Q3 GDP came in at 2.6%, beating the 2.3% consensus and of course Q2’s -0.6%. While good news for the economy, it does little to advance the narrative that the Fed might be ready to pare future rate hikes.

Nevertheless, VIX fell…

Nevertheless, VIX fell… …so futures rose slightly on the news.

…so futures rose slightly on the news. continued for members…

continued for members…

Durable orders came in at 0.4% as expected, but without transportation fell 0.5% versus +0.2% consensus. The chain deflator was lighter than consensus at 4.1%, but the more important PCE is coming out tomorrow, along with ersonal income, personal spending, pending home sales and Michigan sentiment.

SPX and ES are still testing their SMA50s, while COMP is still backtesting its broken channel.

As mentioned above, the tech-heavy COMP continues to struggle. It put in an obvious reversal candle yesterday, and is set to open lower…

As mentioned above, the tech-heavy COMP continues to struggle. It put in an obvious reversal candle yesterday, and is set to open lower…

…as its 60-min chart shows it rolling over and nearing a breakdown…

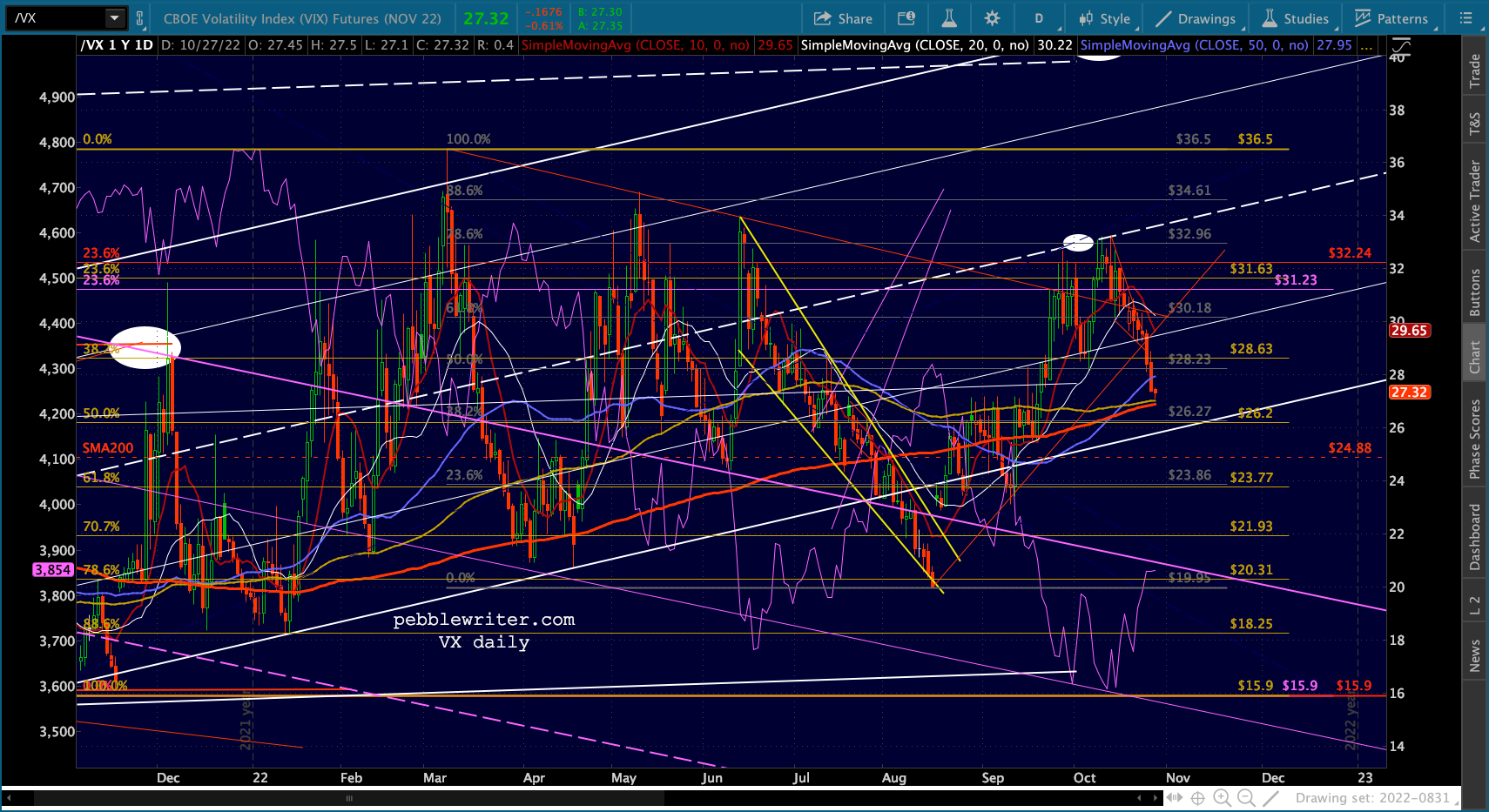

…as its 60-min chart shows it rolling over and nearing a breakdown… …and VX (VIX futures) runs smack dab into its SMA200.

…and VX (VIX futures) runs smack dab into its SMA200. The VIX itself has a little further to go.

The VIX itself has a little further to go.

The other big news this morning came from the ECB, which hiked 75 bps as expected. The EURUSD reversed at the red channel top as expected.

The other big news this morning came from the ECB, which hiked 75 bps as expected. The EURUSD reversed at the red channel top as expected. The USDJPY is struggling to hold its 1998 highs.

The USDJPY is struggling to hold its 1998 highs. This means additional support for DXY, which is nearing a TL off its January lows.

This means additional support for DXY, which is nearing a TL off its January lows. I want to point out an important phenomenon for EURUSD. Note that every single time EURUSD retreated from the red TL (the white arrows) SPX tumbled. It worked with the lower, white TL as well. This illustrates the importance but risk of the euro carry trade – all the more crucial as USDJPY was headed to the moon.

I want to point out an important phenomenon for EURUSD. Note that every single time EURUSD retreated from the red TL (the white arrows) SPX tumbled. It worked with the lower, white TL as well. This illustrates the importance but risk of the euro carry trade – all the more crucial as USDJPY was headed to the moon. If the dollar strengthens from here, it will reinforce the idea of the 10Y yield bouncing off its purple TL from August (also, the purple channel midline.)

If the dollar strengthens from here, it will reinforce the idea of the 10Y yield bouncing off its purple TL from August (also, the purple channel midline.)

This, in turn, would be perfectly in keeping with the ongoing bounce in CL/RB…

This, in turn, would be perfectly in keeping with the ongoing bounce in CL/RB…

…which might be in trouble if XLE has anything to say about it.

…which might be in trouble if XLE has anything to say about it.

If DXY is about to rebound sharply, it certainly doesn’t bode well for GC, SI or BTC.

If DXY is about to rebound sharply, it certainly doesn’t bode well for GC, SI or BTC.