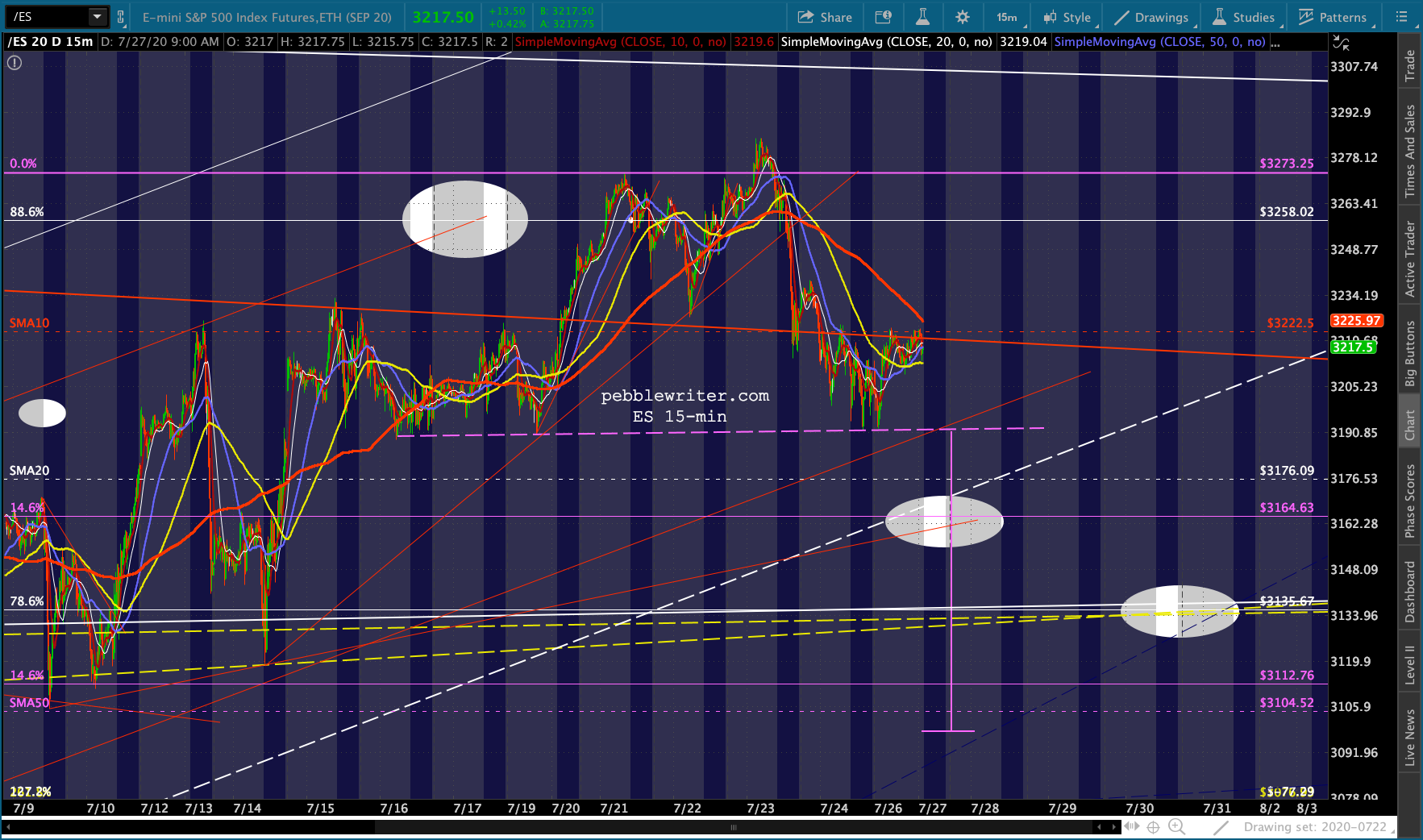

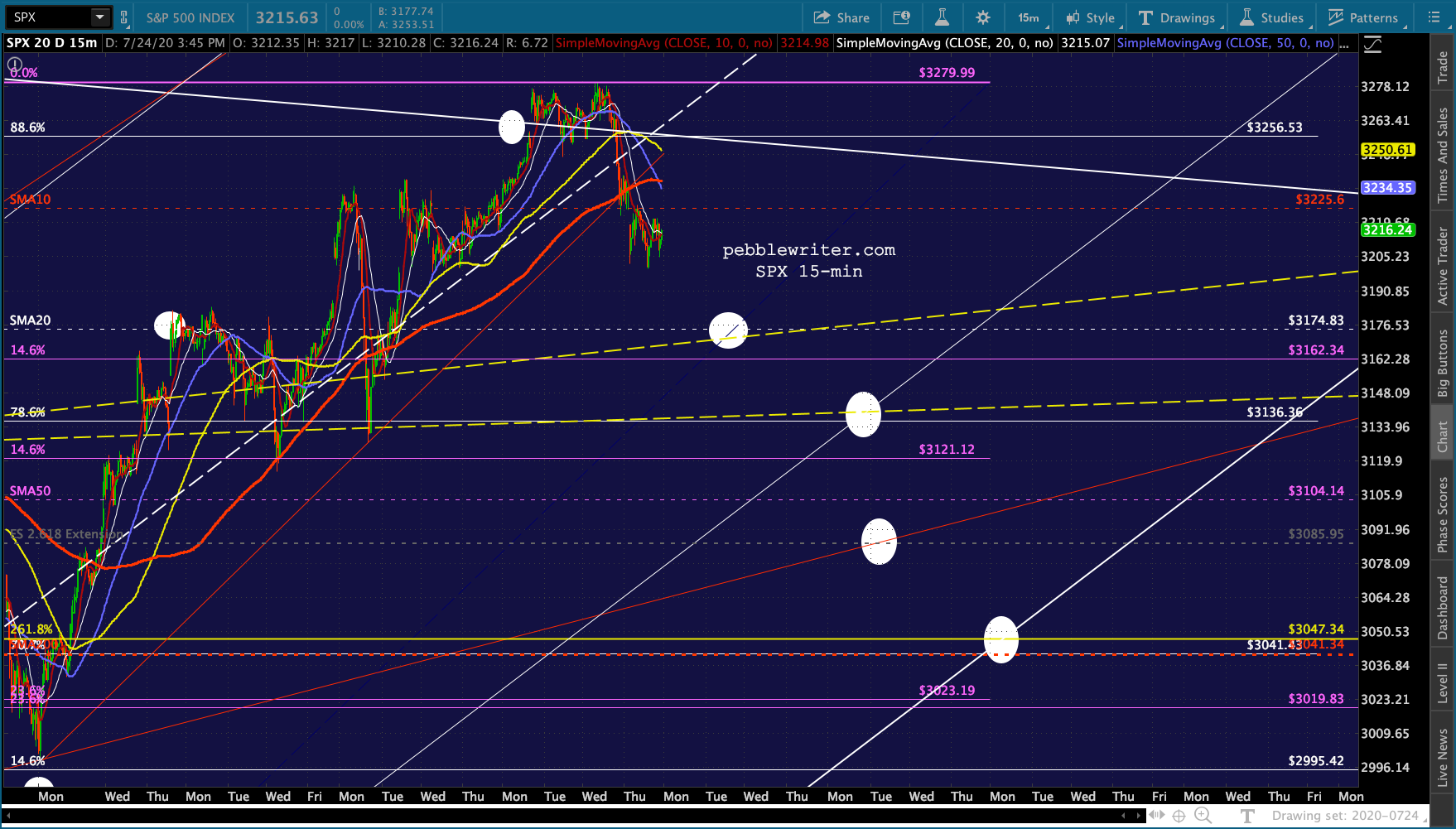

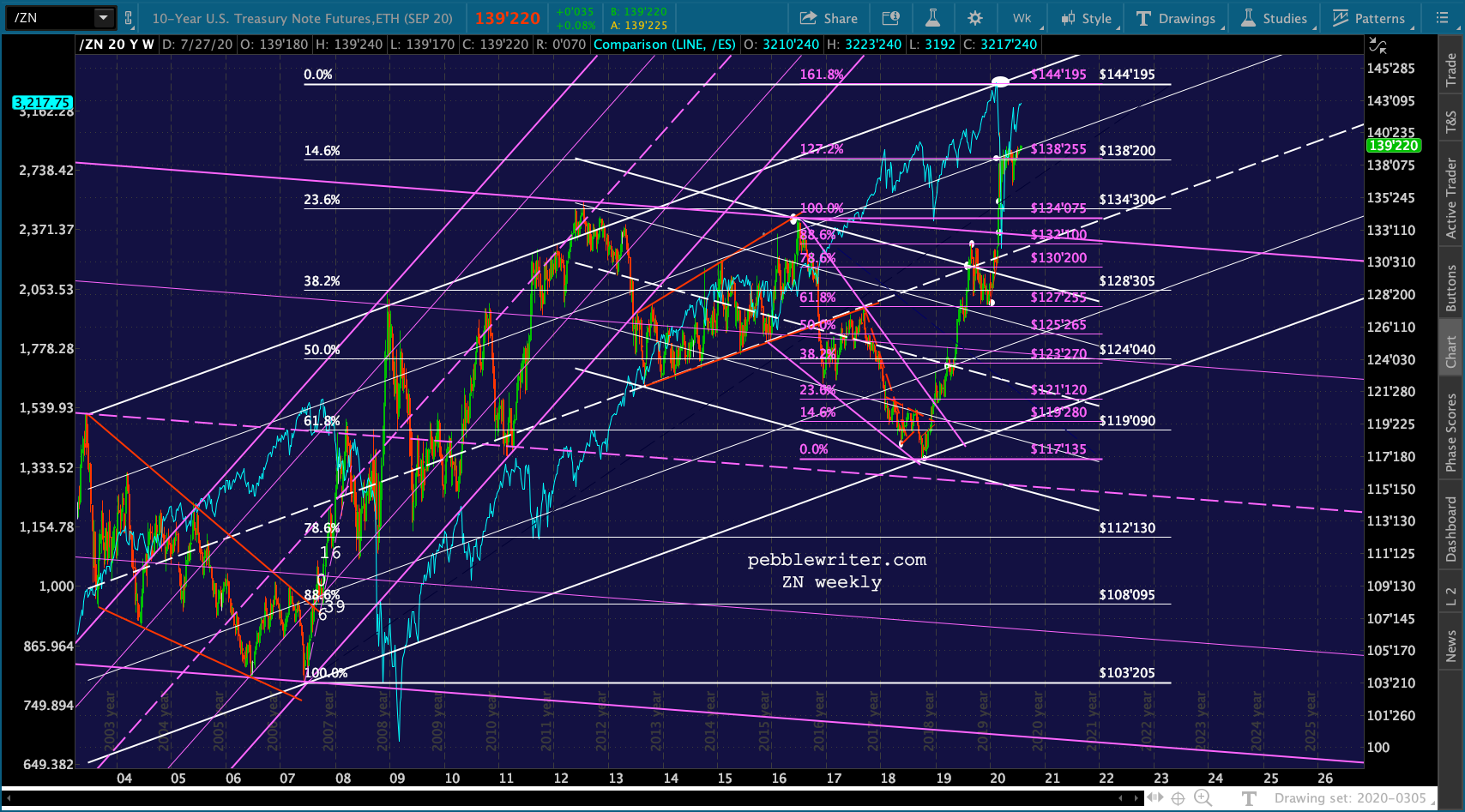

In the latest 30-pt ramp job, ES ran out of juice at a backtest of its 10-day moving average – not exactly a bullish move. This would leave SPX with a backtest of its own, suggestive of the additional downside Friday’s session left on the table.

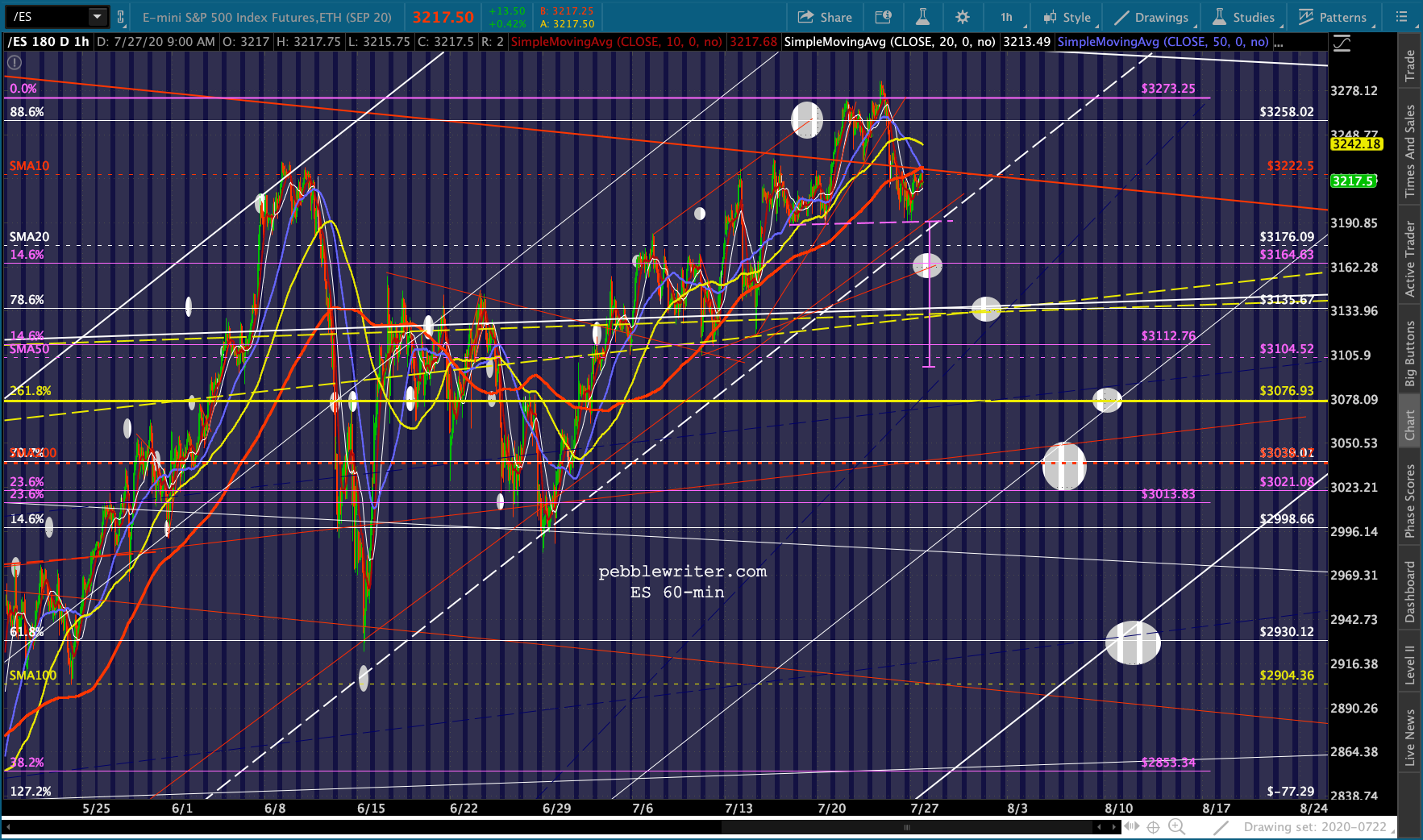

It also suggests a nice little Head & Shoulders pattern that could finally get a correction rolling. Should we be concerned about the breakdown in the dollar and breakout in gold? Or is the yen’s breakdown the more serious threat to stocks?

It also suggests a nice little Head & Shoulders pattern that could finally get a correction rolling. Should we be concerned about the breakdown in the dollar and breakout in gold? Or is the yen’s breakdown the more serious threat to stocks?

continued for members…

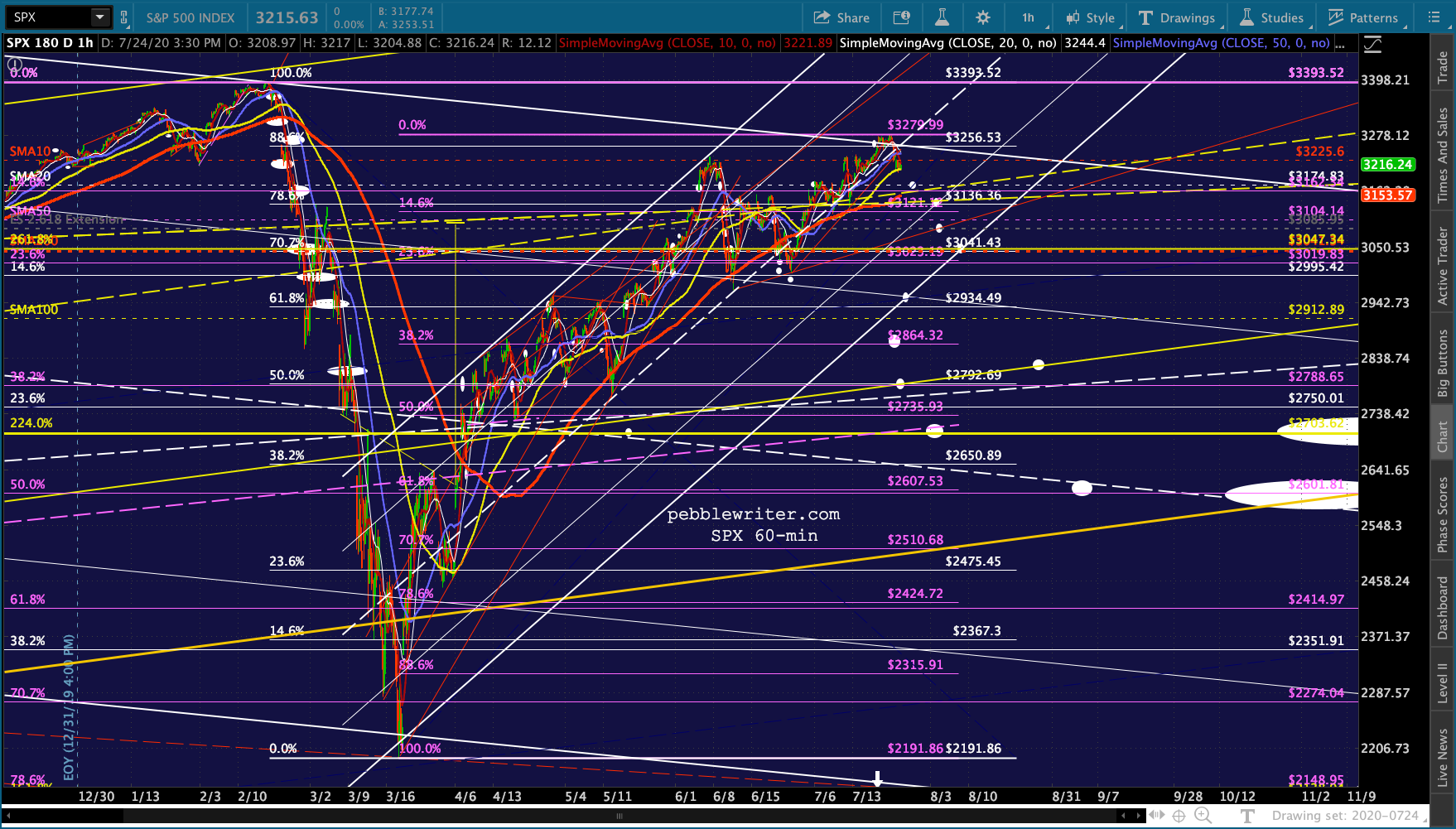

The bigger picture for ES and SPX:

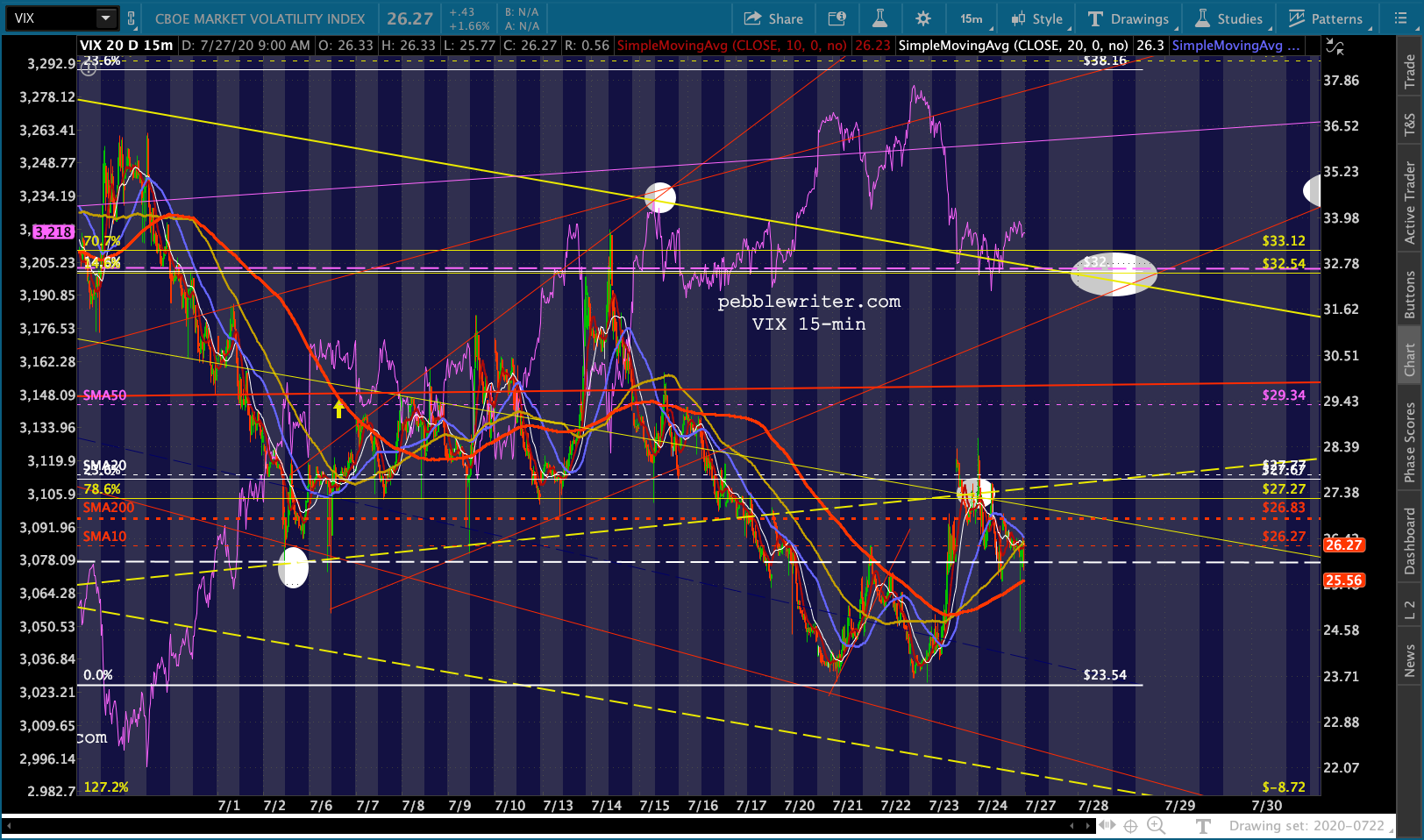

VIX is still being quite coy…

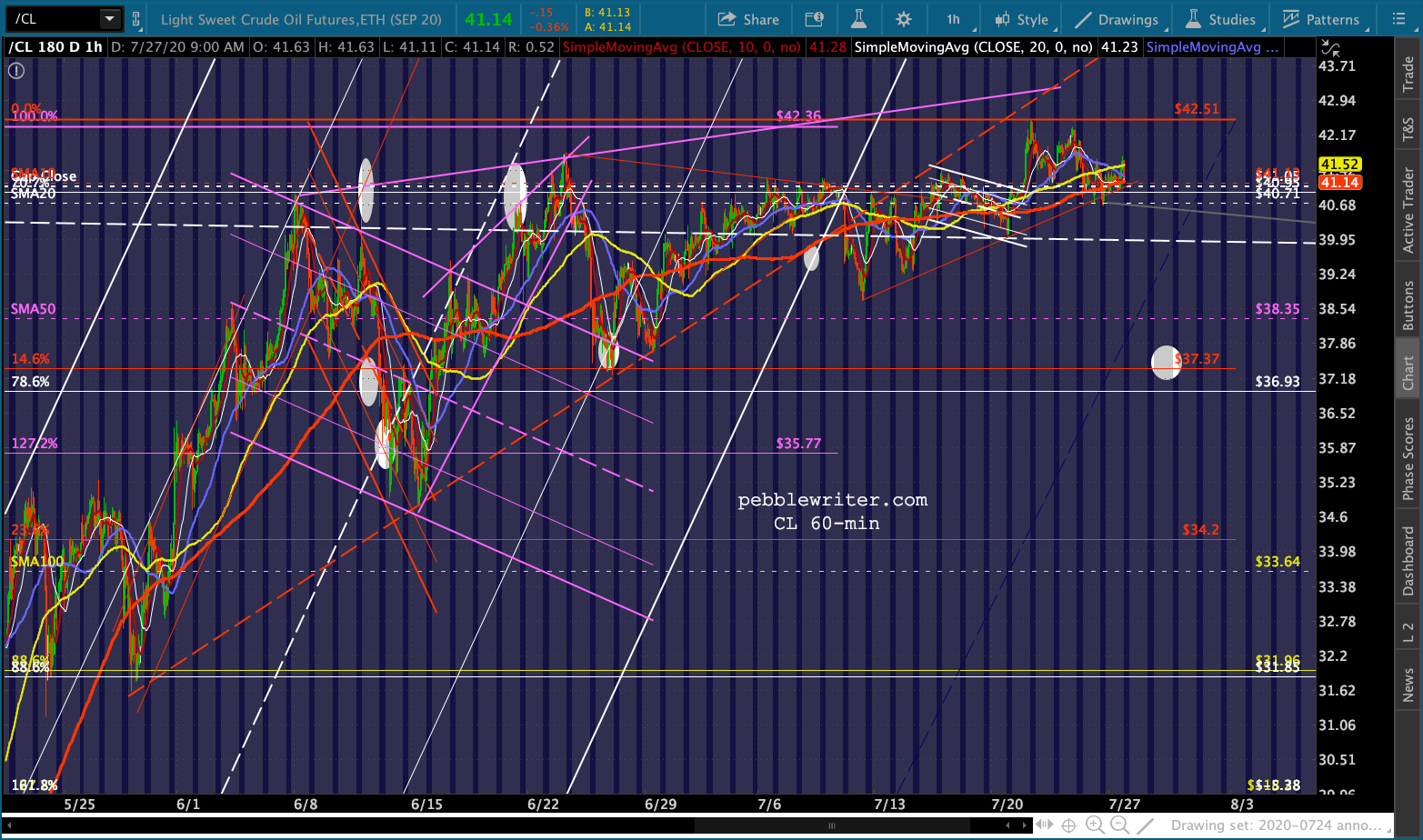

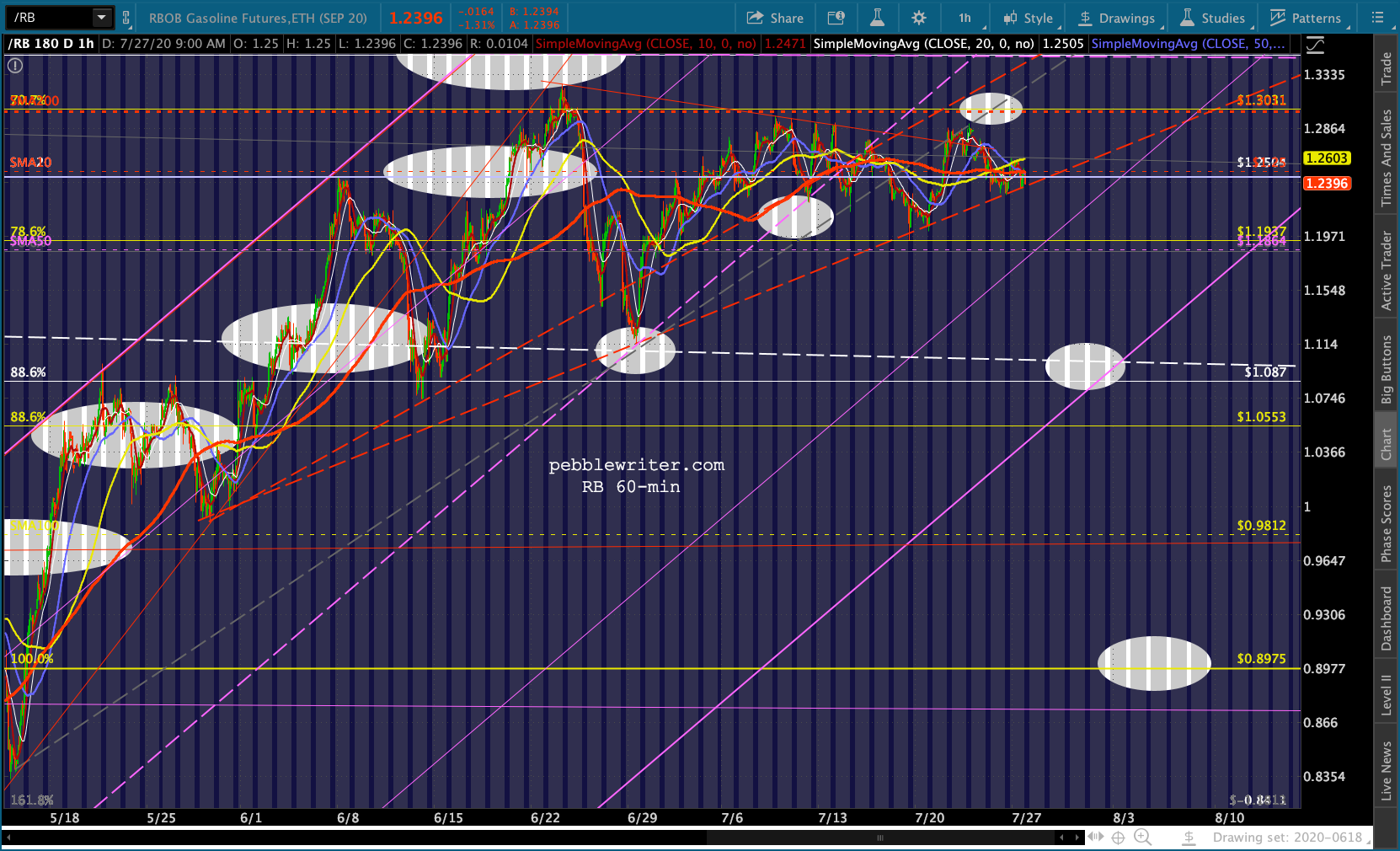

VIX is still being quite coy… …as CL and RB continue to threaten a breakdown – with no follow through so far.

…as CL and RB continue to threaten a breakdown – with no follow through so far.

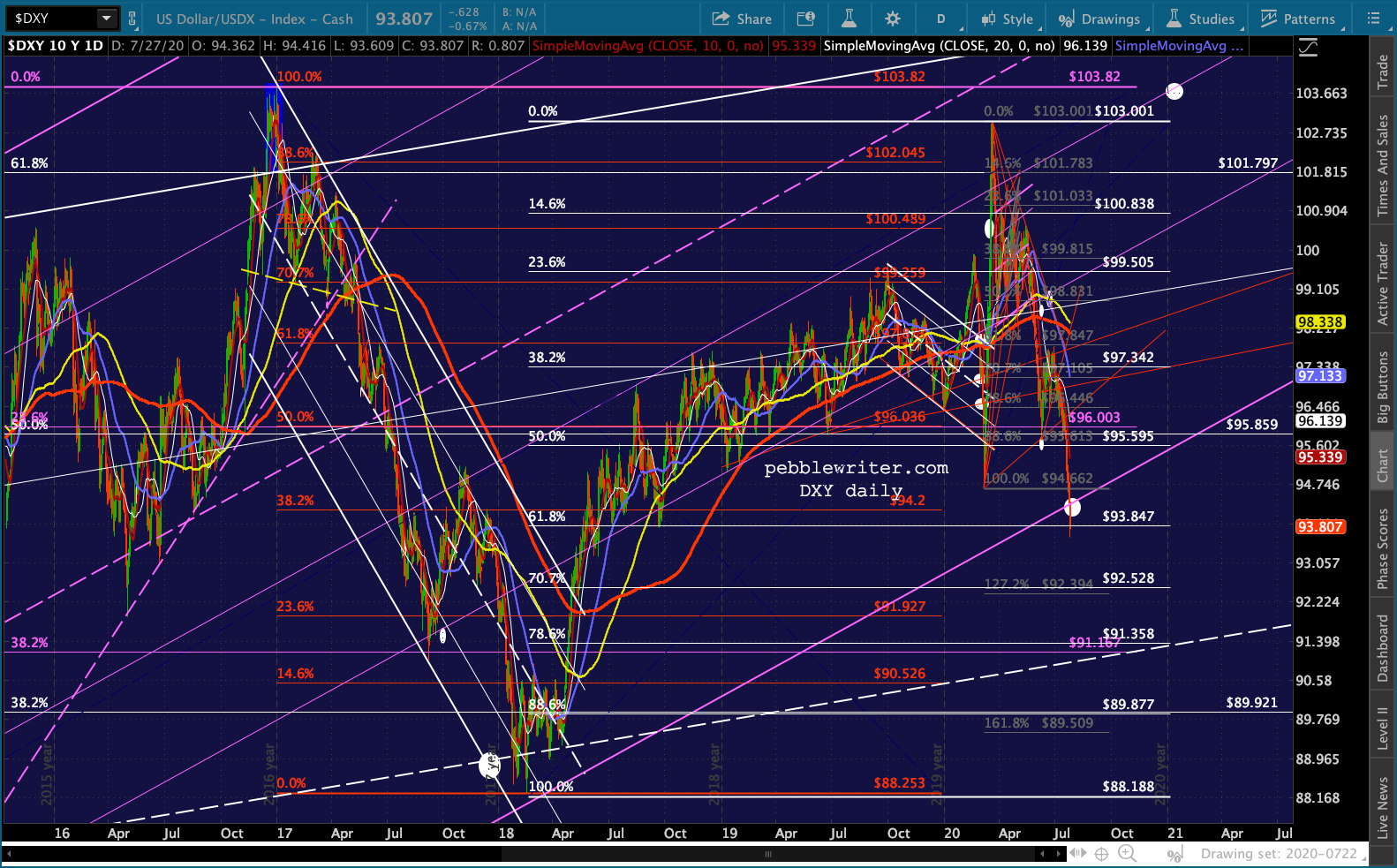

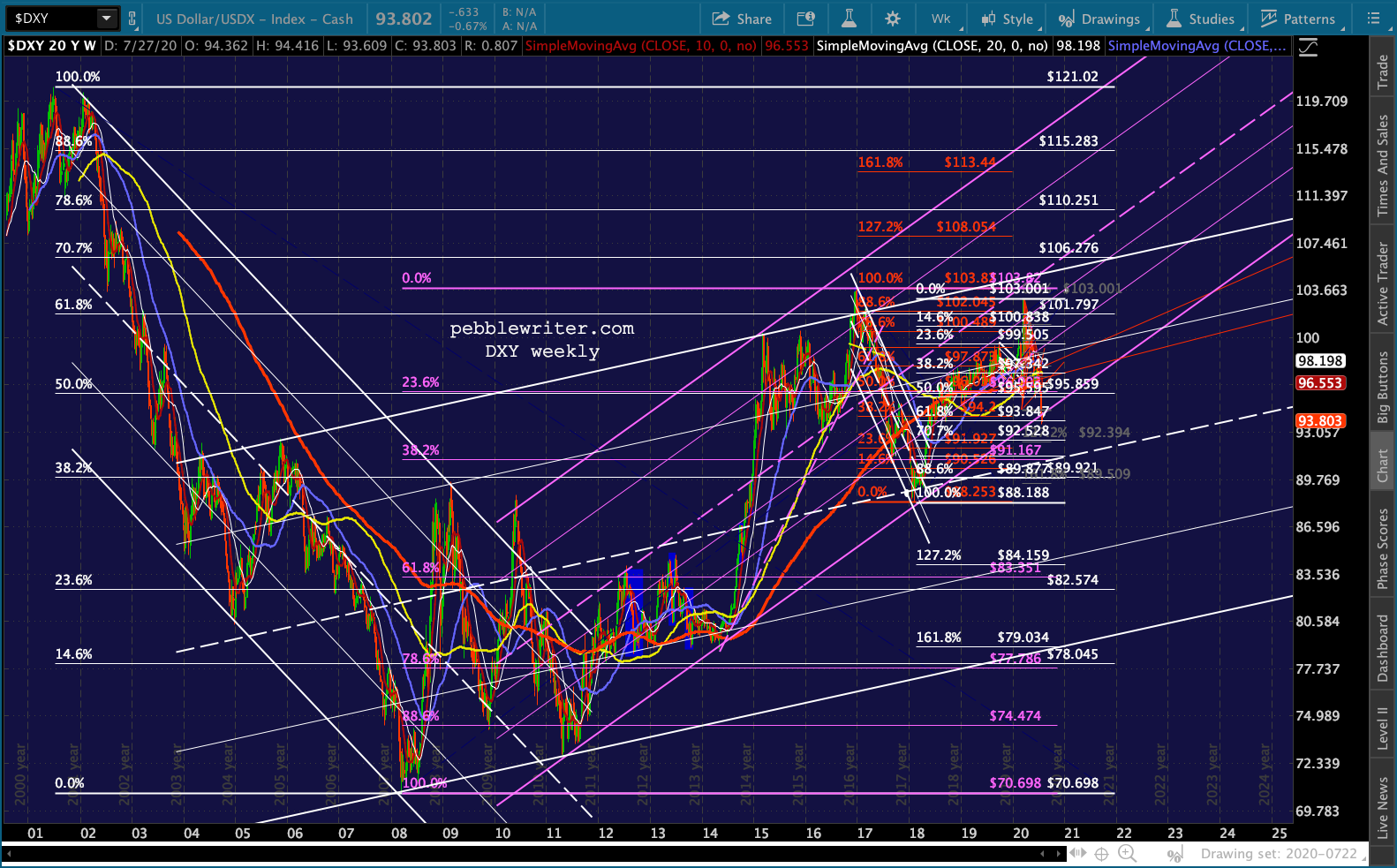

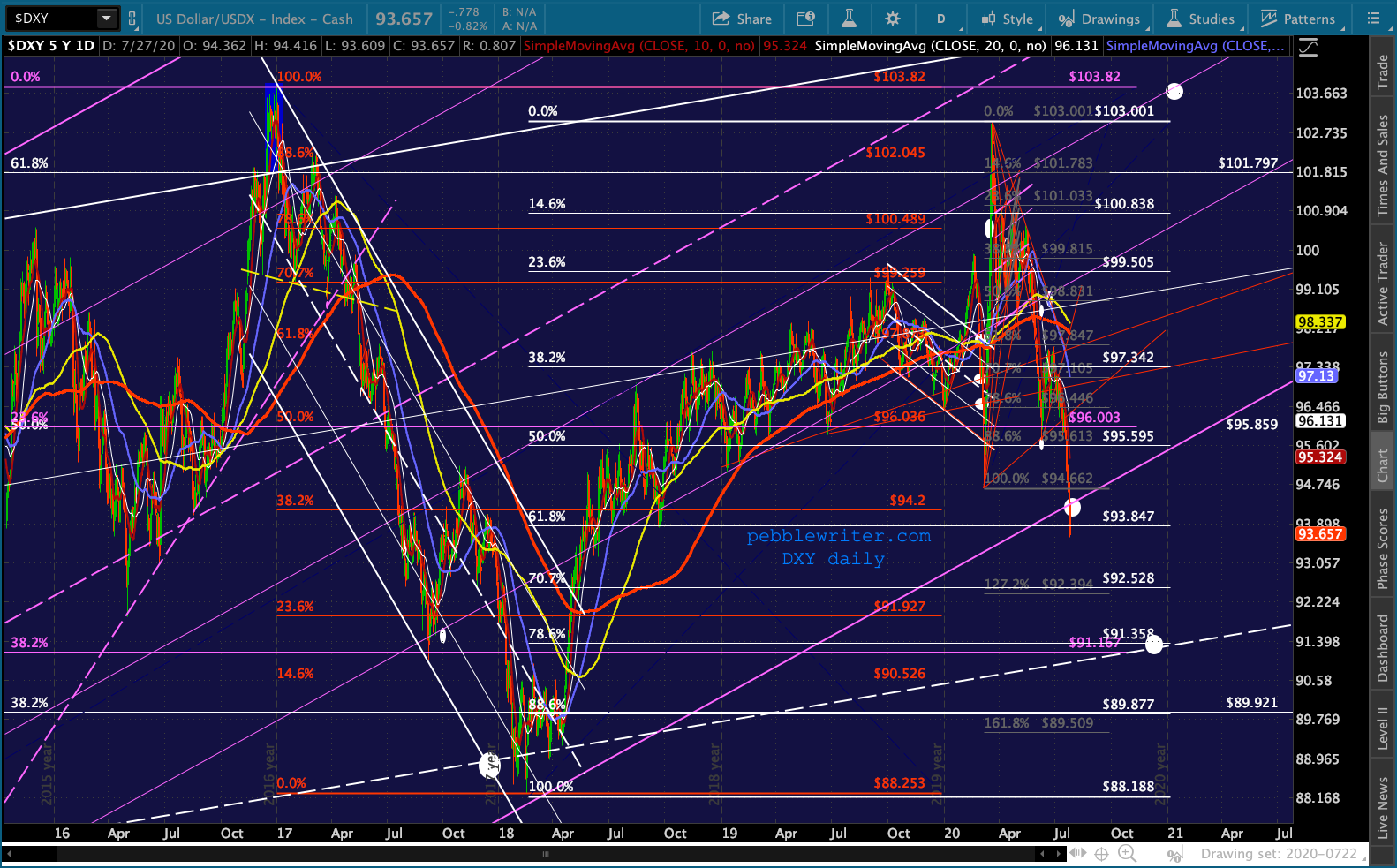

The biggest mystery has ostensibly been solved: the dollar and gold. DXY’s purple channel appears to be breaking down…

The biggest mystery has ostensibly been solved: the dollar and gold. DXY’s purple channel appears to be breaking down…

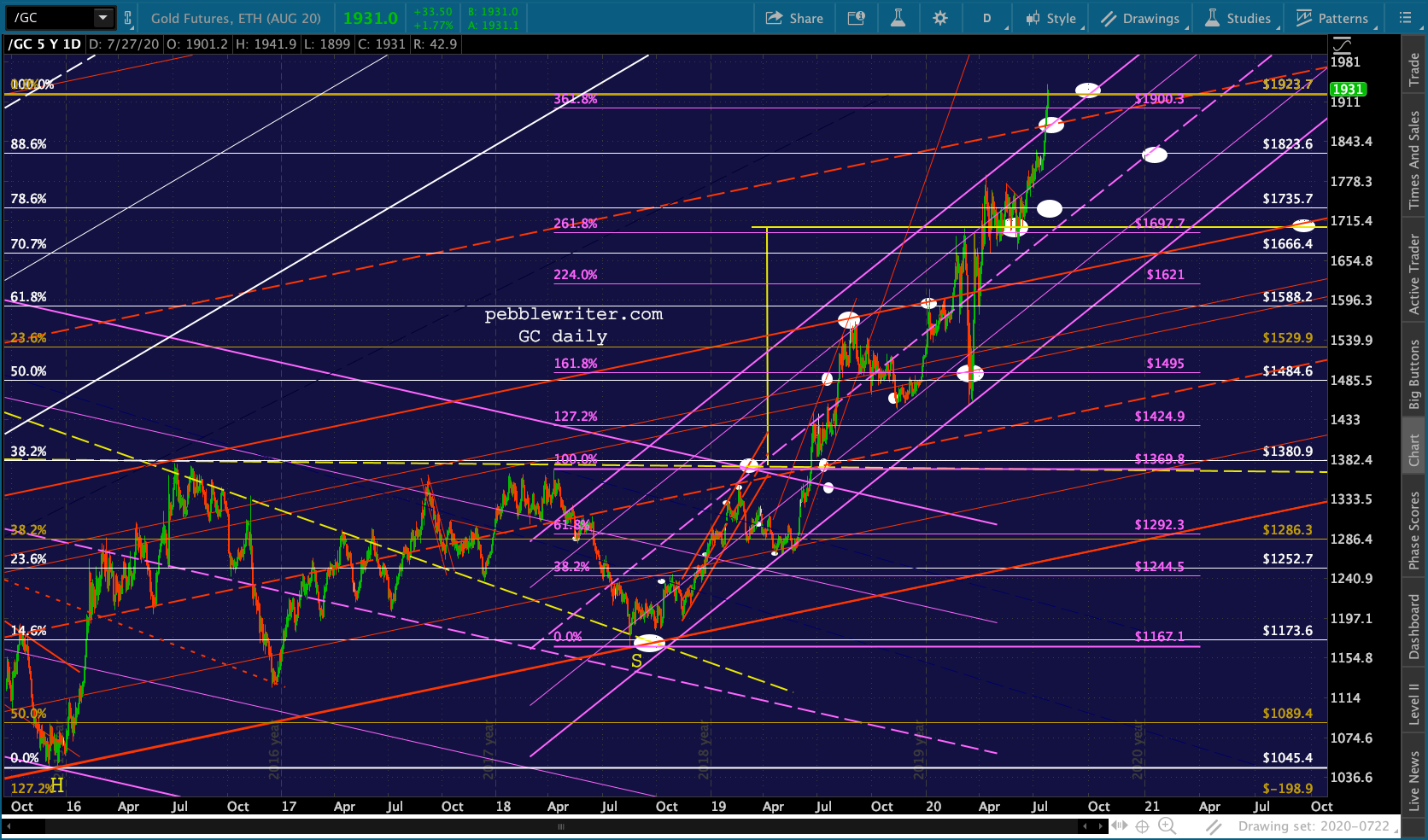

…as GC breaks out to new all-time highs. It can be bought here with 1923.70 as its new support.

…as GC breaks out to new all-time highs. It can be bought here with 1923.70 as its new support. It’s fascinating that, after years of keeping a lid on the price of gold, the Fed would step aside and give the market free reign.

It’s fascinating that, after years of keeping a lid on the price of gold, the Fed would step aside and give the market free reign.

Perhaps they feel it’s enough of an accomplishment to have kept interest rates under control…

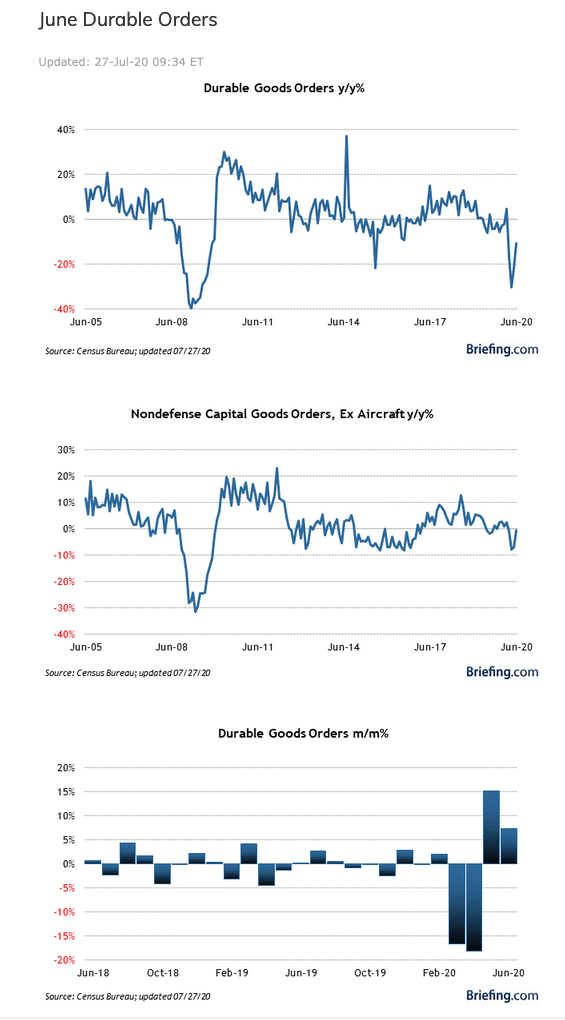

…even as durable goods, at 7.3%, came in well ahead of expectations of 6.4%. Between pockets of inflation, skyrocketing money supply and increasing conflict between the US and China, it’s not terribly surprising that gold is breaking out.

…even as durable goods, at 7.3%, came in well ahead of expectations of 6.4%. Between pockets of inflation, skyrocketing money supply and increasing conflict between the US and China, it’s not terribly surprising that gold is breaking out.  Let’s take a look at the big picture. The purple channel breakdown means at least another few percent drop in DXY to the white channel midline, ideally around the end of the year.

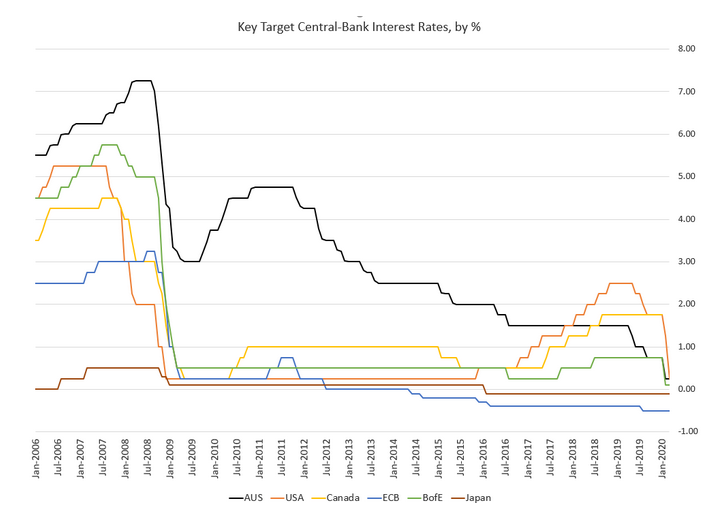

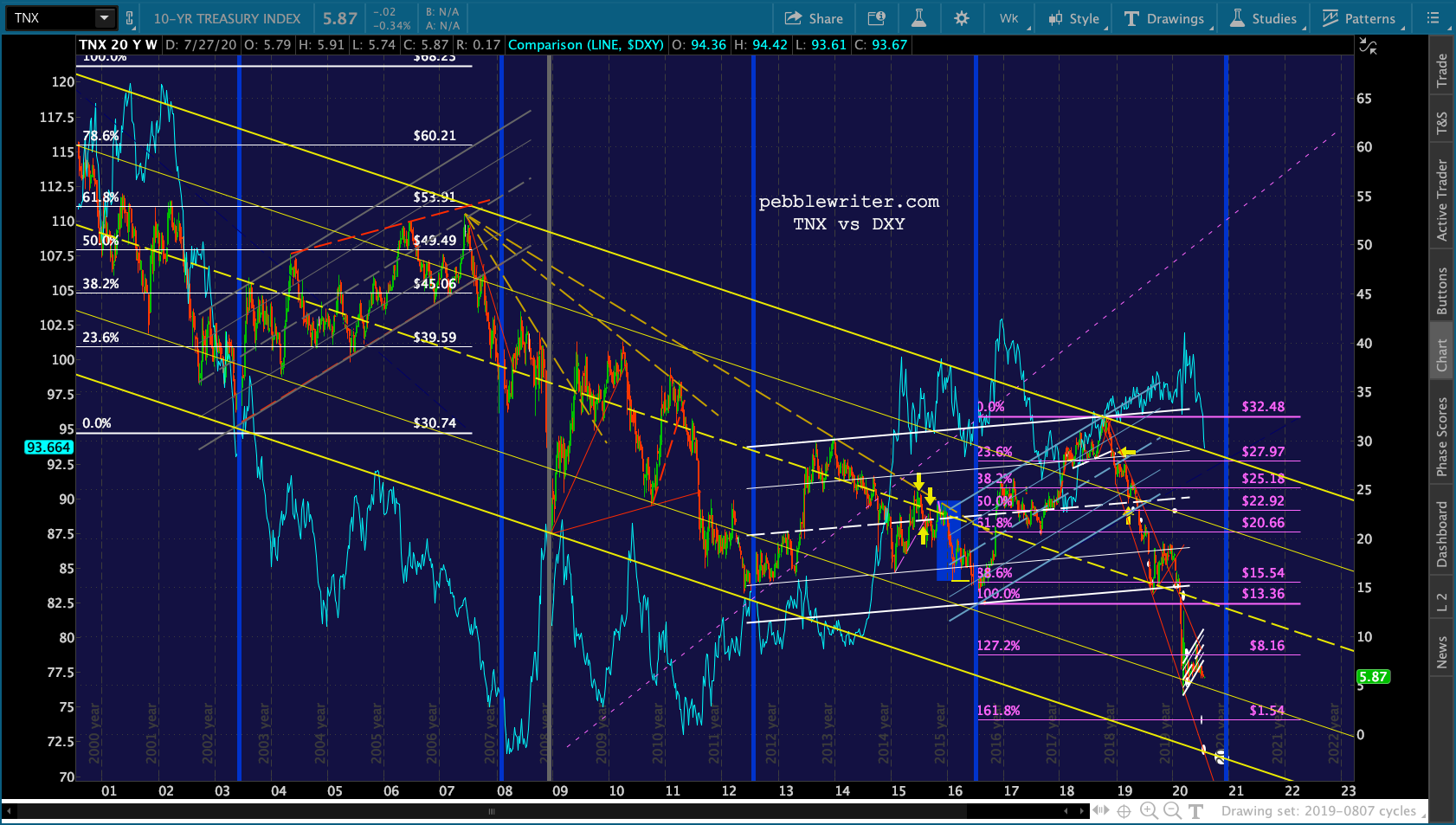

Let’s take a look at the big picture. The purple channel breakdown means at least another few percent drop in DXY to the white channel midline, ideally around the end of the year.  The fundamental factors causing the dollar’s demise are numerous. But, the overarching theme is a collapse in the spread between US rates and those of other competing economies.

The fundamental factors causing the dollar’s demise are numerous. But, the overarching theme is a collapse in the spread between US rates and those of other competing economies.

The Fed bucked the collapsing rates trend between 2016-2018, then went into a holding pattern until the pandemic forced its hand.

With global short-term rates now at or below zero, there is no longer much advantage to holding USD-based short-term instruments and taking currency risk [There’s also less of an advantage over holding gold, which obviously pays no interest.]

With global short-term rates now at or below zero, there is no longer much advantage to holding USD-based short-term instruments and taking currency risk [There’s also less of an advantage over holding gold, which obviously pays no interest.]

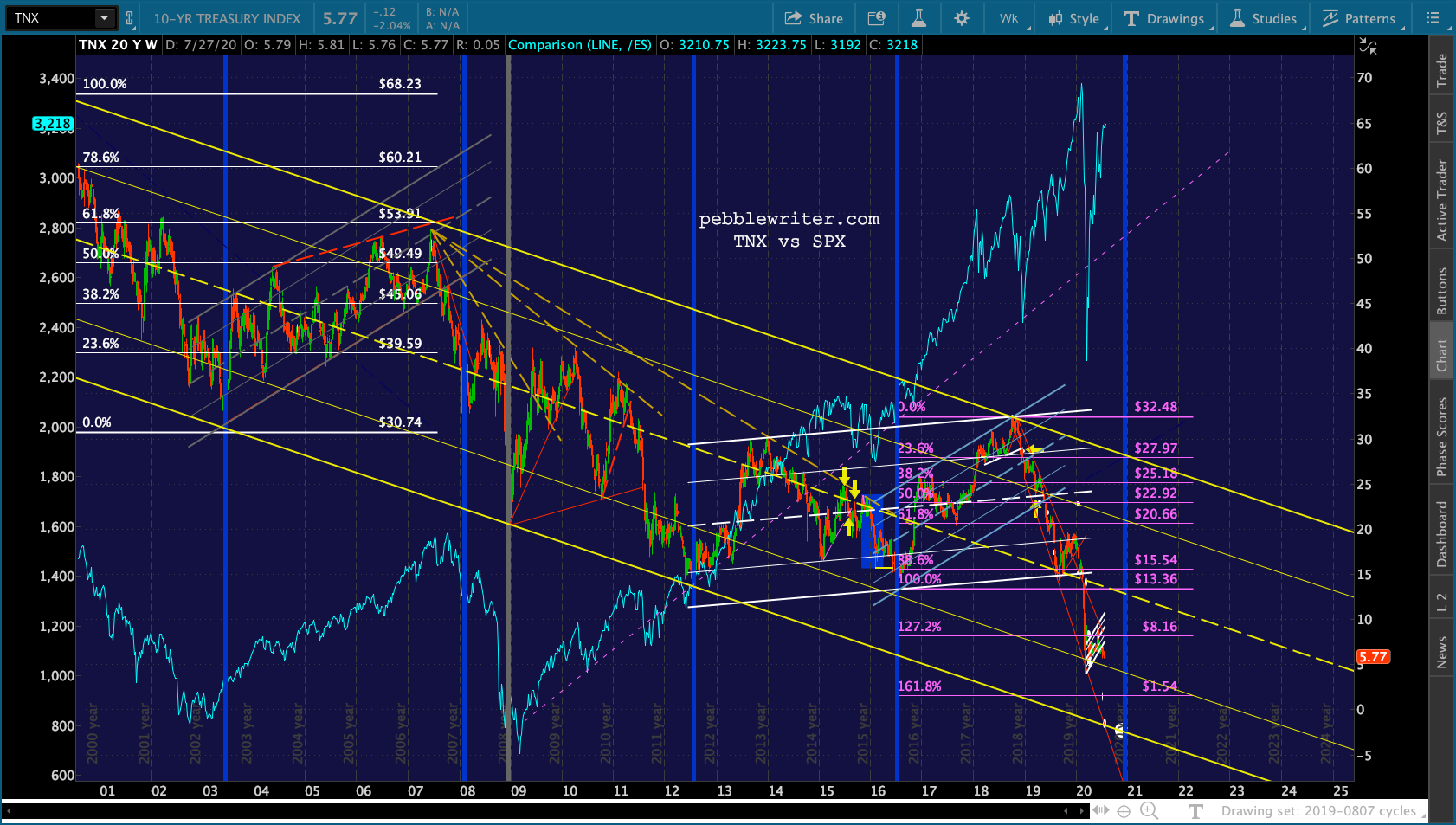

But, the drop in longer 10Y rates was both a function of policy changes and, importantly, the flow of funds from riskier equities into presumably safer notes: the “fear trade” associated with the 35% downturn in stocks between Feb-Mar.

Now that the Fed has dispensed with any need to be fearful of an equity correction, rates remain where the fear trade drove them. The reason, as we’ve discussed many times, is that interest rates must remain low in order to make the spiraling debt/deficit theoretically affordable.

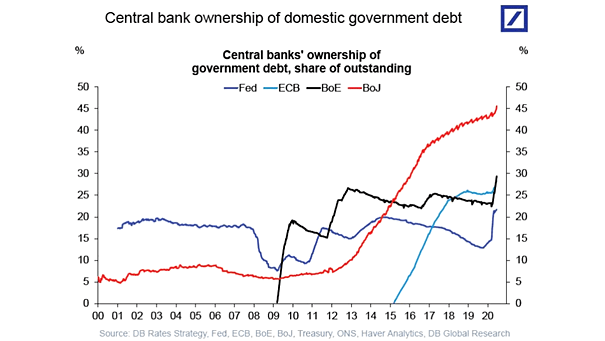

Since the equity crash, the Fed has therefore done everything in its power to put a lid on rates – including owning over 20% of the outstanding government debt. Whatever it takes, indeed… By jumping in to support prices when necessary, the Fed has essentially eliminated yield volatility since May.

By jumping in to support prices when necessary, the Fed has essentially eliminated yield volatility since May.

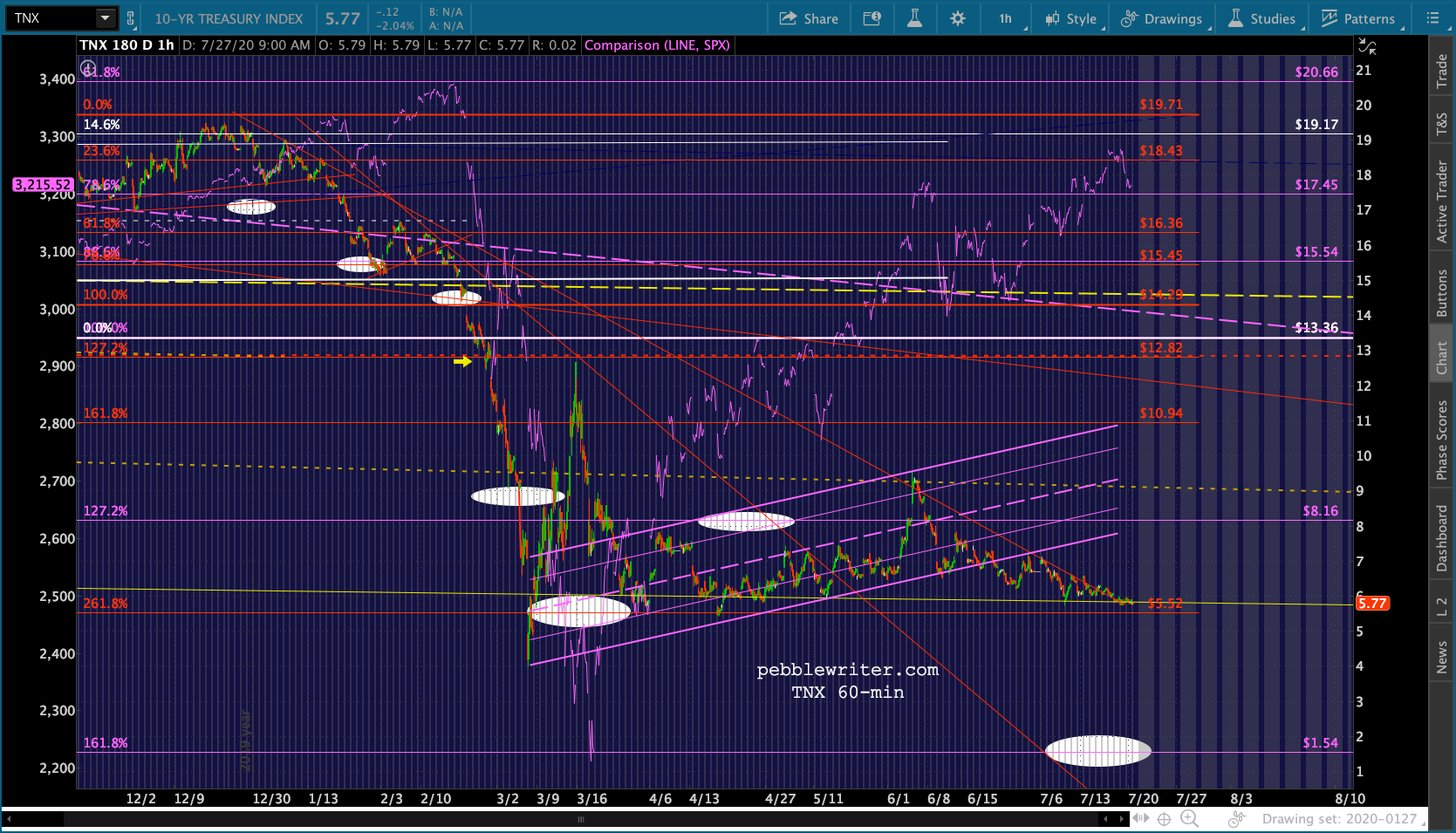

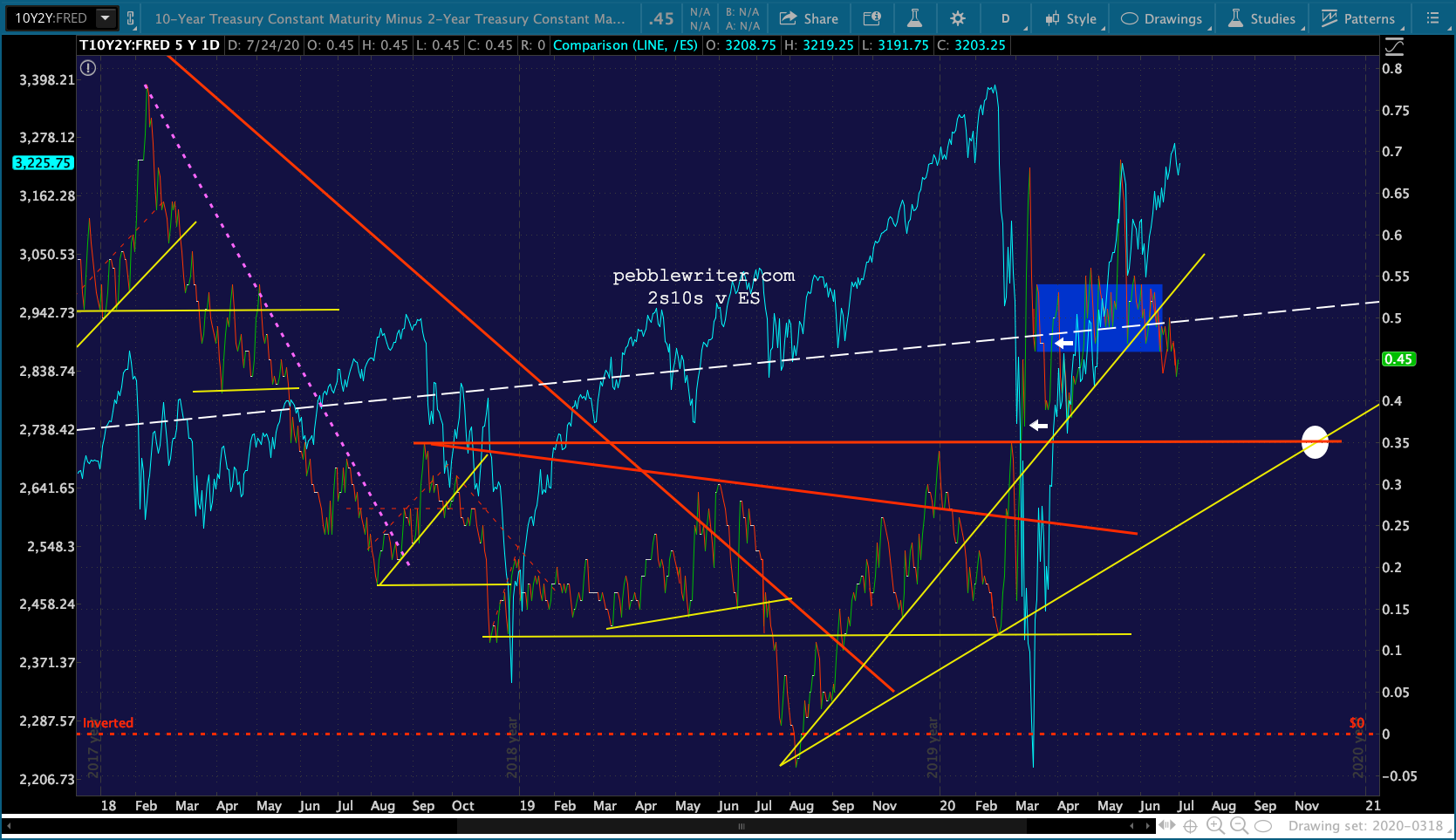

With the 2Y already barely above zero (0.14%) the 10Y has caught down with it (0.595%) to permit the 2s10s to remain largely under control. When the Fed talks about yield curve control, be aware that it is already underway. Aside from a couple of spikes, the 10Y has flatlined…

With the 2Y already barely above zero (0.14%) the 10Y has caught down with it (0.595%) to permit the 2s10s to remain largely under control. When the Fed talks about yield curve control, be aware that it is already underway. Aside from a couple of spikes, the 10Y has flatlined… …which has allowed the 2s10s to essentially flatline for nearly 3 months.

…which has allowed the 2s10s to essentially flatline for nearly 3 months.

However, as debt continues to increase, the need for low or even negative rates will increase a la Japan and the eurozone.

However, as debt continues to increase, the need for low or even negative rates will increase a la Japan and the eurozone.

Had the US been more successful in managing the coronavirus, it would not be in as difficult a situation. As things stand, the US is way behind the curve and the need for low or even negative rates is as great as it is in the eurozone. And, it’s not far behind Japan.

Had the US been more successful in managing the coronavirus, it would not be in as difficult a situation. As things stand, the US is way behind the curve and the need for low or even negative rates is as great as it is in the eurozone. And, it’s not far behind Japan.

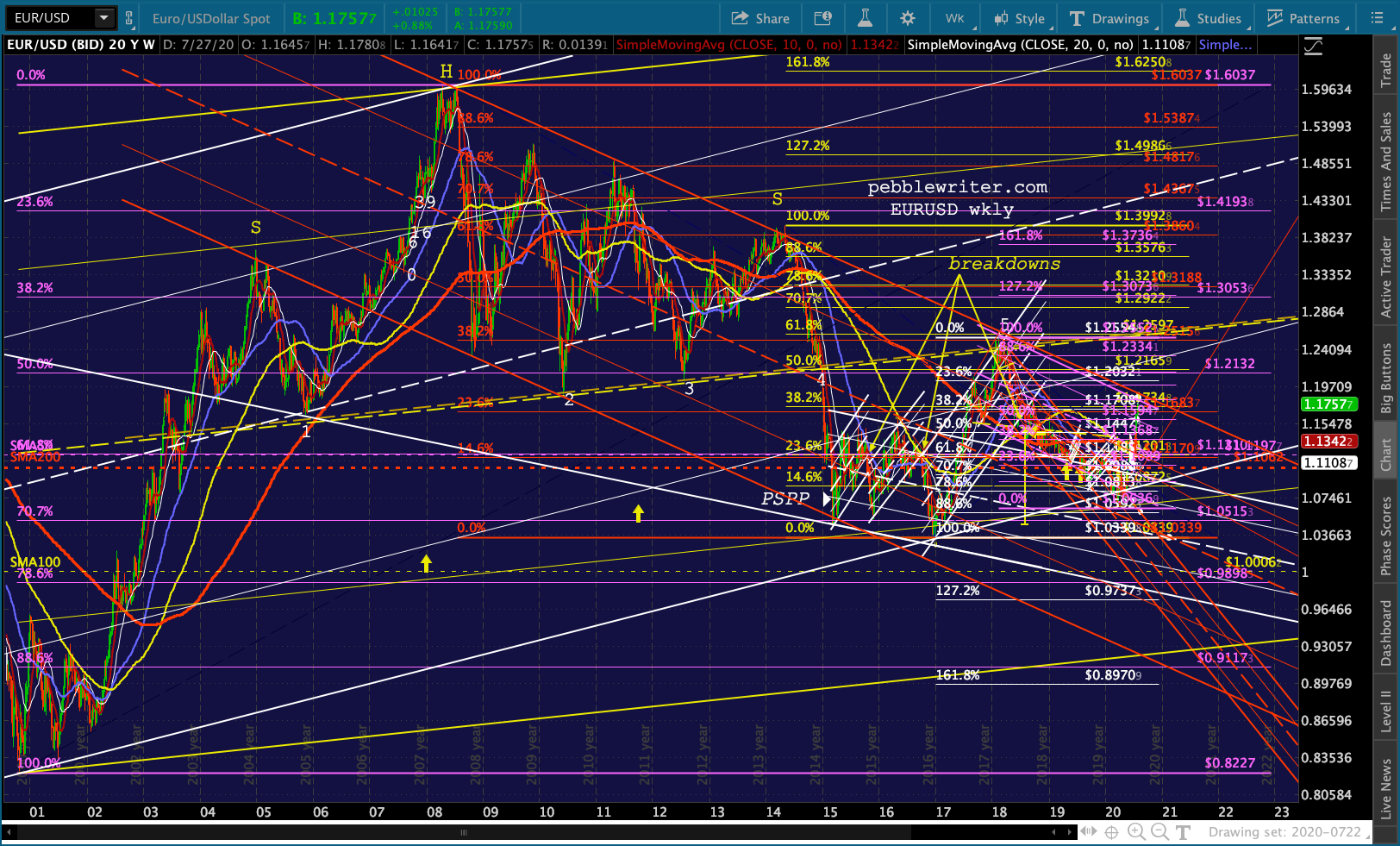

So, the current interest rate difference between US and euro-denominated debt is likely to persist and quite possibly expand – driving the EURUSD higher until the Fed cries “uncle.”

So, the current interest rate difference between US and euro-denominated debt is likely to persist and quite possibly expand – driving the EURUSD higher until the Fed cries “uncle.”

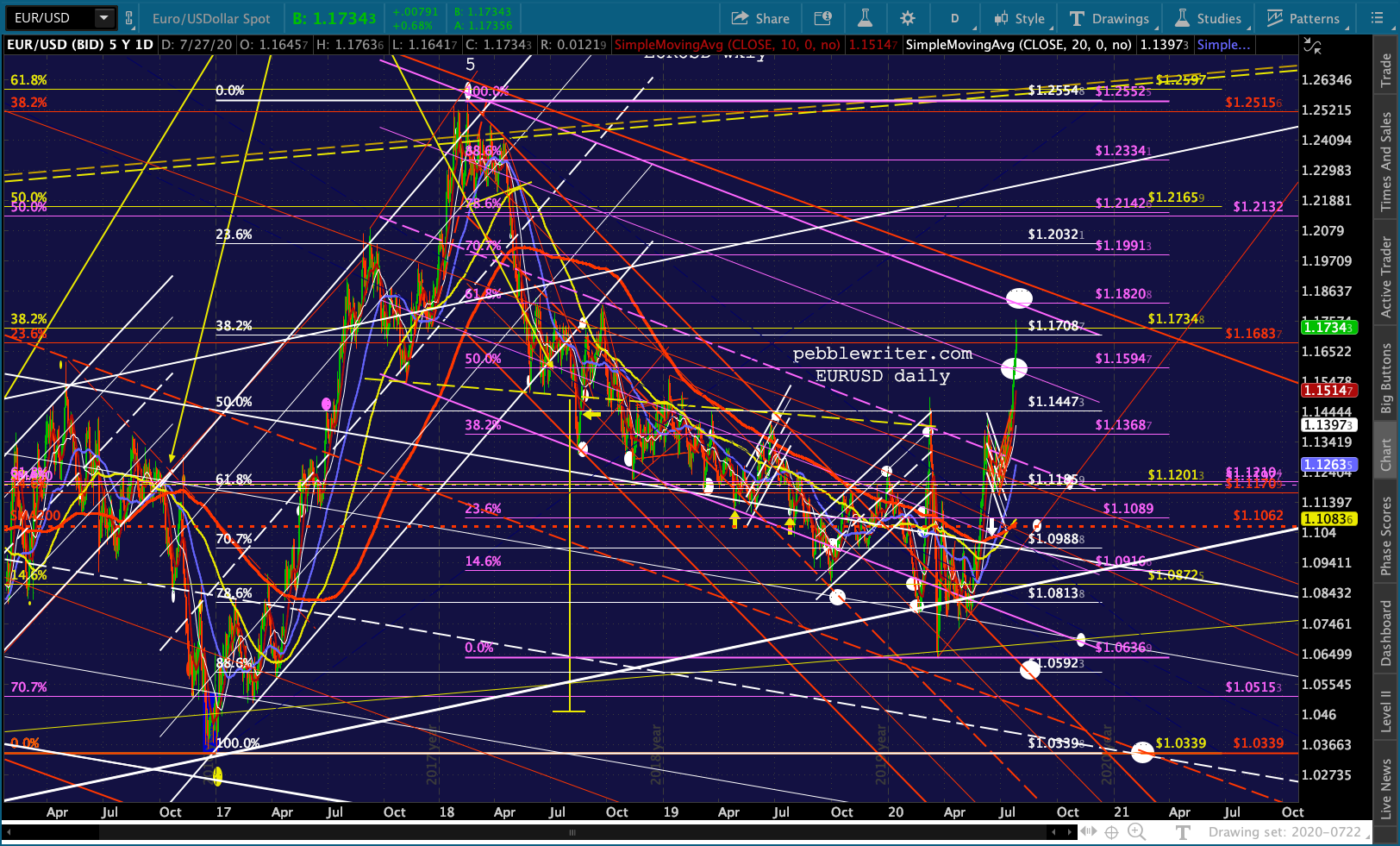

If the EURUSD pushes above the falling red channel shown above, it will have broken out of a trend dating back to 2006.

If the EURUSD pushes above the falling red channel shown above, it will have broken out of a trend dating back to 2006. When does equilibrium arrive? As a net importer, the US’s dollar demise will theoretically increase inflation which, again theoretically, would put more pressure on interest rates at some point. But, there’s a long way to go before import prices put pressure on CPI and rates.

When does equilibrium arrive? As a net importer, the US’s dollar demise will theoretically increase inflation which, again theoretically, would put more pressure on interest rates at some point. But, there’s a long way to go before import prices put pressure on CPI and rates.

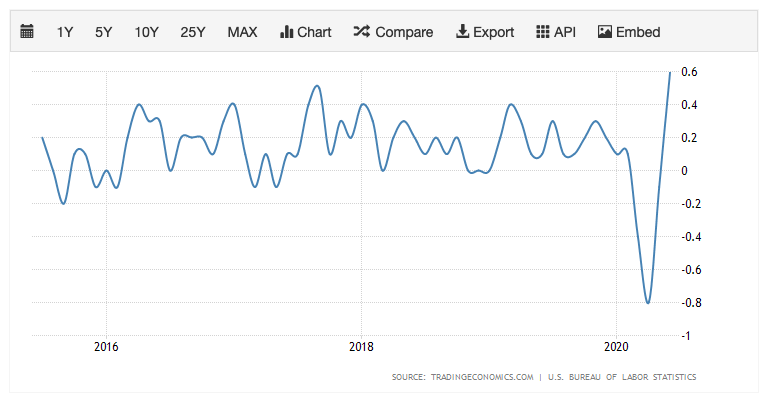

Monthly CPI shot up sharply last month, but primarily because of recovering oil and gas prices…

Monthly CPI shot up sharply last month, but primarily because of recovering oil and gas prices… …and, rising food prices.

…and, rising food prices.  The annual rate is still quite low, and the monthly rate will fall back toward historical norms unless oil and gas prices break out of the holding pattern they’ve been in since early May.

The annual rate is still quite low, and the monthly rate will fall back toward historical norms unless oil and gas prices break out of the holding pattern they’ve been in since early May.

The fact that GC is shooting up past its all-time highs is a clear indication that many investors think that inflation will continue to increase.

GLTA.