At some point – perhaps after six months of hot inflation data – the Fed will be forced to admit that inflation pressure are not transitory. This morning we saw evidence that March personal incomes spiked by 21.1%, the most since 1946. Personal spending for the month shot up 4.2%, the most since last June. And, PCE’s 2.3% is the biggest since 2018.

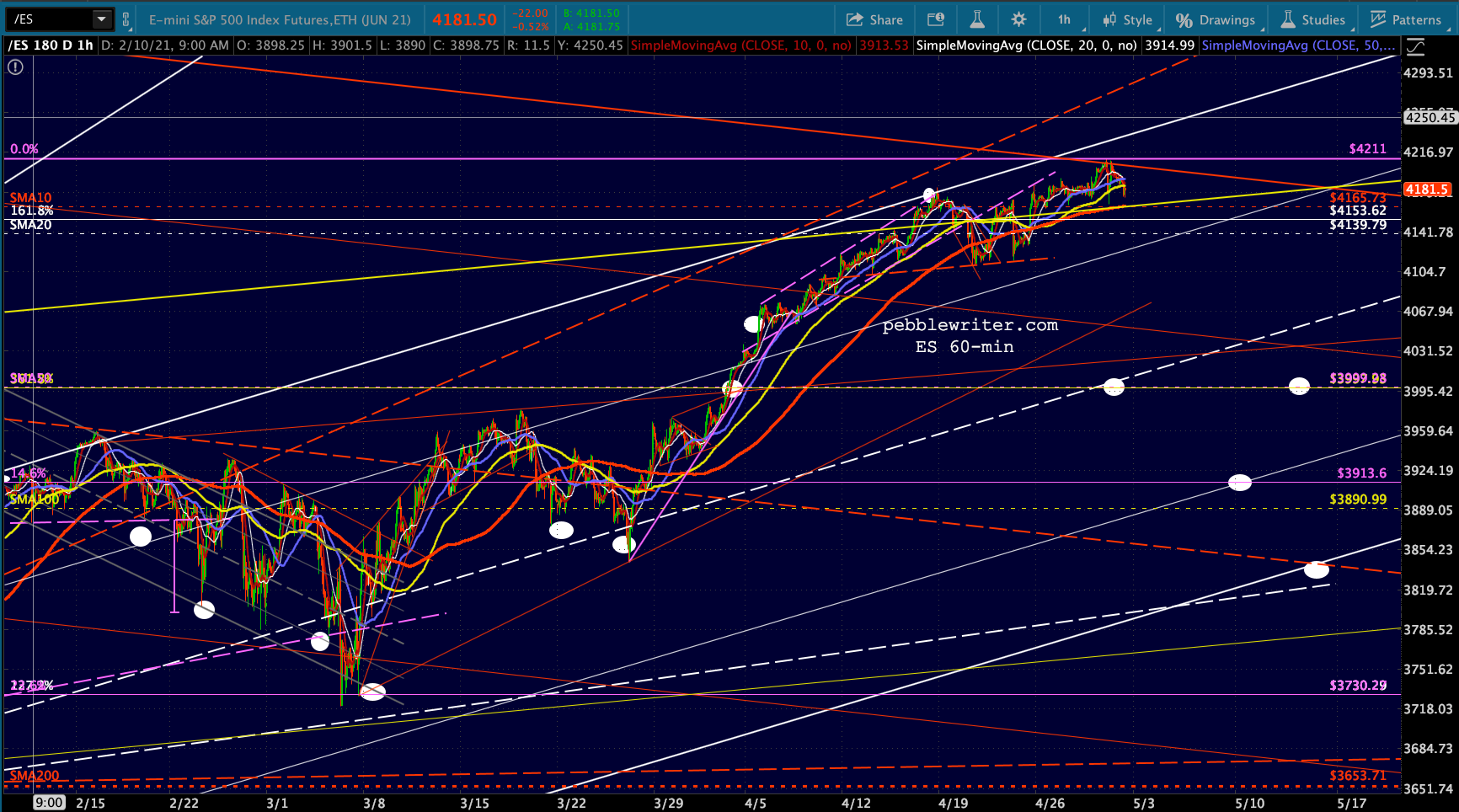

S&P futures are calling BS on the whole modest/transitory inflation story – off over 20 points so far.

S&P futures are calling BS on the whole modest/transitory inflation story – off over 20 points so far.

And, VIX’s bullish (bearish for stocks) 10/20 cross hasn’t gone away.

And, VIX’s bullish (bearish for stocks) 10/20 cross hasn’t gone away.

continued for members…Still lots of downside potential, as long as VIX and USDJPY play along.

VIX’s “breakdown” could persist, but the SMA200 is in a very nice place for a backtest.

VIX’s “breakdown” could persist, but the SMA200 is in a very nice place for a backtest.

And, as discussed yesterday, USDJPY faces another test of the falling purple channel top…

And, as discussed yesterday, USDJPY faces another test of the falling purple channel top…

…as EURUSD runs into overhead resistance…

…as EURUSD runs into overhead resistance…  …meaning we could get another bounce by DXY here at its channel bottom.

…meaning we could get another bounce by DXY here at its channel bottom.  This is typically bearish for GC/SI – the thin purple line above – so I’d revert to short on gold and silver at this point with tight stops at the SMA100. I understand this is completely contrary to my inflation outlook – but the charts suggest that GC/SI will continue to be be suppressed.

This is typically bearish for GC/SI – the thin purple line above – so I’d revert to short on gold and silver at this point with tight stops at the SMA100. I understand this is completely contrary to my inflation outlook – but the charts suggest that GC/SI will continue to be be suppressed.

I remain bearish on CL/RB as well, for all the reasons we’ve discussed over the past few days.

I remain bearish on CL/RB as well, for all the reasons we’ve discussed over the past few days.

Bond yields initially pushed slightly higher, but have been hammered back down and are now slightly lower. Note that TNX again backtested the horizontal resistance that marked the Feb 2020 breakdown.

Bond yields initially pushed slightly higher, but have been hammered back down and are now slightly lower. Note that TNX again backtested the horizontal resistance that marked the Feb 2020 breakdown.

BTW, I’ve updated the current forecast page for the primary charts. Now that most of my operations are behind me, I pledge to do a better job keeping up with this page for those who aren’t able to read the daily posts (where obviously more current charts are posted.) My goal is to do so at the end of each month, so always check the daily posts if you’re not sure what the current outlook is.

BTW, I’ve updated the current forecast page for the primary charts. Now that most of my operations are behind me, I pledge to do a better job keeping up with this page for those who aren’t able to read the daily posts (where obviously more current charts are posted.) My goal is to do so at the end of each month, so always check the daily posts if you’re not sure what the current outlook is.

GLTA.