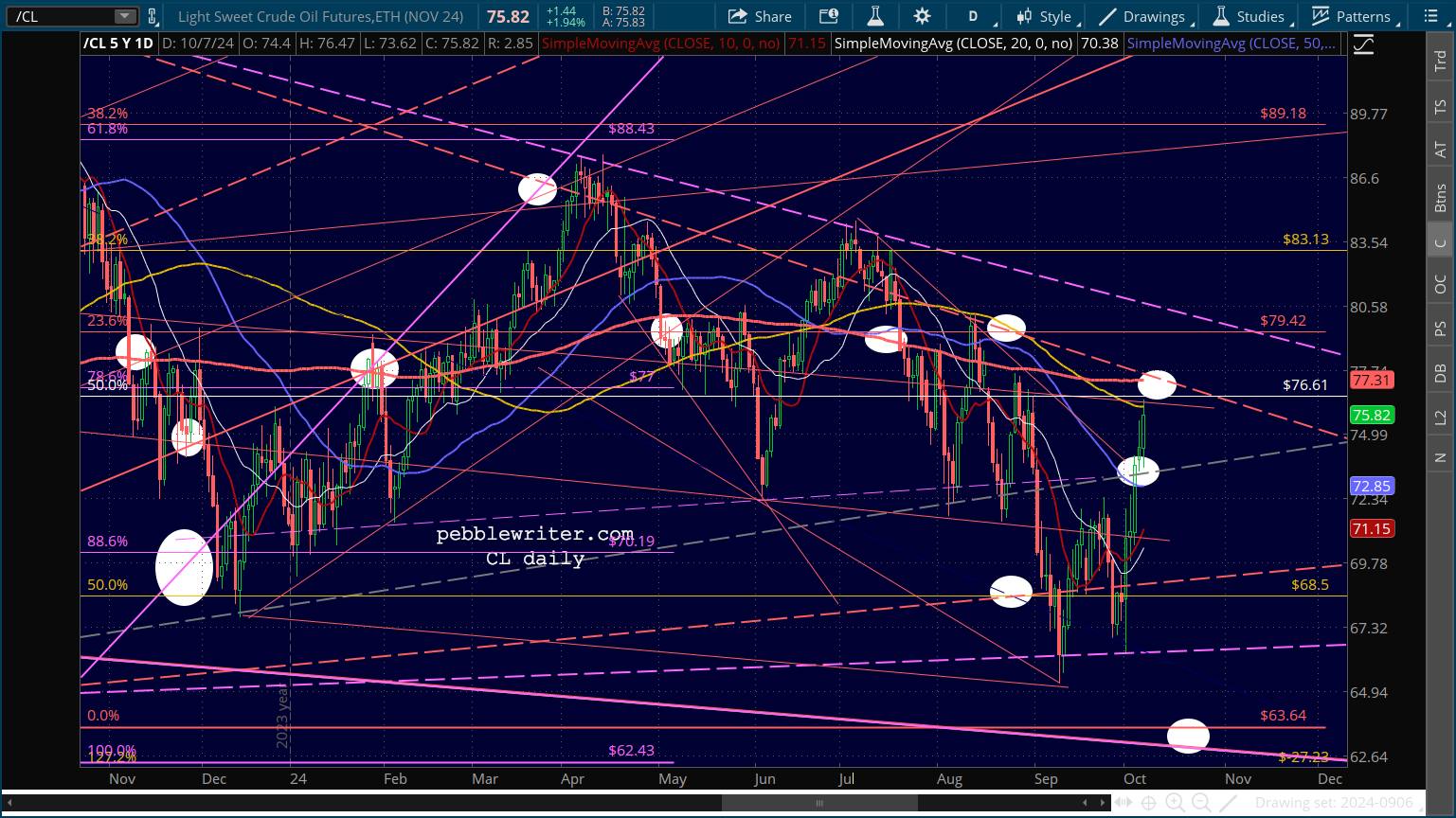

While Friday’s jobs report hinted at a soft landing, it also strongly suggested a more modest rate cutting path than the Fed’s initial 50 bps cut had indicated. After all, Powell has gone out of his way to Fedsplain how employment is the most important mandate now that inflation is licked. But, what if the recent runup in oil/gas brings inflation fears back into vogue?

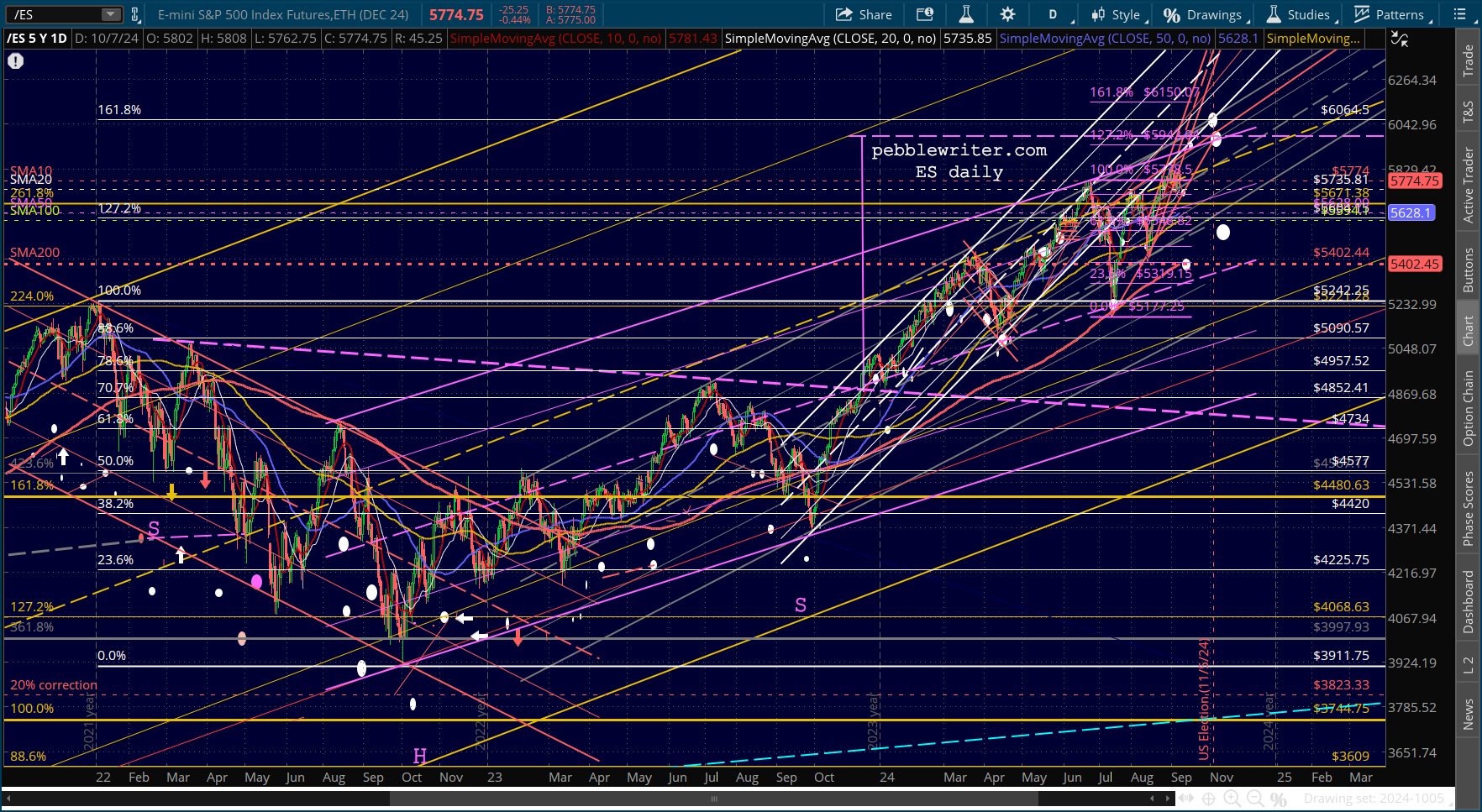

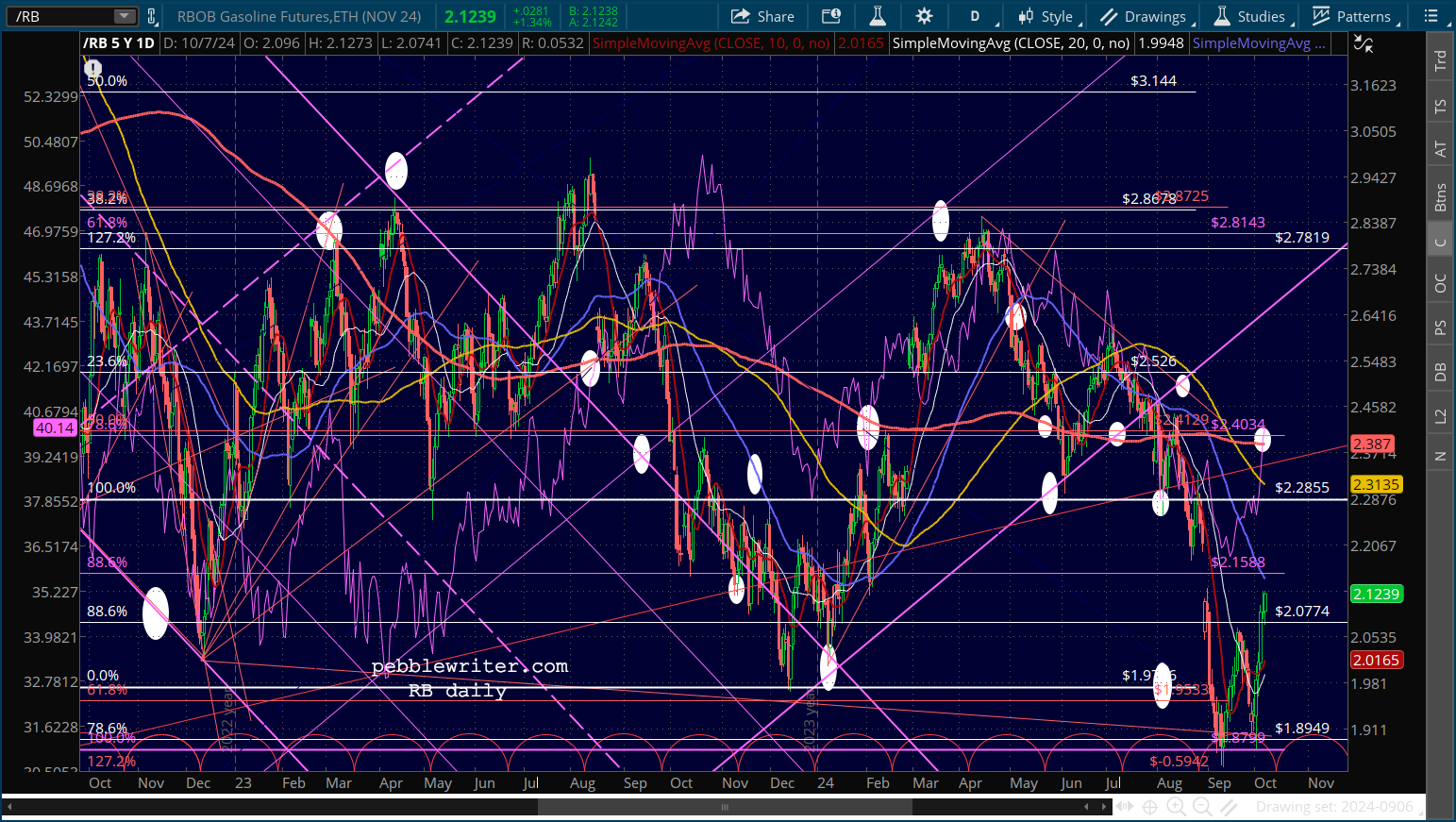

As the chart below shows, the warning signs were already there even before Iran fired a single missile.

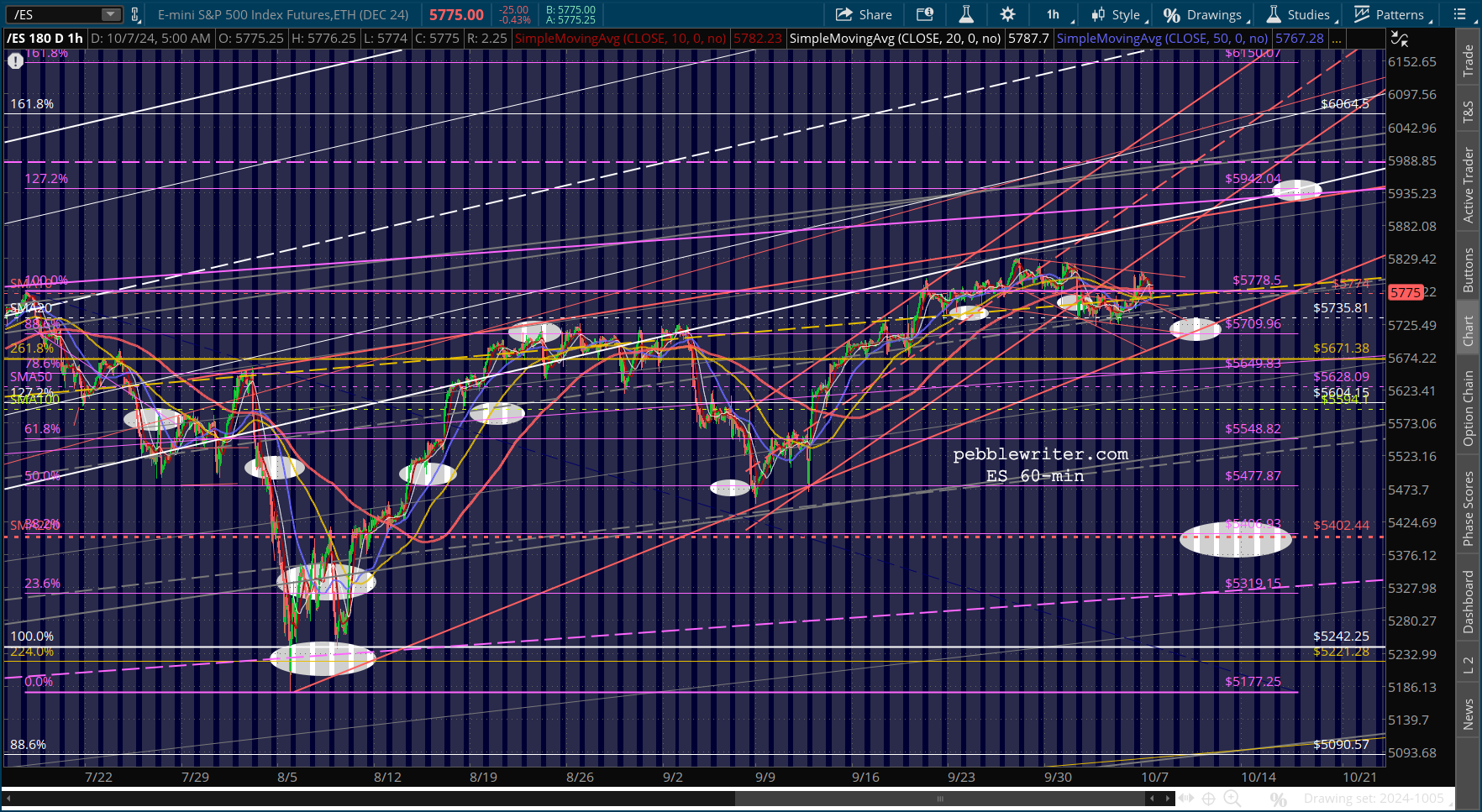

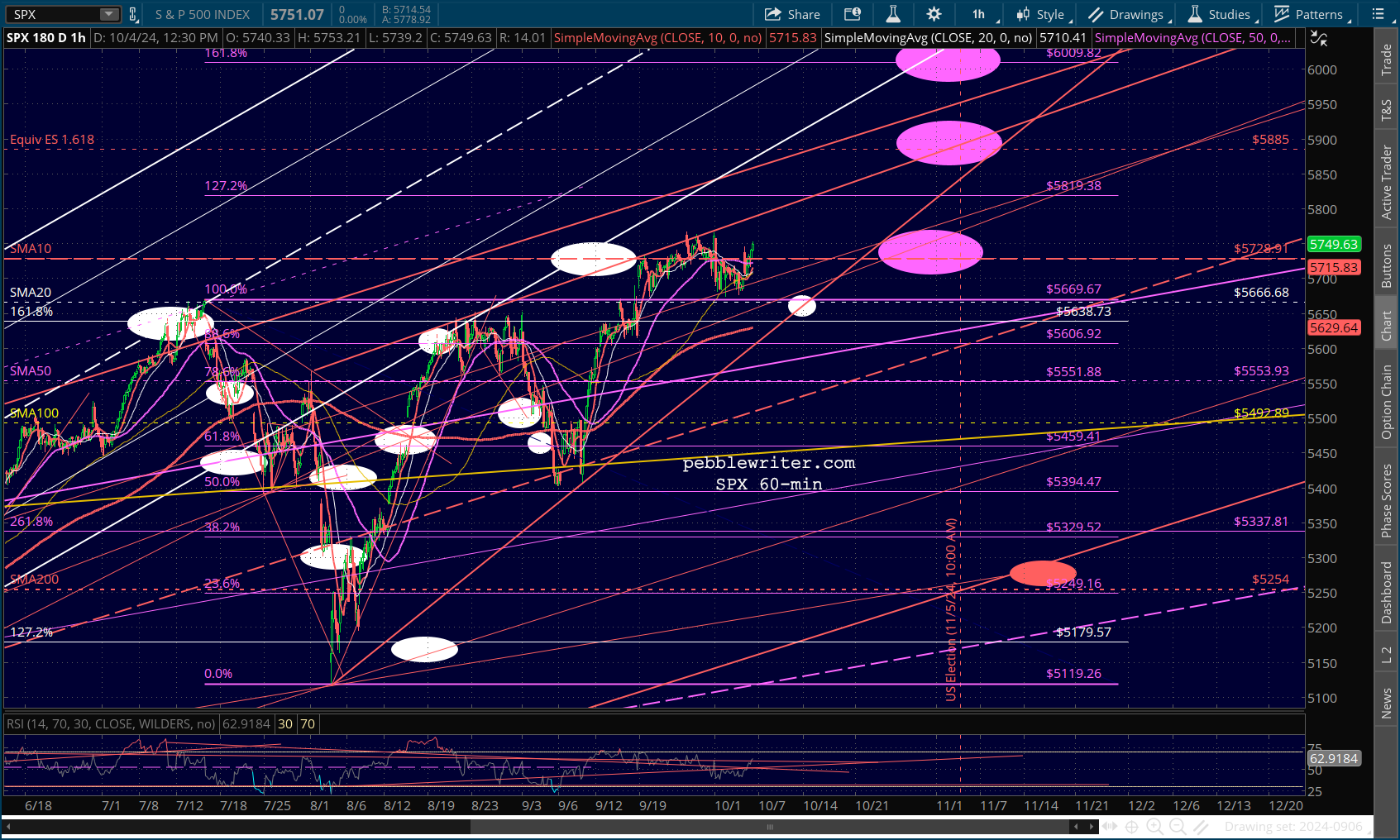

The bond market certainly seems to recognize the shifting tides, with the 10Y back over 4% for the first time since Aug 8.

The bond market certainly seems to recognize the shifting tides, with the 10Y back over 4% for the first time since Aug 8.  Can equities hold their recent support in the face of a more complicated rate environment? The answer lies in the timing of the price increases.

Can equities hold their recent support in the face of a more complicated rate environment? The answer lies in the timing of the price increases.

The recent increases in RB and CL futures haven’t shown up in the retail market just yet. So, they won’t be reflected in CPI until the October print which (conveniently) won’t be released until Nov 13 – after the election.

This is also conveniently after the next Fed meeting occurs (Nov 6-7.) Bottom line, Powell will be able to say – with a straight face – that the FOMC is waiting on the data before altering their rate cut plans.

continued for members…

continuing…