With currencies, commodities and yields coiling, it’s hard to shake the feeling that we’ve entered into a countdown of sorts.

While there’s reason to be optimistic from a pandemic standpoint, markets are making new all-time highs even though many important sectors of the economy are far from having recovered their mojo.

What gives? What awaits us on the other side of New Years?

If I’m right, we face a major regime change in the currency markets which will have important implications for stocks.

If I’m right, we face a major regime change in the currency markets which will have important implications for stocks.

continued for members…

I remain very nervous about lower equity prices ahead. I’ll explain.

While the algos have been very effective at propping up the markets at every turn, it seems that many of the drivers have become quite stretched.

A reminder – both ES and SPX remain broken down from the channels which began at the March lows. They have moved higher, but on very shaky ground from a charting standpoint.

The backtests which have been allowed have been carefully executed so as to not break trend. But, what happens when the algo drivers no longer offer a rising tide?

The backtests which have been allowed have been carefully executed so as to not break trend. But, what happens when the algo drivers no longer offer a rising tide?

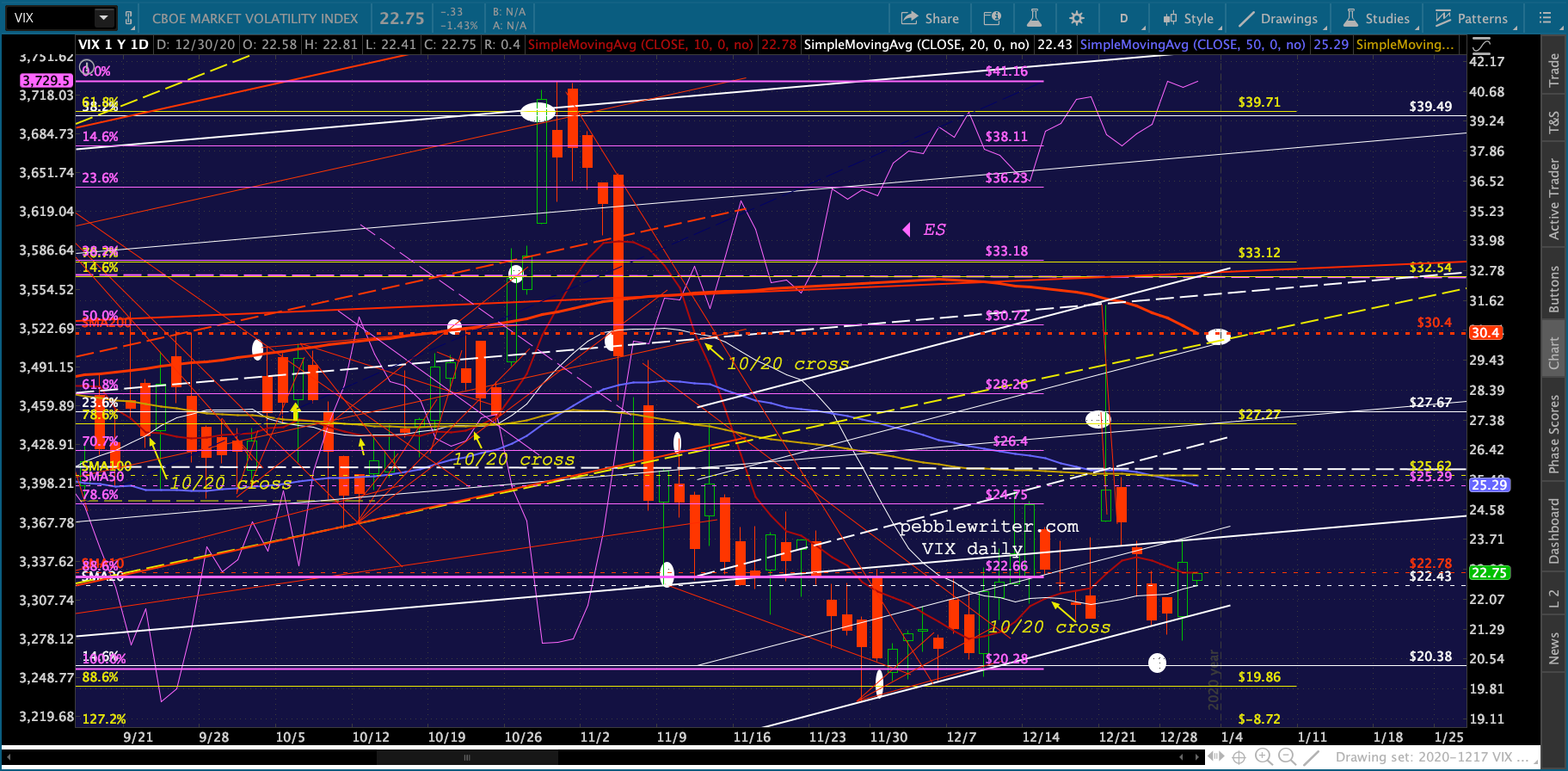

VIX has clearly been effective, with sharp declines when/as needed. There’s even the whiff of a bearish 10/20 cross in the air.

VIX has clearly been effective, with sharp declines when/as needed. There’s even the whiff of a bearish 10/20 cross in the air.

But, the others have run their course IMO.

But, the others have run their course IMO.

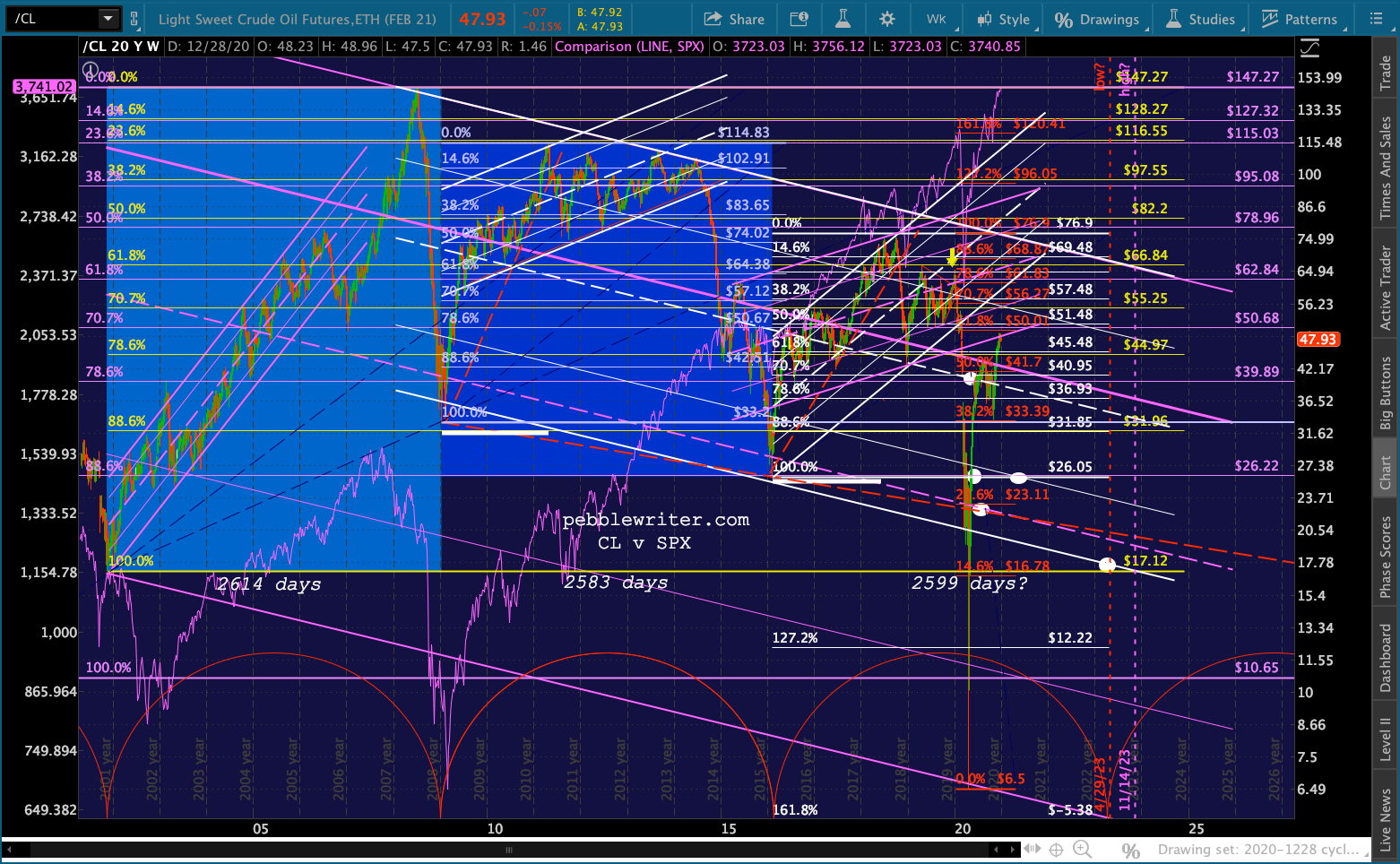

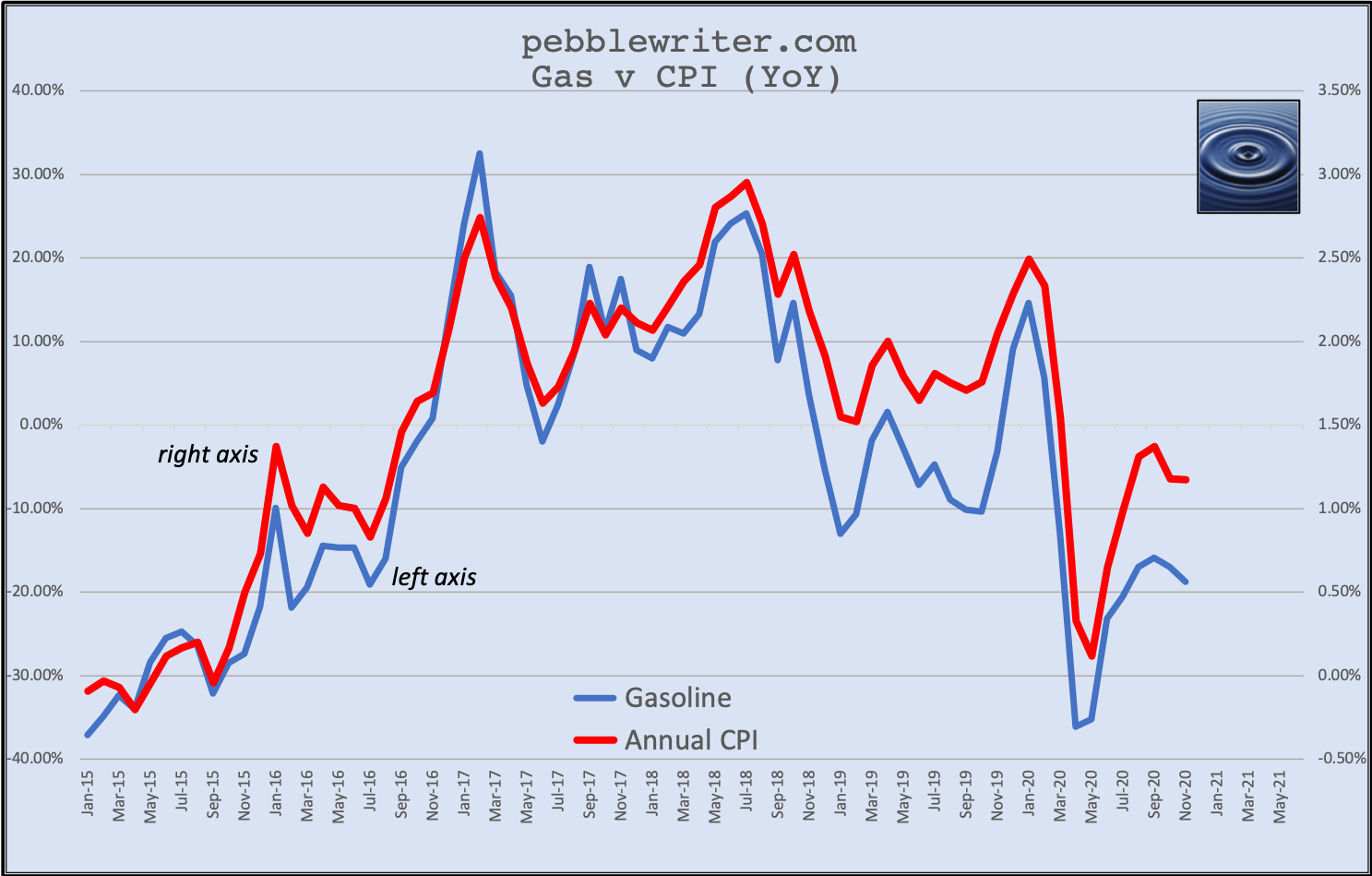

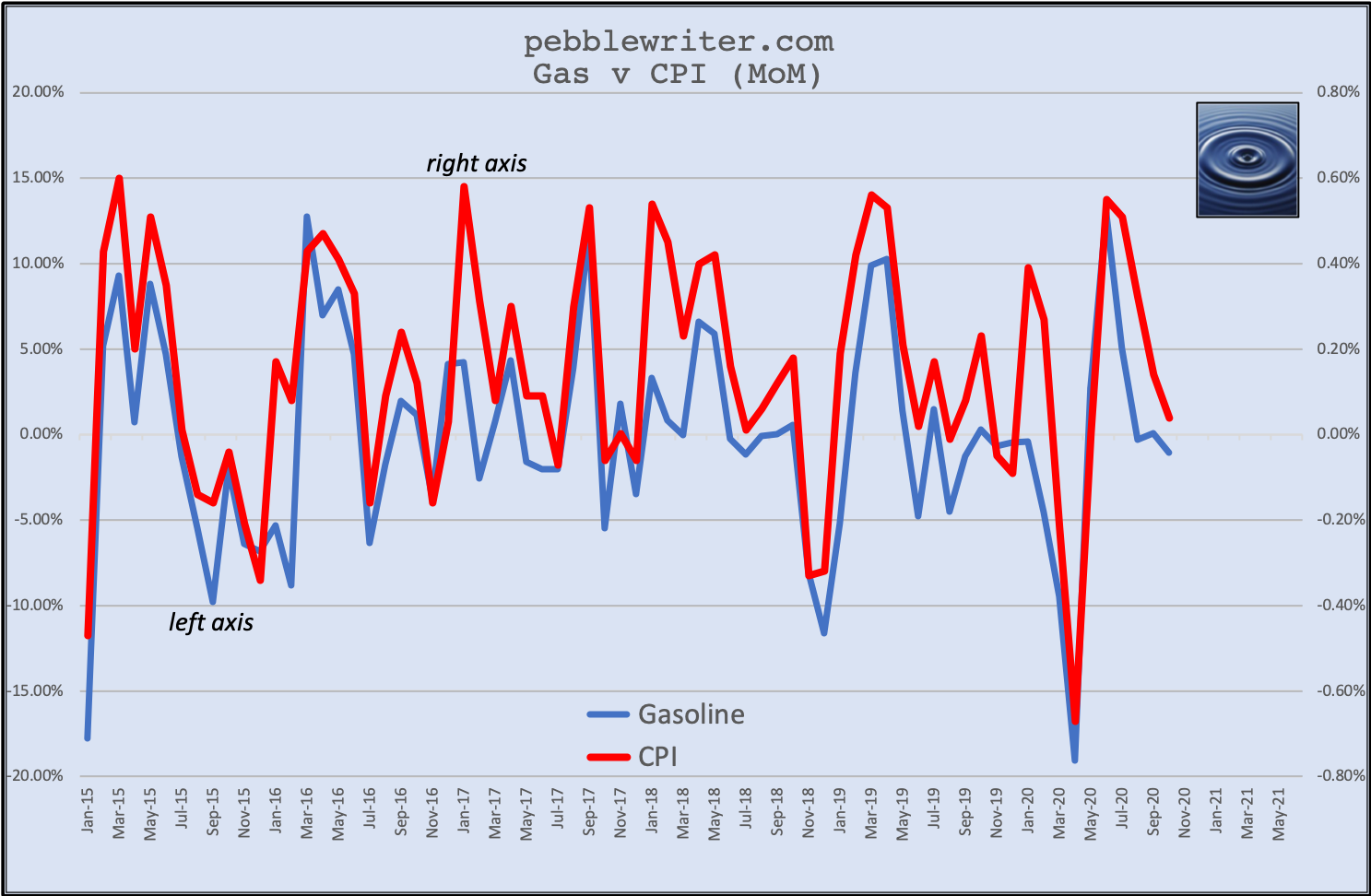

We’ve talked about CL and RB, which need to scream lower in the next two months in order to avoid an unseemly YoY increase in prices and, thus, inflation come Feb-Mar.

Remember these charts from Dec 10…

Remember these charts from Dec 10…

…and the implication: Oil and gas will have to fall significantly by April or we’re looking at a potential 20% YoY increase in gas prices – which has historically produced 2.4-2.7% annual inflation and a 2%+ 10Y.

…and the implication: Oil and gas will have to fall significantly by April or we’re looking at a potential 20% YoY increase in gas prices – which has historically produced 2.4-2.7% annual inflation and a 2%+ 10Y.

Likewise, we’ve talked about the dollar and the fact that it’s at very important support. If it falls any further, it could quickly shed another 7-13%. As a net importer, imagine what that would do to US inflation. I don’t believe the Fed has any intention of permitting such a move.

Likewise, we’ve talked about the dollar and the fact that it’s at very important support. If it falls any further, it could quickly shed another 7-13%. As a net importer, imagine what that would do to US inflation. I don’t believe the Fed has any intention of permitting such a move.

USDJPY is breaking down again and should have no trouble falling to 102.37-101.18. I suspect TPTB are preparing it for a rebound which will have primary responsibility for levitating stocks — in other words, dollar strength.

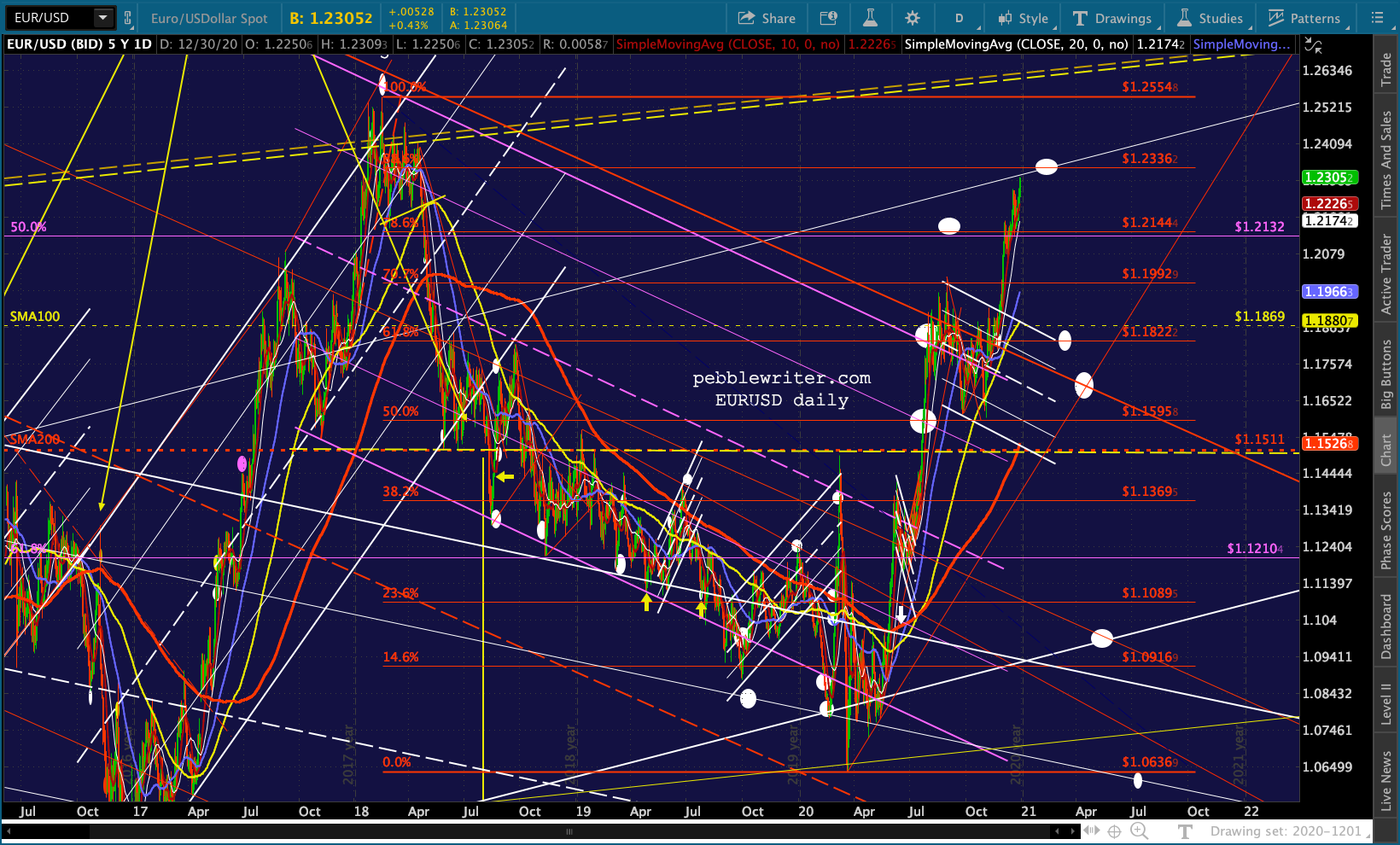

USDJPY is breaking down again and should have no trouble falling to 102.37-101.18. I suspect TPTB are preparing it for a rebound which will have primary responsibility for levitating stocks — in other words, dollar strength. Earlier this morning, EURUSD came within 0.2% of our 1.2336 target – close enough for shorting. Again, more dollar strength on the way.

Earlier this morning, EURUSD came within 0.2% of our 1.2336 target – close enough for shorting. Again, more dollar strength on the way. The 10Y has been edging higher for almost 5 months on the notion of the economy re-inflating – the reflation trade.

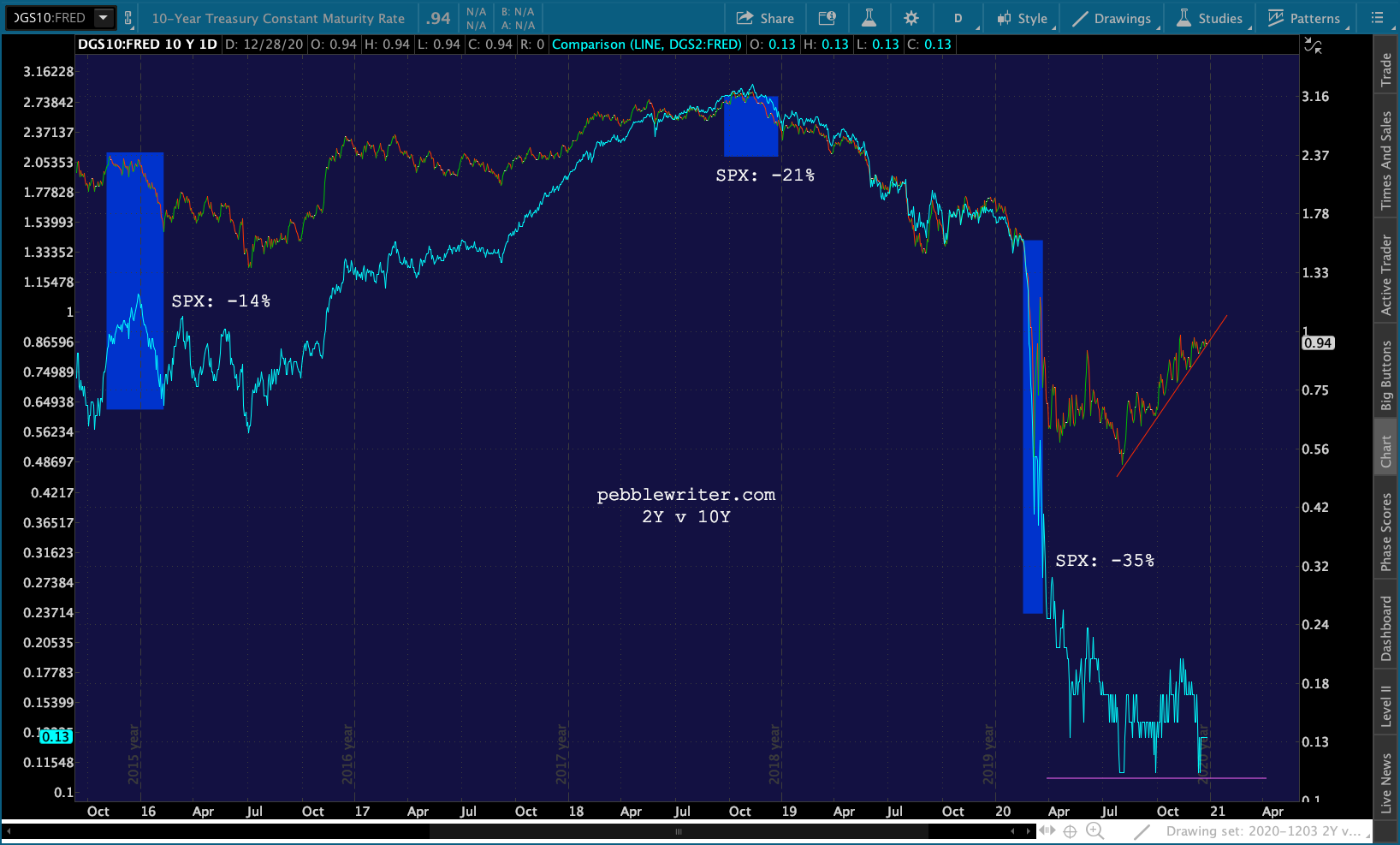

The 10Y has been edging higher for almost 5 months on the notion of the economy re-inflating – the reflation trade.  At this rate, it would lead to a sharp widening in the 2s10s, which we know is bearish for stocks – another reason it won’t be allowed to happen.

At this rate, it would lead to a sharp widening in the 2s10s, which we know is bearish for stocks – another reason it won’t be allowed to happen. This means that the 10Y will need to be reined in. And, a drop in the 10Y means a rebound in DXY – again, dollar strength.

This means that the 10Y will need to be reined in. And, a drop in the 10Y means a rebound in DXY – again, dollar strength.

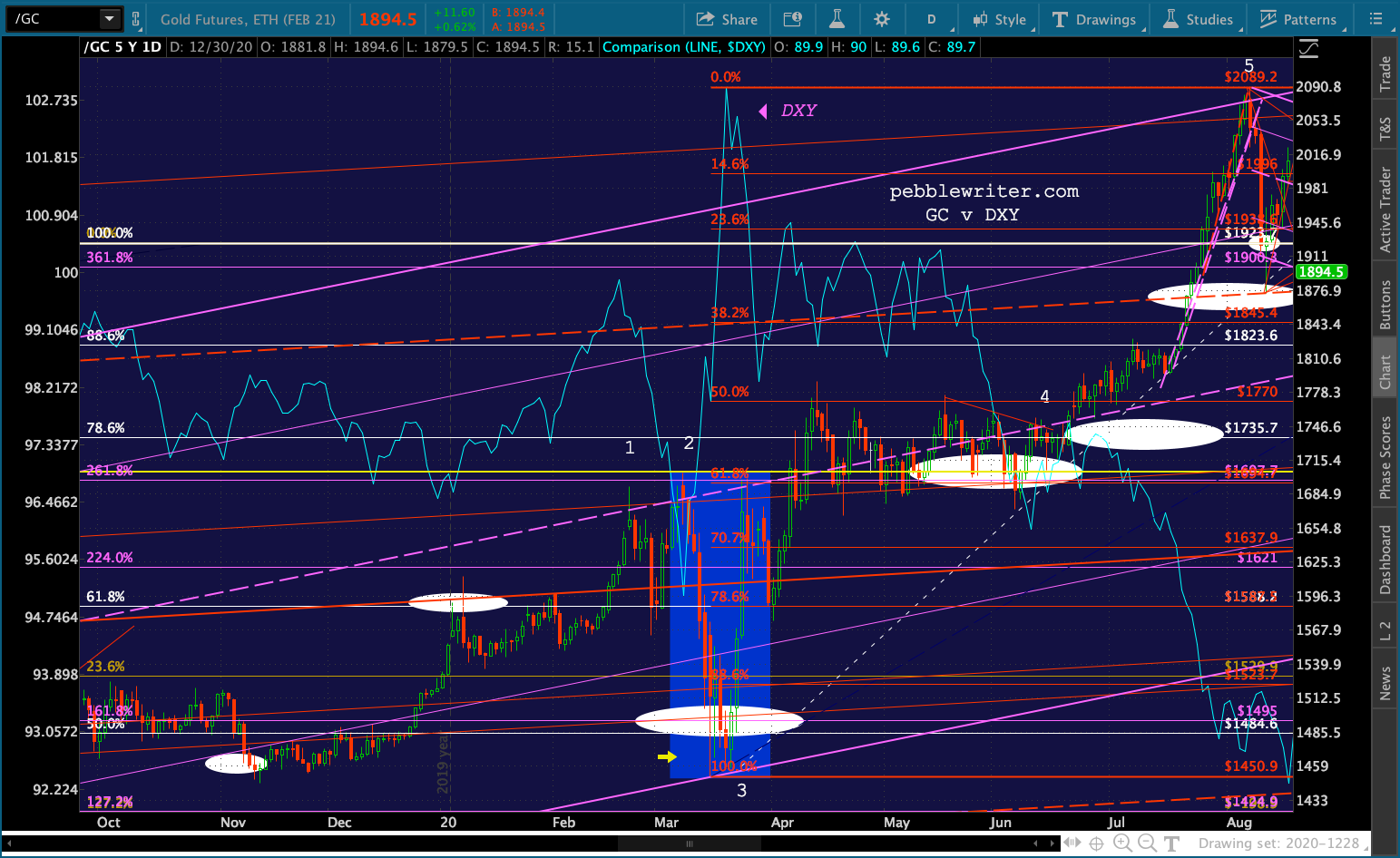

The only fly in the model’s ointment: gold. Gold and silver have been stymied lately, unable to break out of their falling channels.

The only fly in the model’s ointment: gold. Gold and silver have been stymied lately, unable to break out of their falling channels.

Perhaps the reflation theory isn’t that compelling. Or perhaps I’m not the only one expecting a rebound in DXY. But, a sharp drop in the 10Y produces a sharp rise in ZN which has typically been very beneficial to gold prices.

Perhaps the reflation theory isn’t that compelling. Or perhaps I’m not the only one expecting a rebound in DXY. But, a sharp drop in the 10Y produces a sharp rise in ZN which has typically been very beneficial to gold prices.

As an aside, these drops in ZN have been beneficial to stock prices.

As an aside, these drops in ZN have been beneficial to stock prices.

The underlying premise, then, is that DXY and GC always move opposite to one another. A sharp drop in interest rates and DXY can sometimes correspond with a drop in GC.

It typically only happens in periods of great distress in the markets. Last March, for instance, ZN and DXY initially plunged along with GC as interest rates tumbled.  But, DXY quickly reversed course and zoomed higher, only topping out when GC bottomed out.

But, DXY quickly reversed course and zoomed higher, only topping out when GC bottomed out.  This is because sometimes the DXY rises with rising rates — and sometimes it falls. As we’ve discussed before, it depends on the underlying reason. The fear trade can produce strange correlations.

This is because sometimes the DXY rises with rising rates — and sometimes it falls. As we’ve discussed before, it depends on the underlying reason. The fear trade can produce strange correlations.

I believe this is what should expect going forward: falling interest rates, a rising DXY, falling euro, falling GC, falling RB/CL, and – depending on whether or not USDJPY rallies – falling stock prices.

The appeal to taking such a position is that we’ll know rather quickly whether or not it’s correct by whether or not we see the reversals suggested above – particularly EURUSD, DXY, GC and SI. If they all violate our reversal targets, then all bets are off. Rates are probably going higher and we will have much bigger problems ahead.

It rests on the presumption that, despite what they say, the Fed will take action to prevent higher inflation and interest rates. I base this primarily on the path the BoJ has taken. They have spent almost 10 years bitching about needing higher inflation when what they’ve really wanted was insanely low interest rates and an excuse to prop up equities – which has done absolutely nothing to produce higher inflation.

I believe the US is on the exact same path and the Fed will have no choice but to take the exact same actions.

stay tuned…