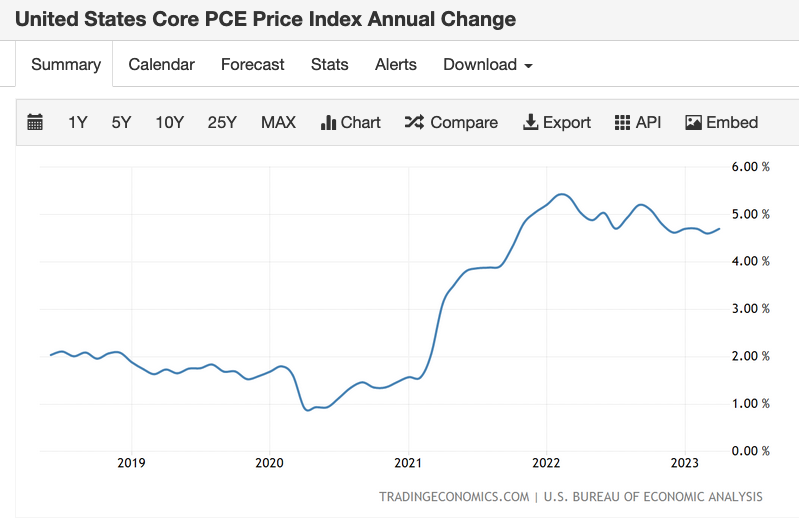

Substantial YoY drops in energy prices continue to dampen headline inflation…  …while core inflation gained 0.4% for the third month in a row.

…while core inflation gained 0.4% for the third month in a row.

The comparison between YoY gas prices and CPI illustrates the outsized influence energy prices have on headline inflation.

The comparison between YoY gas prices and CPI illustrates the outsized influence energy prices have on headline inflation.

Futures, however, popped on the print on the assumption that the Fed will pause its rate hikes despite hotter than expected PCE and employment data that would argue otherwise.

Futures, however, popped on the print on the assumption that the Fed will pause its rate hikes despite hotter than expected PCE and employment data that would argue otherwise.

continued for members…

continued for members…

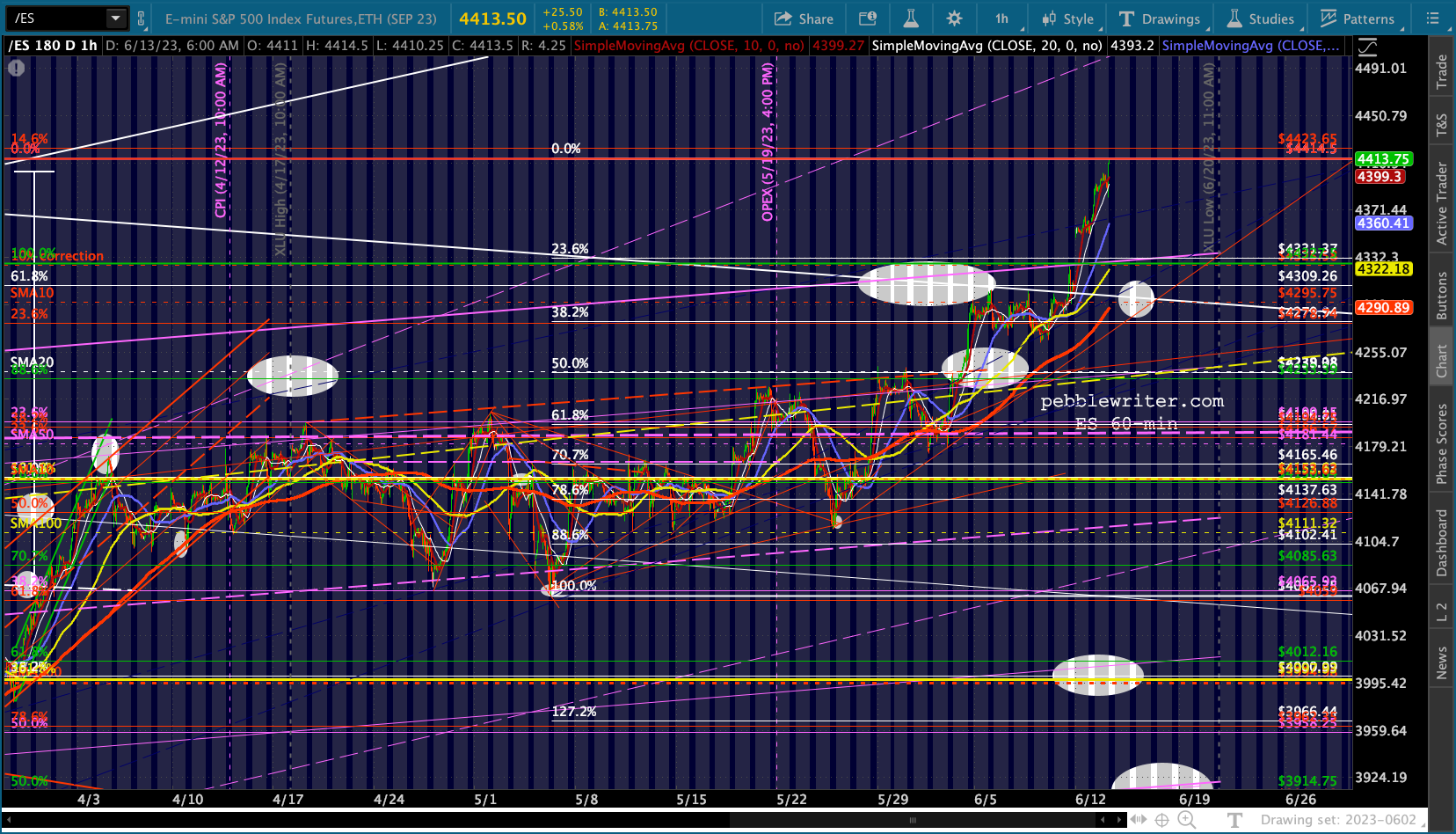

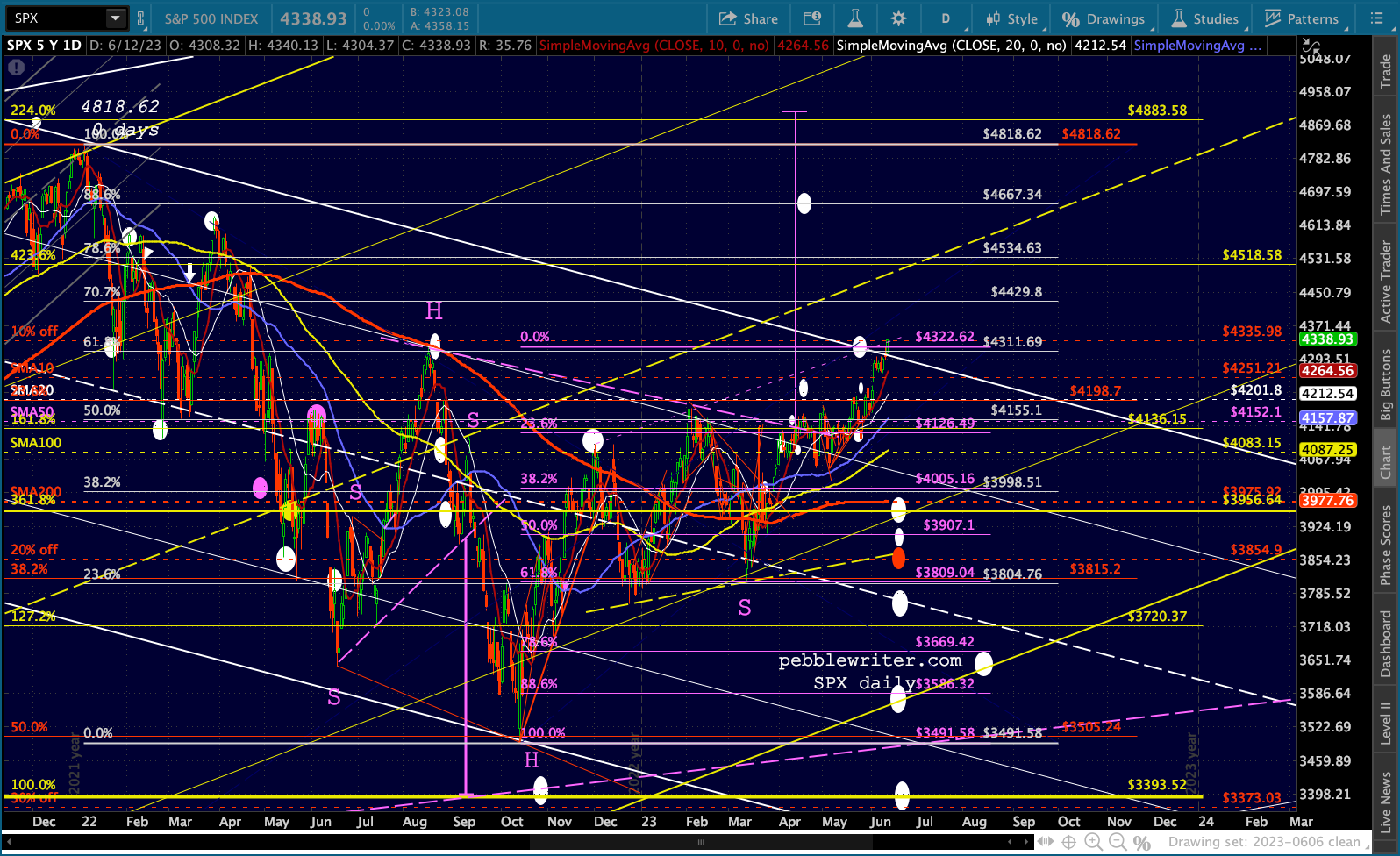

The equity picture: Since SPX and ES have both risen above their .618 Fib retracements, stocks are presumably free to pursue the .786s. But, of course, this assumes the Fed maintains an easing posture this week.

The equity picture: Since SPX and ES have both risen above their .618 Fib retracements, stocks are presumably free to pursue the .786s. But, of course, this assumes the Fed maintains an easing posture this week.

We say “easing” because interest rates remain below core inflation measures. Only by interest rates equaling or exceeding inflation can we say the Fed is tightening. Will the Fed admit to this approach? Probably not.

For now, they seem content to have the market continue its ascent even as they publicly wring their hands over persistently high inflation. It would be quite unusual for stocks to decline as the Fed decision approaches.

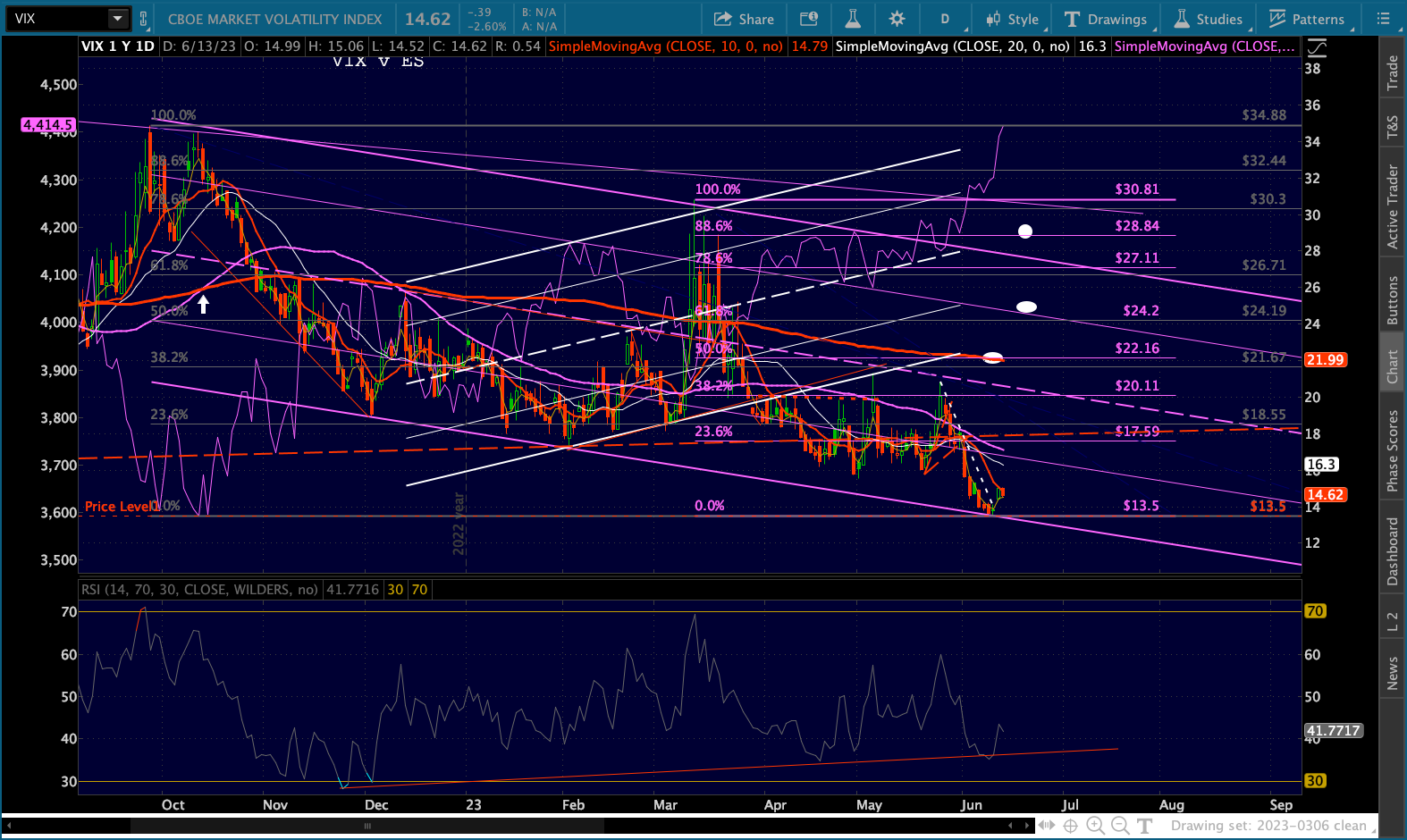

VIX is pulling back from yesterday’s gains and has the potential to close the gap at 14.14.

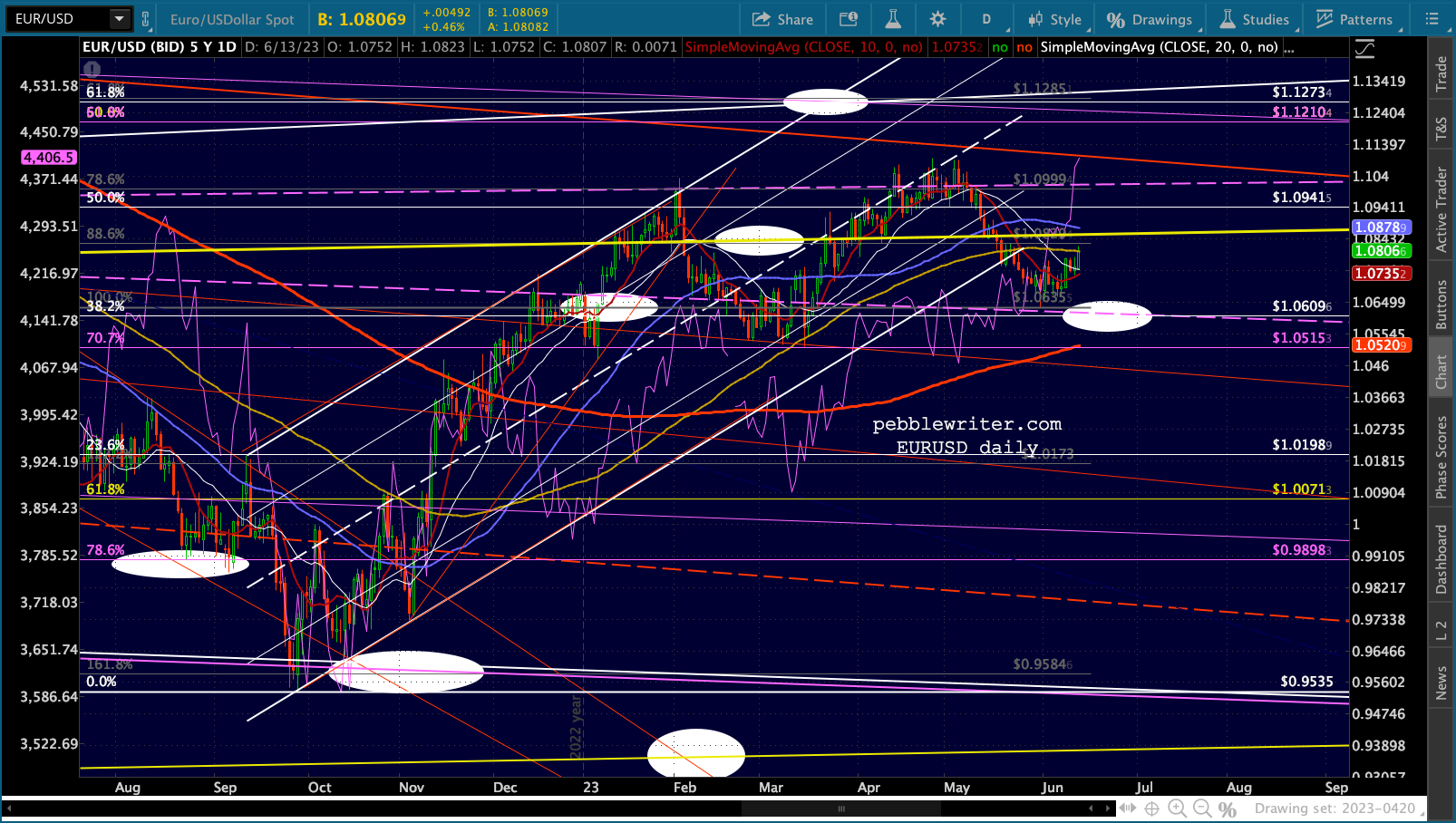

VIX is pulling back from yesterday’s gains and has the potential to close the gap at 14.14. Currencies favor stocks this morning with EURUSD continuing a slight bounce and anticipating a bullish 10/20 cross…

Currencies favor stocks this morning with EURUSD continuing a slight bounce and anticipating a bullish 10/20 cross…

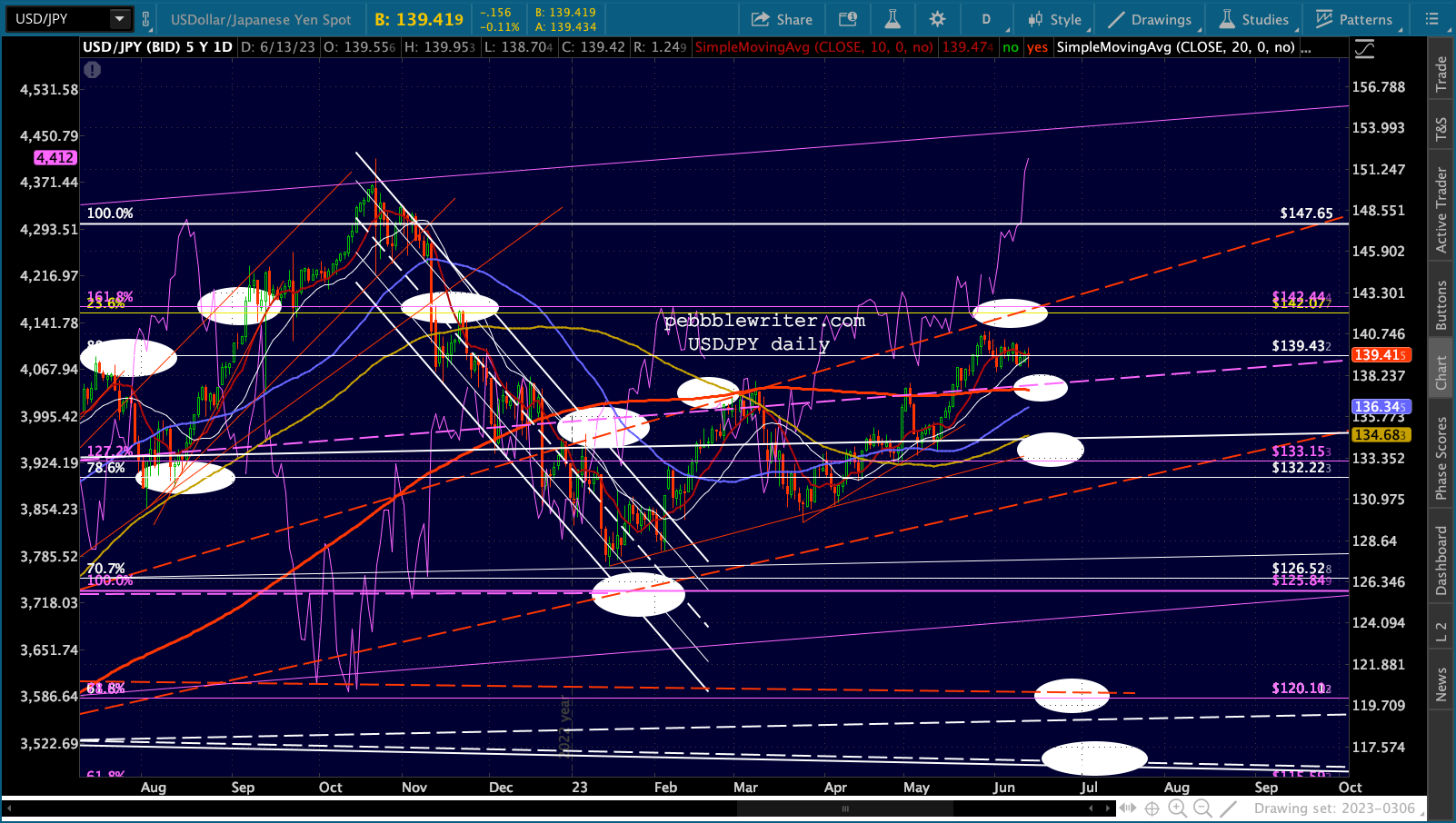

…while USDJPY hints at a bearish 10/20 cross.

…while USDJPY hints at a bearish 10/20 cross.

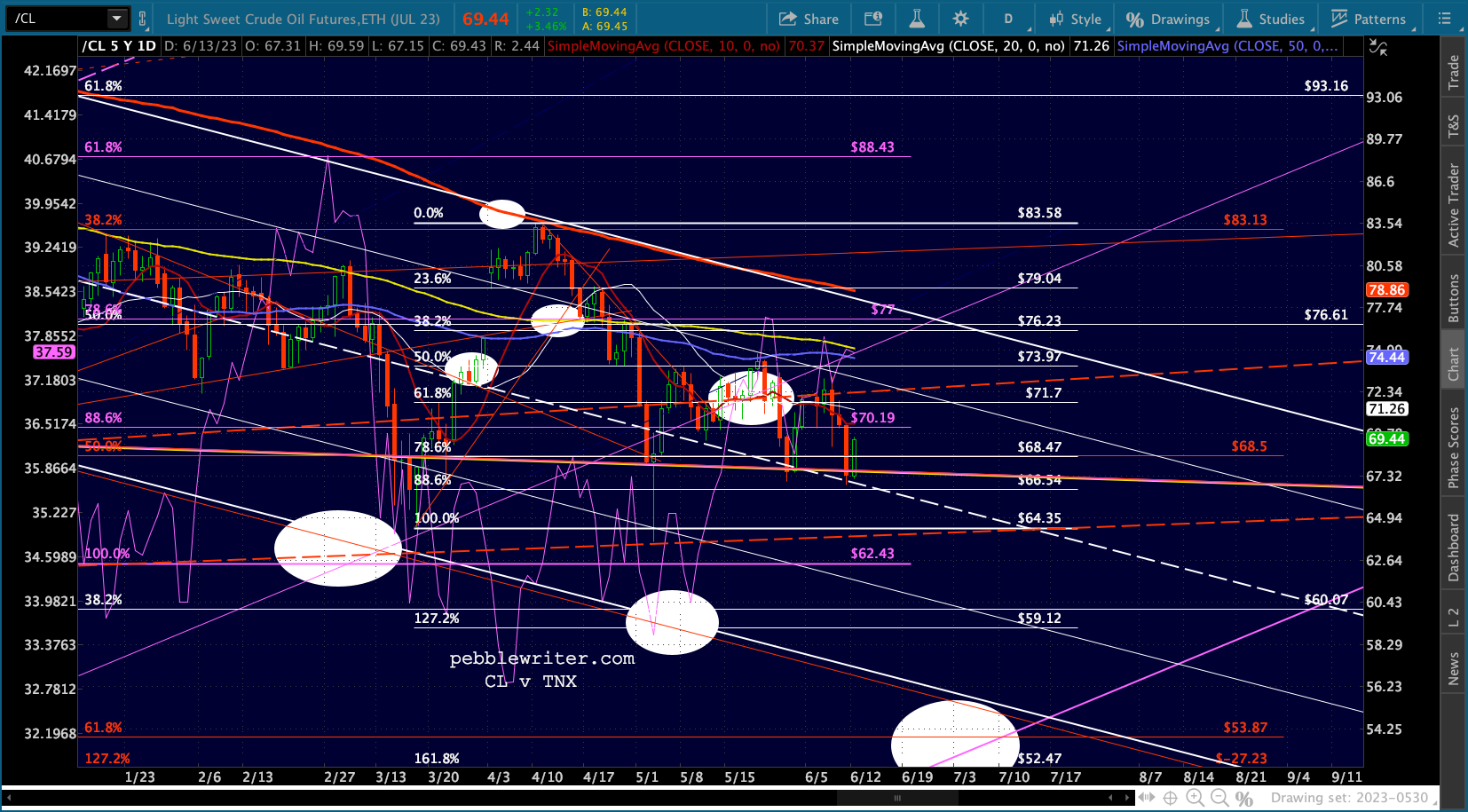

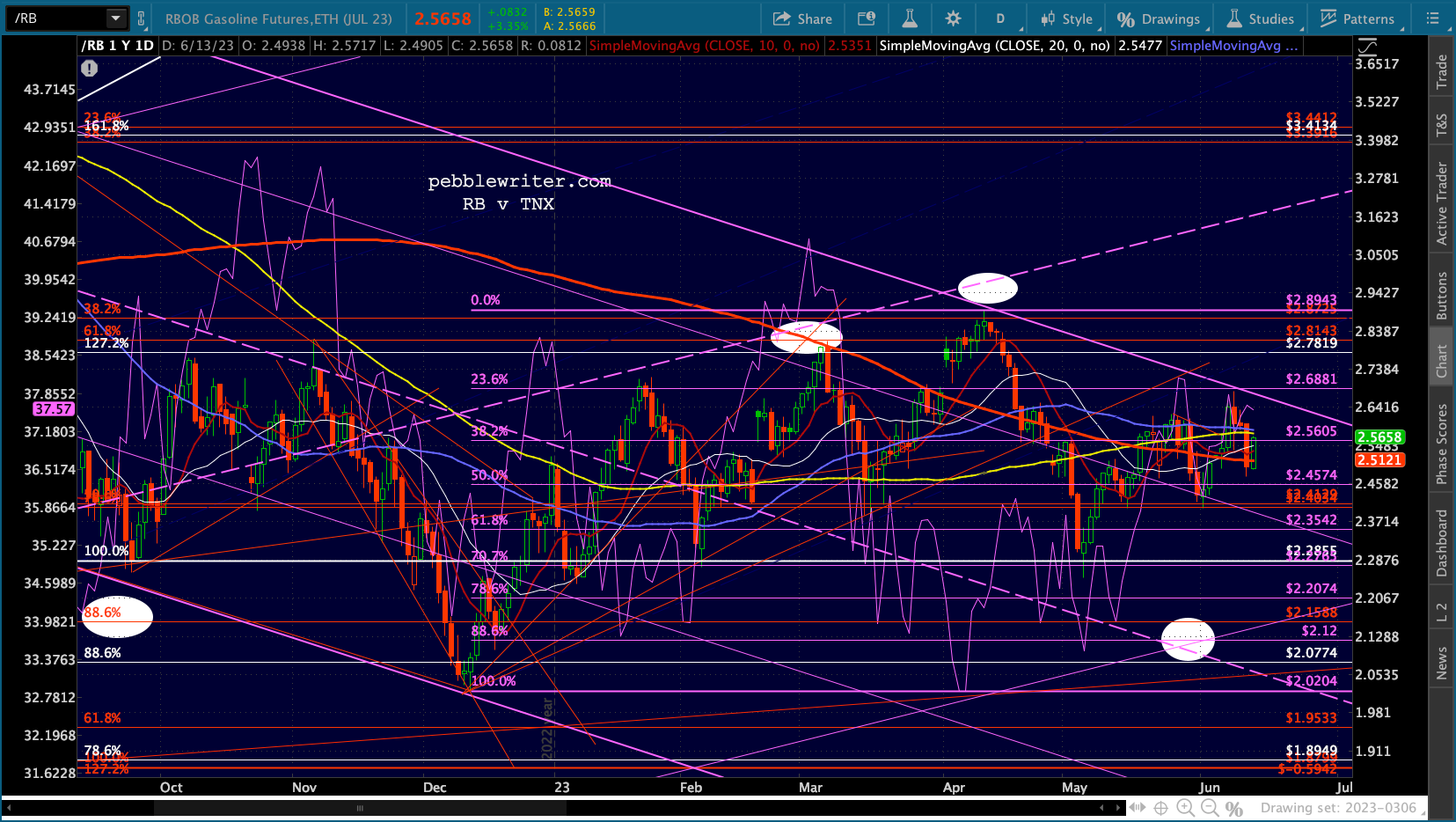

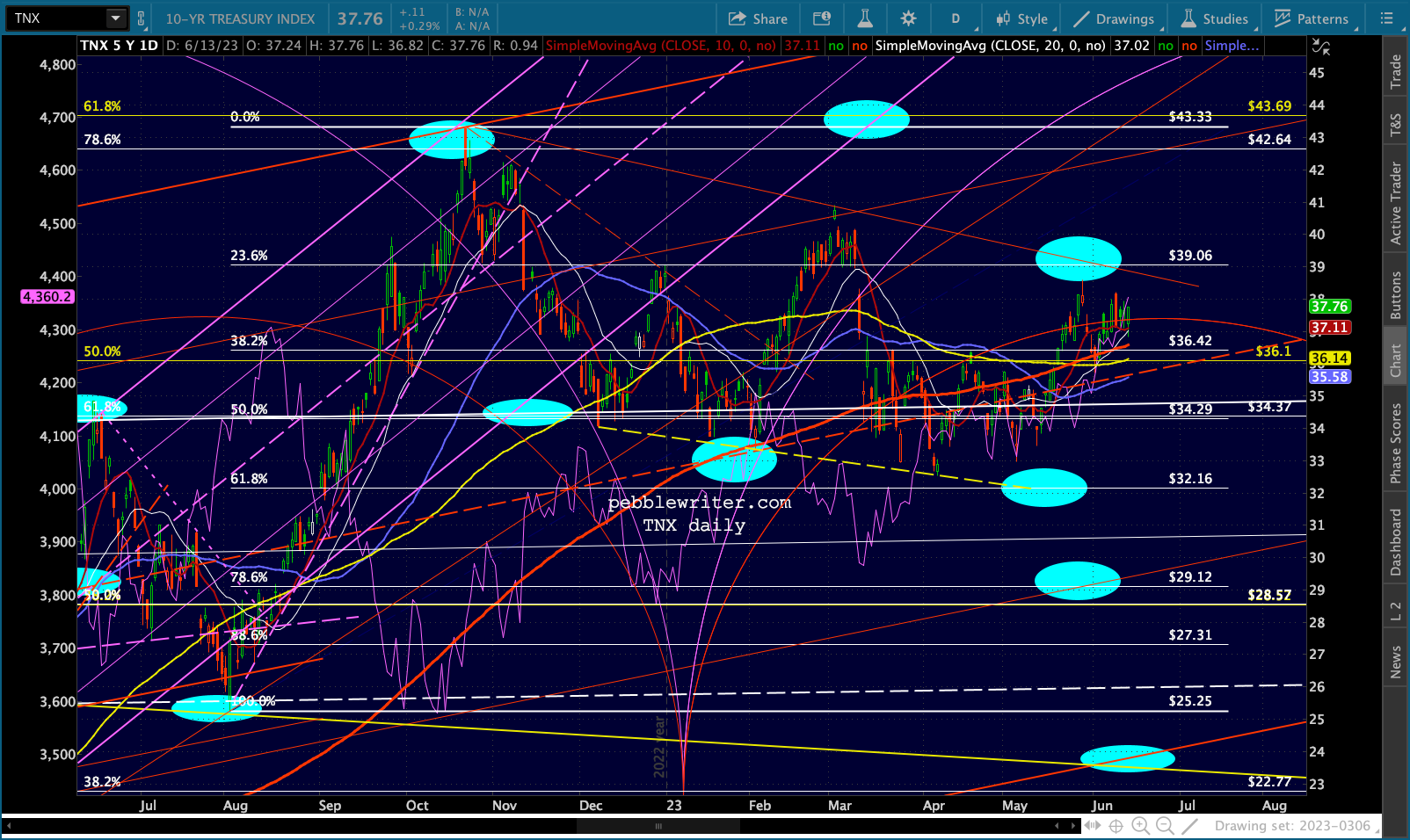

Algos are also getting a boost from recovering oil and gas prices…

Algos are also getting a boost from recovering oil and gas prices…

…which have slightly boosted the 10Y as it maintains a bullish 10/20 configuration.

…which have slightly boosted the 10Y as it maintains a bullish 10/20 configuration.

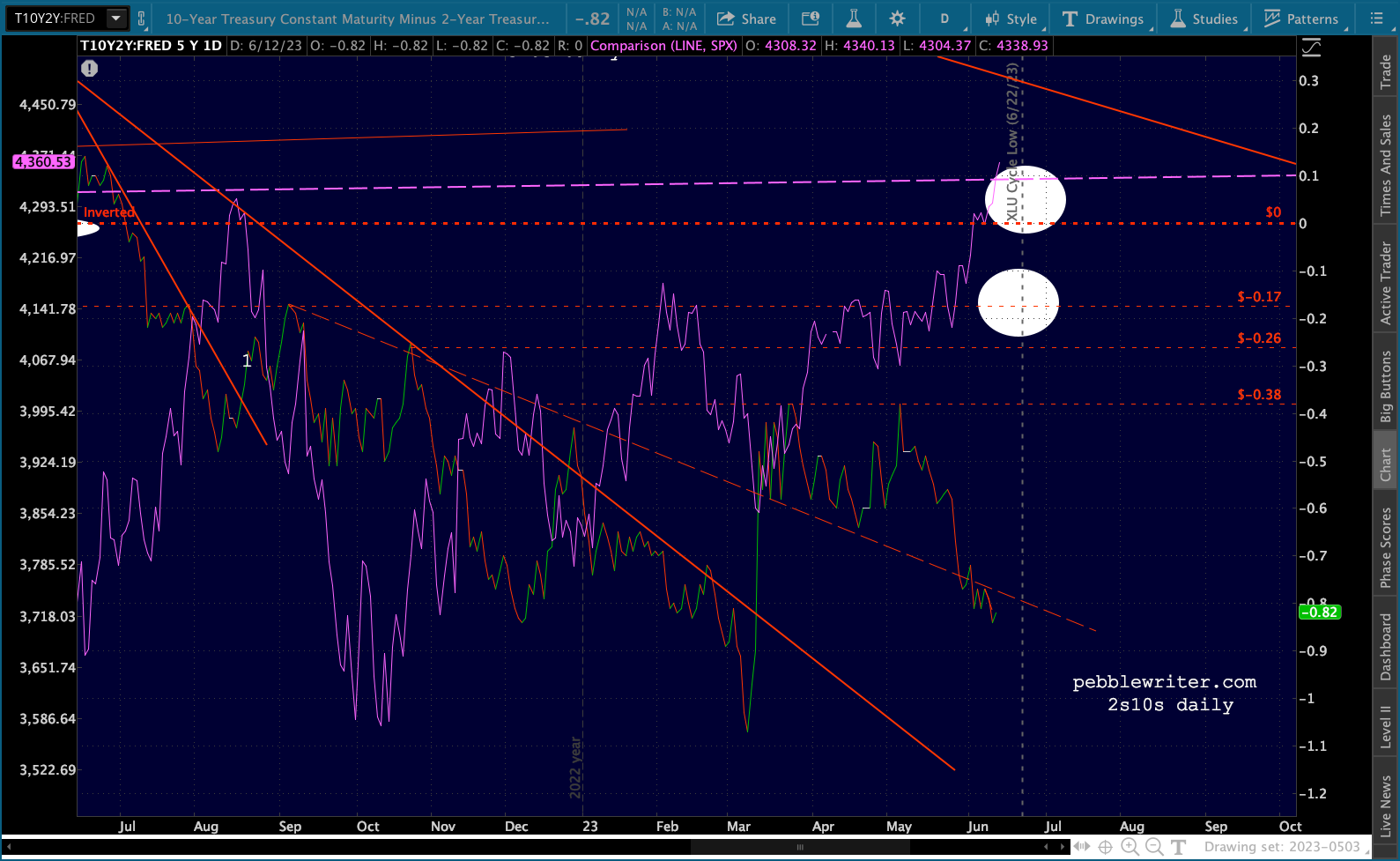

The 2s10s continues to test the Dec 2022 lows.

The 2s10s continues to test the Dec 2022 lows.

Stay tuned…