On the third page of Jay Powell’s prepared remarks yesterday, he finally touches on inflation’s effect on ordinary Americans:

We understand that high inflation imposes significant hardship, especially on those least able to meet the higher costs of essentials like food, housing, and transportation. We are committed to our price stability goal. We will use our tools both to support the economy and a strong labor market and to prevent higher inflation from becoming entrenched. We will be watching carefully to see whether the economy is evolving in line with expectations.

I’m sure that’s a relief to everyone trying to decide between putting food on the table or gas in the car or paying the rent check – all of which have increased by 10-60% over the past year. Pay no attention to your troubles, the Fed will be watching to see if they get any worse.

One of the best questions in the Q&A came from CNBC’s Steve Liesman:

It’s often said that monetary policy has long and variable lags. How does continuing to buy assets now, even though it’s at a slower pace, address the current inflation problem? Won’t the impact of today’s changes not really have any impact for six months or a year down the road on the current inflation problem, and aren’t you actually lengthening that time by continuing to buy assets when it could be not until the long and variable lag after you end purchases sometime in March that you’ll start to have any impact on the inflation problem?

Powell read the prepared answer (actually non-answer) from his notes. Completely ignoring the question posed by Liesman, it possessed all the intellectual merit of a parent exclaiming “because I said so.” Added emphasis is mine.

…why not stop purchasing now? …We’ve learned that in dealing with balance sheet issues…that it’s best to take a careful, methodical approach to make adjustments. Markets can be sensitive to it. And, we thought that this was a doubling of the speed, we’re just two meetings away from finishing the taper, we thought that was the appropriate way to go, so we announced it and that’s what will happen.

In this world where the global financial markets are connected together, financial conditions can change very quickly and my own sense is that they get into conditions that the affect the economy fairly rapidly, longer than the traditional thought of a year or 18 months – shorter than that rather – and when we communicate what we’re going to do, the markets move immediately to that. So, financial conditions are changing to reflect the forecast that we made, which was basically in line with what the markets were expecting.

I was a little surprised he didn’t grab a golf club at that point and say “now watch this drive.”

If you got to the end of that word salad and are still wondering why, in the midst of record breaking inflation, the Fed is continuing to throw hundreds of billions into an already overpriced market, there’s your answer: the market. Everything else, including the suffering of those slammed by inflation, is secondary.

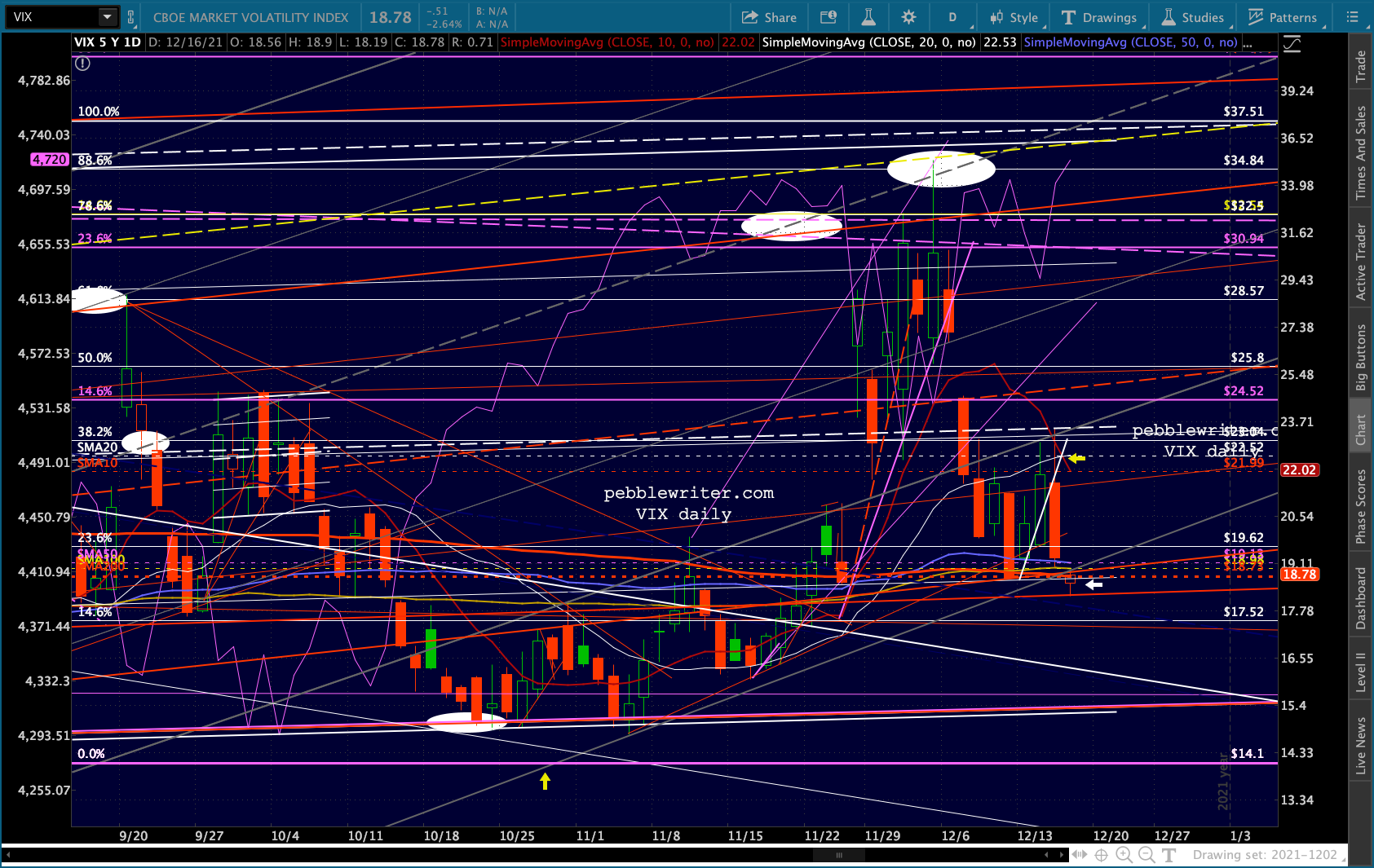

Meanwhile, the real target of the Fed’s policy – the algos – were thrilled by the lack of surprises and, most importantly, by the crushing blow dealt to vol. As we discussed yesterday, VIX broke down below the latest straw man trend line… …and put in a bearish 10/20 cross. Oh, and it gapped down below the 200-day moving average just for good measure.

…and put in a bearish 10/20 cross. Oh, and it gapped down below the 200-day moving average just for good measure.

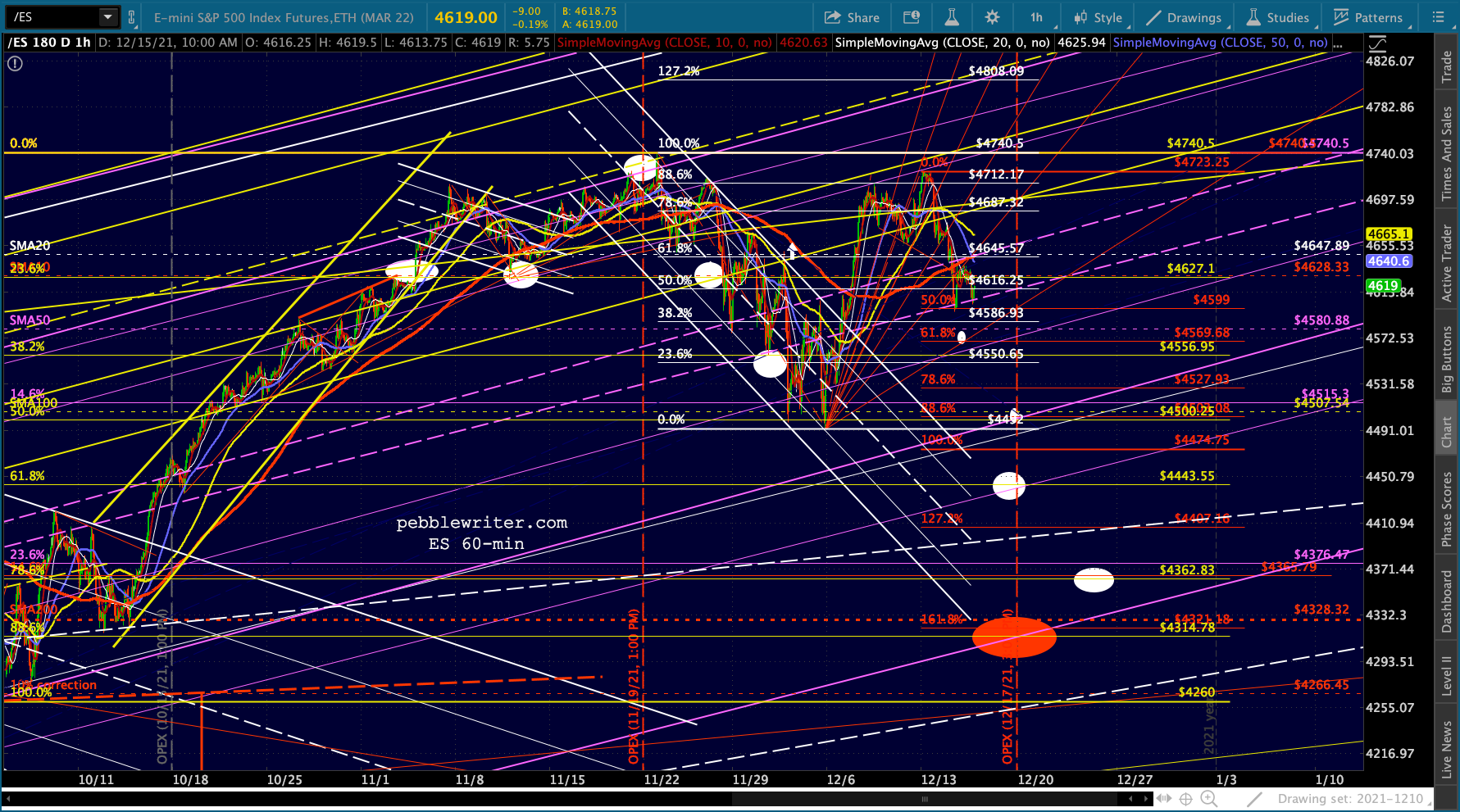

All better and new all-time highs (coincidentally just above stops) for ES just in time for OPEX. Just don’t call it a bubble.

All better and new all-time highs (coincidentally just above stops) for ES just in time for OPEX. Just don’t call it a bubble.

continued for members…

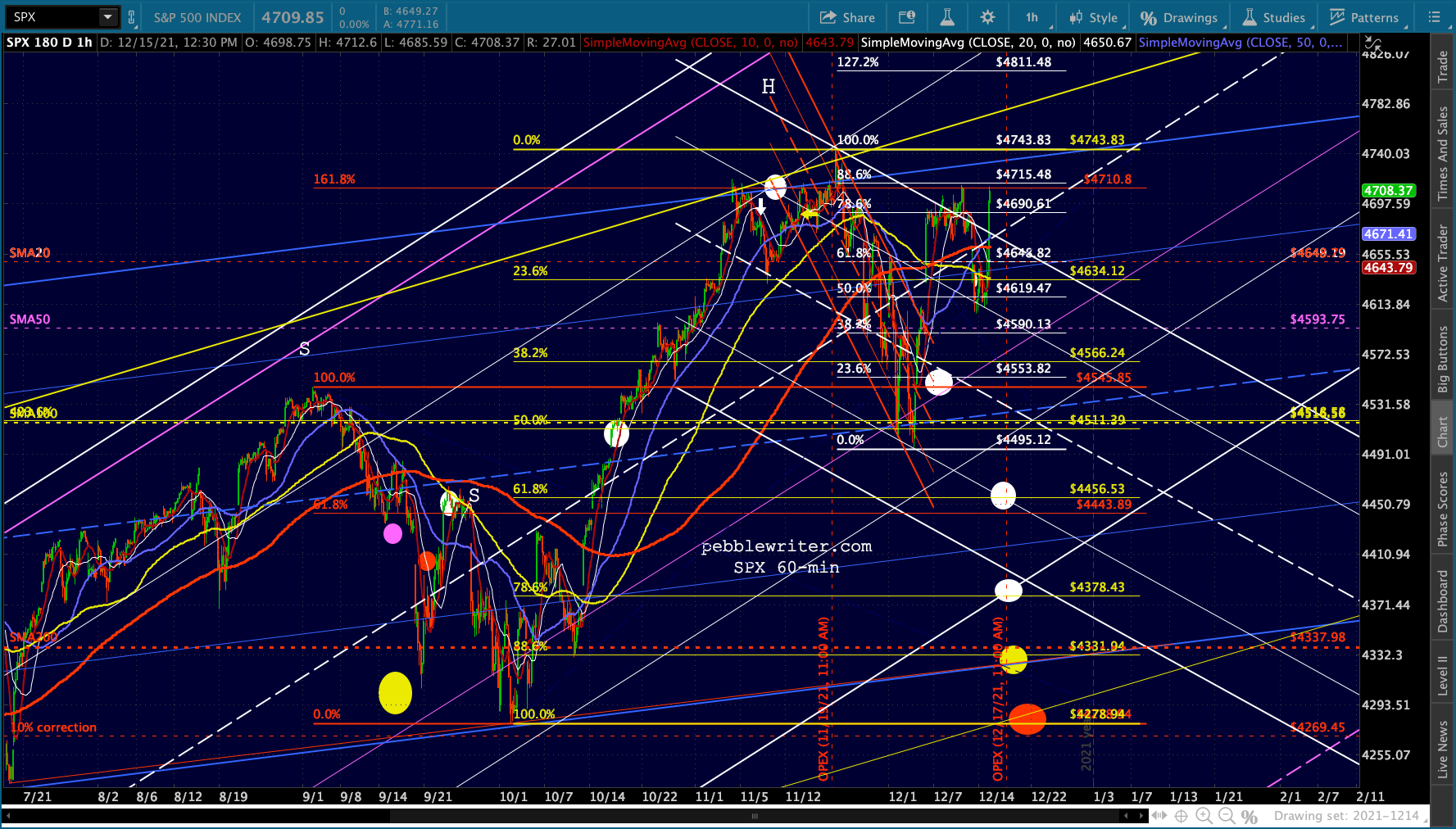

The equity picture: We got bullish 10/20 crosses in both ES and SPX, but no new highs for SPX yet. Remember, it had come close but hadn’t yet officially tagged its .886 until this morning.

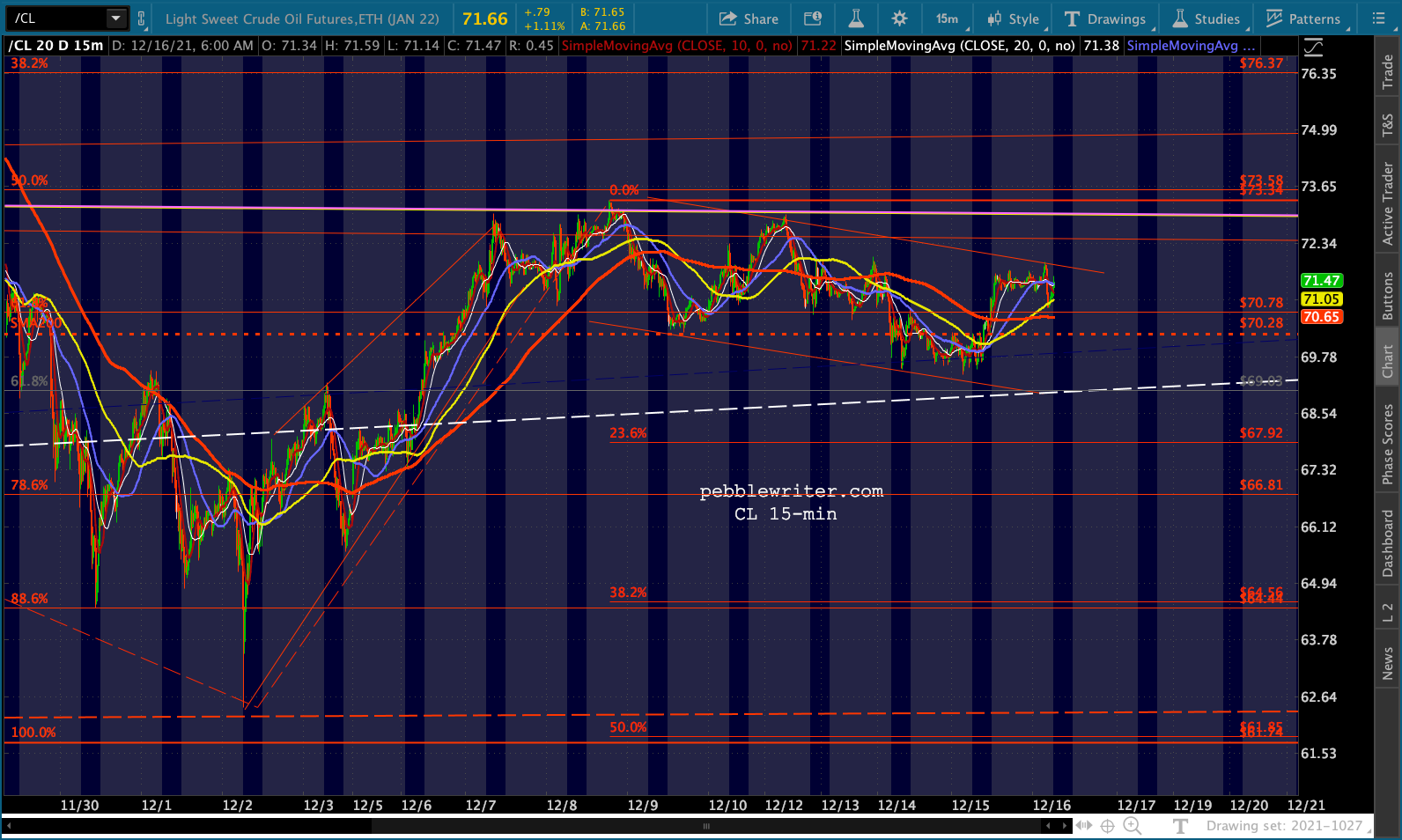

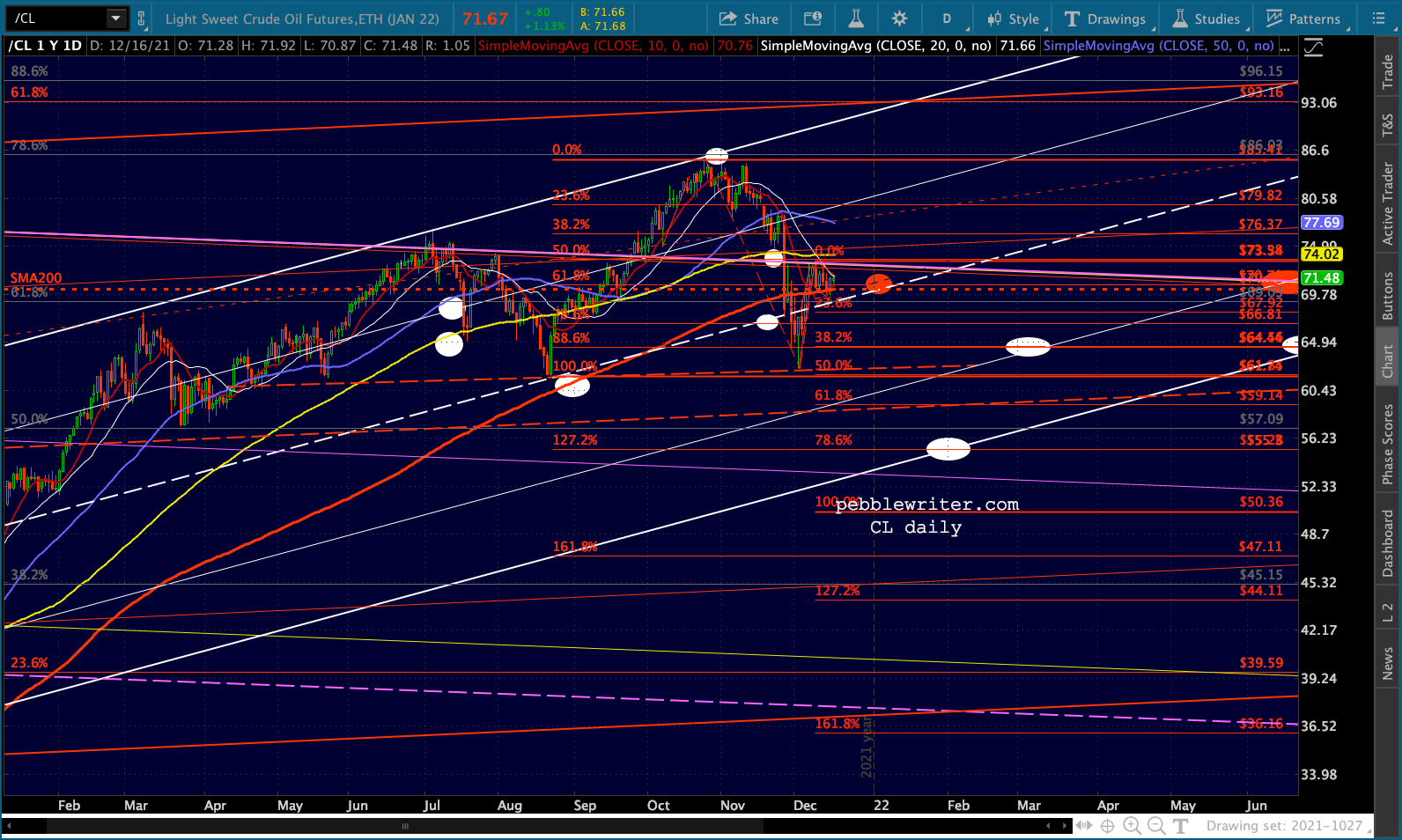

Coincidentally, CL popped up above its SMA200 (it had to dip below it first) just in time to fan the flames.

Coincidentally, CL popped up above its SMA200 (it had to dip below it first) just in time to fan the flames.

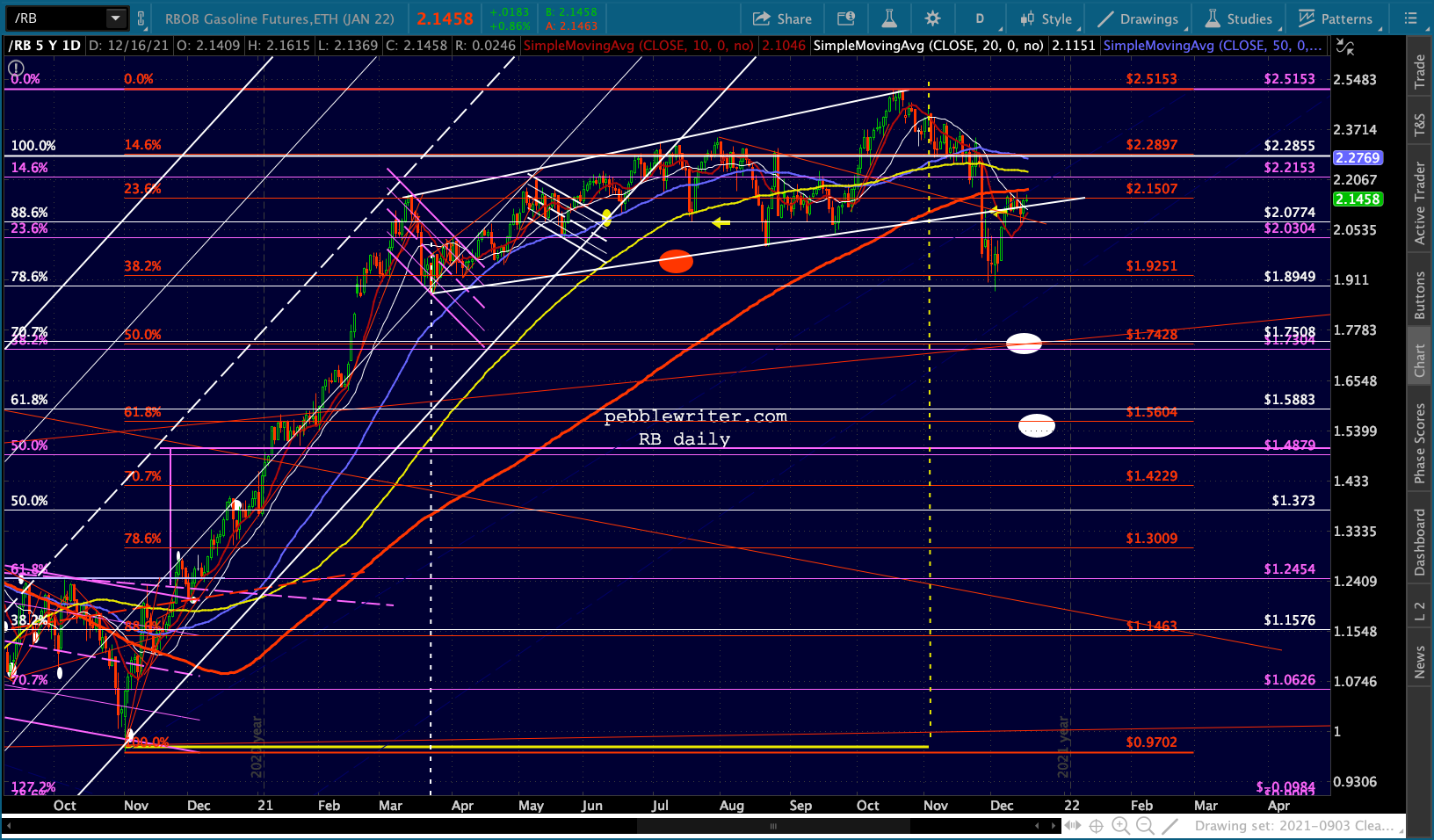

RB should finally be done with its backtest.

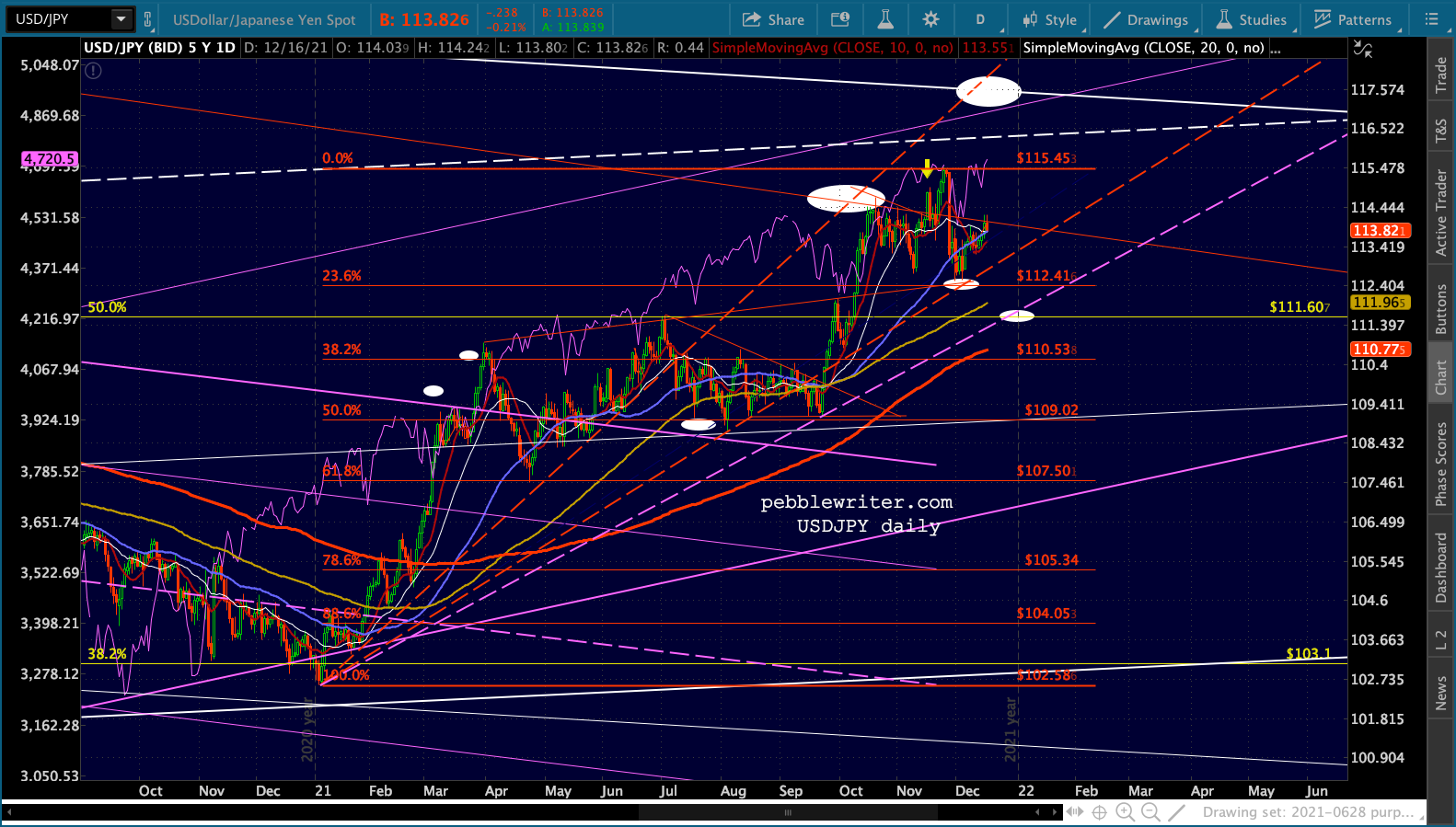

RB should finally be done with its backtest. USDJPY’s bump should be done…

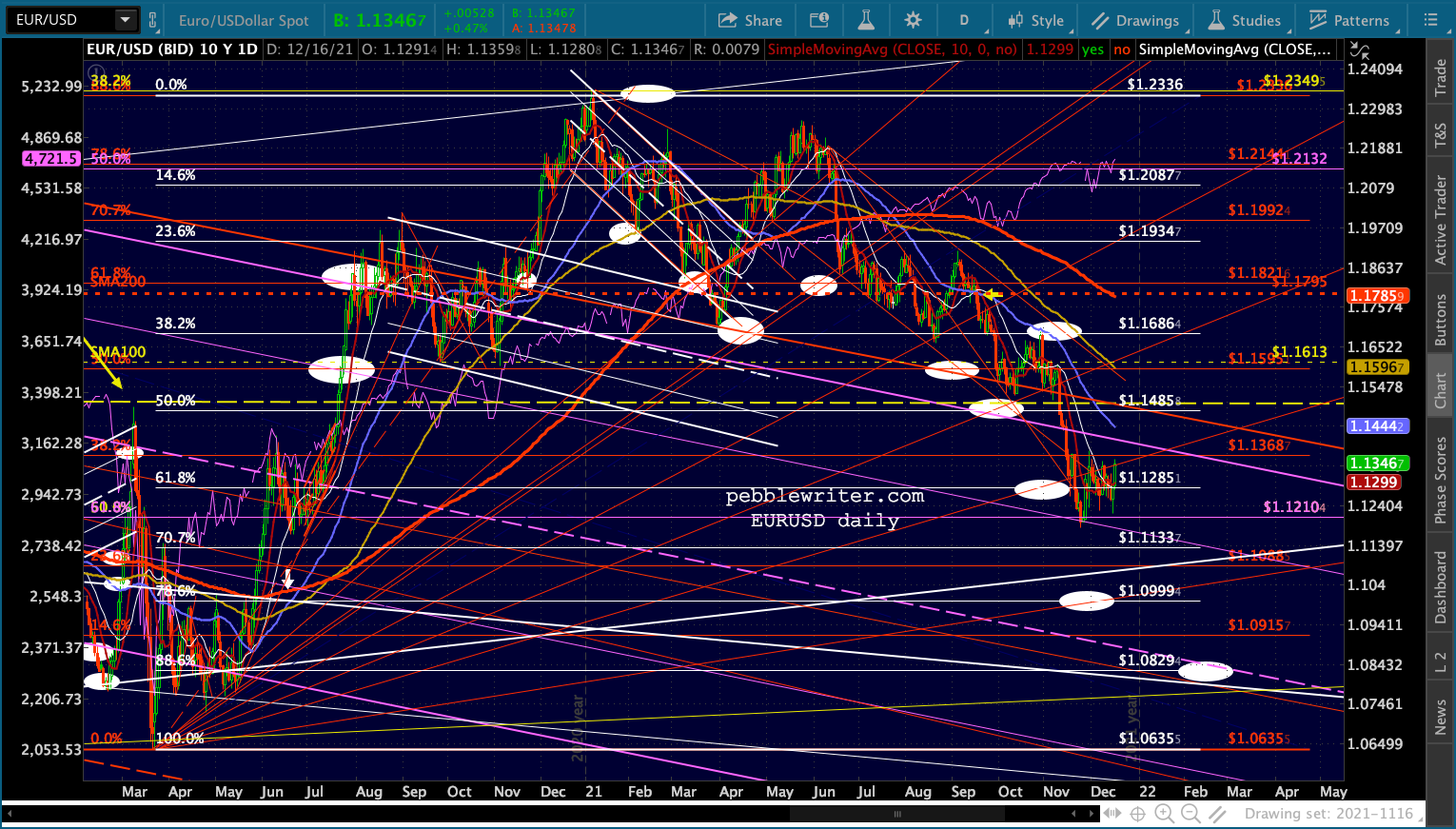

USDJPY’s bump should be done… …as should EURUSD’s…

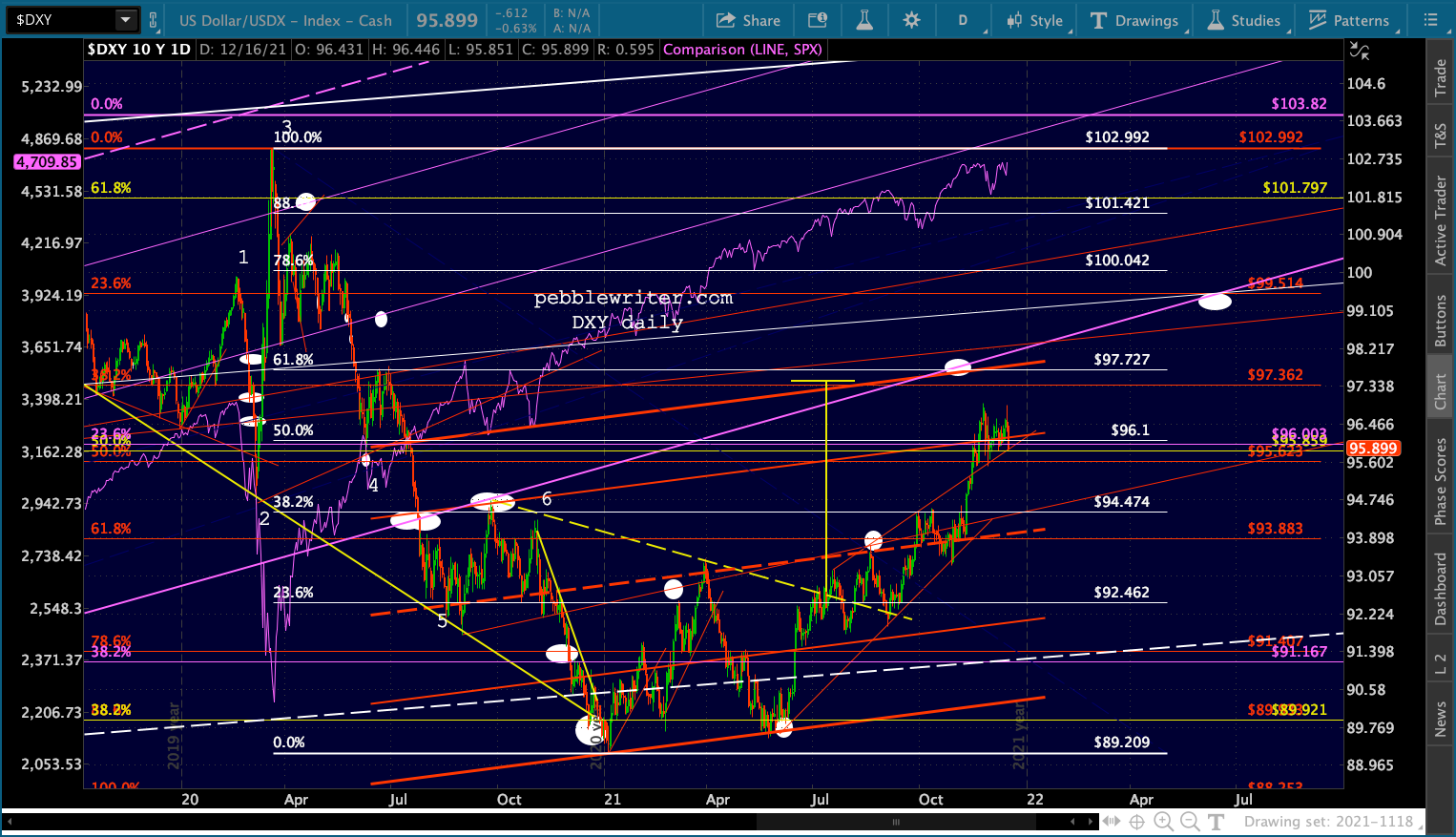

…as should EURUSD’s… …and DXY’s latest backtest.

…and DXY’s latest backtest.  As to the bond market, fade this initial bump in yields.

As to the bond market, fade this initial bump in yields.

Will the rally continue or was this just a headfake designed to get us past OPEX and the year-end? We’ll know soon enough. But, suffice it to say that the Fed still has the market’s back.

Will the rally continue or was this just a headfake designed to get us past OPEX and the year-end? We’ll know soon enough. But, suffice it to say that the Fed still has the market’s back.