Following the recent takeover of BLS data by the Oval Office, we’re less trusting than ever of headline CPI. But, for what it’s worth, the print came in on target: +0.2% MoM and a repeat of June’s 2.7% YoY. Core CPI ticked higher to 3.1% versus 2.9% prior and 3.0% expected.

The algos believe what they’re told, so futures popped up to the .886 Fibonacci retracement on the “news.” Just to be on the safe side, Trump postponed China tariffs by another 90 days.

The algos believe what they’re told, so futures popped up to the .886 Fibonacci retracement on the “news.” Just to be on the safe side, Trump postponed China tariffs by another 90 days.

continued for members…

continued for members…

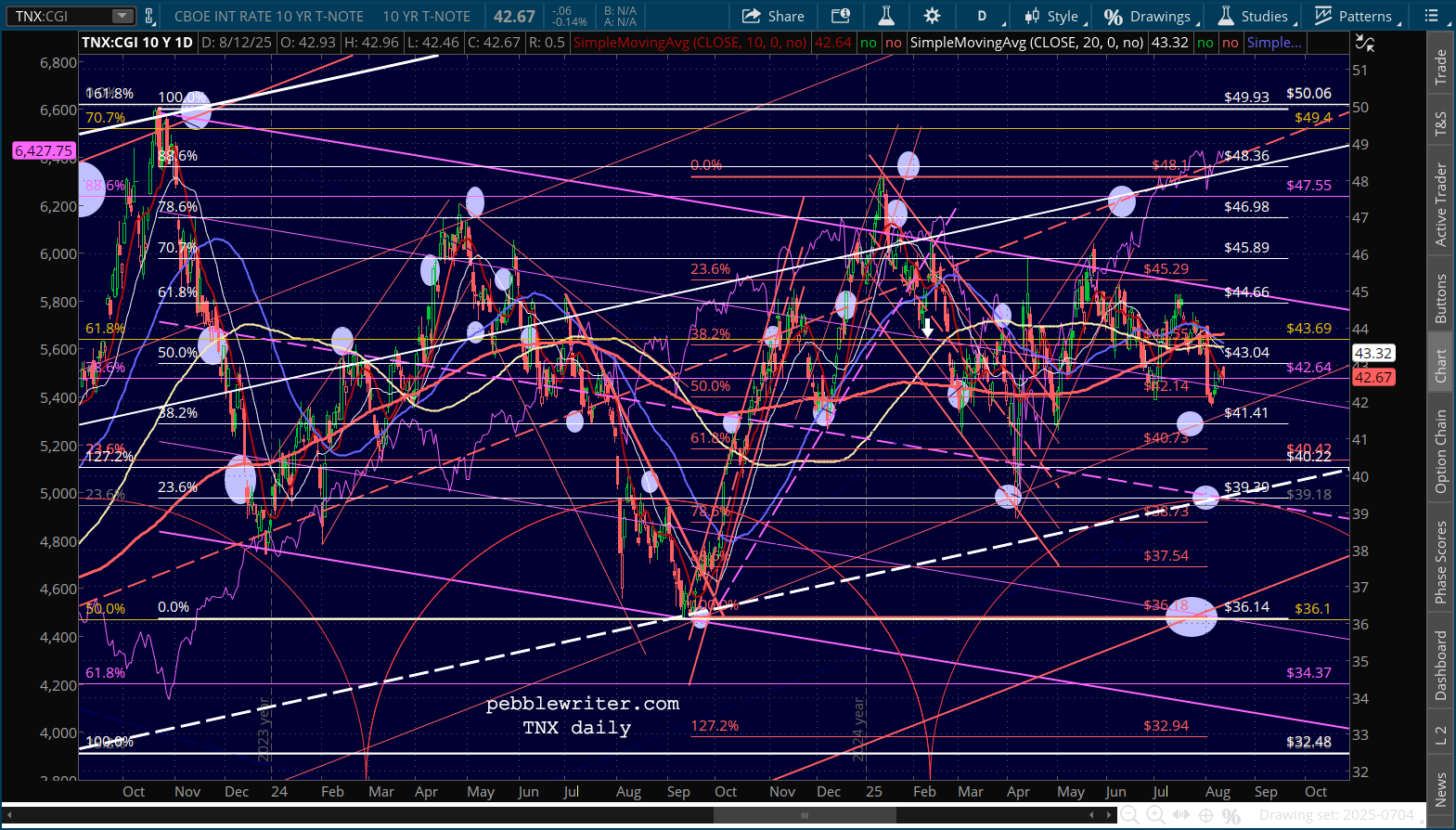

Not surprisingly, the results were just in time to prevent a bearish 10/20 cross. It’s been bullish since June 5 and has narrowly averted several previous instances.

The results were generally in line with out gas/CPI model’s forecast.

The forecast hasn’t really changed, though as we noted yesterday this gives the market a better shot at new highs.

Naturally, VIX and VX were both hammered leading up to the print.

Naturally, VIX and VX were both hammered leading up to the print.

The USD has also been under pressure.

The USD has also been under pressure.

CL and RB are still in downturns, now reaching 2 weeks.

They continue to matter to rates, but TNX is actually higher (+0.51%) this morning.

continuing…