We’ve had a 4.75% target for the 10Y for almost 2 years – reasoning that the breakout in oil/gas prices would eventually force inflation and interest rates higher [see: The 10Y Breaks Out] and equity prices lower.

Sure, the Fed was able to postpone it with the usual misleading jawboning. But, the bill has finally come due.

Higher interest rates, coupled with high energy, housing, and grocery bills and the resumption of student loan payments, present a considerable challenge to the American consumer and economy alike.

Now that the 10Y has reached our target, what does the future hold?

Can the damage to stocks be limited to just a backtest of the 200-day moving average?

Can the damage to stocks be limited to just a backtest of the 200-day moving average? continued for members…

continued for members…

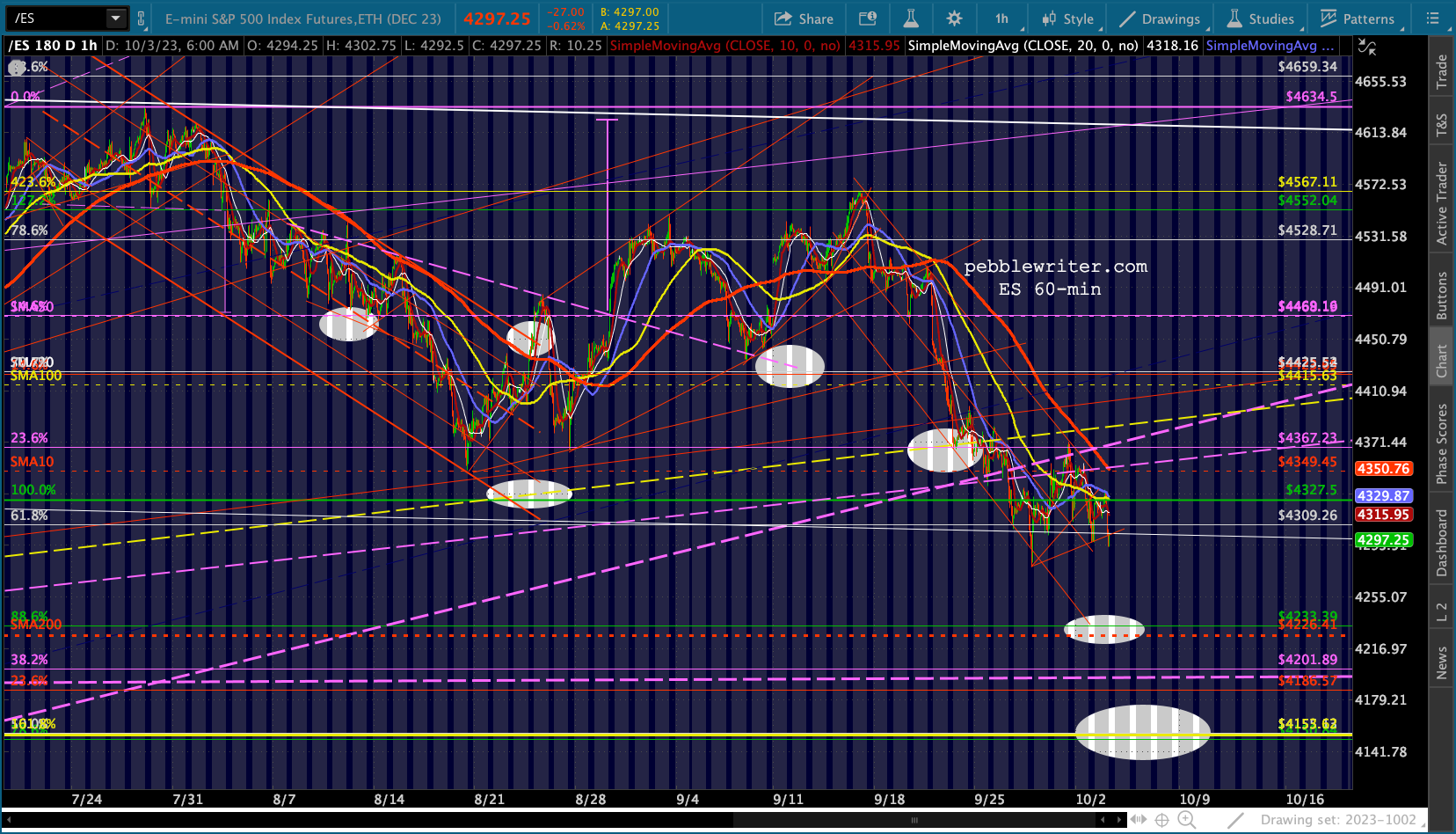

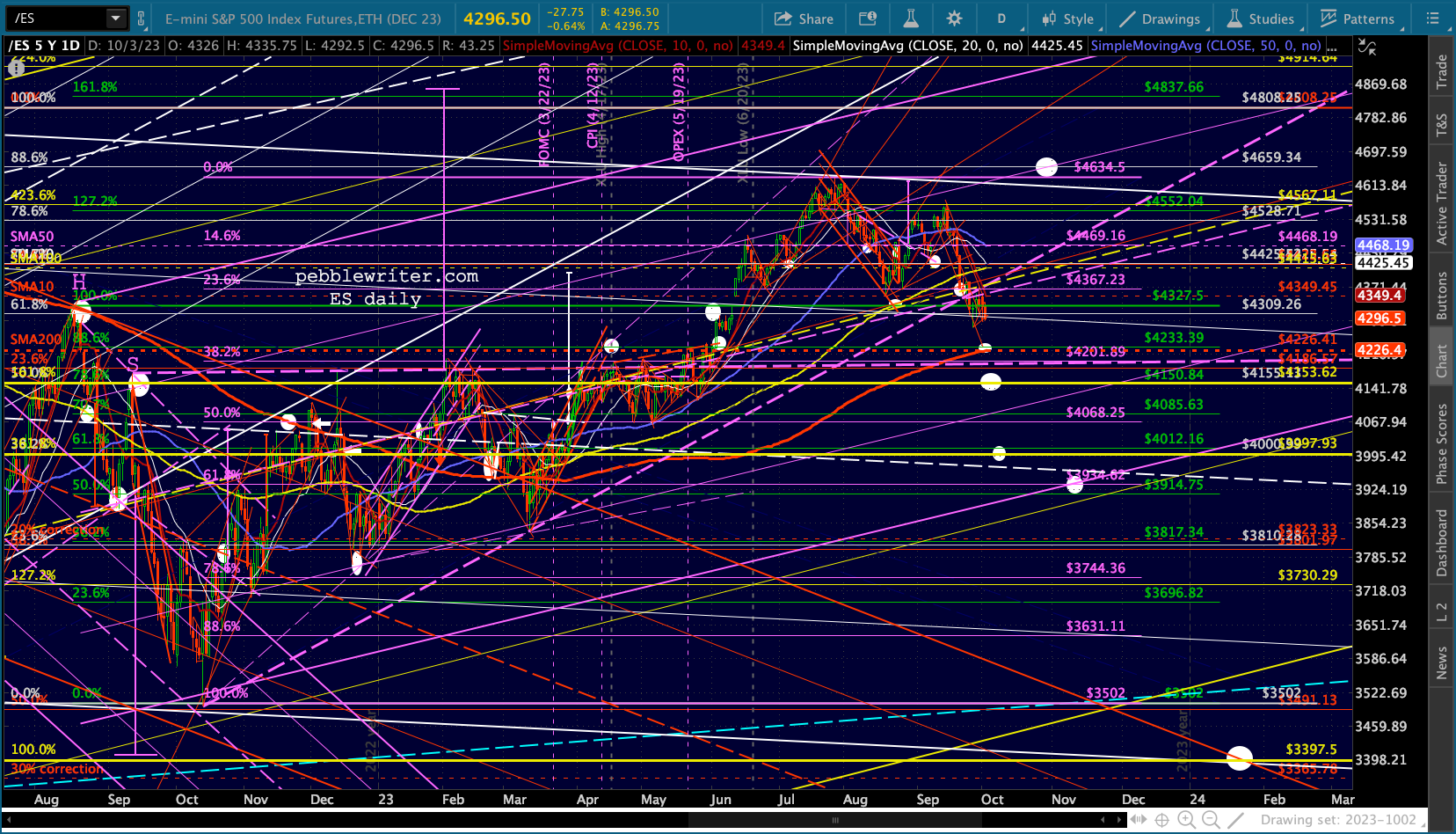

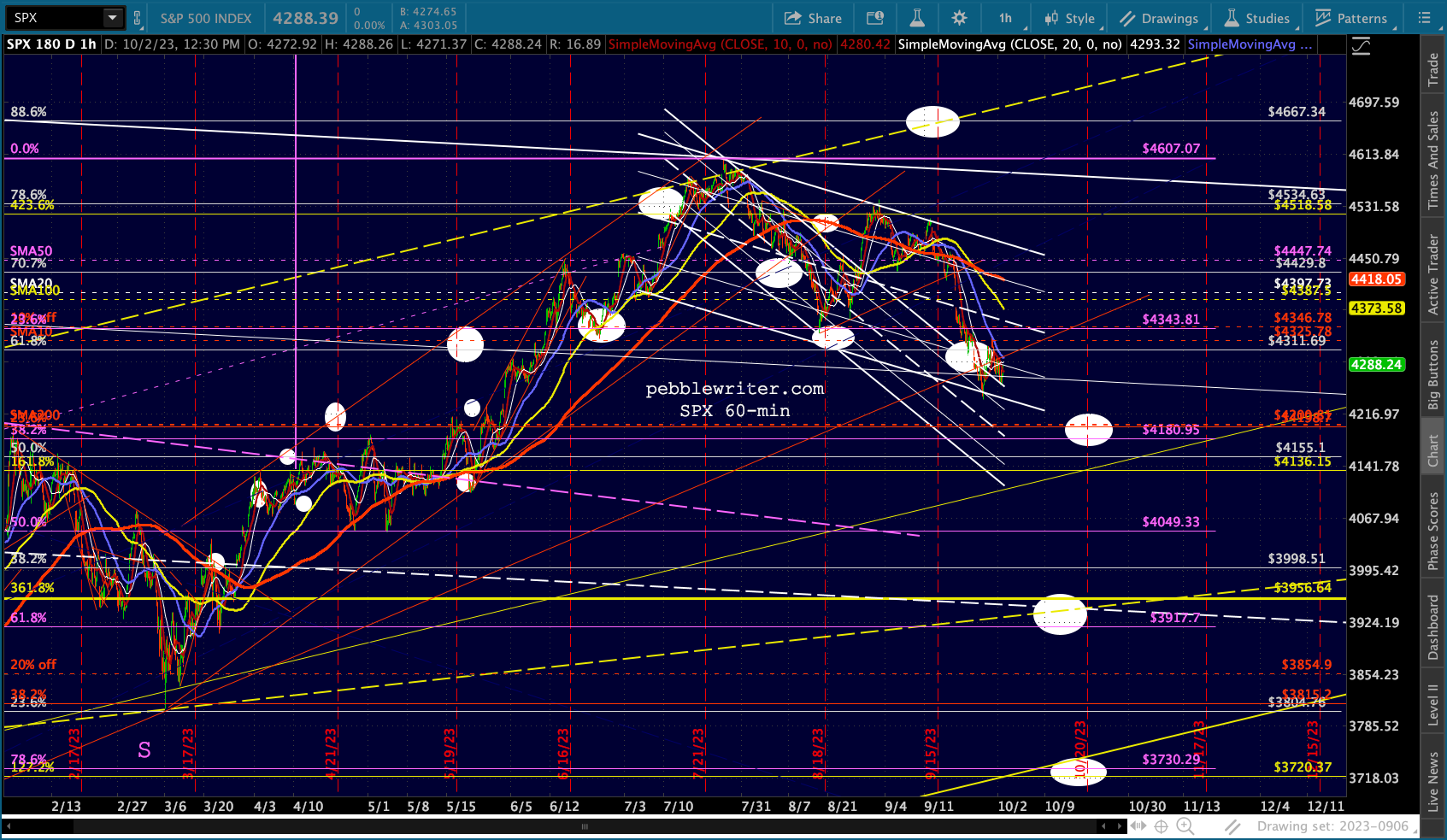

The 4200 SMA-200 for SPX will be quite the important test.

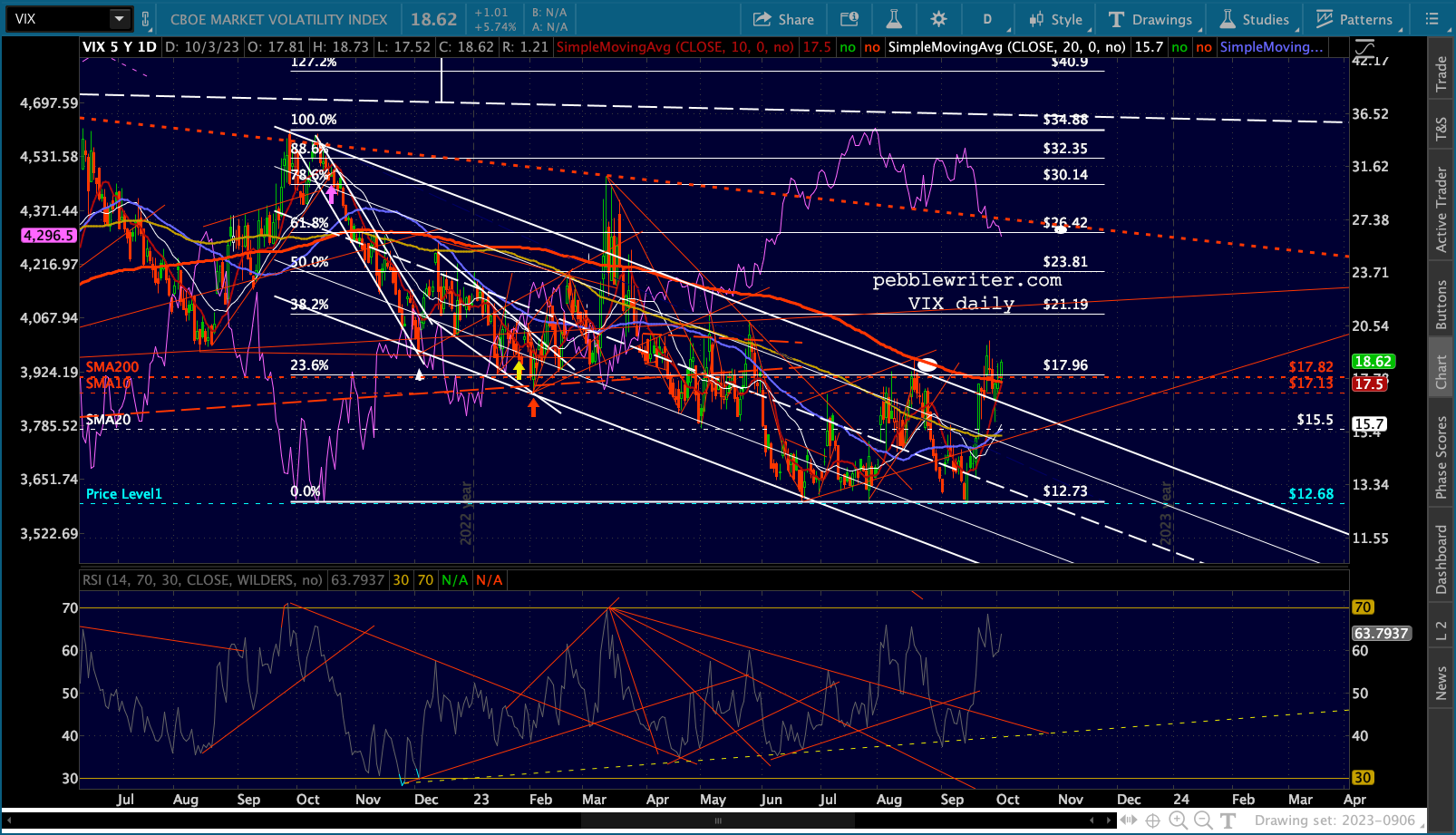

The 4200 SMA-200 for SPX will be quite the important test. Note that VIX hasn’t really gone crazy just yet…

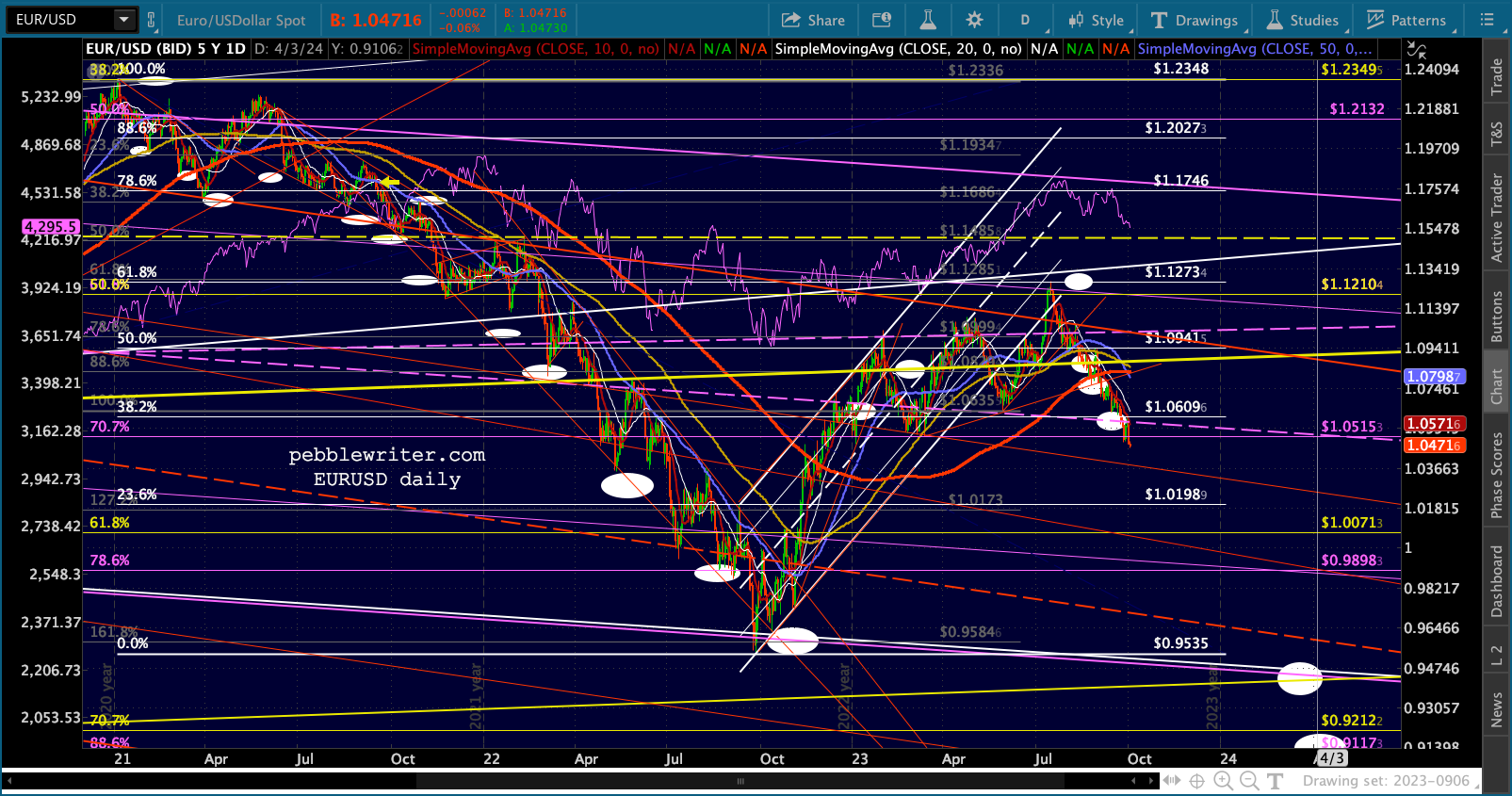

Note that VIX hasn’t really gone crazy just yet…  …though the EURUSD continues to melt down…

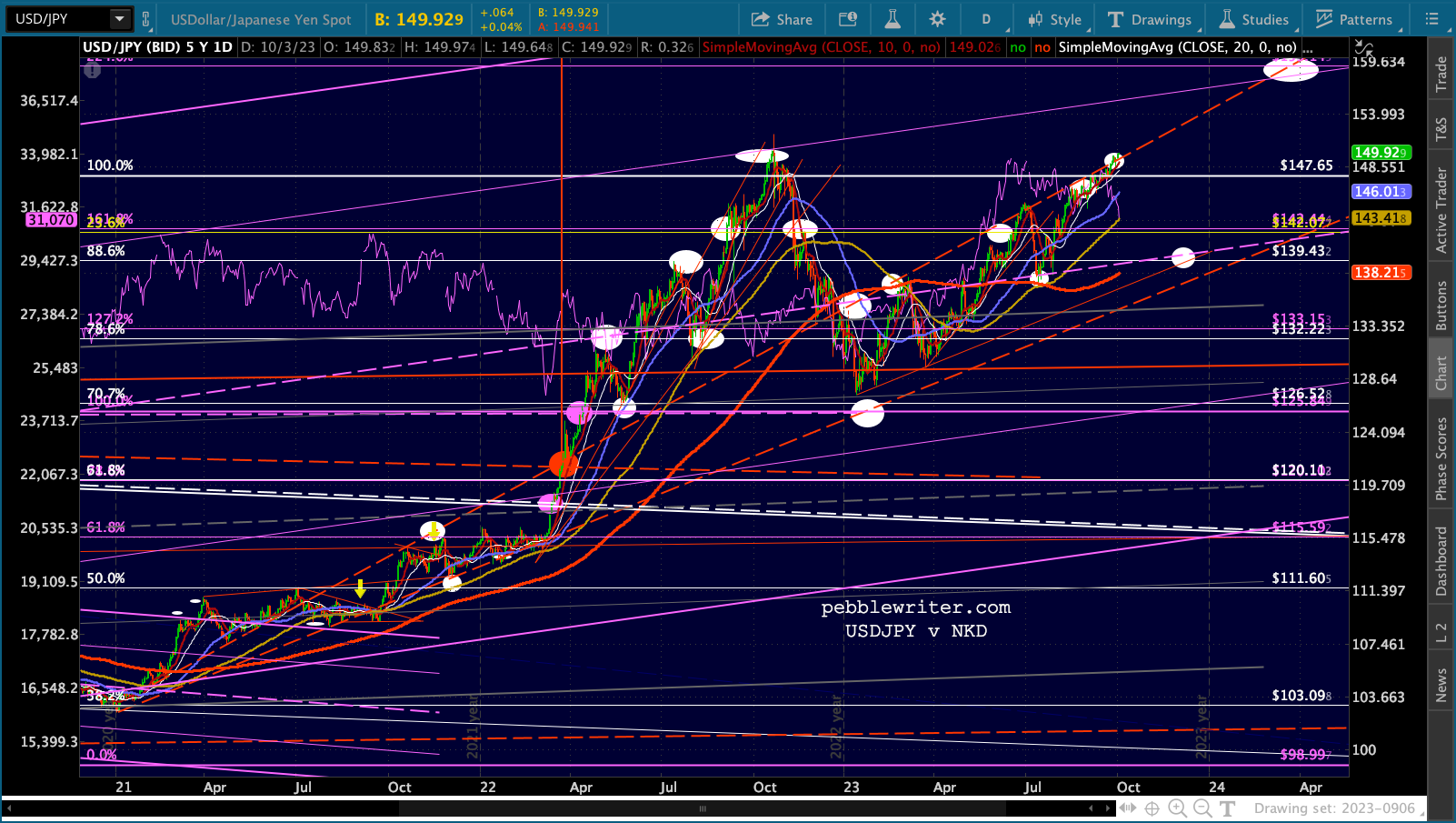

…though the EURUSD continues to melt down… …and, the USDJPY continues to push higher…

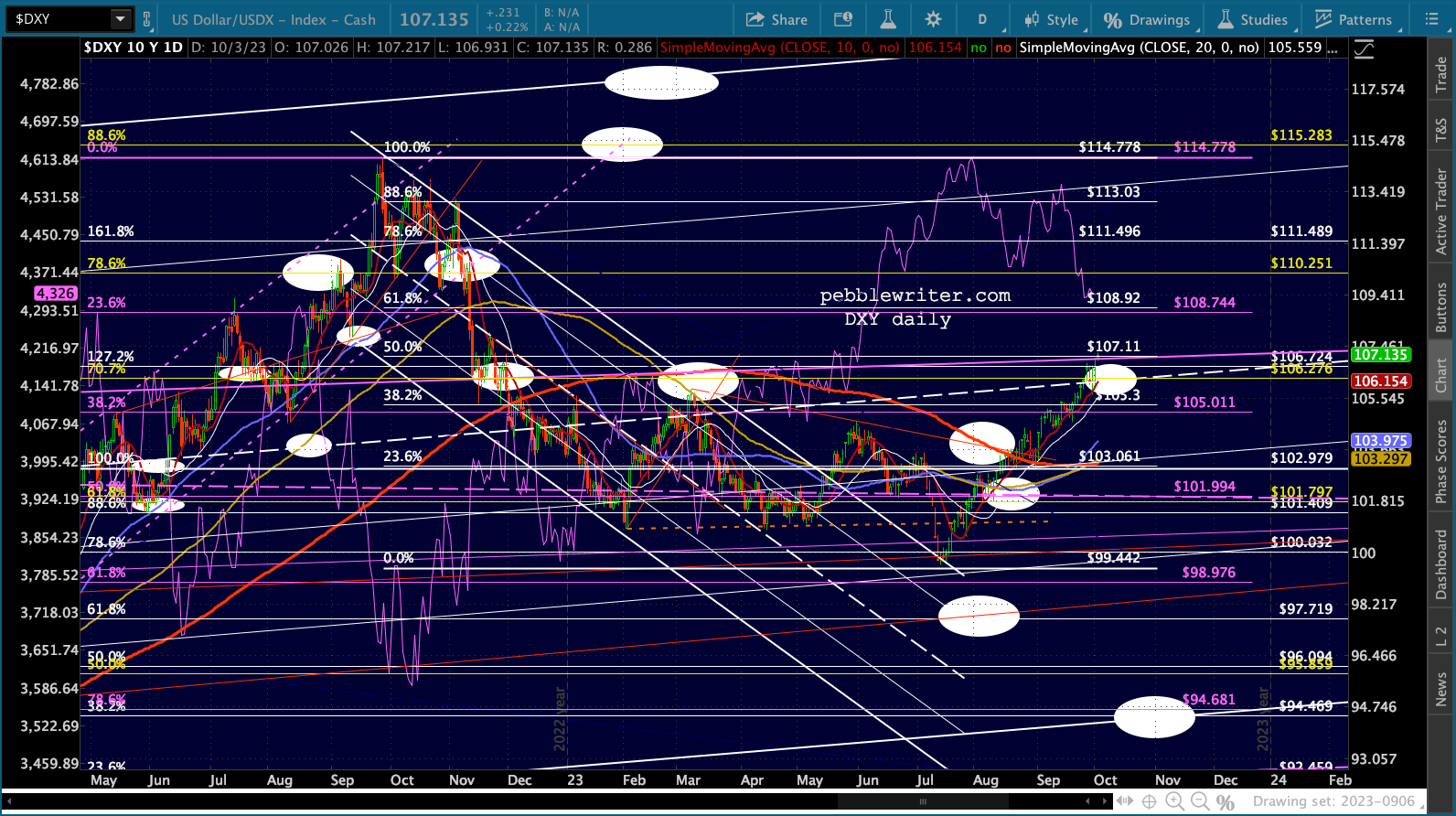

…and, the USDJPY continues to push higher… …pushing the DXY to a 50% retracement of its drop from 114.78 – not that big a move just yet. Higher relative interest rates could change that.

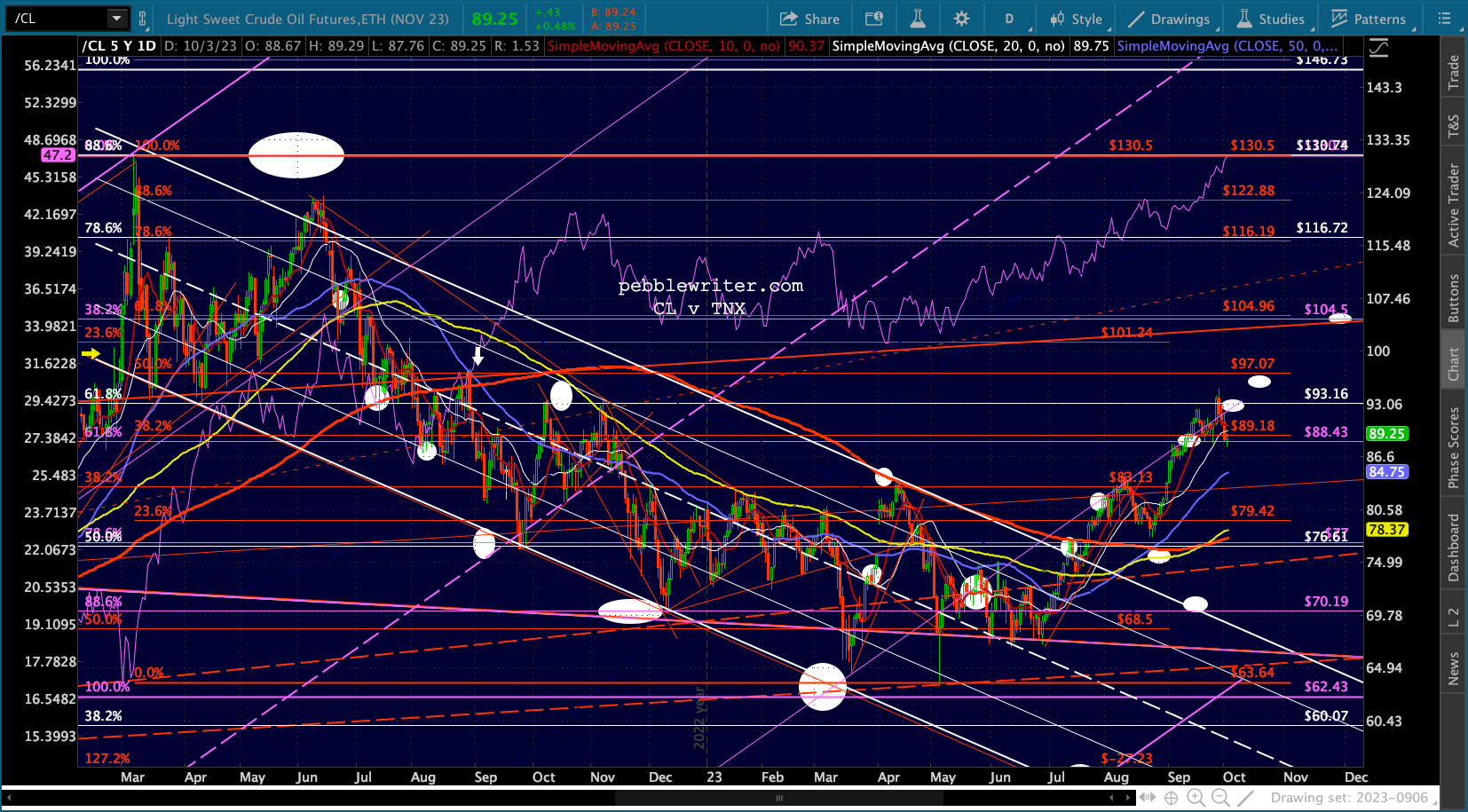

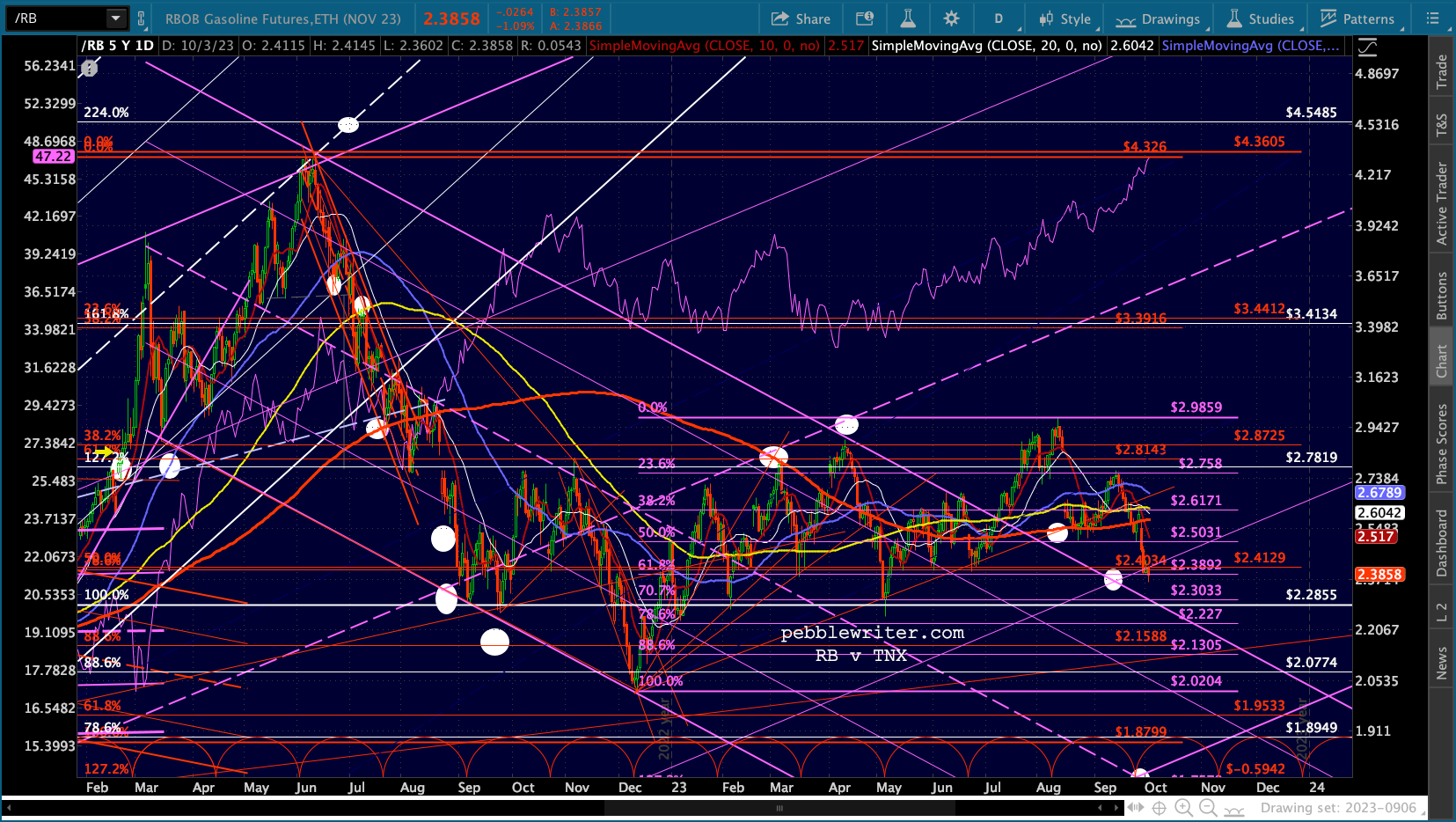

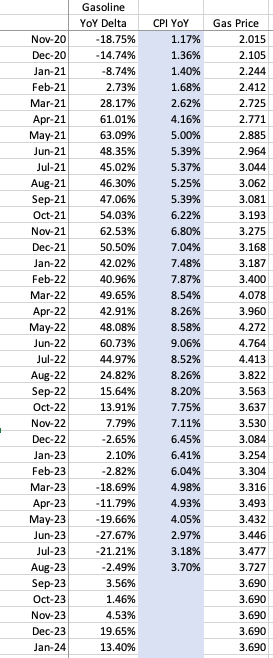

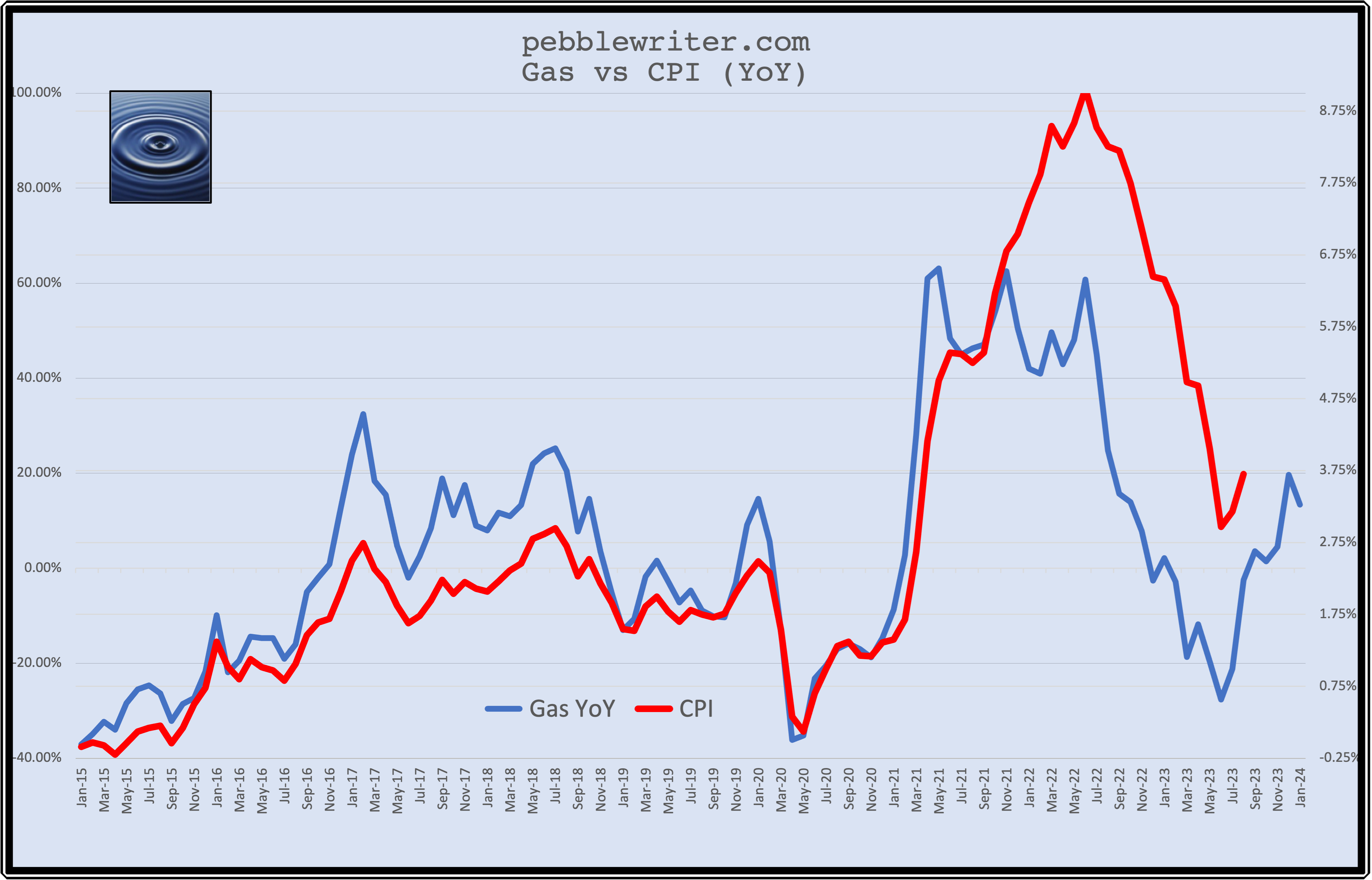

…pushing the DXY to a 50% retracement of its drop from 114.78 – not that big a move just yet. Higher relative interest rates could change that.  The rise in oil/gas prices will obviously continue to play an important role.

The rise in oil/gas prices will obviously continue to play an important role.

The YoY delta in gas prices recently turned positive again after dropping to as low as -28%. If prices hold steady, we could be back to +20% by December.

The YoY delta in gas prices recently turned positive again after dropping to as low as -28%. If prices hold steady, we could be back to +20% by December.

Good luck getting inflation back to 2% should that occur…

continuing…