Uberdove Jim Bullard does it again — upending the rules of economics and, more importantly, calming the markets.

“We should always plan for the worse and hope for the best. I think the idea that you’re inevitably going to have a recession just because you’ve had an expansion for a while is not really right.”

Put simply, “inevitably” means at some point in the future. Is he really suggesting that we’ll never have a recession?

“I think the yield curve issue is one that is sending a signal to us about, well, maybe the whole structure of rates is just lower today, maybe we should just react to data and not plan to try to get rates up to such a high level that they match what we’ve seen in the 2000s or the 1990s.”

Translation: we’re flattening the curve in order to build in some headroom for the next time we rescue markets, but forget about a return to normalcy. The only thing he’s really worried about…

“I have been worried that we don’t overdo normalization.”

Normal is by definition the natural state of things. How can you overdo a natural state?

Futures bounced nearly 10 points on his comments — leaving the H&S Pattern we’ve been watching and which the latest VIX crush negated in the dust.

He momentarily dropped his poker face when acknowledging US dollar strength, which of course has been instrumental in supporting stocks.

He momentarily dropped his poker face when acknowledging US dollar strength, which of course has been instrumental in supporting stocks.

Given that central banks control currencies, interest rates, and many futures and equity markets and government data providers have joined the goal-seeking brigade, I see his statements as a measure of confidence in their ability to keep all those plates spinning.

Given that central banks control currencies, interest rates, and many futures and equity markets and government data providers have joined the goal-seeking brigade, I see his statements as a measure of confidence in their ability to keep all those plates spinning.

It’s certainly worked well so far. But, what happens when it doesn’t any more?

continued for members…

Bullard’s narrative only works if everything (except equity prices) continues to go sideways.

As such inflation remains a thorny issue. At 3%+, it requires higher interest rates which would upset the apple cart. With all due respect to Jamie Dimon, I see no way in the world the Fed will allow a return to a 5% 10Y. Therefore, I continue to see oil and gas prices dropping — at least to the former lows and potentially to the SMA200.

Therefore, I continue to see oil and gas prices dropping — at least to the former lows and potentially to the SMA200.

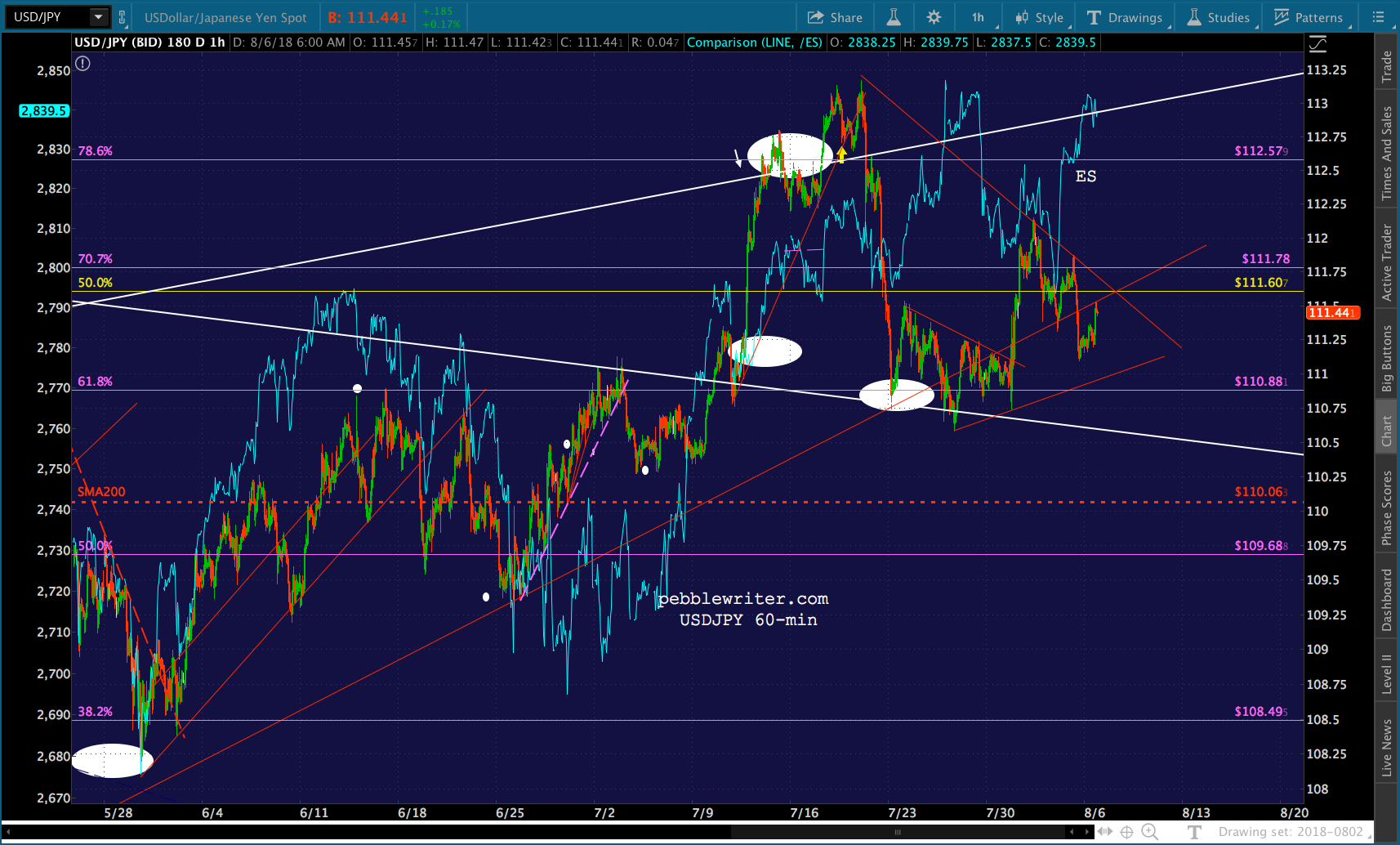

EURUSD and USDJPY are playing along with stock propping — extending the USD’s positive slope

EURUSD and USDJPY are playing along with stock propping — extending the USD’s positive slope

With the H&S Patterns battered but not quite broken, ES and SPX are in limbo.

With the H&S Patterns battered but not quite broken, ES and SPX are in limbo.

UPDATE: 1:00 PM

UPDATE: 1:00 PM

ES and SPX just popped through their Jul 25 highs, which were already north of the white .886s. It looks pretty clear at this point that the goal is to take out the Jan highs. The rising white channel crosses 2872 around this Friday (Aug 10) morning. We’re basically back to the same strategy as was used beginning in December 2016, dipping below the yellow channel top every time a little extra help is needed.

We’re basically back to the same strategy as was used beginning in December 2016, dipping below the yellow channel top every time a little extra help is needed.

It doesn’t mean there is no downside risk, simply that we’re much more likely to see new highs before any meaningful downside (with the usual headline risk caveats.) Once the new highs are established, we could easily see some meaningful drops. But, by then, the bearish Fib patterns will have been busted.

If the goal is simply to bust the bearish patterns (which I believe it is) then there’s a decent chance that CL and RB won’t make much headway until then. Note that RB’s SMA200 has almost reached the purple channel top. By Friday, it will have — and, very near the gray .786 Fib. CL is pretty clearly backtesting — which is often a sign of stalling. The yellow target is the intersection of the white channel midline and the .886 and my charts say tomorrow or Wednesday. Perhaps RB will lag.

CL is pretty clearly backtesting — which is often a sign of stalling. The yellow target is the intersection of the white channel midline and the .886 and my charts say tomorrow or Wednesday. Perhaps RB will lag. It’s important to note that the drops in RB and CL are often occurring during the after hours. So, if you’re a US-based trader playing the downside, know that it might come in the wee hours.

It’s important to note that the drops in RB and CL are often occurring during the after hours. So, if you’re a US-based trader playing the downside, know that it might come in the wee hours.

I have a meeting this afternoon that will keep me out the rest of the day. I’ll post more tonight if there’s anything startling. Otherwise, tomorrow morning.