Inflation was a little higher than expected, but initial claims were also higher than expected. Since the Fed’s emphasis has seemingly shifted to the employment side of the dual mandate question, this morning’s economic data supports the likelihood of a 50 bps rate cut either all at once next week or spread over the next two FOMC meetings.

A rate cut into a bull market pushing to all-time highs might seem odd. Especially when the index for all items less food and energy rose 3.1% again and services remain quite sticky at 3.6%. But, the correlation with YoY gas changes is still holding…

But, the correlation with YoY gas changes is still holding… …and sagging energy prices (-6.6% for gasoline!) are keeping headline inflation in check. It’s not so much that gas prices are much lower lately, just that the base effect is so strong. And, the tailwinds from the base effect are coming to an end.

…and sagging energy prices (-6.6% for gasoline!) are keeping headline inflation in check. It’s not so much that gas prices are much lower lately, just that the base effect is so strong. And, the tailwinds from the base effect are coming to an end.

Unless prices nosedive this is the last month when YoY price drop will be very substantial. Next month we should see a small drop, followed by increases.

Considering a 3.2% increase in food prices, steady commodity prices (subject to tariffs) and a 3.6% increase in services, CPI will likely rise for September. The only question is whether the BLS will report it truthfully…

Considering a 3.2% increase in food prices, steady commodity prices (subject to tariffs) and a 3.6% increase in services, CPI will likely rise for September. The only question is whether the BLS will report it truthfully…

But, let’s examine how the Fed might respond. First, the 10Y just tested 4%. So, the bond market is already doing the Fed’s job for it. Would a lower fed funds rate cause firms to fire fewer or hire more employees to offset the impact of AI? It’s clearly different this time.

For now, algos are responded as expected, following the dovish data and, of course, the VIX smackdown.

continued for members…

continued for members…

This allows ES to hold the latest TL…

…and SPX to remain above its 3.618 Fib.

…and SPX to remain above its 3.618 Fib.

The afore-mentioned VIX charts:

The afore-mentioned VIX charts:

DXY is slightly lower again.

DXY is slightly lower again.

…but note that USDJPY has gone nowhere since testing its SMA200. This doesn’t bode well for equities.

…but note that USDJPY has gone nowhere since testing its SMA200. This doesn’t bode well for equities.

I find it very difficult to believe that lower oil/gas prices will drive the 10Y below 4%, let alone our 3.25% target. It’s more than likely going to require an equity correction.

I find it very difficult to believe that lower oil/gas prices will drive the 10Y below 4%, let alone our 3.25% target. It’s more than likely going to require an equity correction.

Because while the Saudis have thus far accommodated Trump’s desire to bring down inflation via gas prices, they have drawn the line at the support offered by yellow channel backtest.

Note that CL bounced nicely on the yellow .618, but has exhibited little interest in dropping to the .786 at 33.

Note that CL bounced nicely on the yellow .618, but has exhibited little interest in dropping to the .786 at 33.

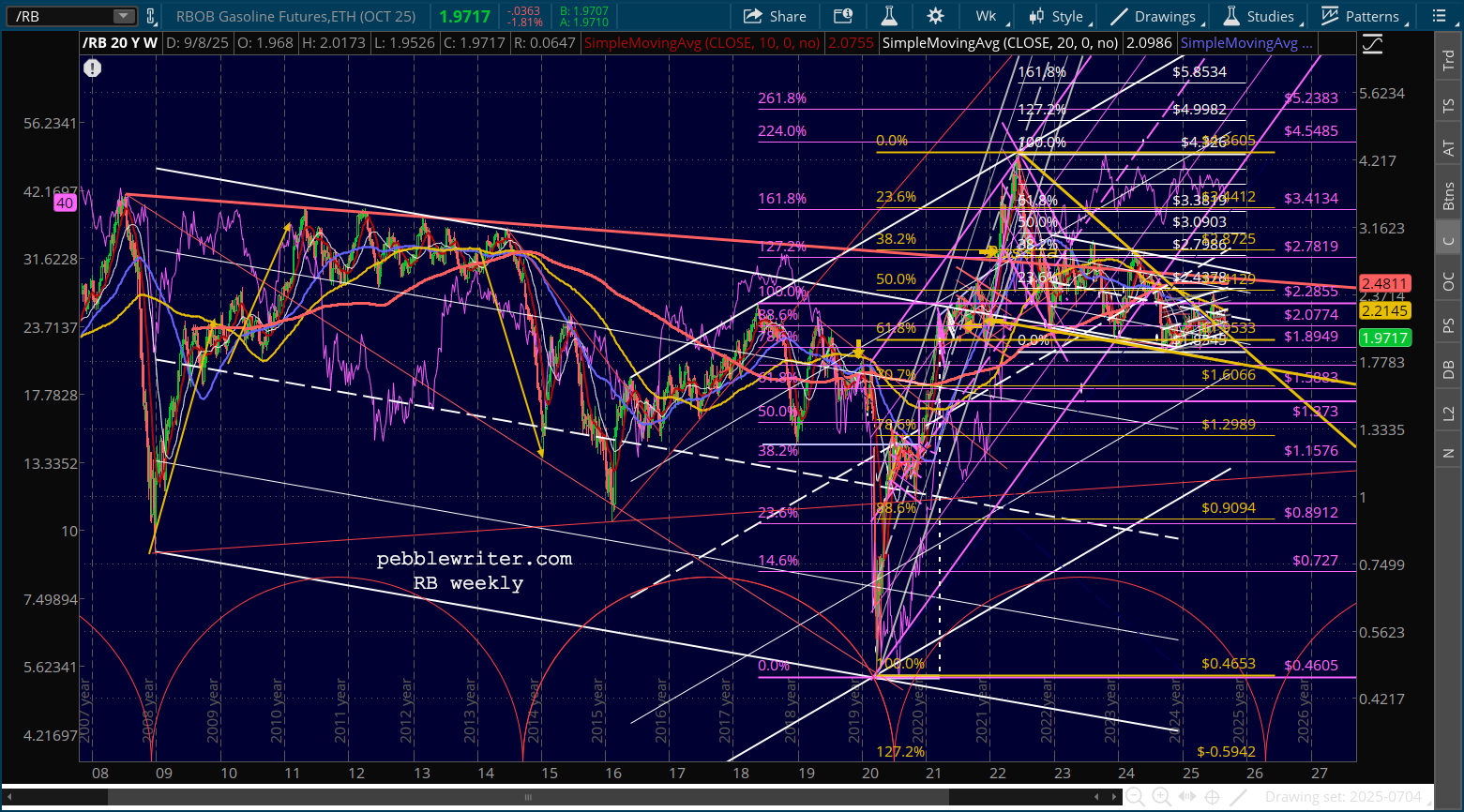

Likewise, while RB’s rising white channel broke down…

Likewise, while RB’s rising white channel broke down…

…it has bounced strongly off the yellow channel top and .618 at 1.95. The next stop in a Fib-driven breakdown would be the .707 at 1.60 or .786 at 1.30 – highly unlikely.

…it has bounced strongly off the yellow channel top and .618 at 1.95. The next stop in a Fib-driven breakdown would be the .707 at 1.60 or .786 at 1.30 – highly unlikely.

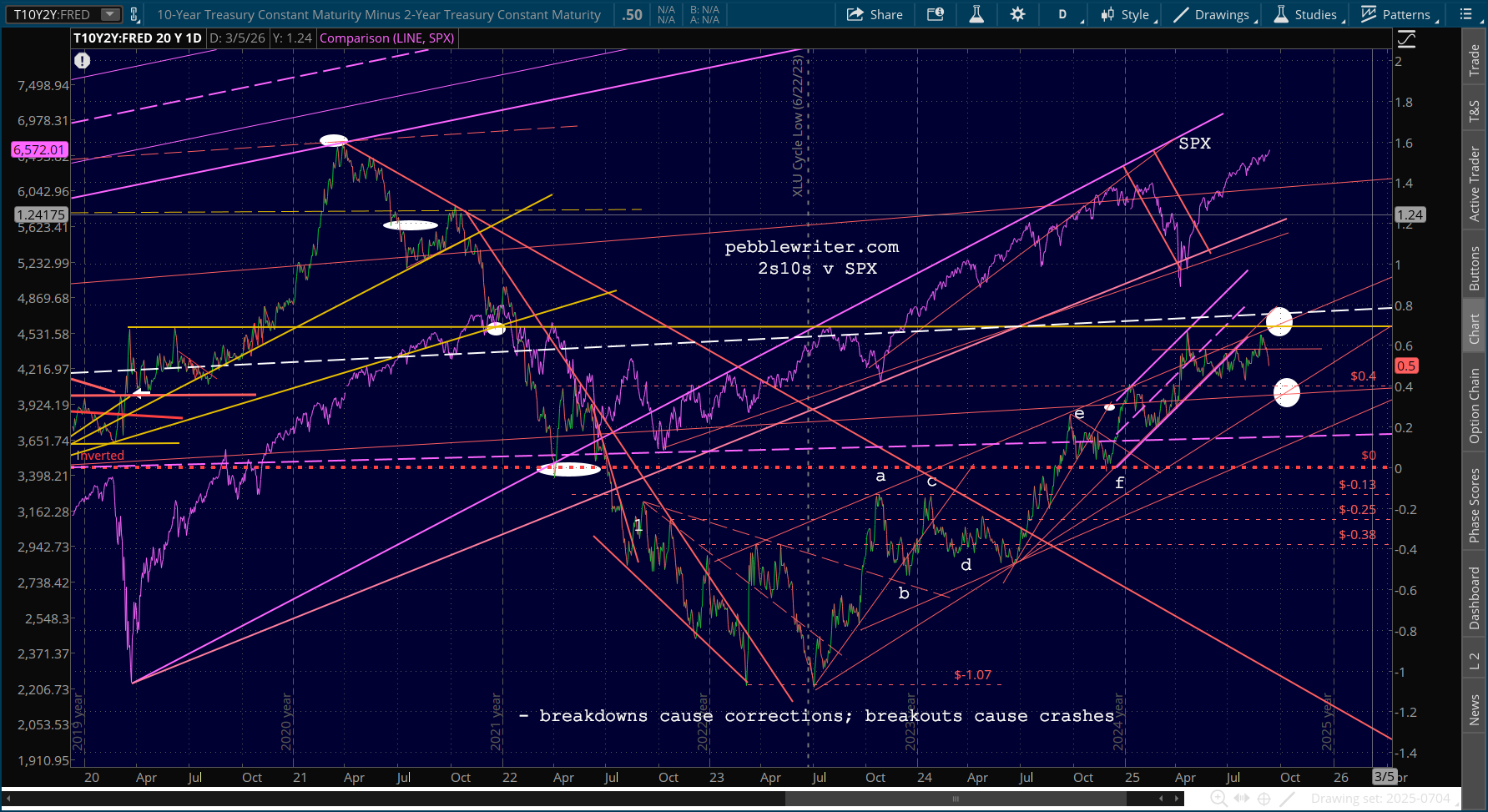

Last, we should keep an eye on the 2s10s. It has broken below the May and July highs and could soon test the June 43 bps lows. A drop through those levels would make a correction much more likely.

Last, we should keep an eye on the 2s10s. It has broken below the May and July highs and could soon test the June 43 bps lows. A drop through those levels would make a correction much more likely.

While I expect the 2Y to reach 3.3% fairly soon, the 10Y could take a while to break down below 4%. A rise in the 2s10s to 70 bps would mean a very tough equity environment.

Stay tuned.

Stay tuned.