September CPI came in higher than expected, at 0.4% MoM and 3.7% YoY versus estimates of 0.3% and 3.6%. Core CPI (less food and energy) remained elevated at 4.1%.

The details reveal continuing challenges with shelter, food and energy.

While the YoY print has trended lower…

While the YoY print has trended lower…  …the last two monthly prints suggest that inflation might be leveling out at elevated levels.

…the last two monthly prints suggest that inflation might be leveling out at elevated levels. Bottom line, the YoY trend is of little benefit to consumers who are tapped out, with depleted savings and higher expenses including the resumption of student loan payments. We don’t see a significant drop in CPI in the months ahead unless oil/gas prices collapse – a scenario that seems unlikely given recent events in the Middle East.

Bottom line, the YoY trend is of little benefit to consumers who are tapped out, with depleted savings and higher expenses including the resumption of student loan payments. We don’t see a significant drop in CPI in the months ahead unless oil/gas prices collapse – a scenario that seems unlikely given recent events in the Middle East.

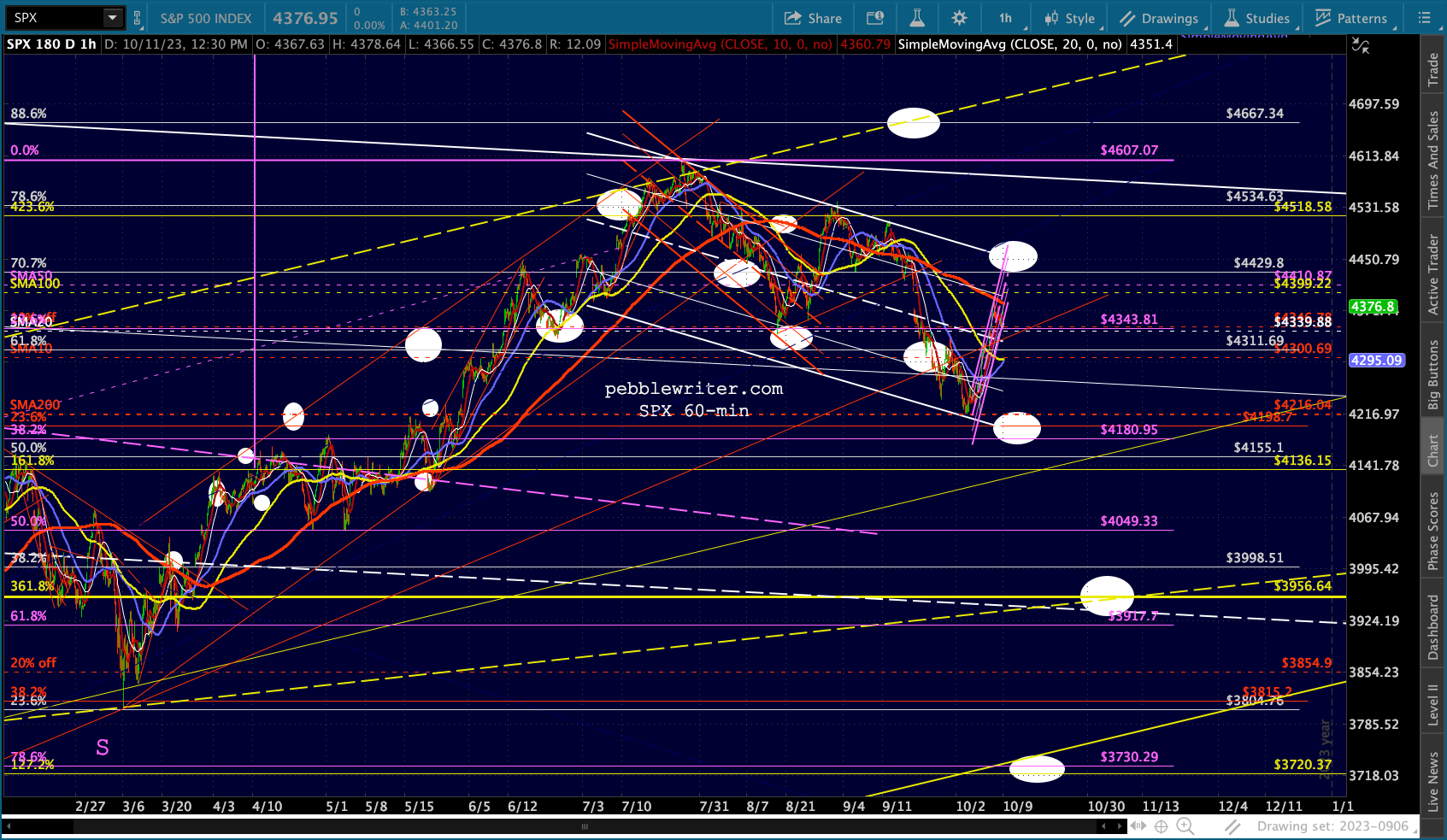

Futures have lost most of their overnight ramp and are almost back to flat.

Futures have lost most of their overnight ramp and are almost back to flat.

continued for members…Note that the SMA200s are now higher than recent lows – meaning that ES/SPX could actually tag them while making higher lows. This would be a net positive as it would provide a stronger base for a year-end rally.

continued for members…Note that the SMA200s are now higher than recent lows – meaning that ES/SPX could actually tag them while making higher lows. This would be a net positive as it would provide a stronger base for a year-end rally.

VIX is testing its SMA50, a moving average that has mattered in the recent past.

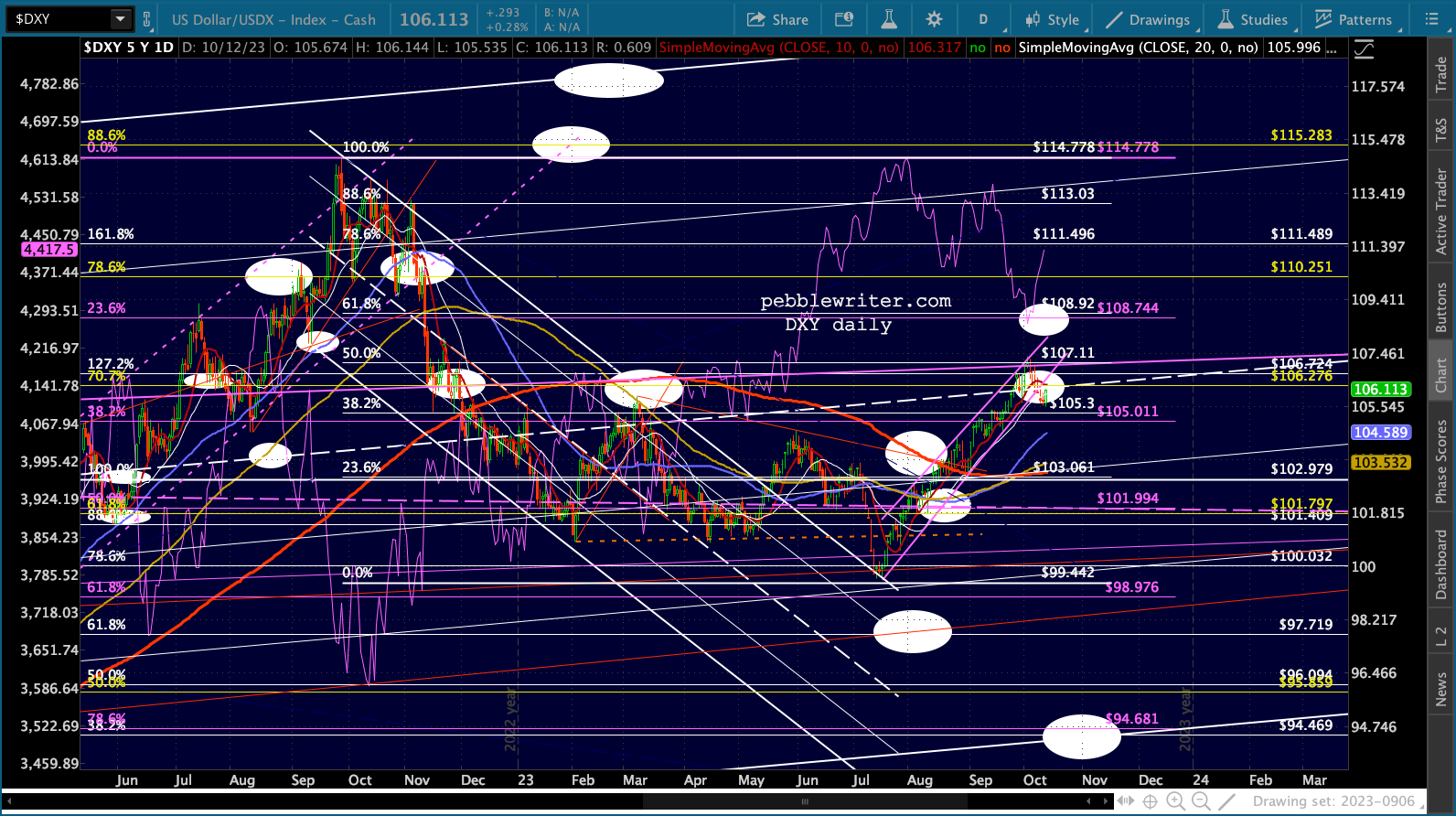

VIX is testing its SMA50, a moving average that has mattered in the recent past. The currency tea leaves are a bit too hard to read at the moment, though EURUSD’s reversal at the channel top is bearish for stocks and could break down to new lows.

The currency tea leaves are a bit too hard to read at the moment, though EURUSD’s reversal at the channel top is bearish for stocks and could break down to new lows.

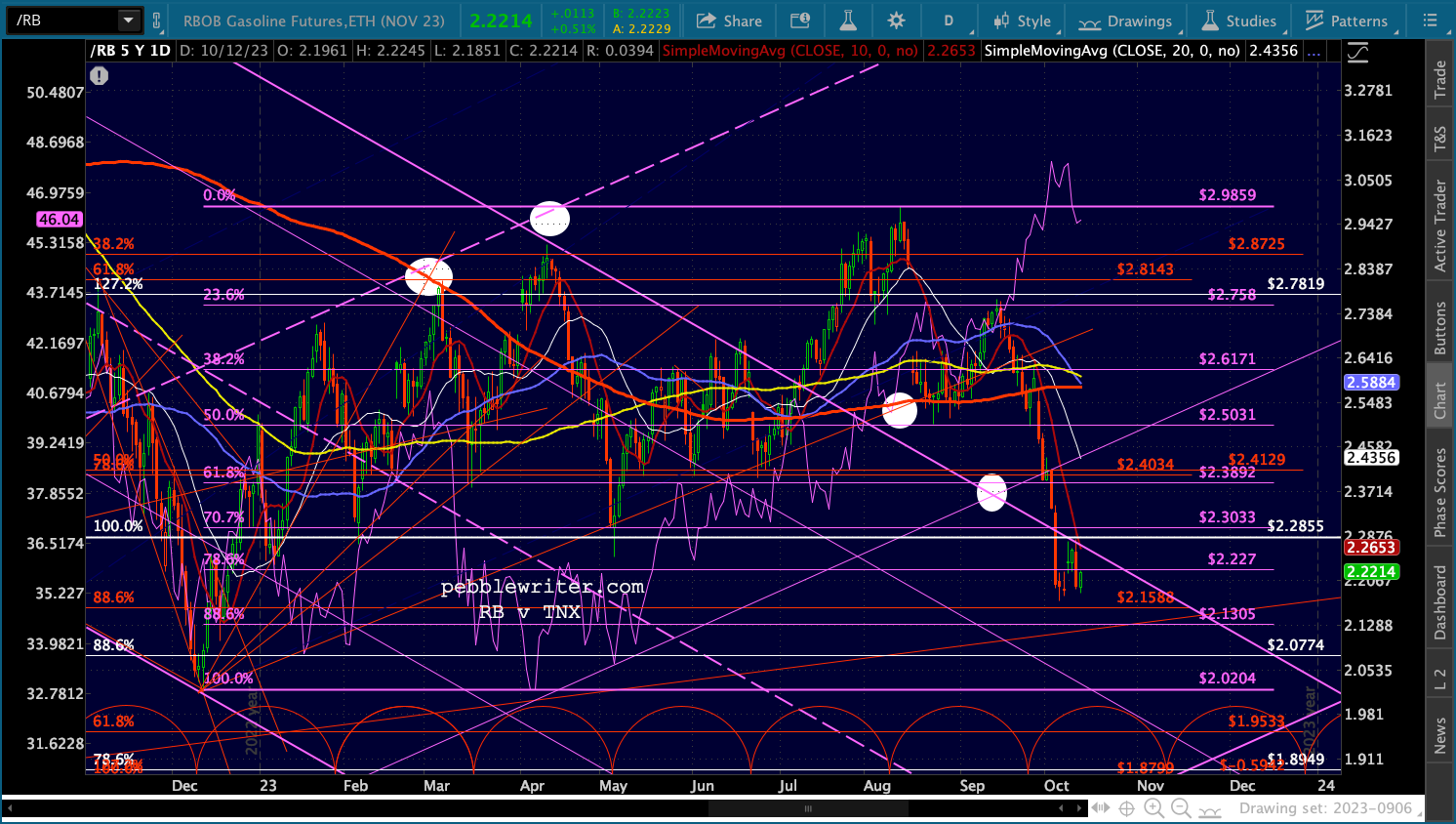

It doesn’t help equities that oil and gas prices are higher on the Middle East conflict.

It doesn’t help equities that oil and gas prices are higher on the Middle East conflict.