Yesterday’s 93-point bounce off our backtest target was remarkable — not because it was so extreme or resulted in new all-time highs, but because it surprised so many market experts.  The algos are not only very powerful (especially in an indecisive market), but are very difficult to rein in once they’re unleashed because of how they work in the first place – by triggering a cascade of buying by the massive passive universe of buyers. Happens every time.

The algos are not only very powerful (especially in an indecisive market), but are very difficult to rein in once they’re unleashed because of how they work in the first place – by triggering a cascade of buying by the massive passive universe of buyers. Happens every time.

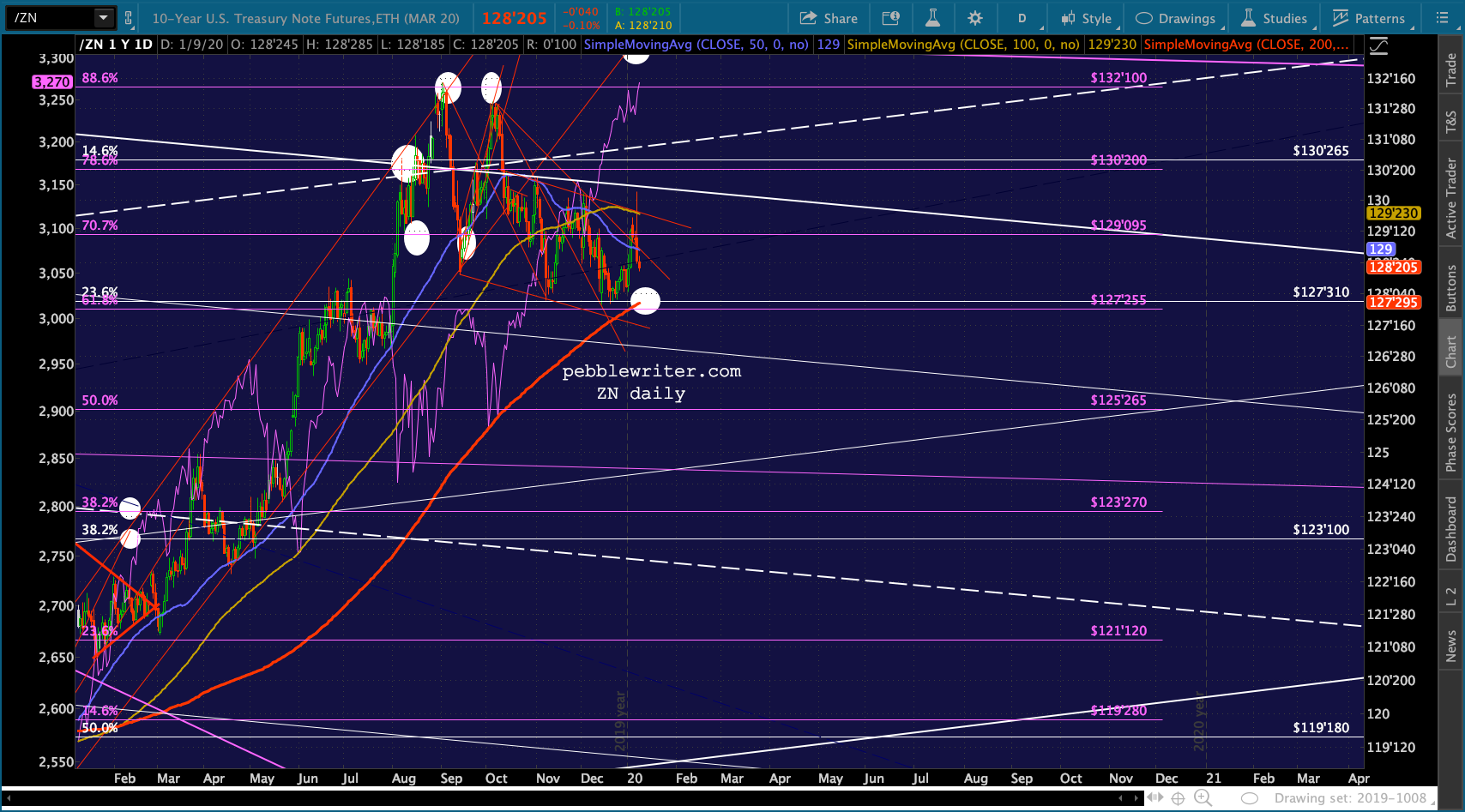

In the absence of another escalation in the Middle East, stocks are now in the clear — facing the same issues we’ve been discussing for the past month: a coming spike in inflation and a yield curve which still signals significant risk.

continued for members…

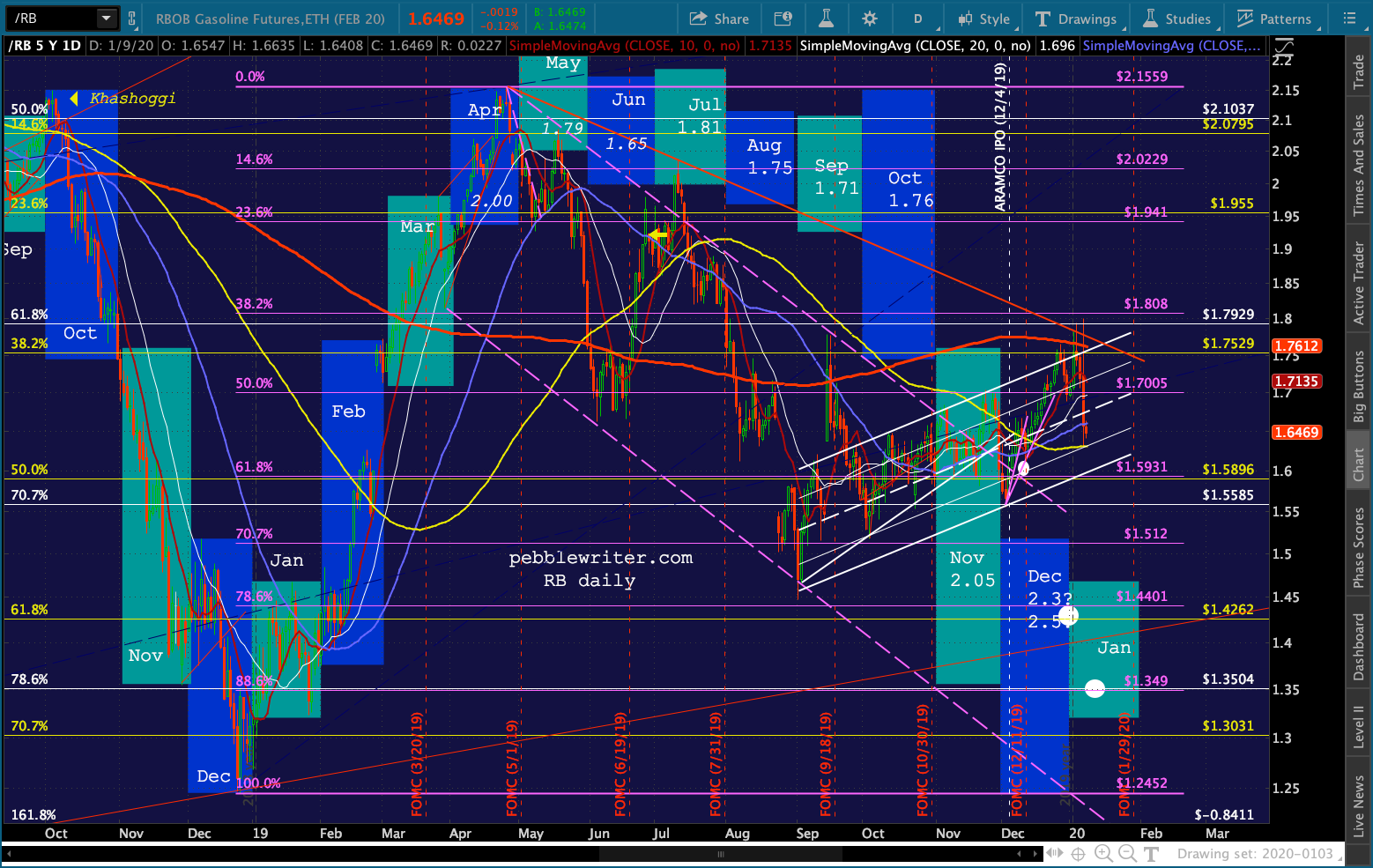

These are the charts to watch. If the 2s10s should continue to rise sharply, it poses big risks to the market. And, the drop still necessary in oil and gas prices in order to rein inflation back in – for January, at least – will be a headwind for stocks. Right now, the drop is viewed as a positive.

And, the drop still necessary in oil and gas prices in order to rein inflation back in – for January, at least – will be a headwind for stocks. Right now, the drop is viewed as a positive.

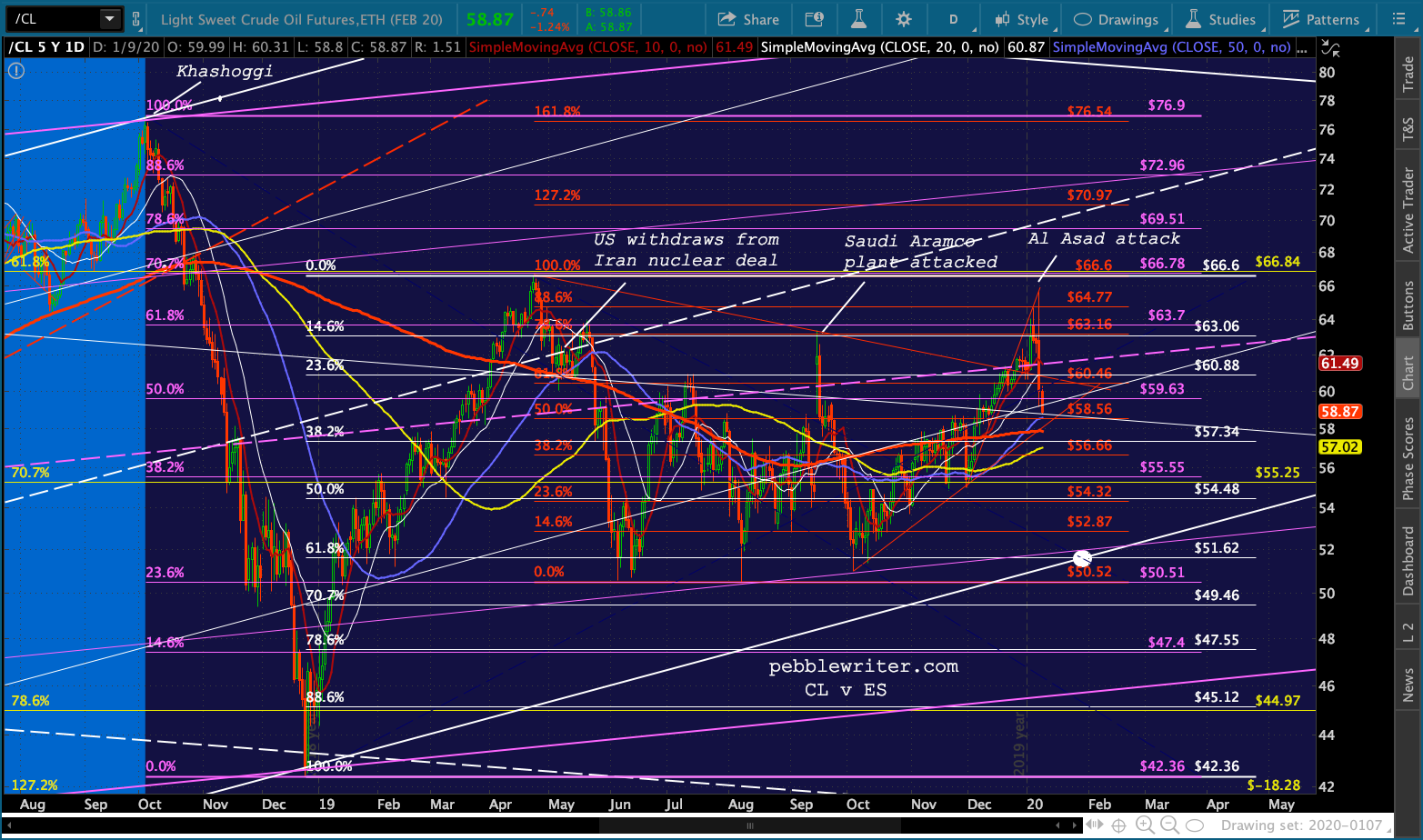

But, at some point, that sentiment will shift — probably when RB’s SMA100 or white channel breaks down… …and if/when CL’s red TL breaks down. Its SMA200 is currently right on top of it at 57.03. I’m looking for a drop to the white .618 and white channel bottom at 51.62.

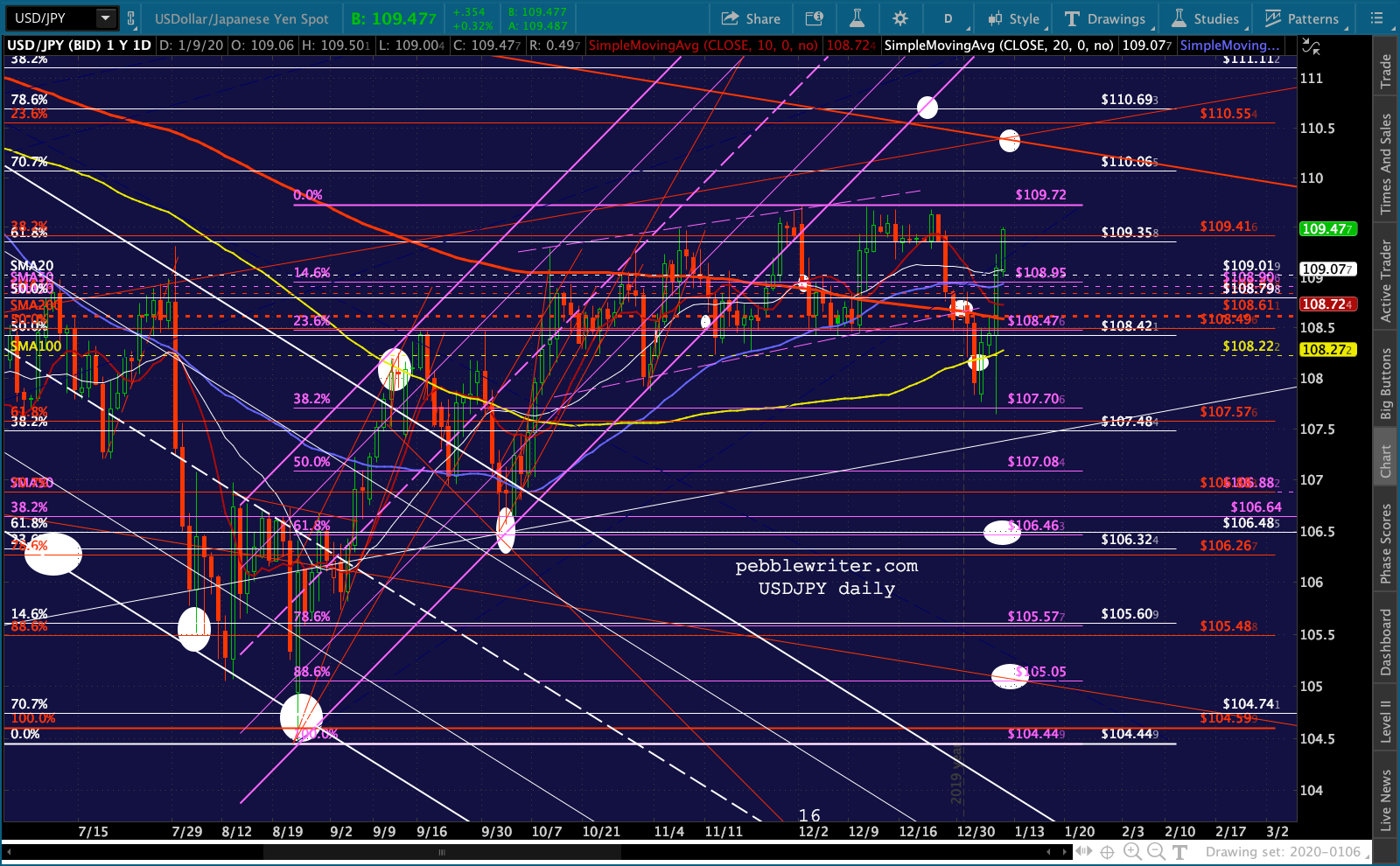

…and if/when CL’s red TL breaks down. Its SMA200 is currently right on top of it at 57.03. I’m looking for a drop to the white .618 and white channel bottom at 51.62. These risks will continue to be offset by a USDJPY which has no compunctions about reaching for those upside targets…

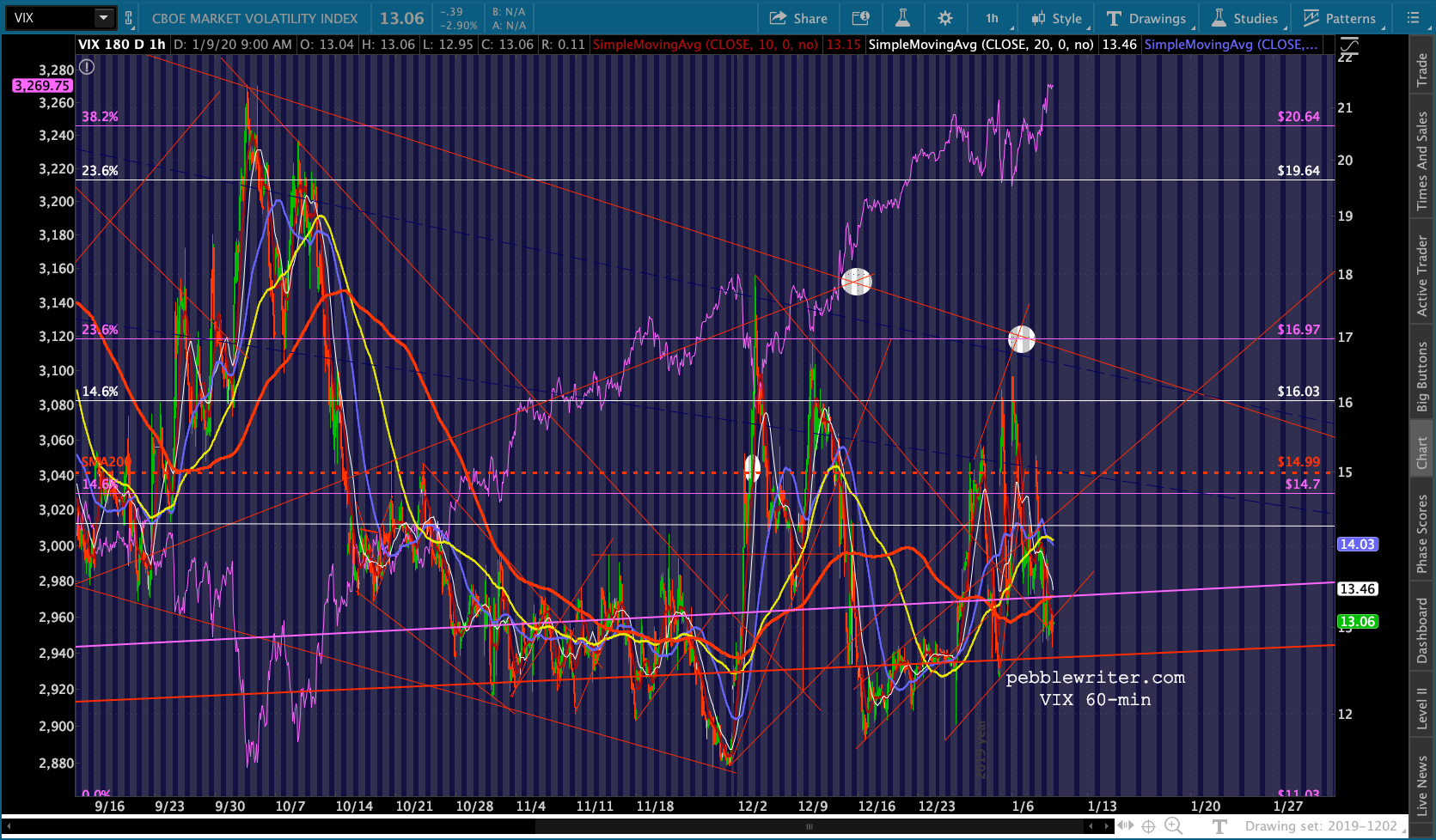

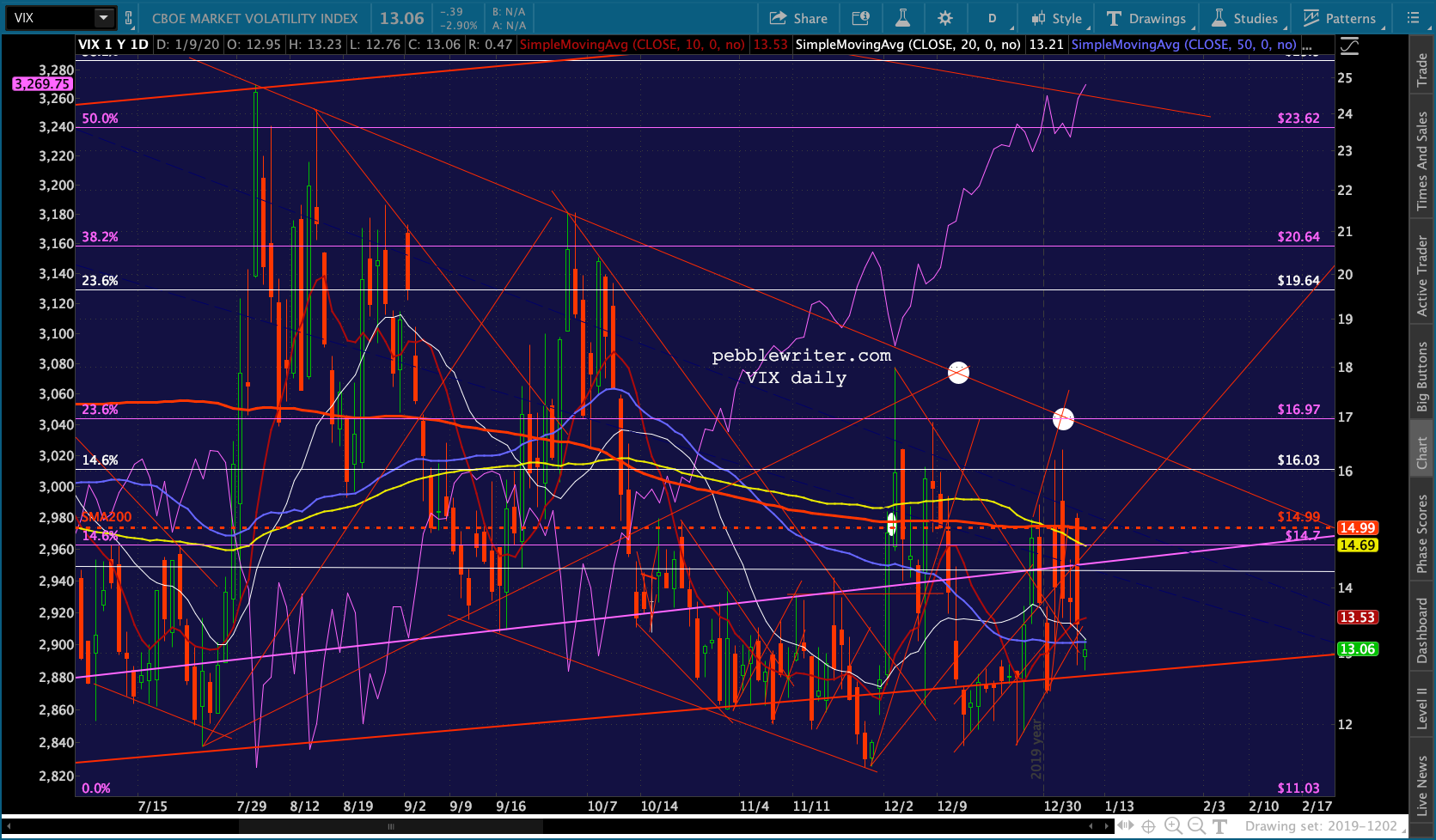

These risks will continue to be offset by a USDJPY which has no compunctions about reaching for those upside targets… …and, a VIX which has been easily controlled so far with breakdown after breakdown.

…and, a VIX which has been easily controlled so far with breakdown after breakdown.

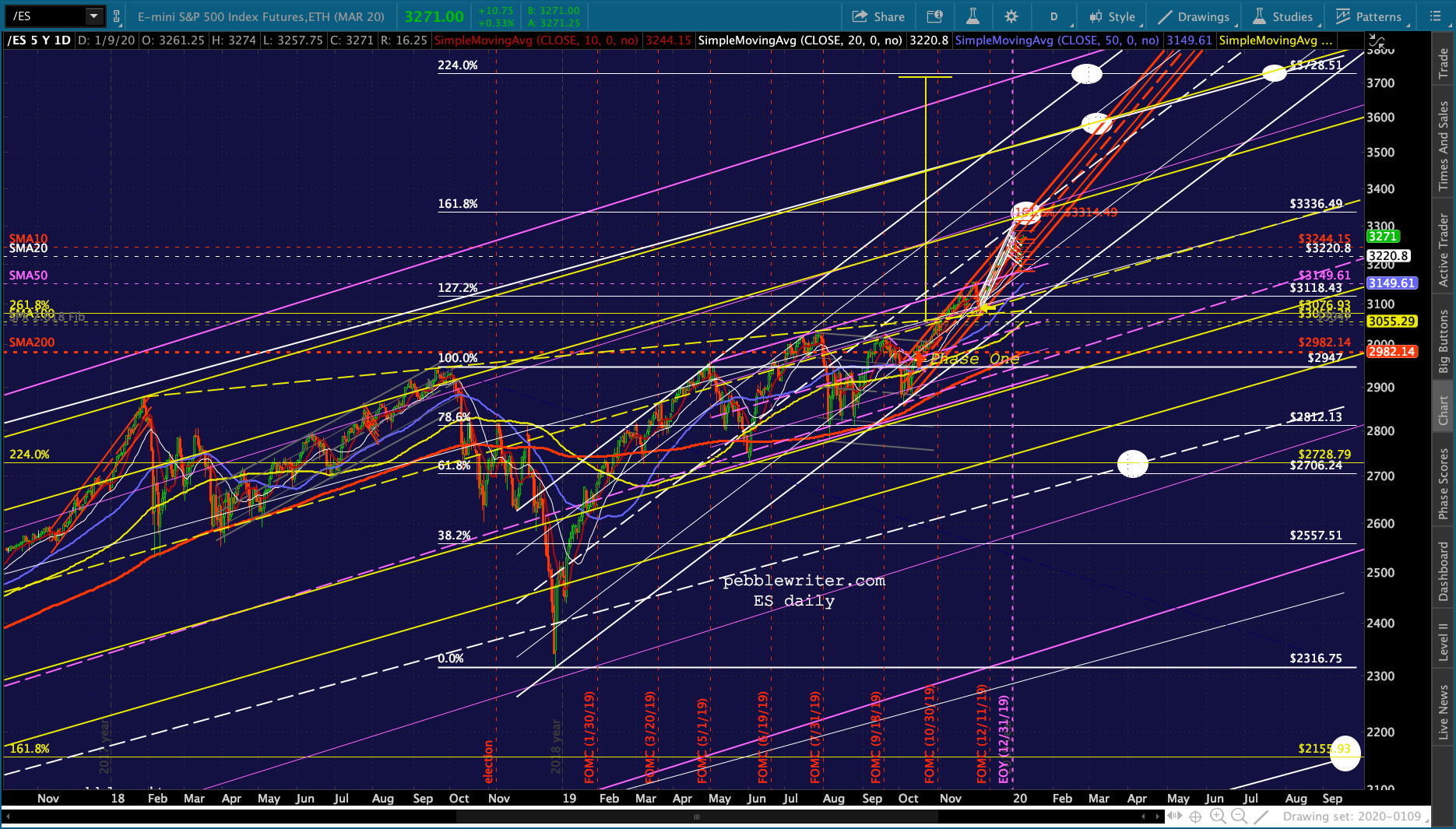

This leaves ES with a clear shot at the upside targets we’ve had for some time – again, in the absence of more MENA problems.

This leaves ES with a clear shot at the upside targets we’ve had for some time – again, in the absence of more MENA problems.  There are several paths it might take, but the one to watch will continue to be the rising red channel.

There are several paths it might take, but the one to watch will continue to be the rising red channel.

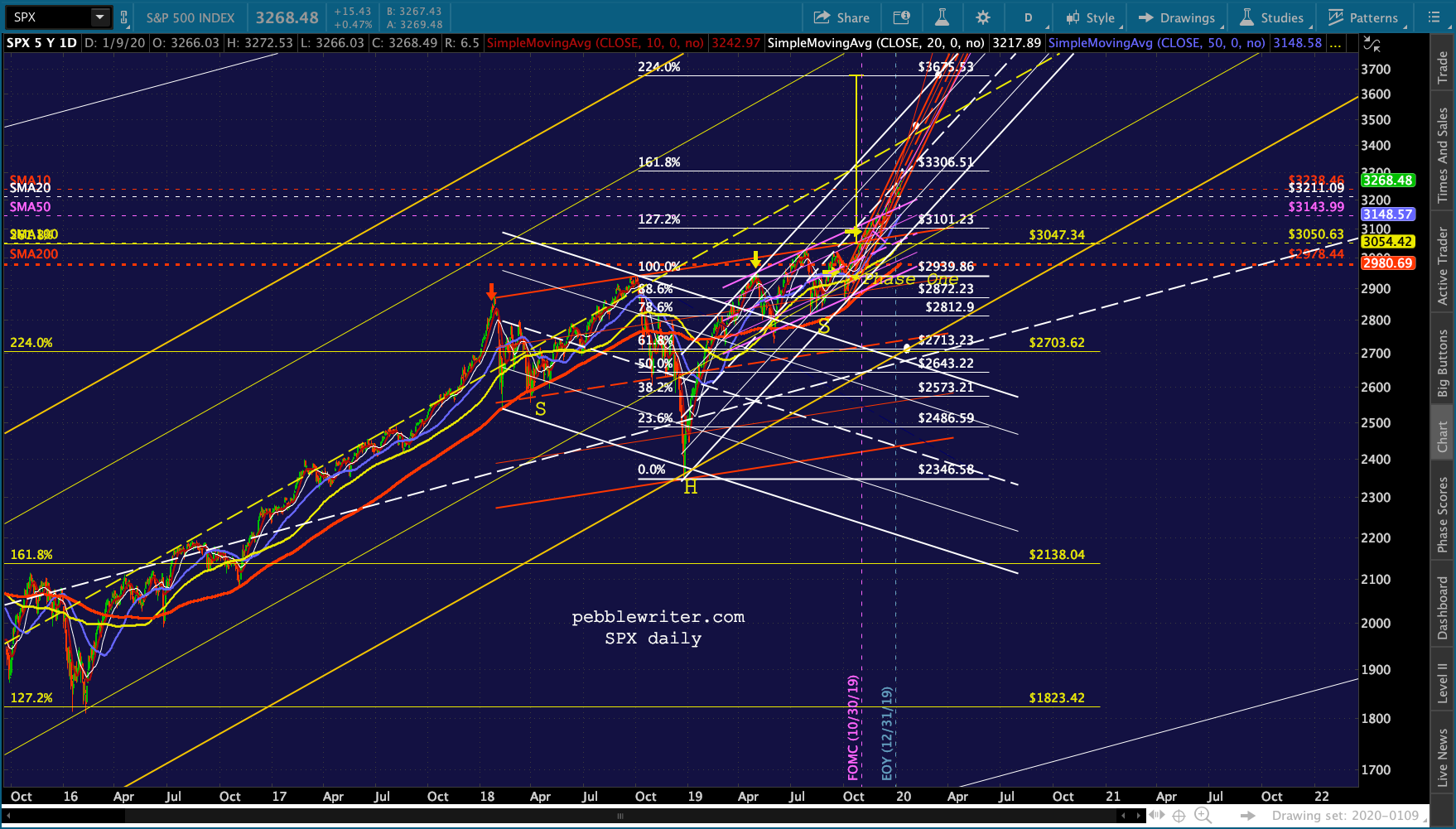

The downside targets remain on the chart as reference points and, in general, mark the point where rising channel bottoms intersect with major Fibs — some of which, like the 1.618 at 2138, have never been backtested.

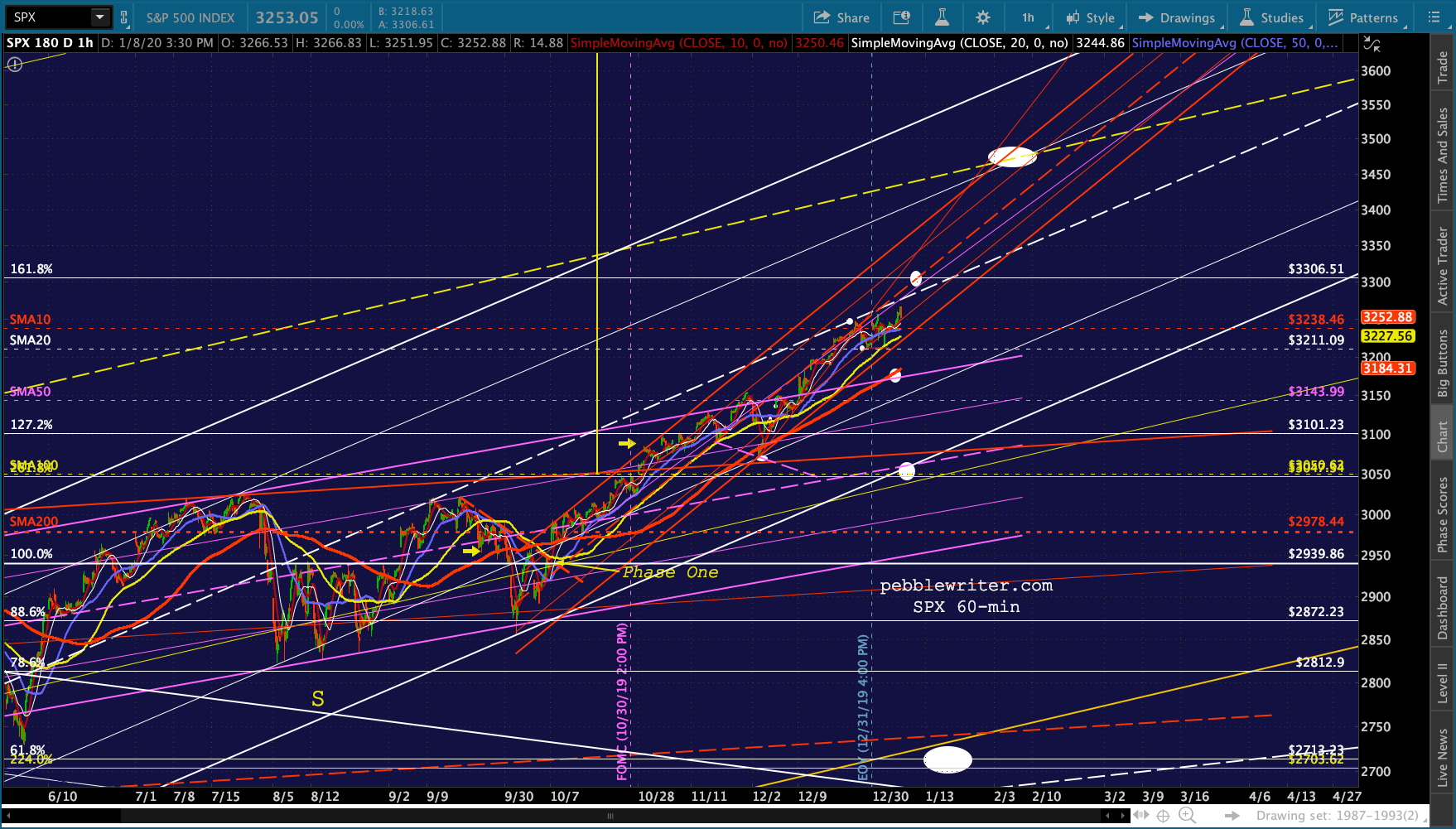

The SPX version:

The SPX version:

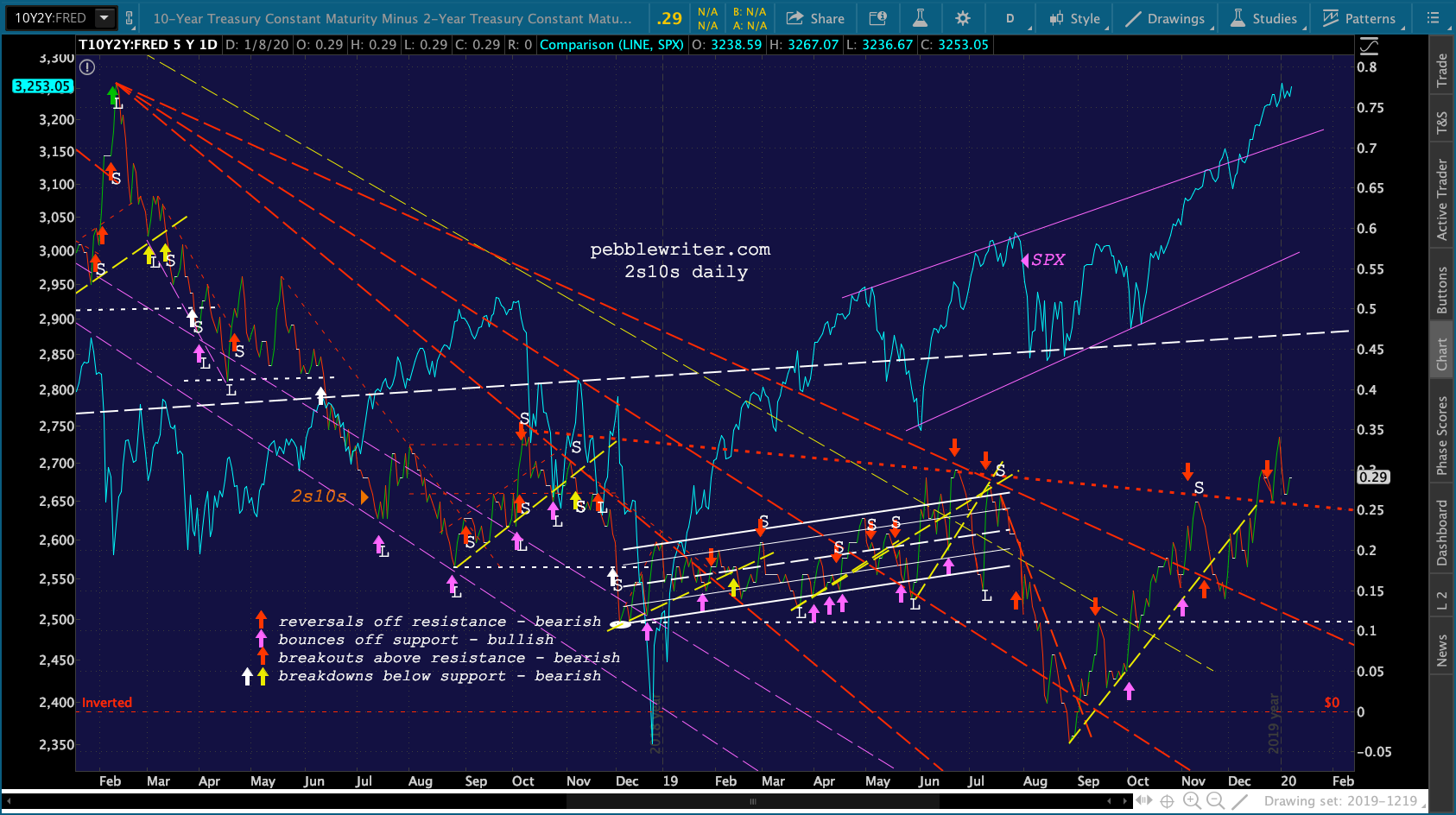

The threat posed by a breakdown of TNX is supposedly off the table for now, which means the 2s10s spread could continue to widen. The Fed’s challenge will be to keep it in the 25-35 bps range even after CPI tops expectations next week.

The threat posed by a breakdown of TNX is supposedly off the table for now, which means the 2s10s spread could continue to widen. The Fed’s challenge will be to keep it in the 25-35 bps range even after CPI tops expectations next week.

The fundamentals continue to be a concern. Earnings and revenues have generally been flat over the past year. Much of the economic data has been disappointing, with many measures at or near 2009 or 2015 lows. And, the upcoming impeachment and election promise plenty of fireworks.

The fundamentals continue to be a concern. Earnings and revenues have generally been flat over the past year. Much of the economic data has been disappointing, with many measures at or near 2009 or 2015 lows. And, the upcoming impeachment and election promise plenty of fireworks.

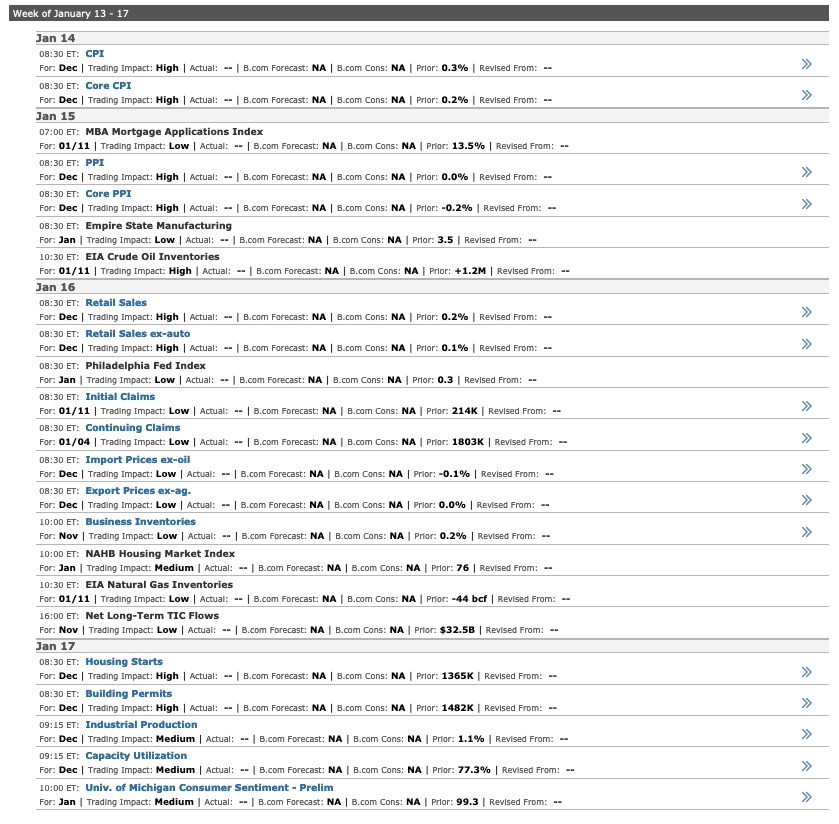

This week is almost over, with only tomorrow’s employment data left to digest. But, next week is chock full of potentially unsettling data: CPI, PPI, retail sales, Philly Fed, housing starts, building permits, industrial production and Michigan sentiment.