Stocks are essentially flat following a slight downward revision in Q1 GDP from -1.5% to -1.6% and export numbers which are truly circling the drain.

The disappointing data came on the heels of the worst consumer confidence reading since Feb 2021 and three (so far) Fed presidents advocating a 75 bps rate hike in July.

The disappointing data came on the heels of the worst consumer confidence reading since Feb 2021 and three (so far) Fed presidents advocating a 75 bps rate hike in July.

continued for members…Once this little flag pattern breaks down, the next leg down should be ugly.

VIX should test its SMA10 today. A pullback means TPTB are committed to saving the 2Q from the ignominy of a -20% print.

VIX should test its SMA10 today. A pullback means TPTB are committed to saving the 2Q from the ignominy of a -20% print.  EURUSD is back below its SMA10 and should resume its fall very soon.

EURUSD is back below its SMA10 and should resume its fall very soon. Although USDJPY is edging higher…

Although USDJPY is edging higher… …it won’t be enough to prevent new highs for DXY.

…it won’t be enough to prevent new highs for DXY. GC and SI are holding on, but for how long? SI looks especially vulnerable.

GC and SI are holding on, but for how long? SI looks especially vulnerable.

And, BTC’s attempt to retake its SMA10 has failed.

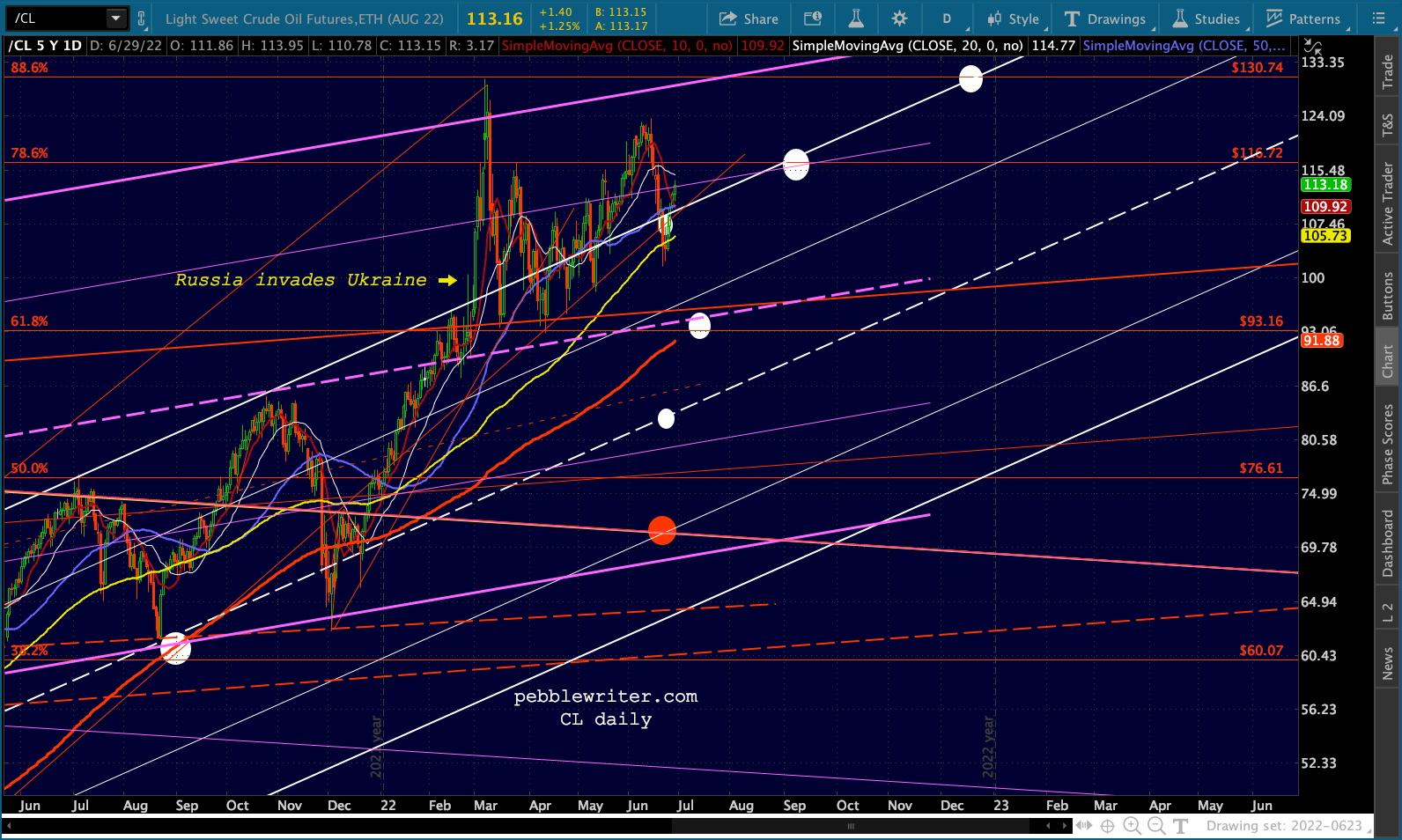

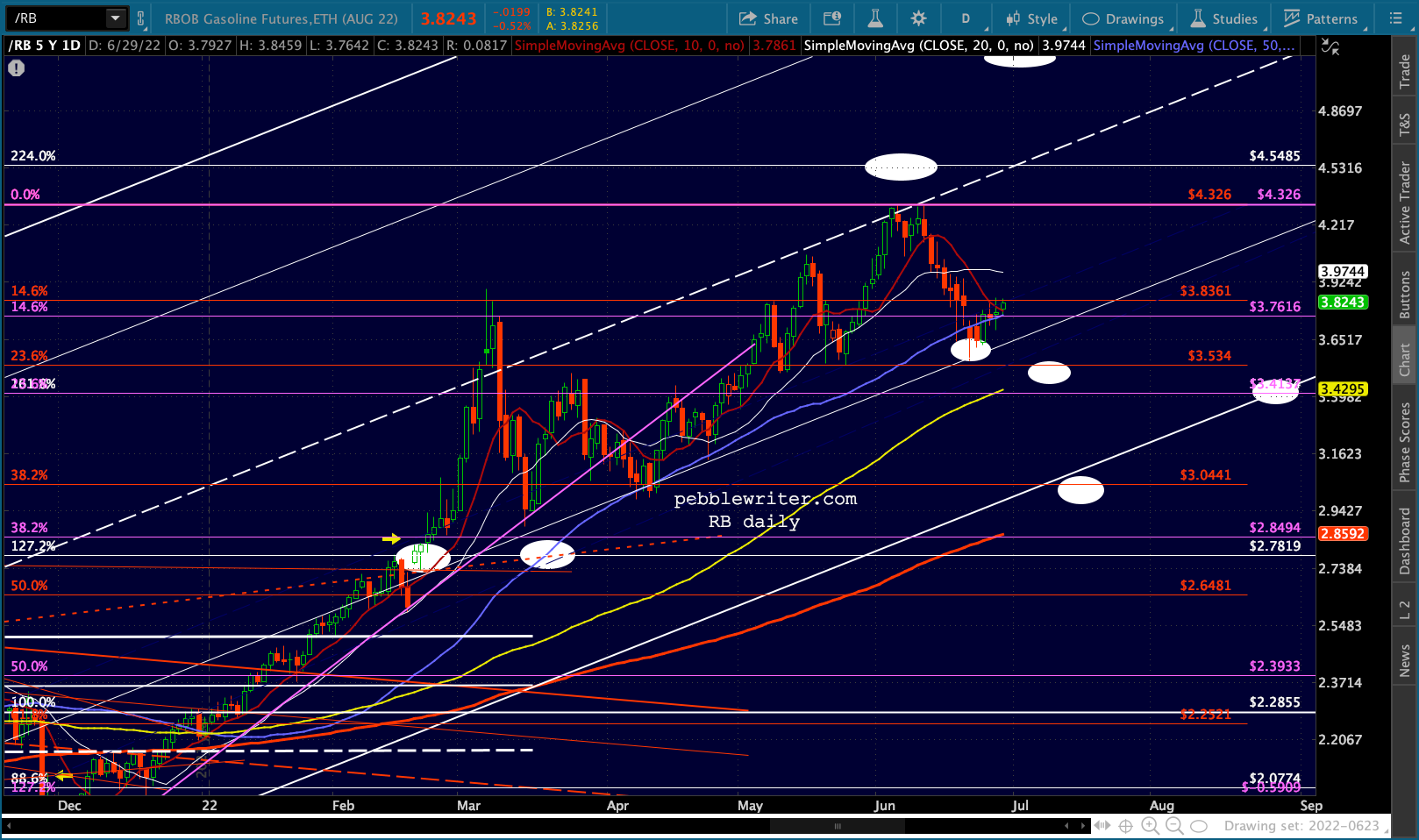

And, BTC’s attempt to retake its SMA10 has failed. Oil and gas are split, with CL putting in a small increase and RB a small decrease.

Oil and gas are split, with CL putting in a small increase and RB a small decrease.

This leaves the 10Y still on the TL from March, still thinking about that backtest.

This leaves the 10Y still on the TL from March, still thinking about that backtest.  Yesterday’s meltdown was a stark reminder of the coming downdraft our analog suggests will occur over the next three weeks.

Yesterday’s meltdown was a stark reminder of the coming downdraft our analog suggests will occur over the next three weeks.

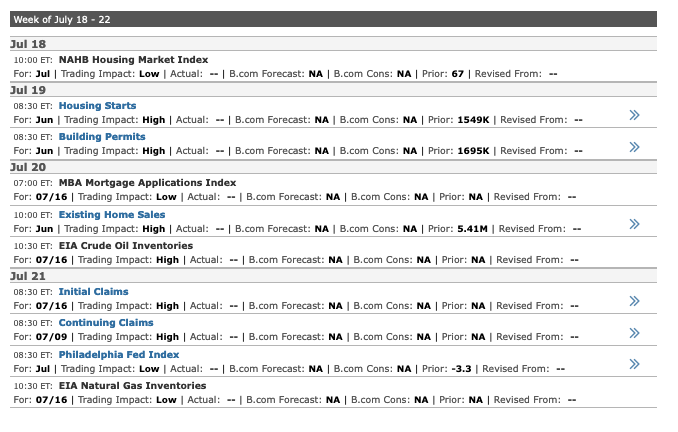

The market faces a gauntlet of tough YoY economic comps these next two weeks, starting with factory orders and consumer credit next week, both of which are likely to suggest another negative GDP print for Q2.

Consumer credit’s growth is approaching an unsustainable rate as consumers are increasingly turning to credit to make ends meet.

Consumer credit’s growth is approaching an unsustainable rate as consumers are increasingly turning to credit to make ends meet. The following week brings another CPI print as well as retail sales and consumer sentiment.

The following week brings another CPI print as well as retail sales and consumer sentiment. The week we’re expecting the market to finally bounce will center around housing starts and claims.

The week we’re expecting the market to finally bounce will center around housing starts and claims. Stay frosty.

Stay frosty.