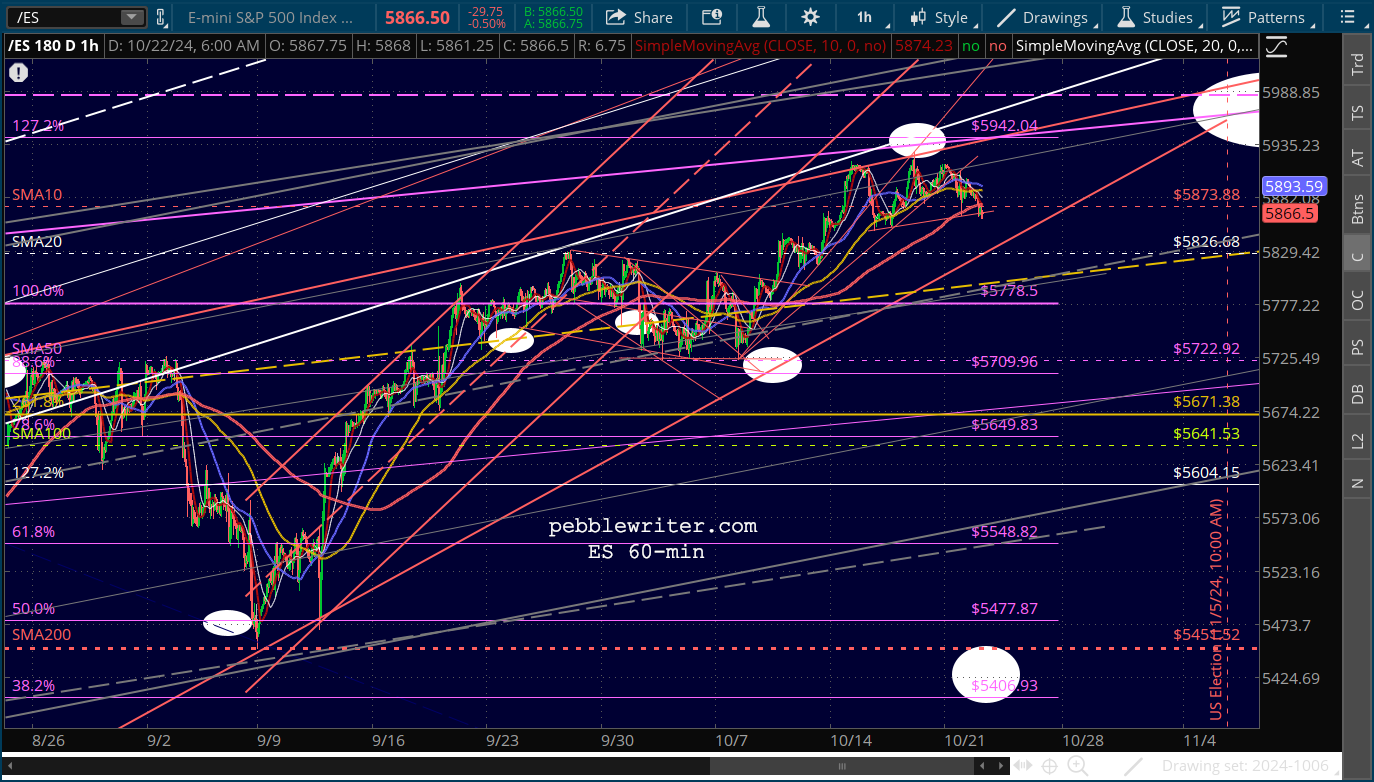

Futures are flirting with the 10-day moving average again this morning following yesterday’s volatile session.

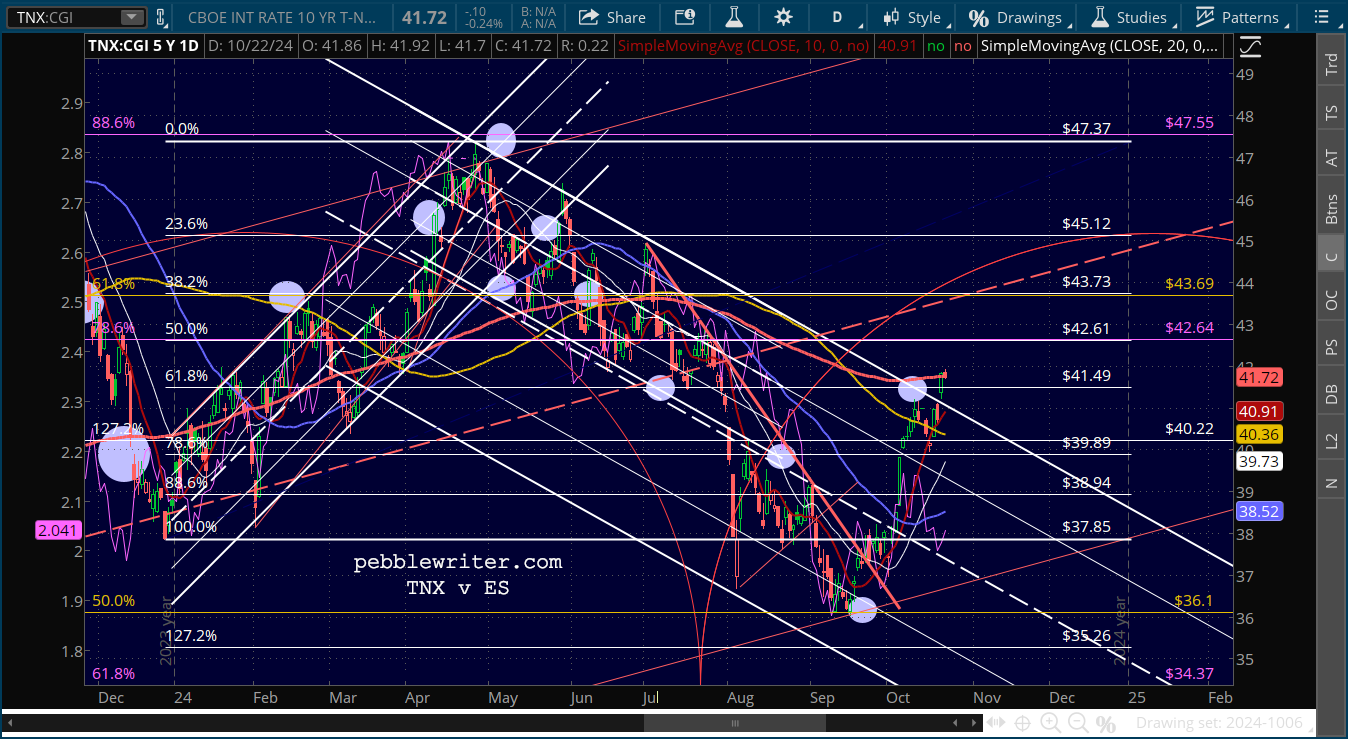

As we noted yesterday, the 10Y’s recent spurt has investors concerned about the risk that additional Fed rate cuts might not be as certain as bulls would like to believe.

As we noted yesterday, the 10Y’s recent spurt has investors concerned about the risk that additional Fed rate cuts might not be as certain as bulls would like to believe.

continued for members…

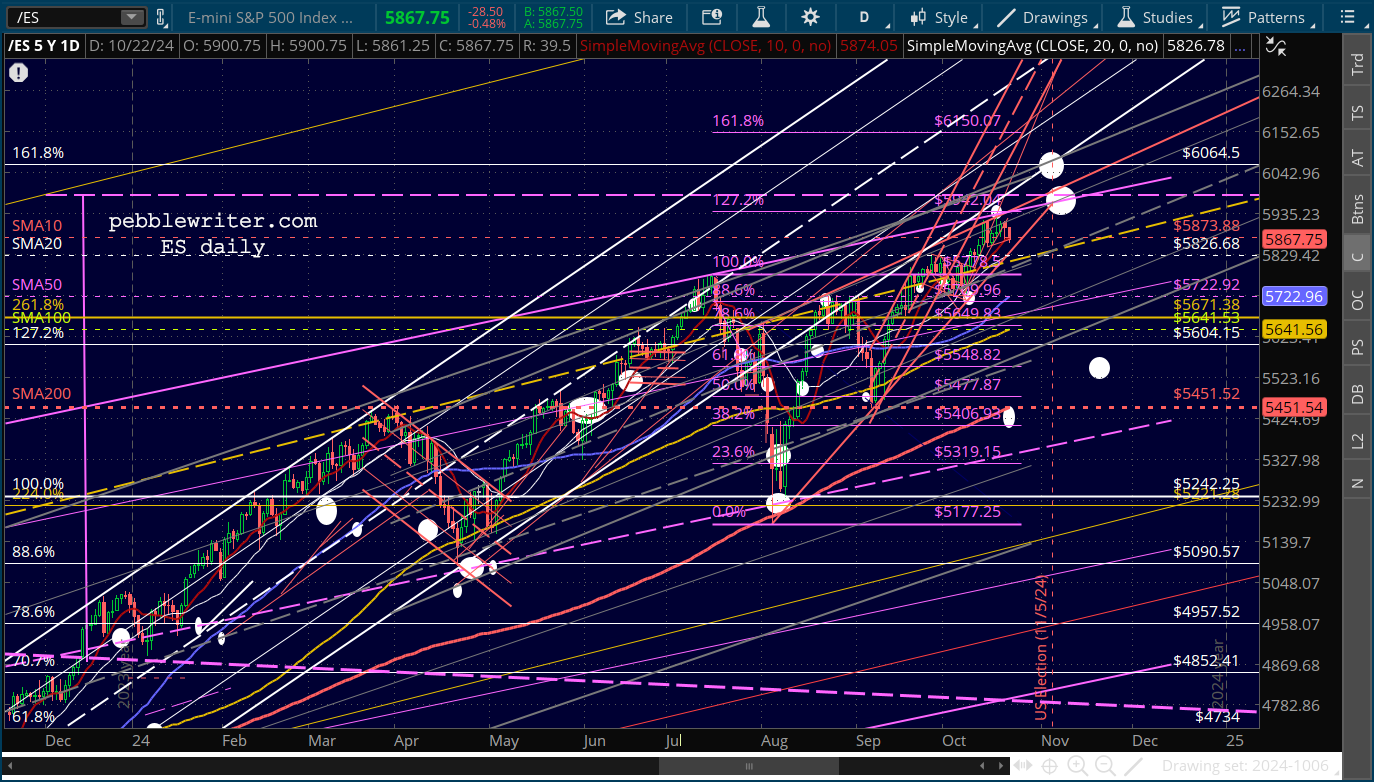

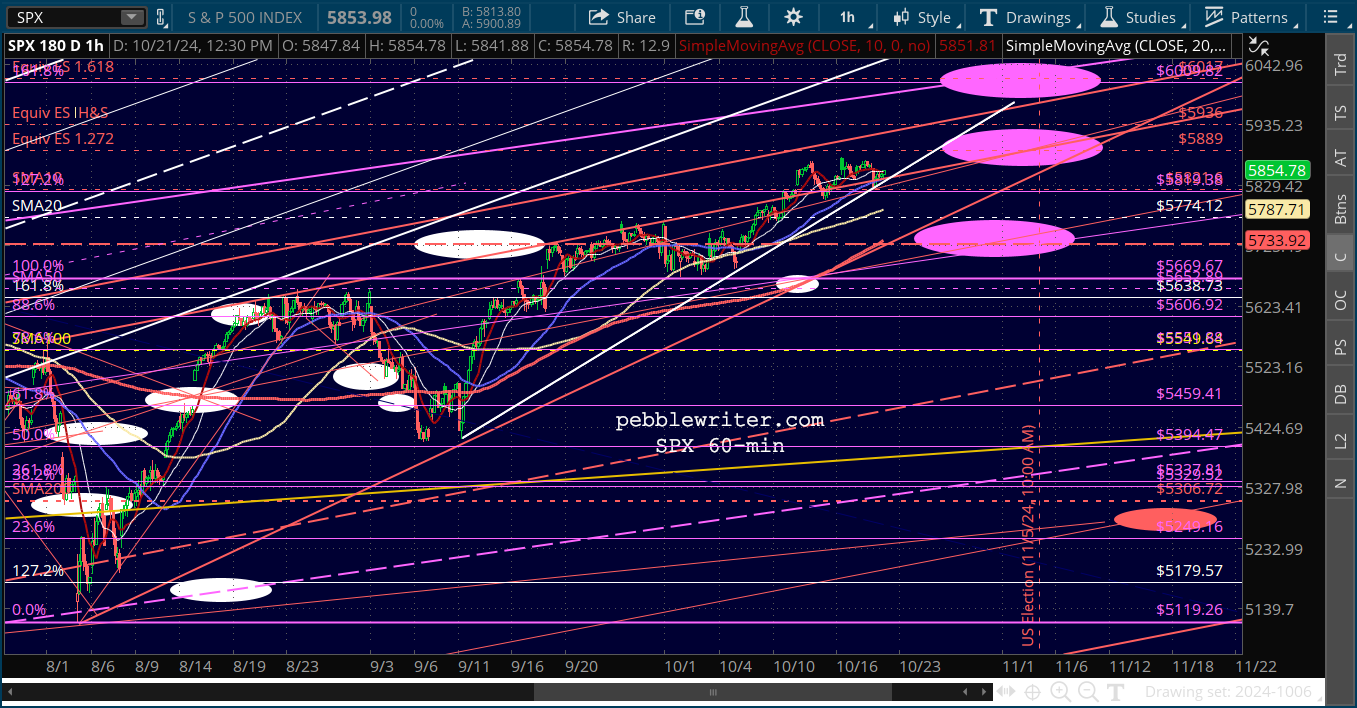

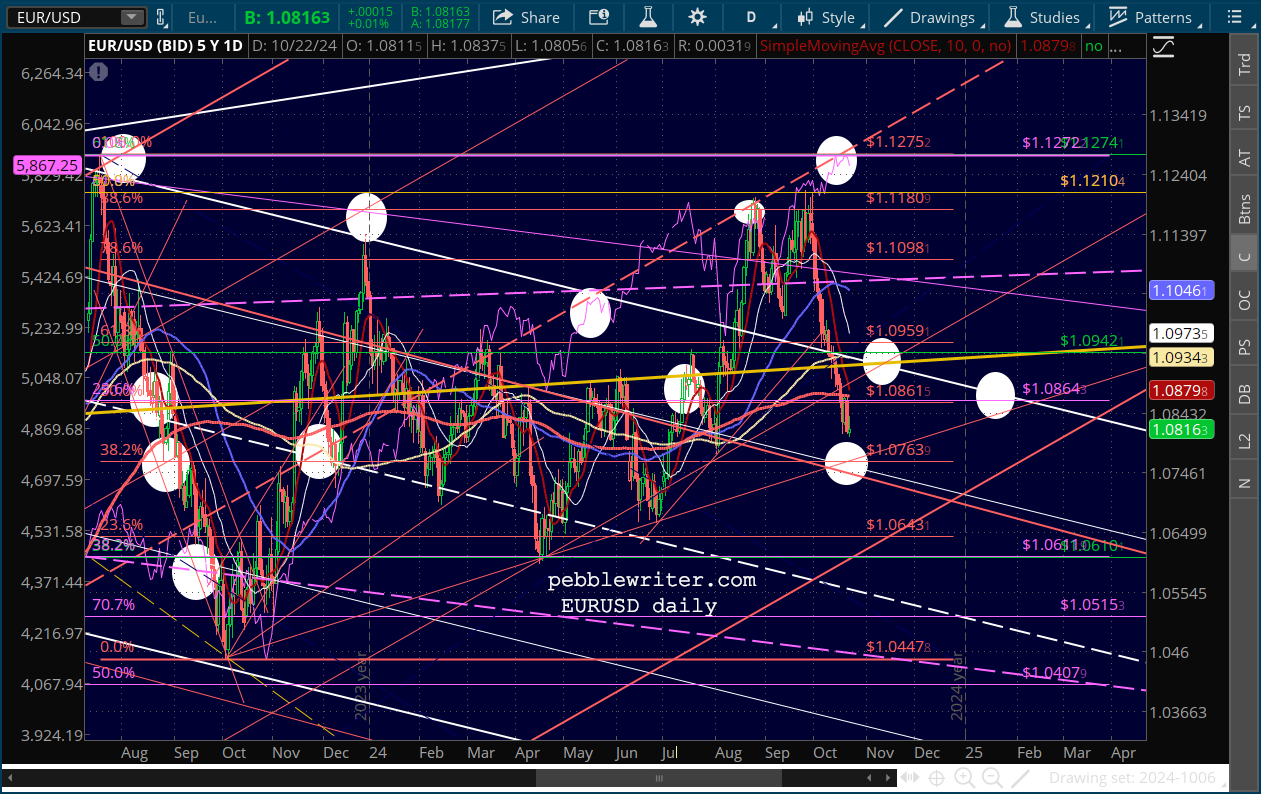

SPX could obviously slide a little more and still maintain the rising wedge that’s been in place for a while.

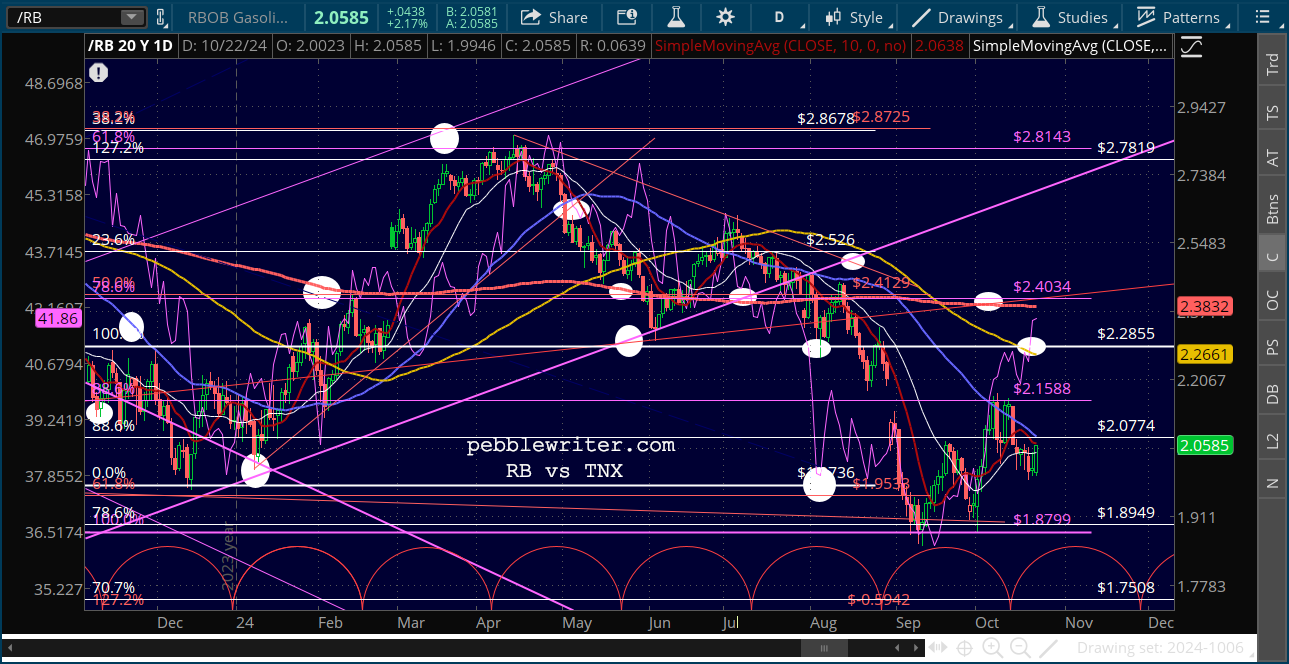

SPX could obviously slide a little more and still maintain the rising wedge that’s been in place for a while.  As we discussed yesterday, the 10Y is threatening to break out above the SMA200 and the falling white channel. The rise in interest rates reflects not only the actual but the aditional potential rise in oil and gas prices that would accompany a broadening of an Israel-Iran conflict.

As we discussed yesterday, the 10Y is threatening to break out above the SMA200 and the falling white channel. The rise in interest rates reflects not only the actual but the aditional potential rise in oil and gas prices that would accompany a broadening of an Israel-Iran conflict.

I have been expecting Israel to take advantage of the US election to more forcefully attack Iran, perhaps going after its nuclear facilities. Biden would be hard pressed to bring the hammer down – threatening to cut weapons and/or aid – on Israel for fear of alienating some voters prior to the election.

I have been expecting Israel to take advantage of the US election to more forcefully attack Iran, perhaps going after its nuclear facilities. Biden would be hard pressed to bring the hammer down – threatening to cut weapons and/or aid – on Israel for fear of alienating some voters prior to the election.

It’s an unfortunate reality that practically everything in government revolves around the election. But, it’s the reality we have to contend with. Two weeks to go…and then, of course, the post election complaints and legal battles which are sure to follow.

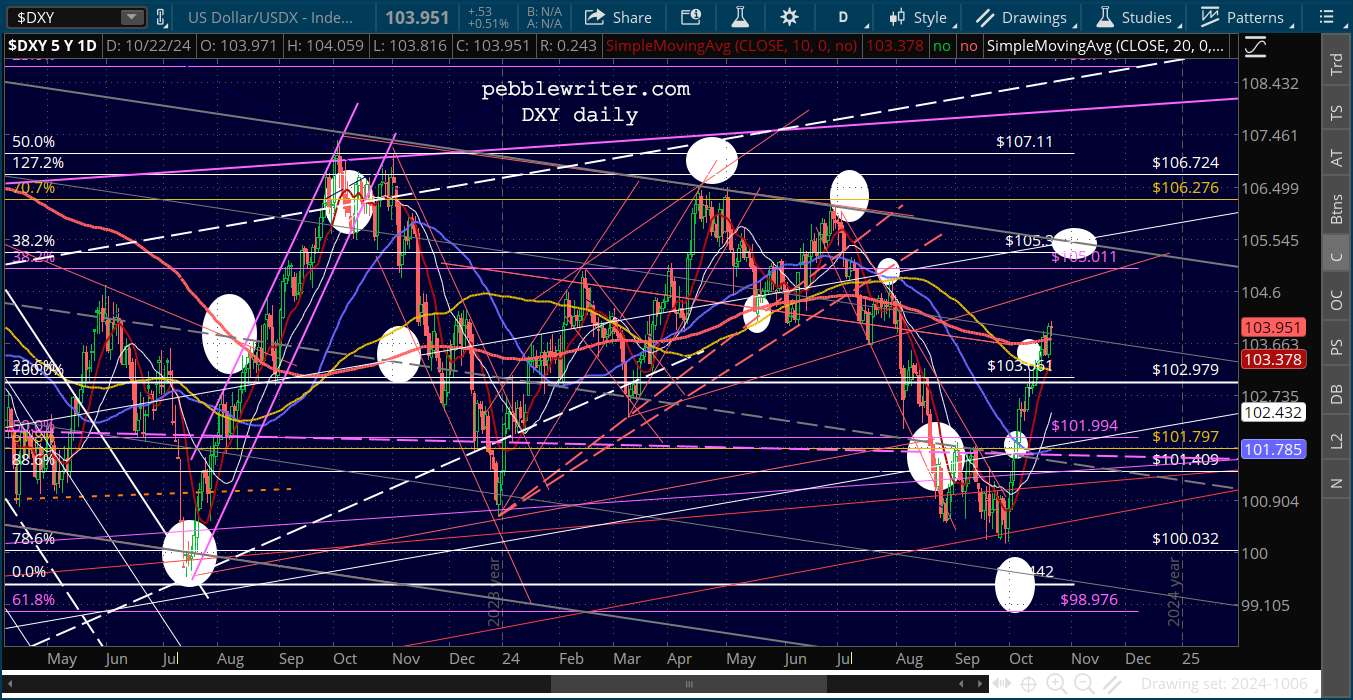

The market is also gnashing its teeth over the strength of the US dollar. Our charts show that the USD has almost reached a relatively important trend line which has presided over three previous bounces. There’s no reason to think it won’t provide another one in the next few days, which to me means that stocks will get one more chance to reach SPX 6009..

DXY could scoot up to the channel top target, but it needn’t do it without any futzing around at its SMA200.

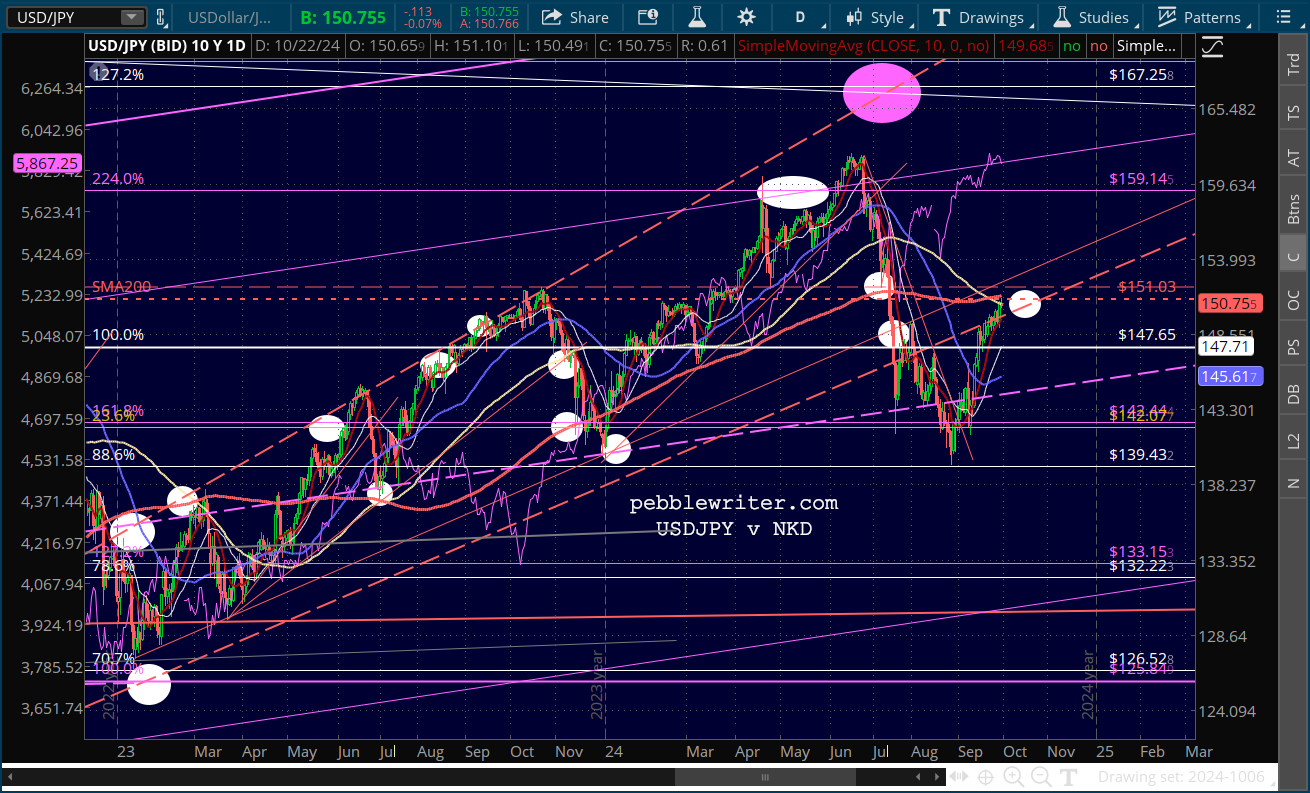

DXY could scoot up to the channel top target, but it needn’t do it without any futzing around at its SMA200. A lot of it will depend on what the BoJ does with this backtest. If they decide to further devalue the yen, then the waters would be very much muddied.

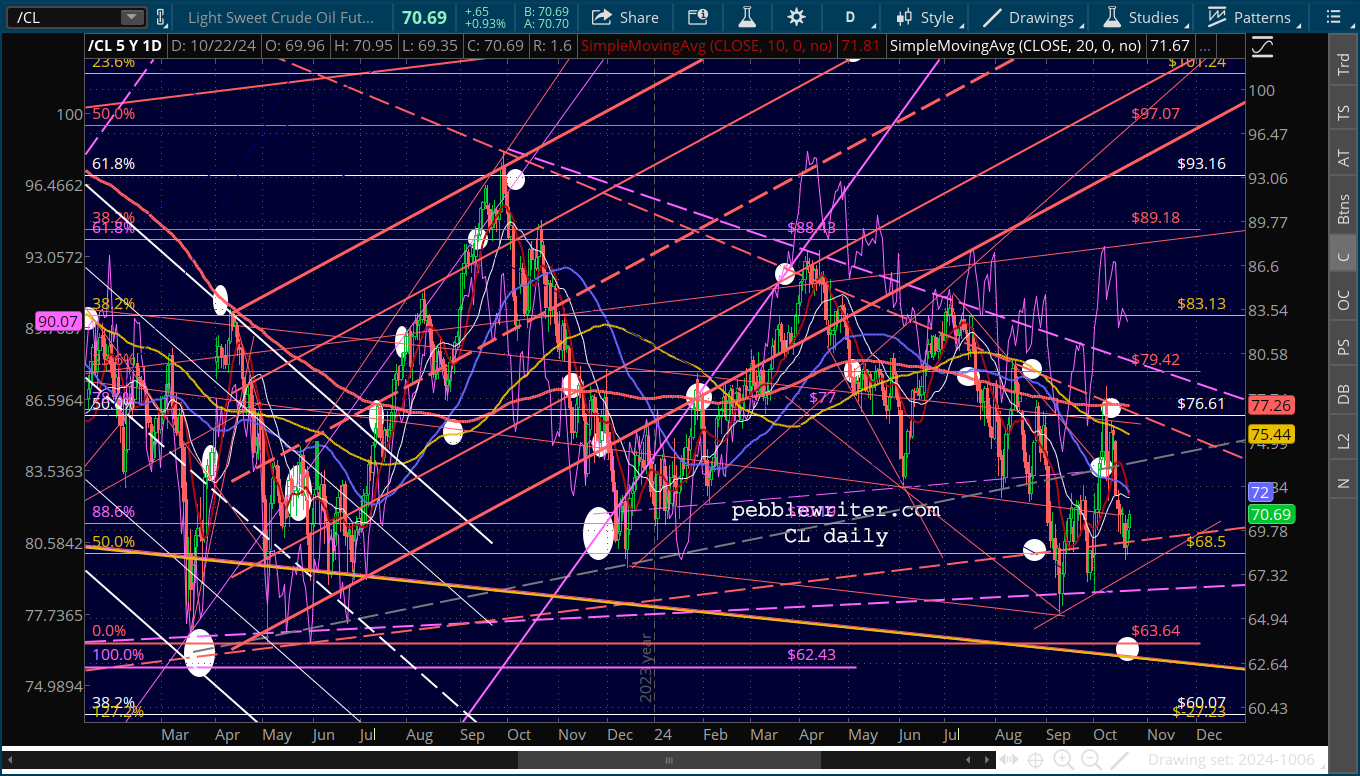

A lot of it will depend on what the BoJ does with this backtest. If they decide to further devalue the yen, then the waters would be very much muddied. For now, oil and gas prices continue to reflect the rising geopolitical risk in the Middle East and, if they don’t reverse soon, will mean a real tick up in inflation in October which we expect to be reported after the election.

For now, oil and gas prices continue to reflect the rising geopolitical risk in the Middle East and, if they don’t reverse soon, will mean a real tick up in inflation in October which we expect to be reported after the election.

Stay tuned…

Stay tuned…