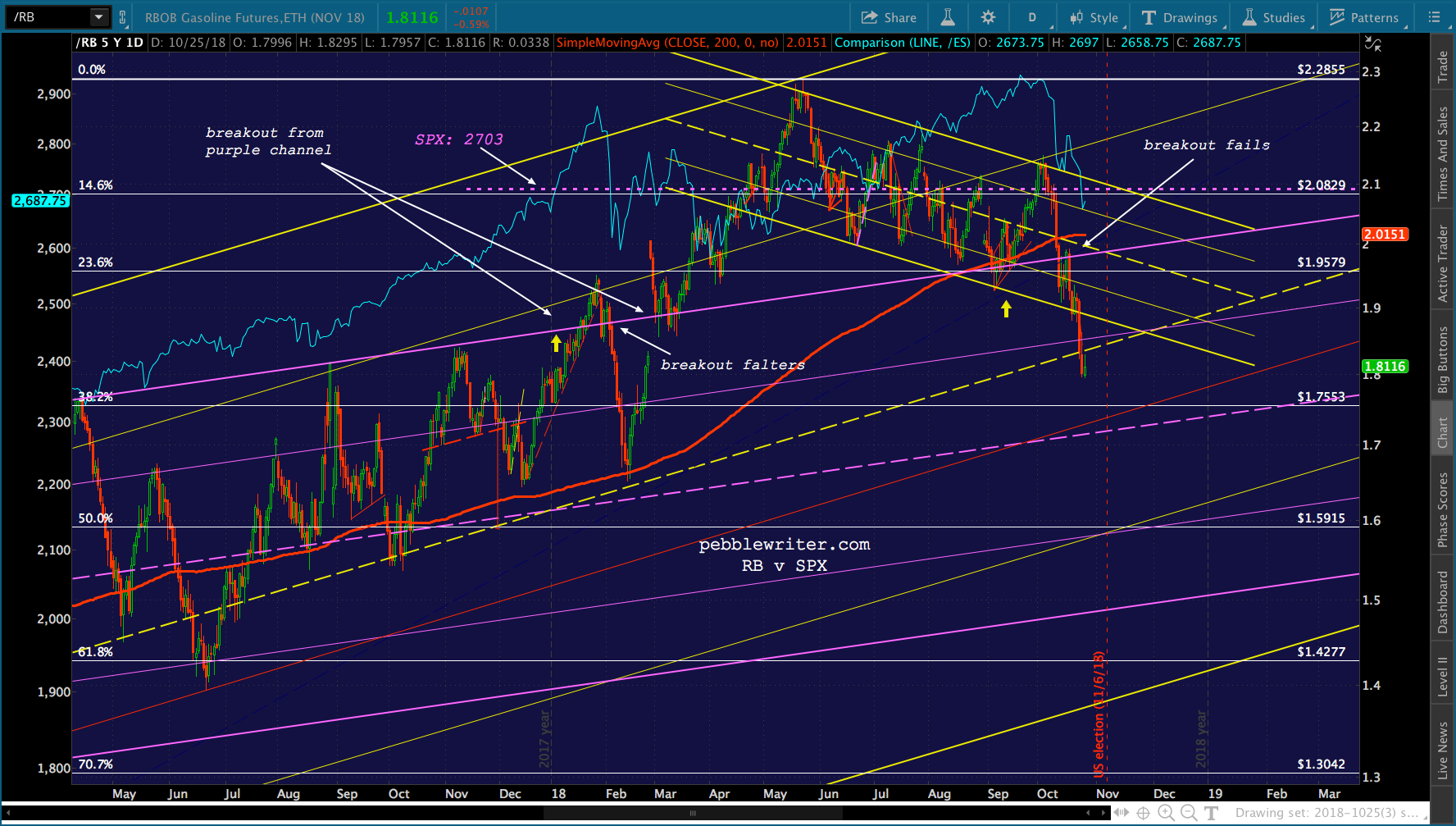

We commented back in October about the connection [see: Coincidences and Consequences] and speculated that it would finally give Trump the leverage he needed to force oil and gas prices lower.

We commented back in October about the connection [see: Coincidences and Consequences] and speculated that it would finally give Trump the leverage he needed to force oil and gas prices lower.

Condemnation of Saudi Crown Prince Mohammad bin Salman was nearly universal. The lone holdout/apologist? Donald Trump. Highlights from his statement:

…the Kingdom agreed to spend and invest $450 billion in the United States…it could very well be that the Crown Prince had knowledge of this tragic event – maybe he did and maybe he didn’t! King Salman and Crown Prince Mohammad bin Salman vigorously deny any knowledge of the planning or execution of the murder..we may never know all of the facts surrounding the murder of Mr. Jamal Khashoggi. The United States intends to remain a steadfast partner of Saudi Arabia…

It’s not much of a leap to conclude that the price for Trump’s equivocation was a big decline in the price of oil. CPI, which reached 2.95% in July, came in at only 2.18% in November. In December, it will likely return to below 2% as the YoY delta in gasoline prices turns negative.

The 10-year treasury, which topped out at 3.25% on Oct 5, is back down to 2.75%. The Fed is under renewed pressure to scrap plans for additional rate hikes. Mission accomplished. But, there was one thread which threatened to unravel the whole deal.

The 10-year treasury, which topped out at 3.25% on Oct 5, is back down to 2.75%. The Fed is under renewed pressure to scrap plans for additional rate hikes. Mission accomplished. But, there was one thread which threatened to unravel the whole deal.

According to Turkish President Recep Erdoğan, recordings of the entire incident were shared with the US, the UK, France, Germany and Saudi Arabia. He specifically mentioned providing a copy to Secretary Pompeo and to the CIA, which shortly afterwards concluded that MBS was behind the killing.

According to Turkish President Recep Erdoğan, recordings of the entire incident were shared with the US, the UK, France, Germany and Saudi Arabia. He specifically mentioned providing a copy to Secretary Pompeo and to the CIA, which shortly afterwards concluded that MBS was behind the killing.

Caught between a rock and a hard place, how could Trump convince Erdoğan to refrain from publicly releasing the recordings? Apparently after deciding that handing over Gulen would be a little too repugnant, even for Trump, he handed them an even bigger prize.

Without US troops at their side, most observers believe the Kurds in Northern Syria will be easy prey for Erdoğan. He has graciously agreed to postpone the massacre.

Without US troops at their side, most observers believe the Kurds in Northern Syria will be easy prey for Erdoğan. He has graciously agreed to postpone the massacre.