PCE came in on target at 0.3% MoM and 2.5% YoY. Core PCE was up 2.6% YoY. Although personal income shot up 0.9% (versus 0.3% expected), personal spending declined to -0.2% (-0.5% real) versus 0.3% expected.

In other words, consumers’ spending is in line with declining consumer confidence, home sales and employment and slowing GDP. Combined with elevated inflation, the data continues to hint at stagflation. It leaves the Fed in a box which doesn’t allow for any rate cuts in the next few months.

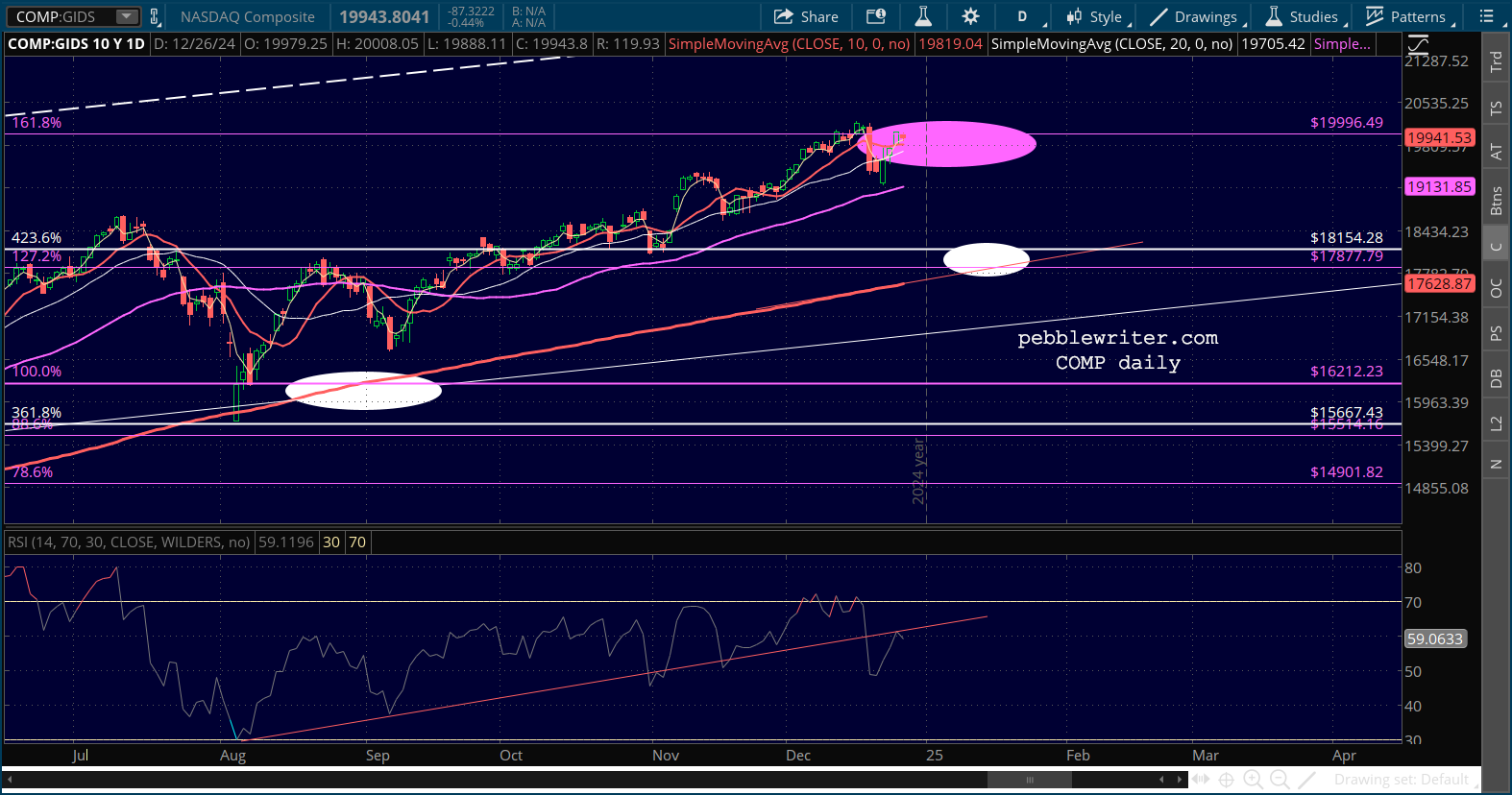

Meanwhile, stocks continue melting down. COMP has been especially walloped. approaching our 200-day MA target from December 26 [see: Update on COMP – Dec 26, 2024.] continued for members…

continued for members…

From back then: COMP’s SMA200 tag is potentially important, as the last few times it’s done so have correlated with nice bounces to new highs for COMP and SPX.

COMP’s SMA200 tag is potentially important, as the last few times it’s done so have correlated with nice bounces to new highs for COMP and SPX.

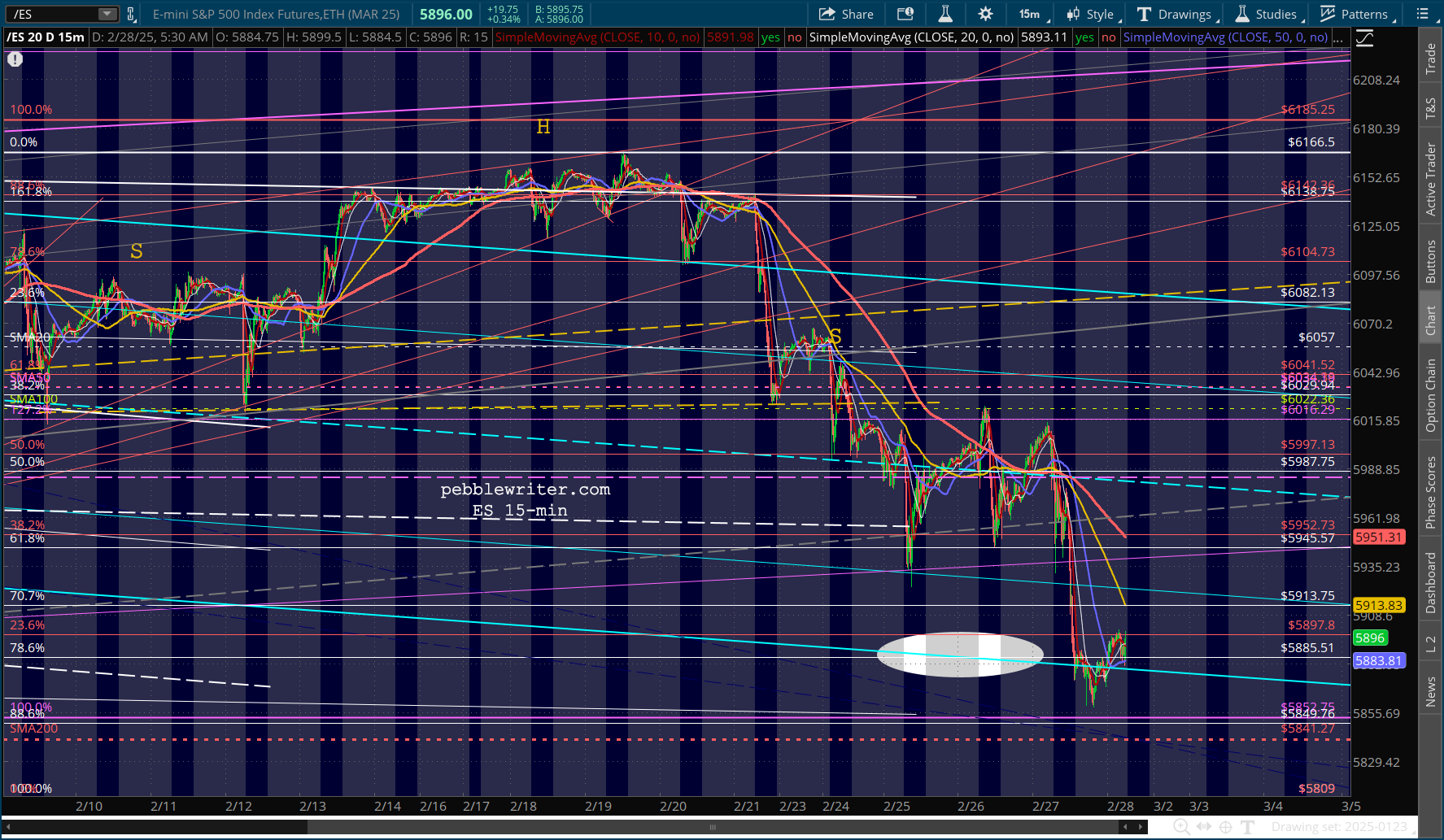

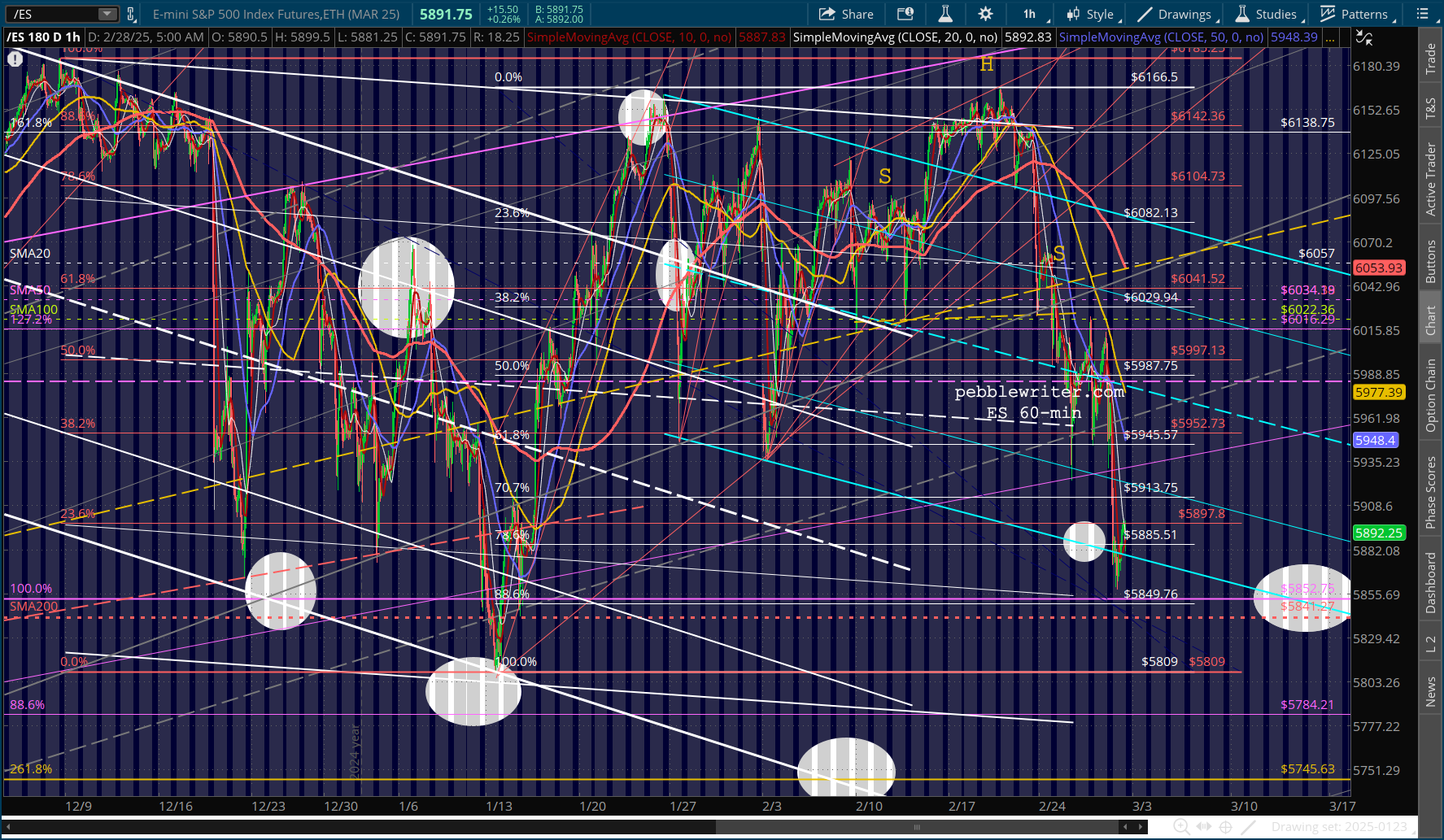

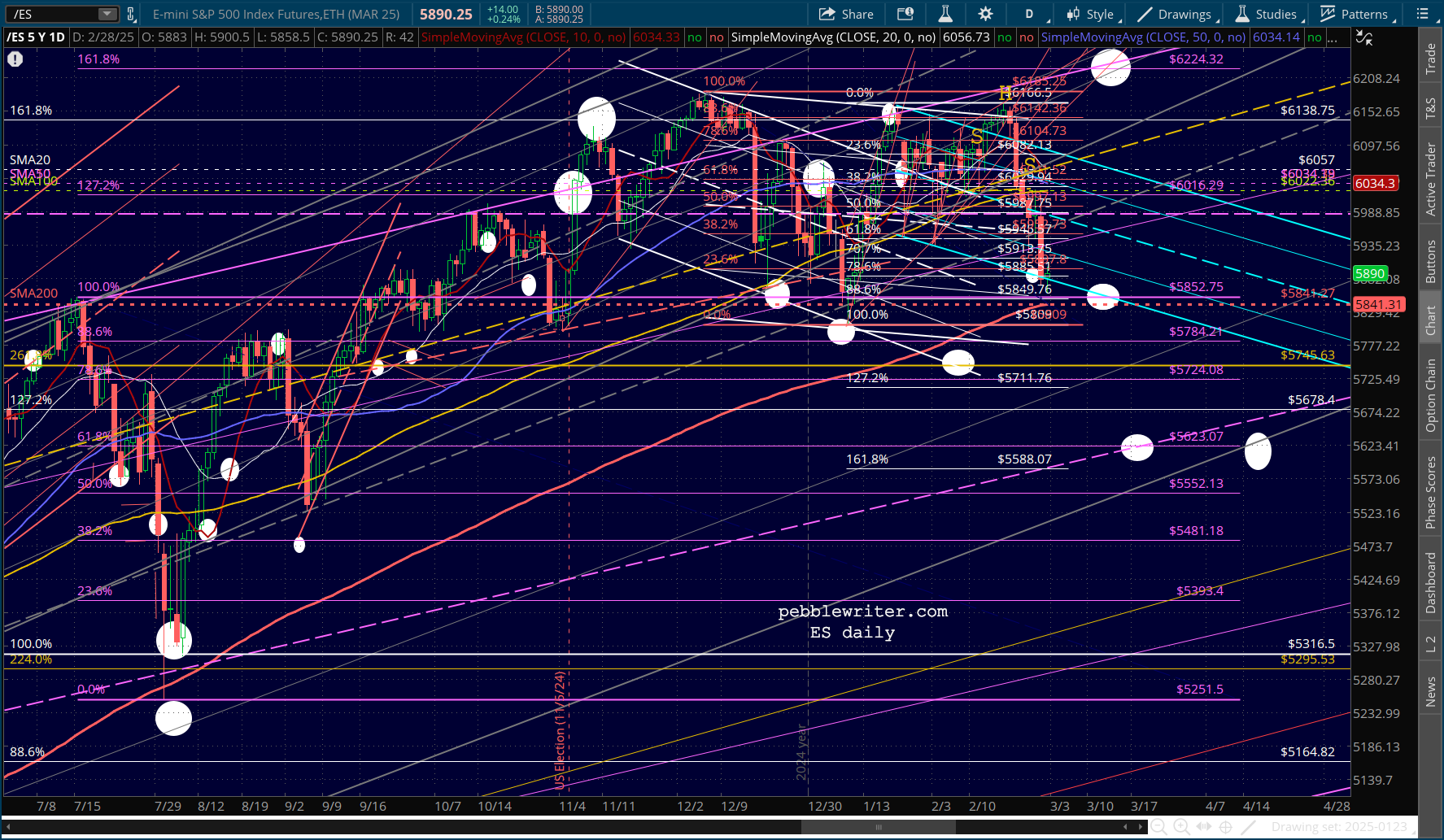

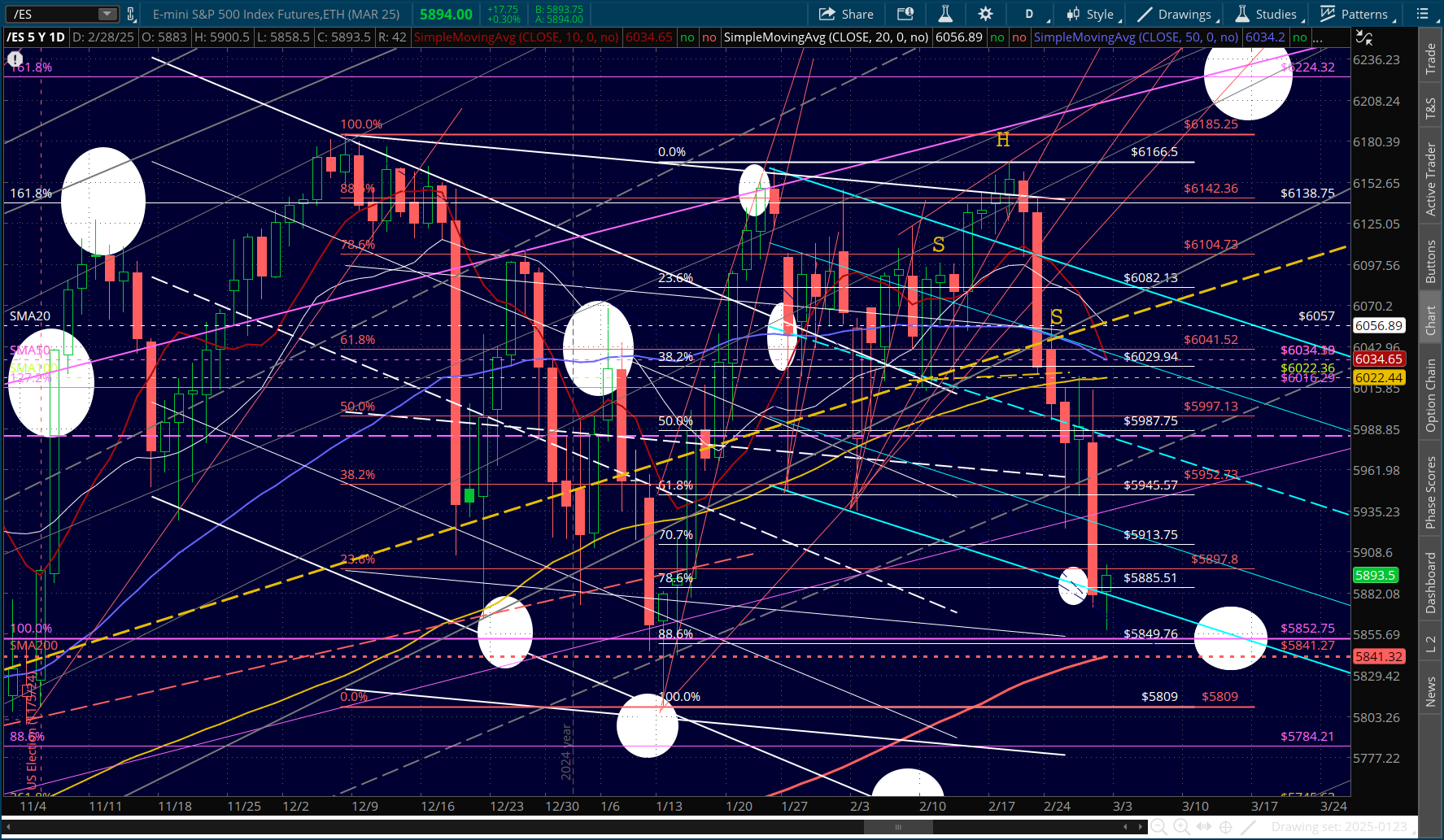

The rest of the equity picture shows ES approaching our .886/SMA200 target at 5849.

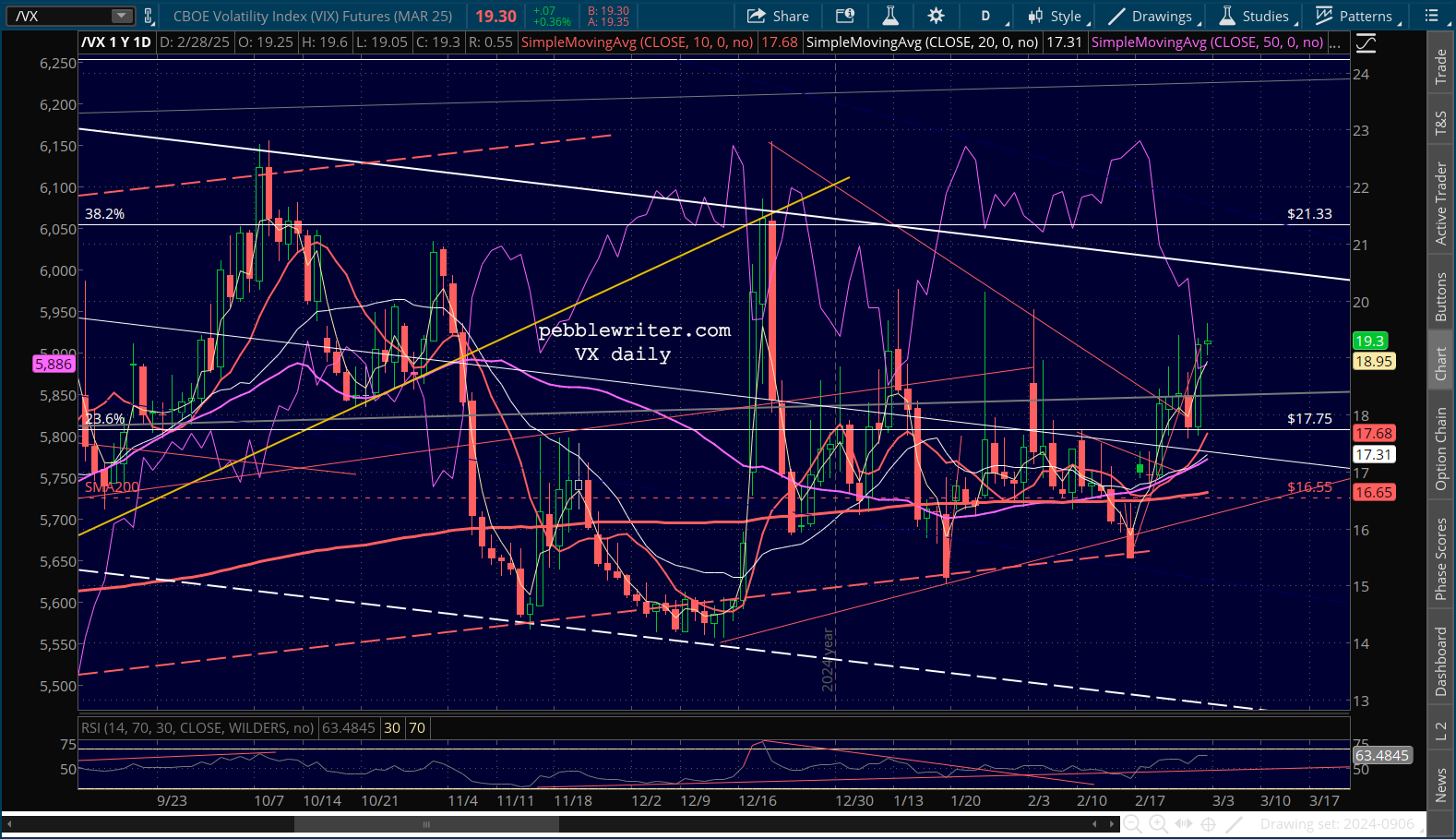

VIX and VX are both broken out without being overbought.

VIX and VX are both broken out without being overbought.

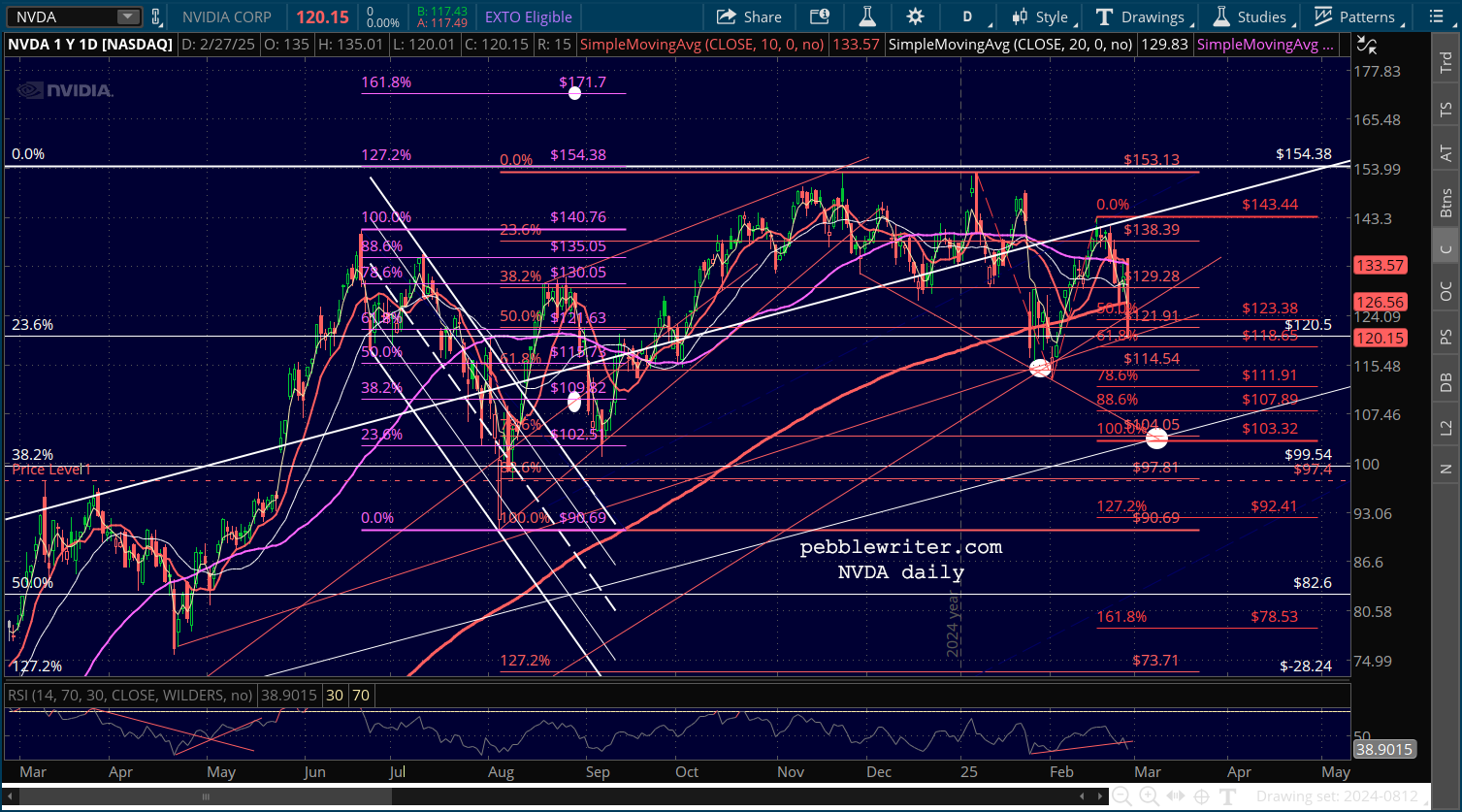

NVDA really stumbled yesterday, and appears to still have more downside.

NVDA really stumbled yesterday, and appears to still have more downside.

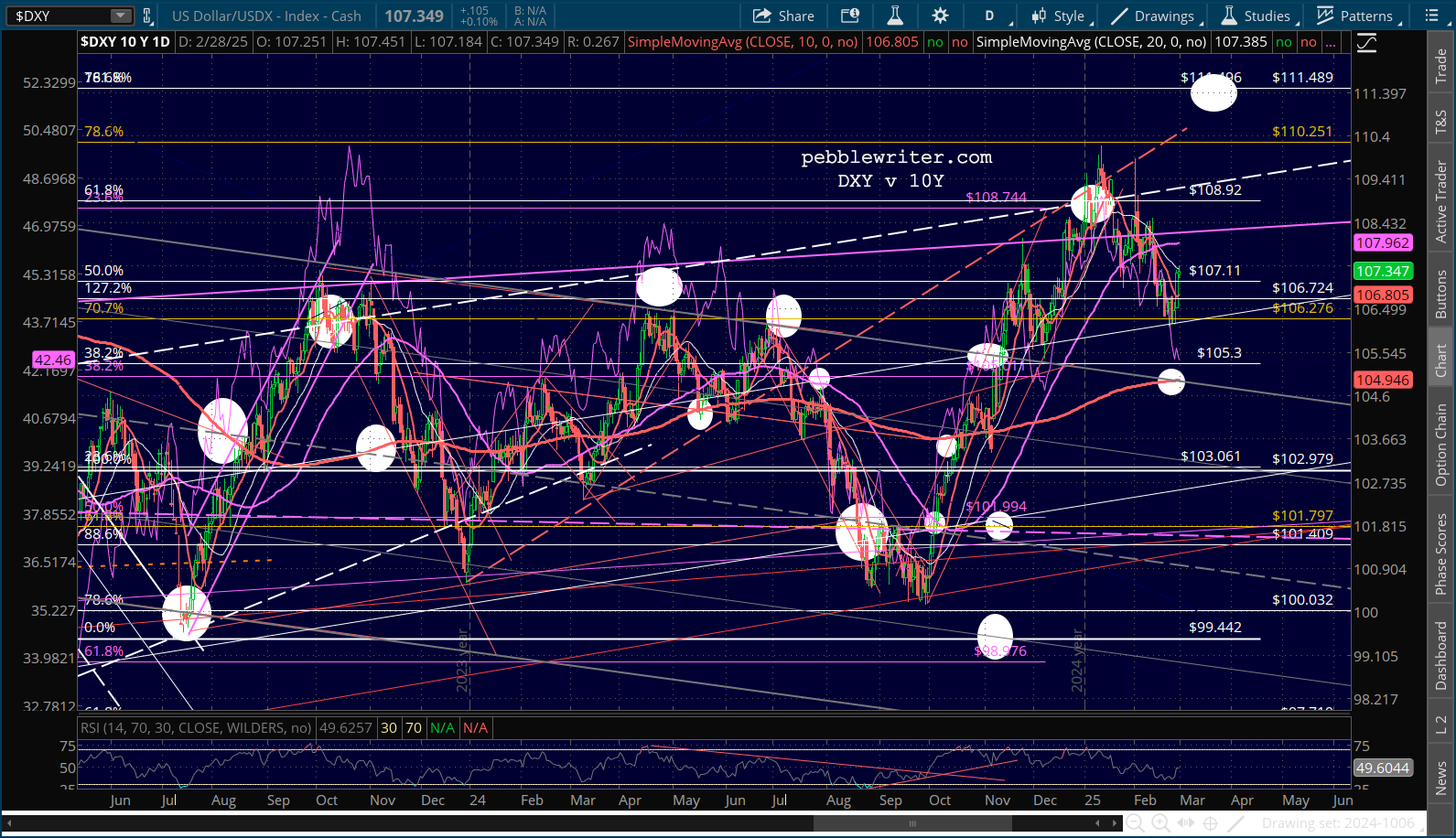

Currencies continue to simmer, with DXY up very slightly.

Currencies continue to simmer, with DXY up very slightly.

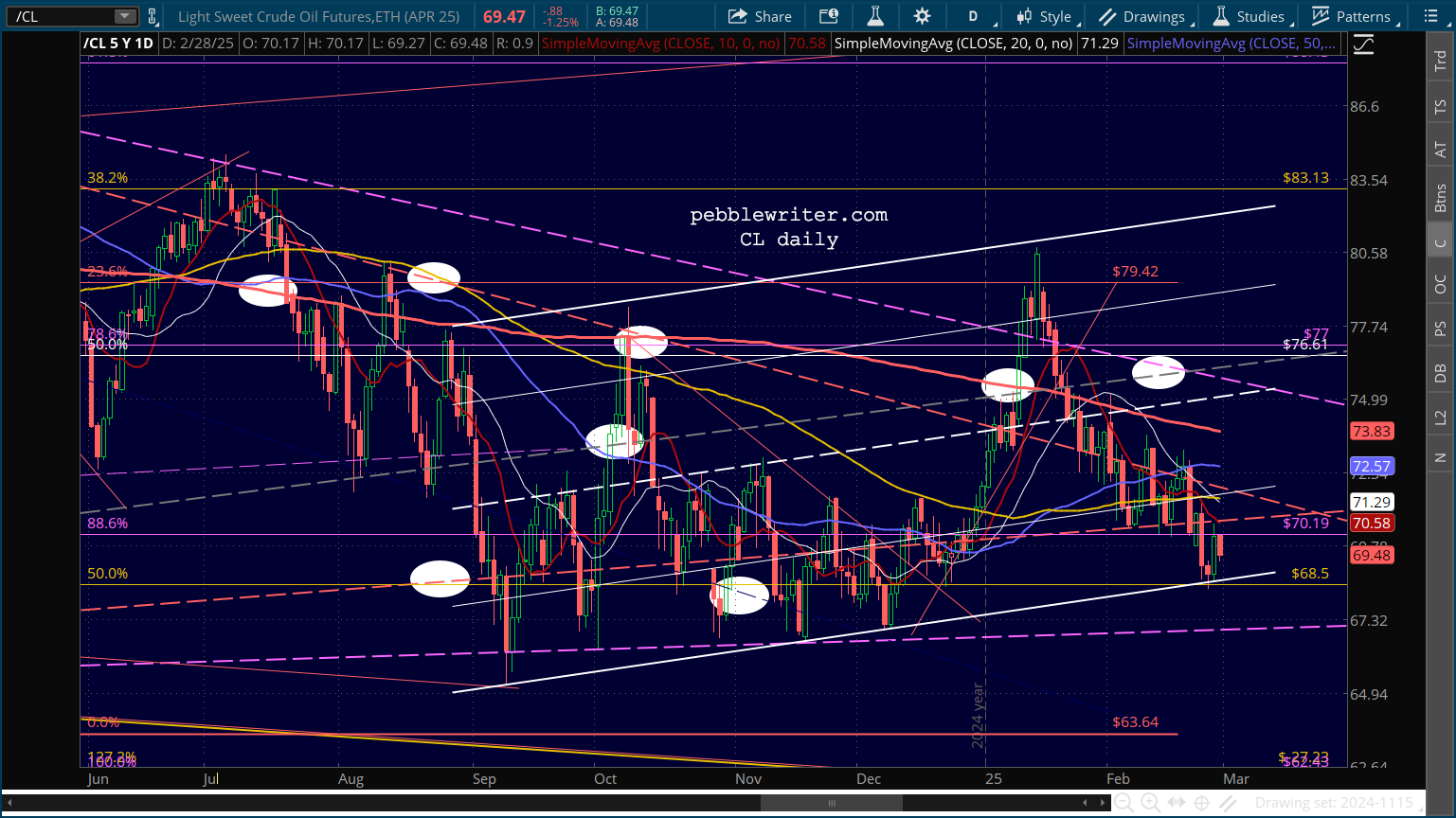

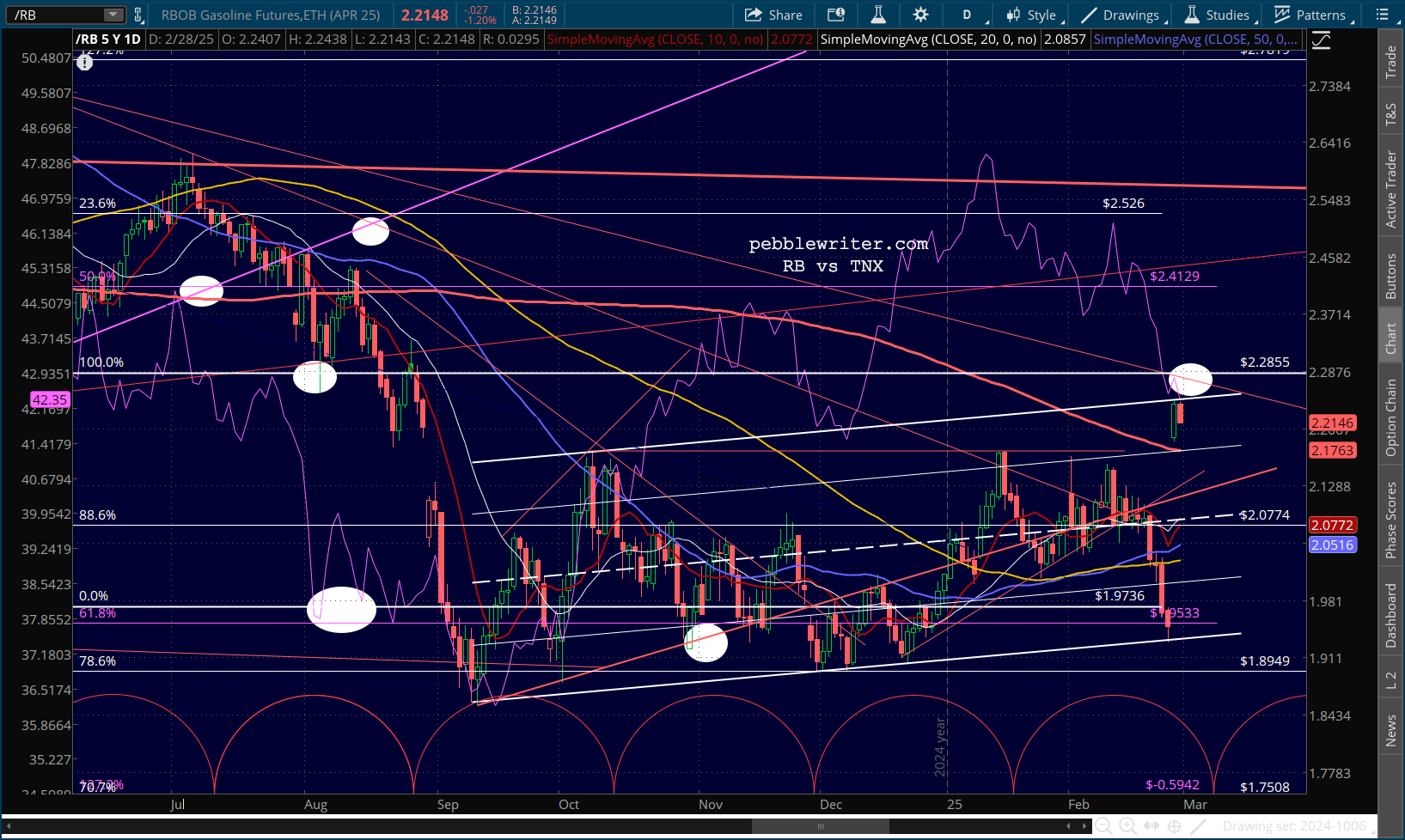

Oil and gas are both coming under pressure, as are everything else. But the recent bounces on support are still concerning to the inflation picture.

Oil and gas are both coming under pressure, as are everything else. But the recent bounces on support are still concerning to the inflation picture.

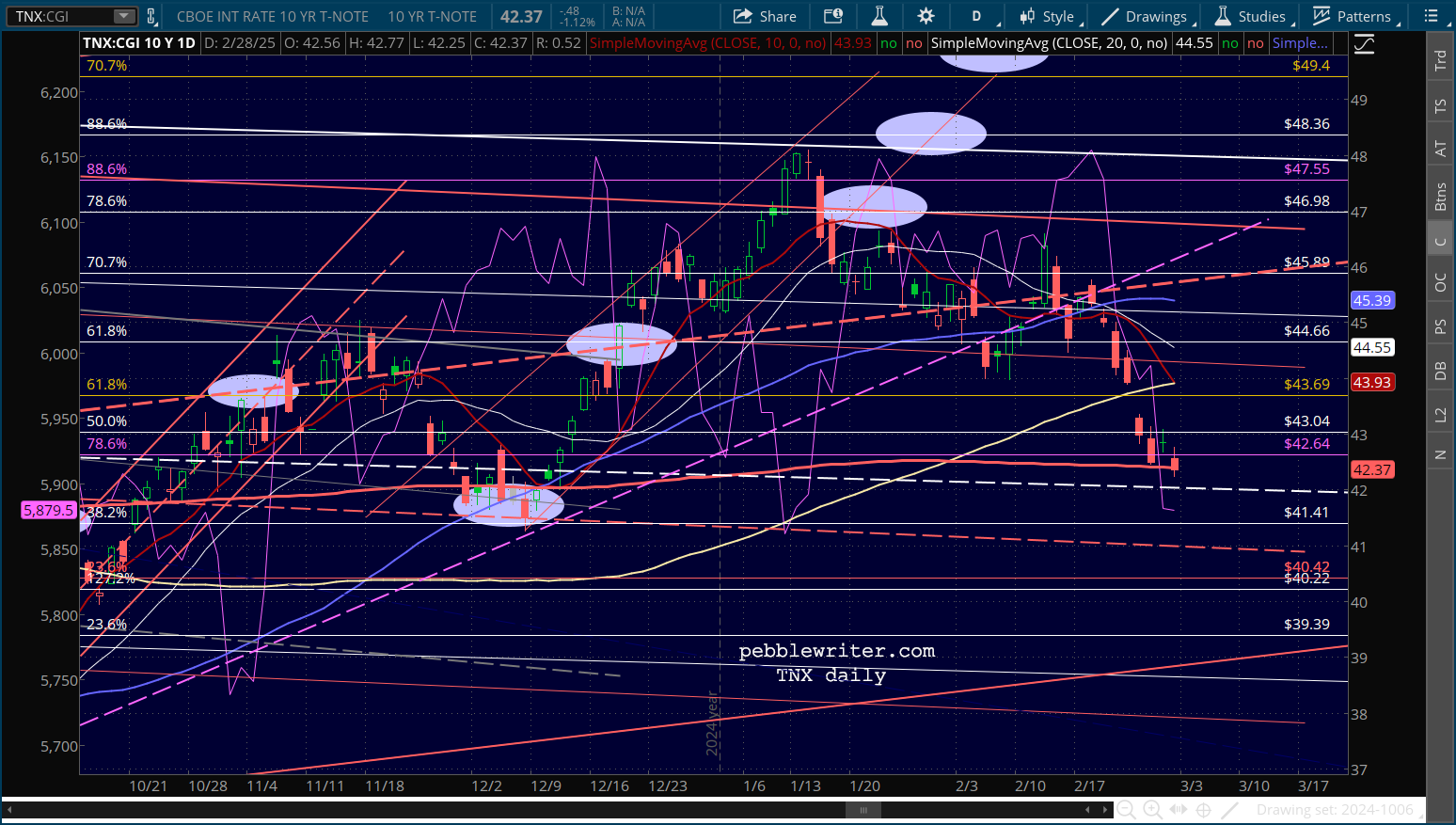

Of course, at this point yields are reacting more to the equity troubles than they are to inflation. The 2s10s is still hanging around 20 bps, but both the 2Y and 10Y have clearly broken trend, with the 10Y barely hanging on to its SMA200.

Of course, at this point yields are reacting more to the equity troubles than they are to inflation. The 2s10s is still hanging around 20 bps, but both the 2Y and 10Y have clearly broken trend, with the 10Y barely hanging on to its SMA200.