CPI, due out tomorrow morning, always plays an important role in driving interest rates and economic forecasts. This one is especially important given the extent to which the market has already rallied in anticipation of lower rates.

Our gas price model for CPI shows inflation settling lower after a slight bump up over the last several months. But, what happens if events in the Middle East begin to affect oil/gas prices?

Our gas price model for CPI shows inflation settling lower after a slight bump up over the last several months. But, what happens if events in the Middle East begin to affect oil/gas prices?

At current prices, our model suggests CPI should continue to moderate – remaining around 3-3.25%. Again, this is if gas prices were to remain steady around 3.02 for regular conventional gas prices as reported by the EIA. This would result in the current -9.13% delta rising very slightly to -8.57% in February, then widening to as much as -19% by August before rising back toward 0% by January 2025.

In the past, these large negative deltas have correlated with CPI readings of 2% or less. Ceteris paribus, this would suggest a CPI in the 2% range by election time. But, what happens if hostilities in the Middle East expand and gas prices revert to 4.0? It’s a very different picture.

Bottom line, the Fed and the Biden administration are likely of one mind on the topic of Middle East affairs. A broader war that sends prices higher would be disastrous for both.

Bottom line, the Fed and the Biden administration are likely of one mind on the topic of Middle East affairs. A broader war that sends prices higher would be disastrous for both.

continued for members… (more…)

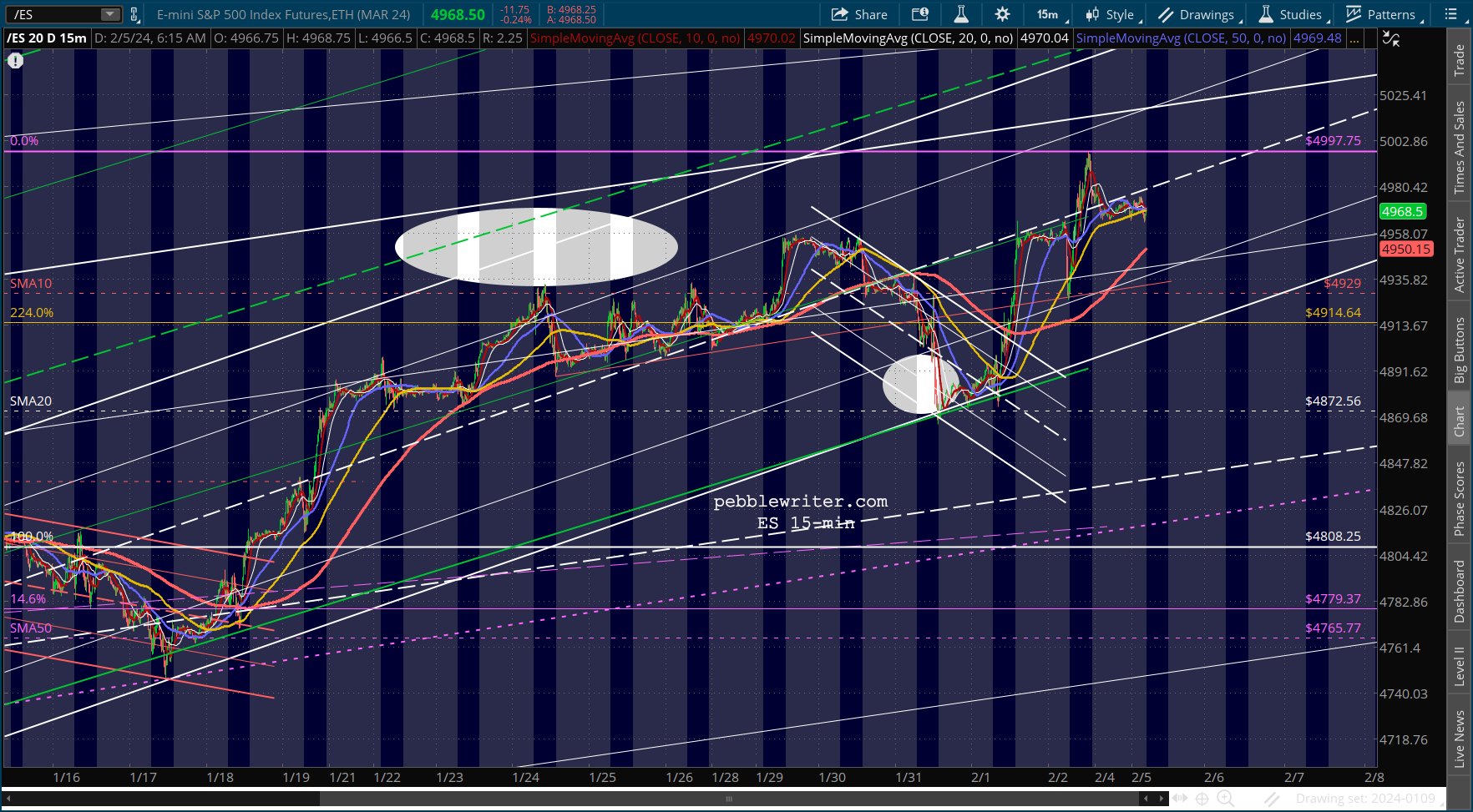

Futures have given up some of their slight overnight gains.

Futures have given up some of their slight overnight gains.