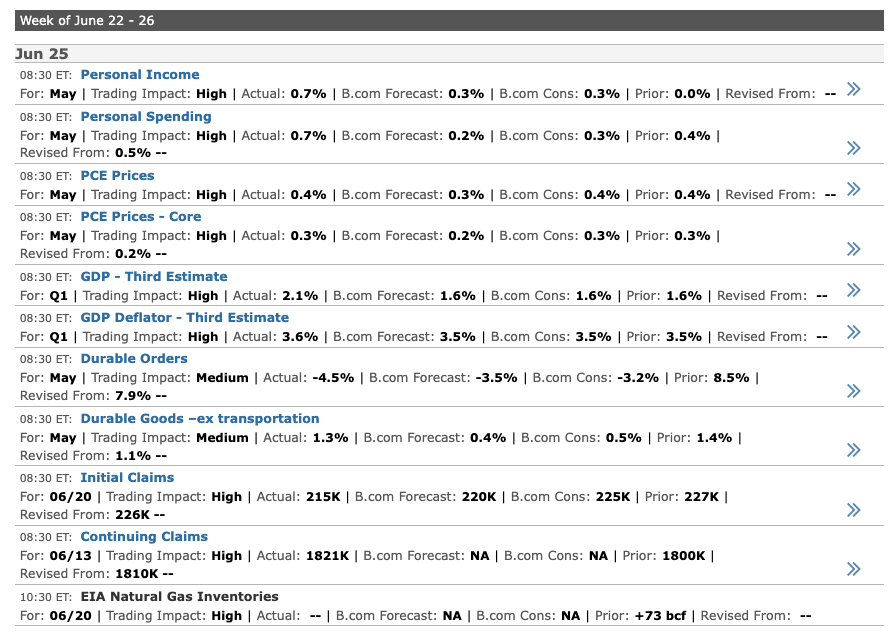

Starts for housing projects with 5 units or more plunged 41.6% to a rate of 284,000 units in May. Multi-family housing starts dipped 12.3% year-on-year, while overall housing starts dropped 15.4% ( 8.7% year-on-year.) Building permits didn’t do much better. Multi-family housing projects fell 3.5%. last month while overall building permits slipped 0.7%.

High interest rates and materials costs have made building housing a very difficult prospect, indeed. A significant segment of the economy, it increases the risk of an overall slowdown in the economy.

But, AI! And SpaceX! Well, SpaceX anyway. AI is looking less spiffy in the wake of the administration

throttling Anthropic. And, against that backdrop, the new and improved (if you’re a dove) Fed will issue its first appraisal of the economy tomorrow. While few are expecting a change in rates, we’re all anxious to hear their thinking on the state of the economy.

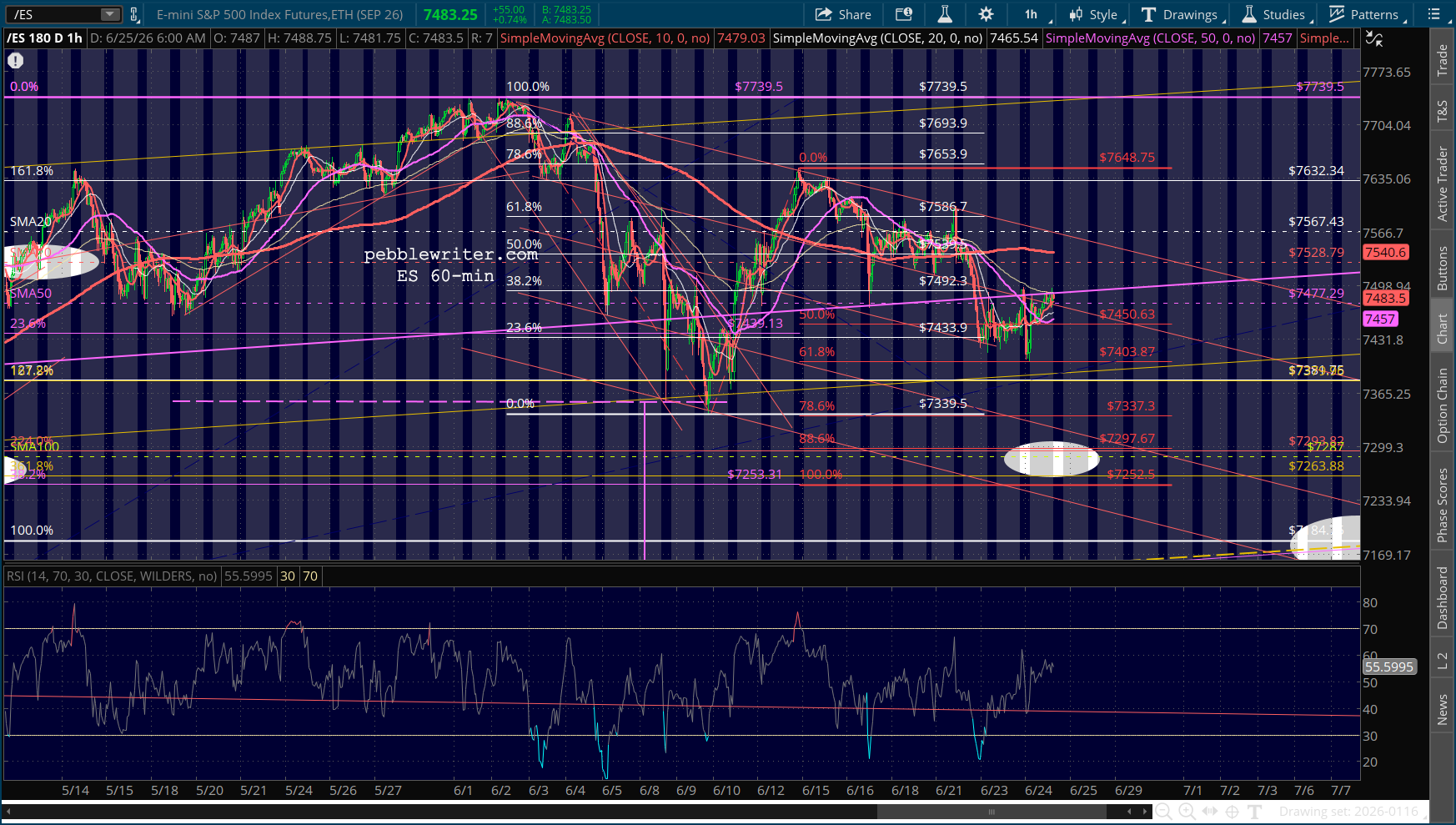

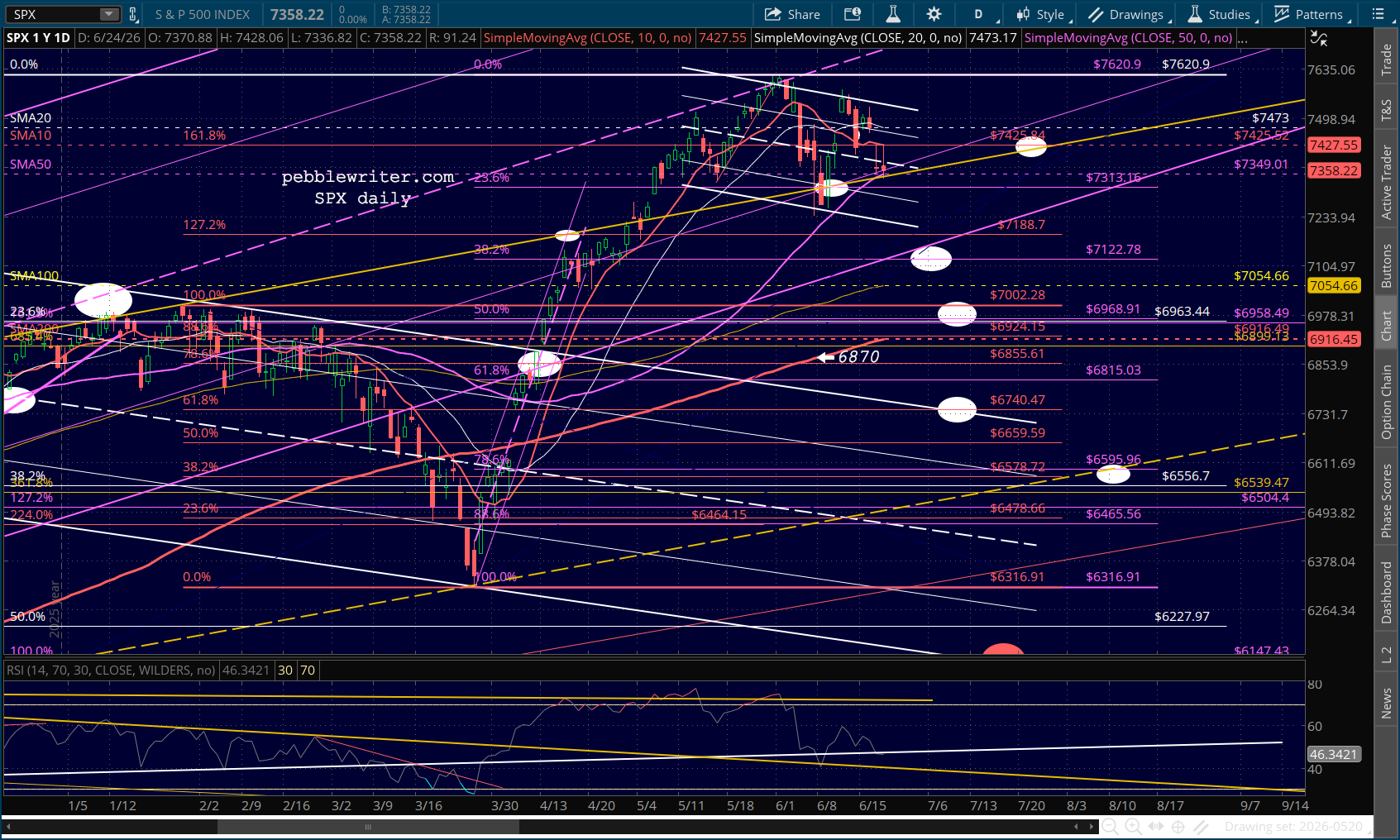

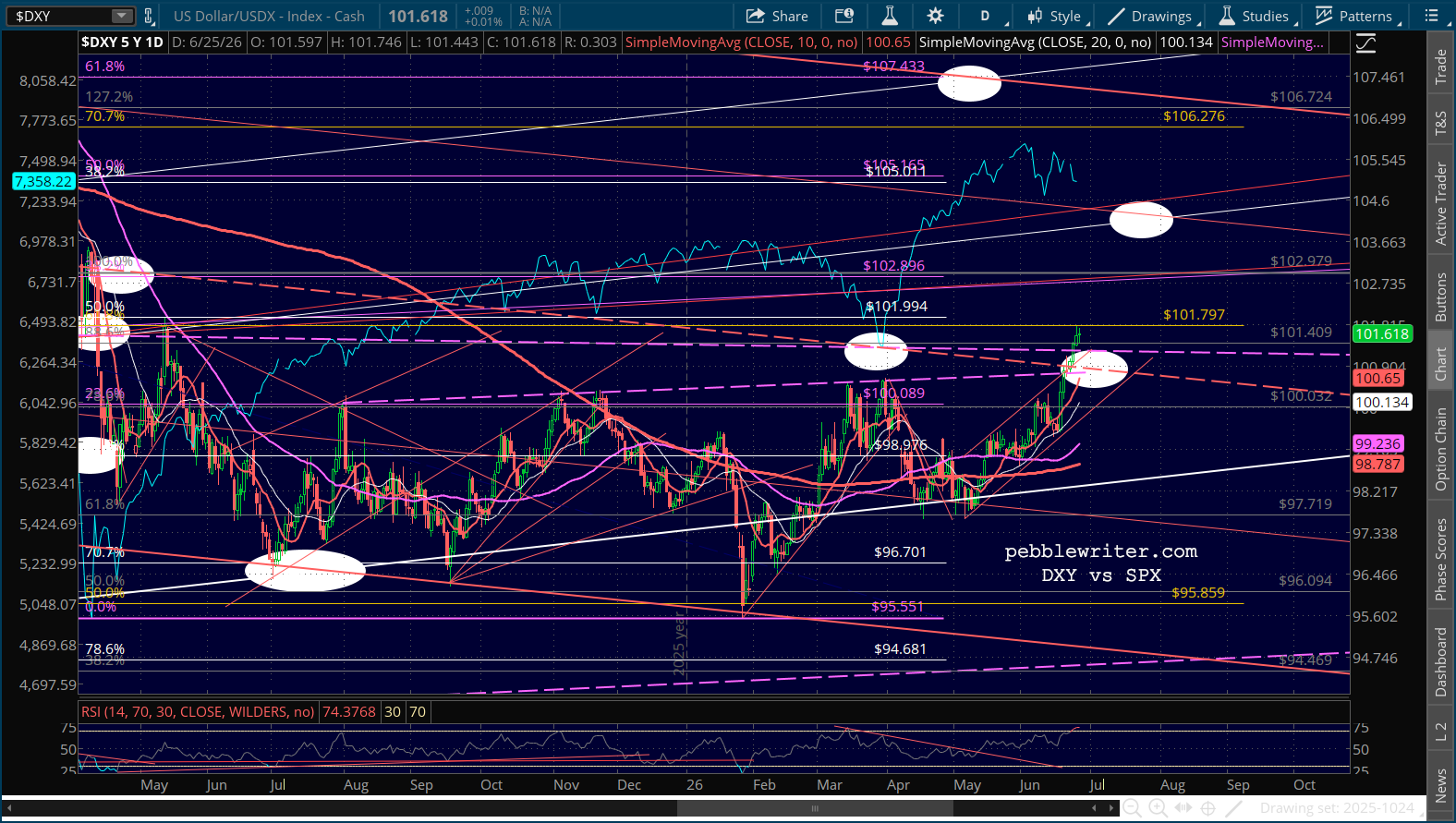

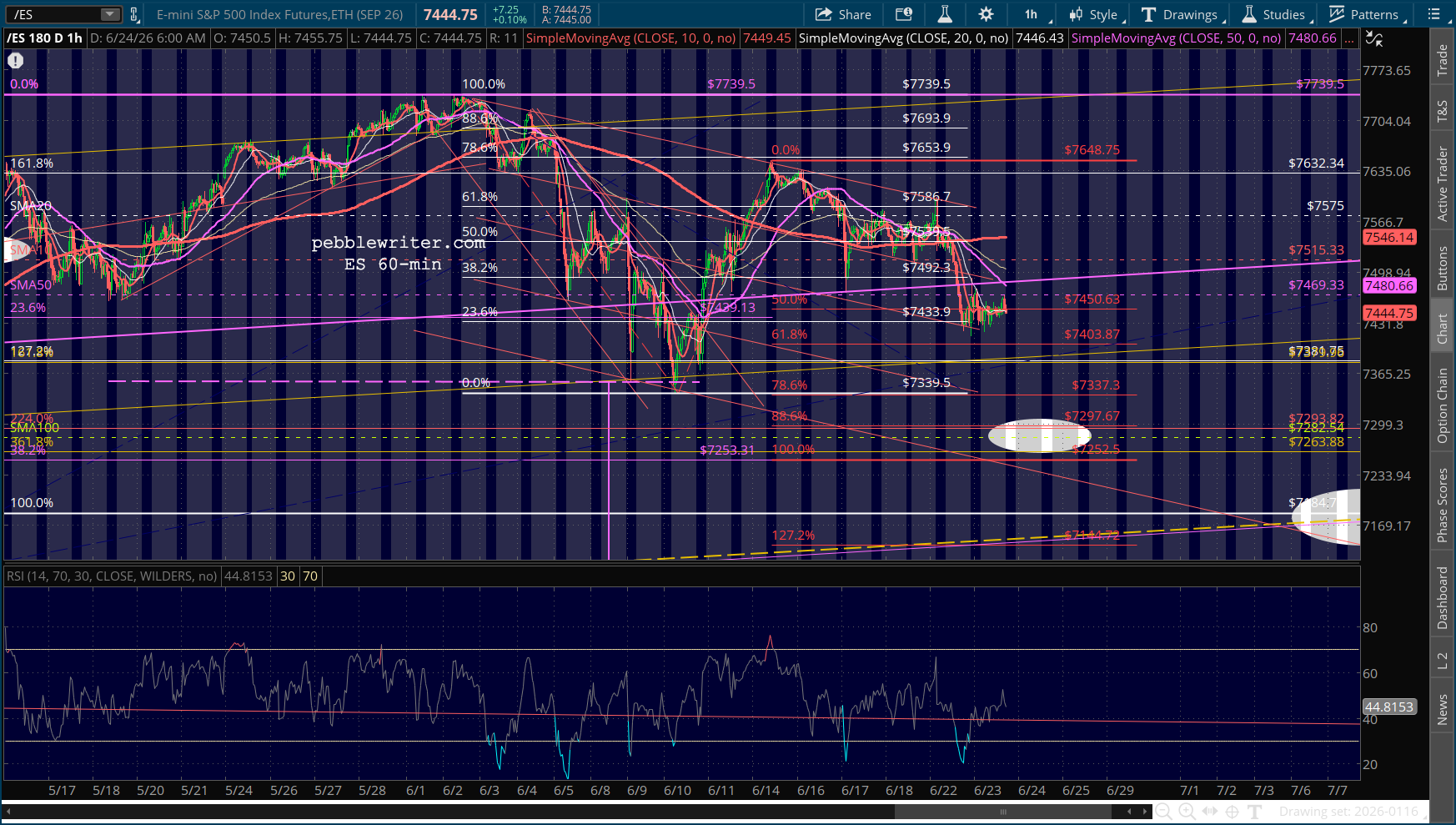

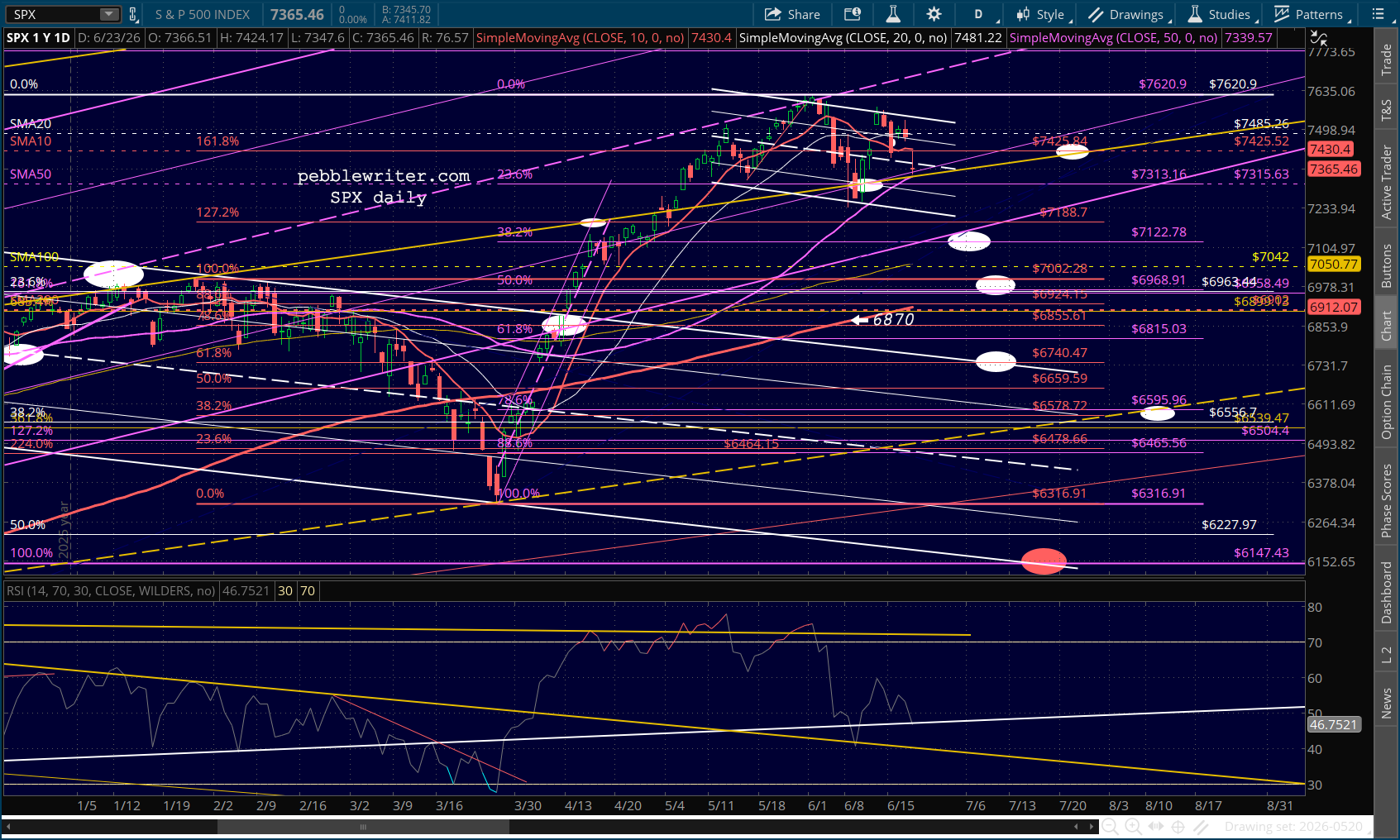

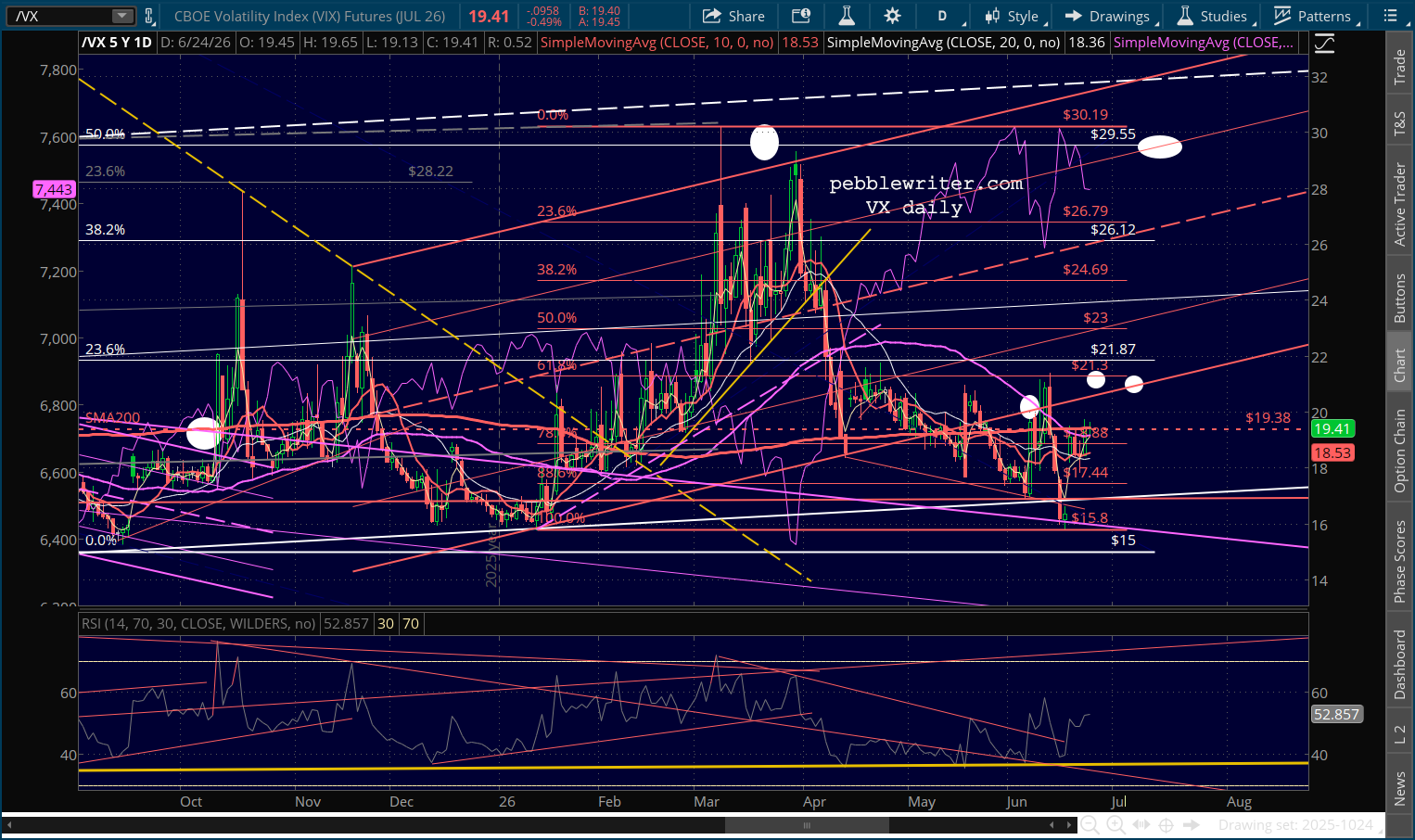

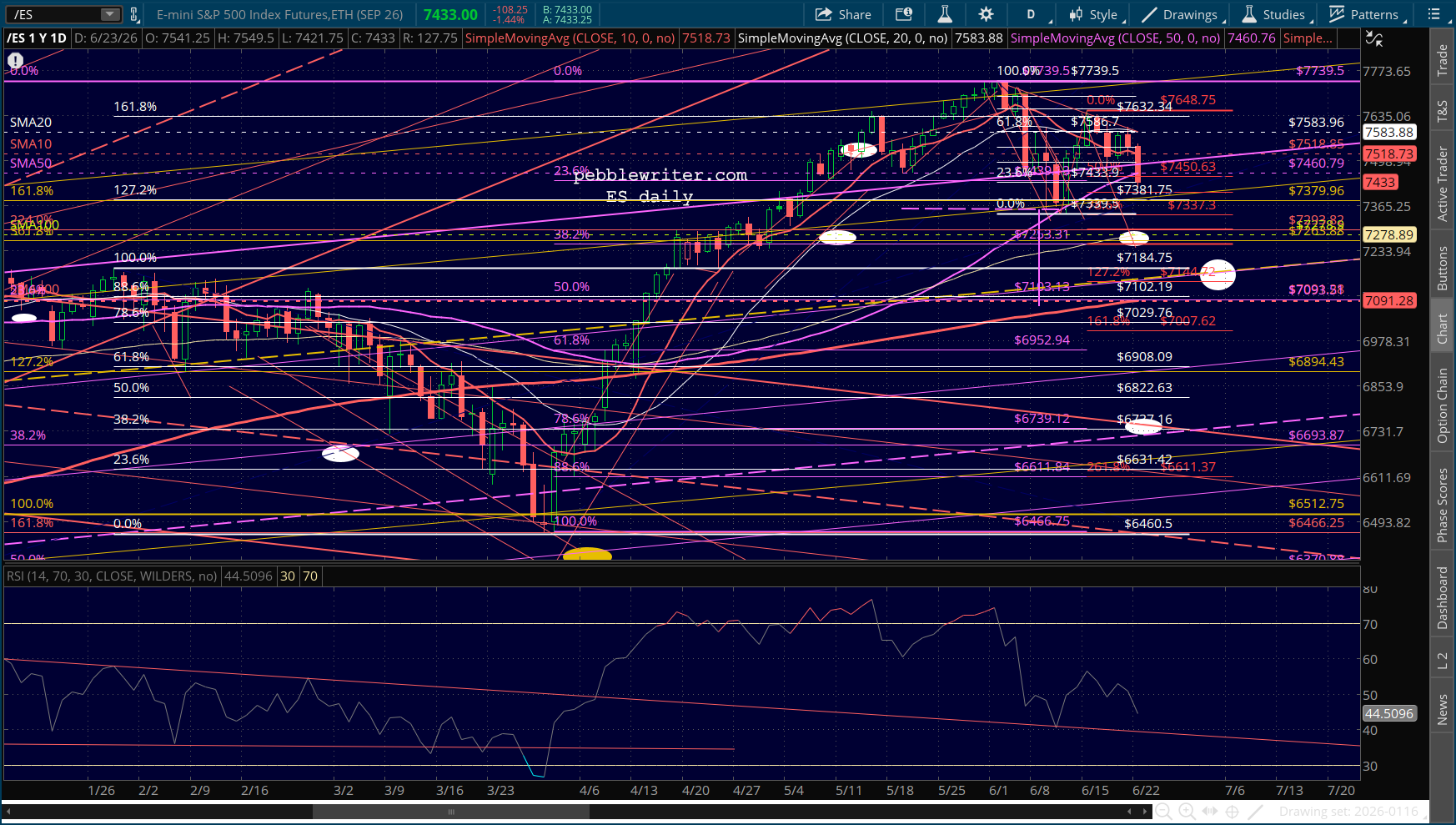

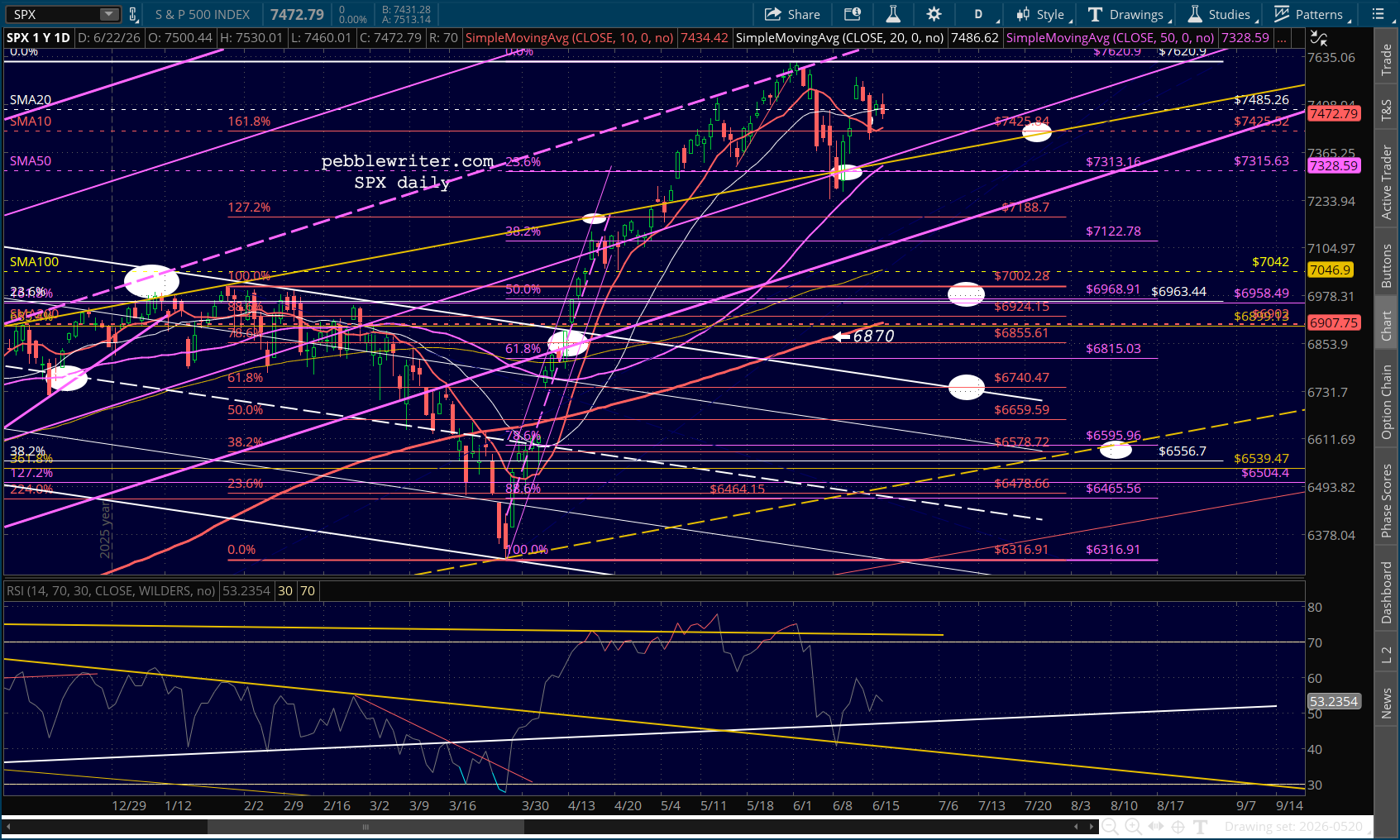

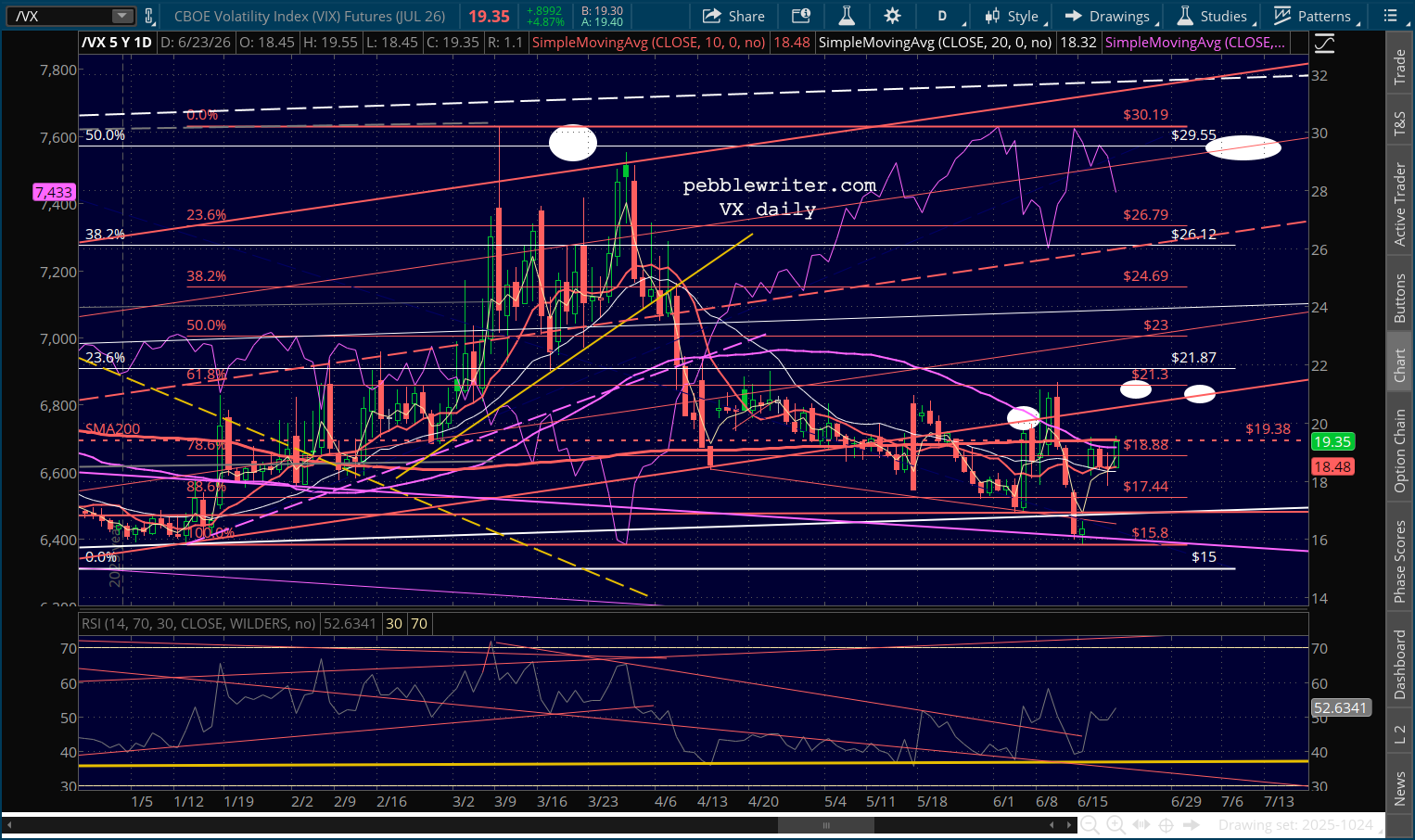

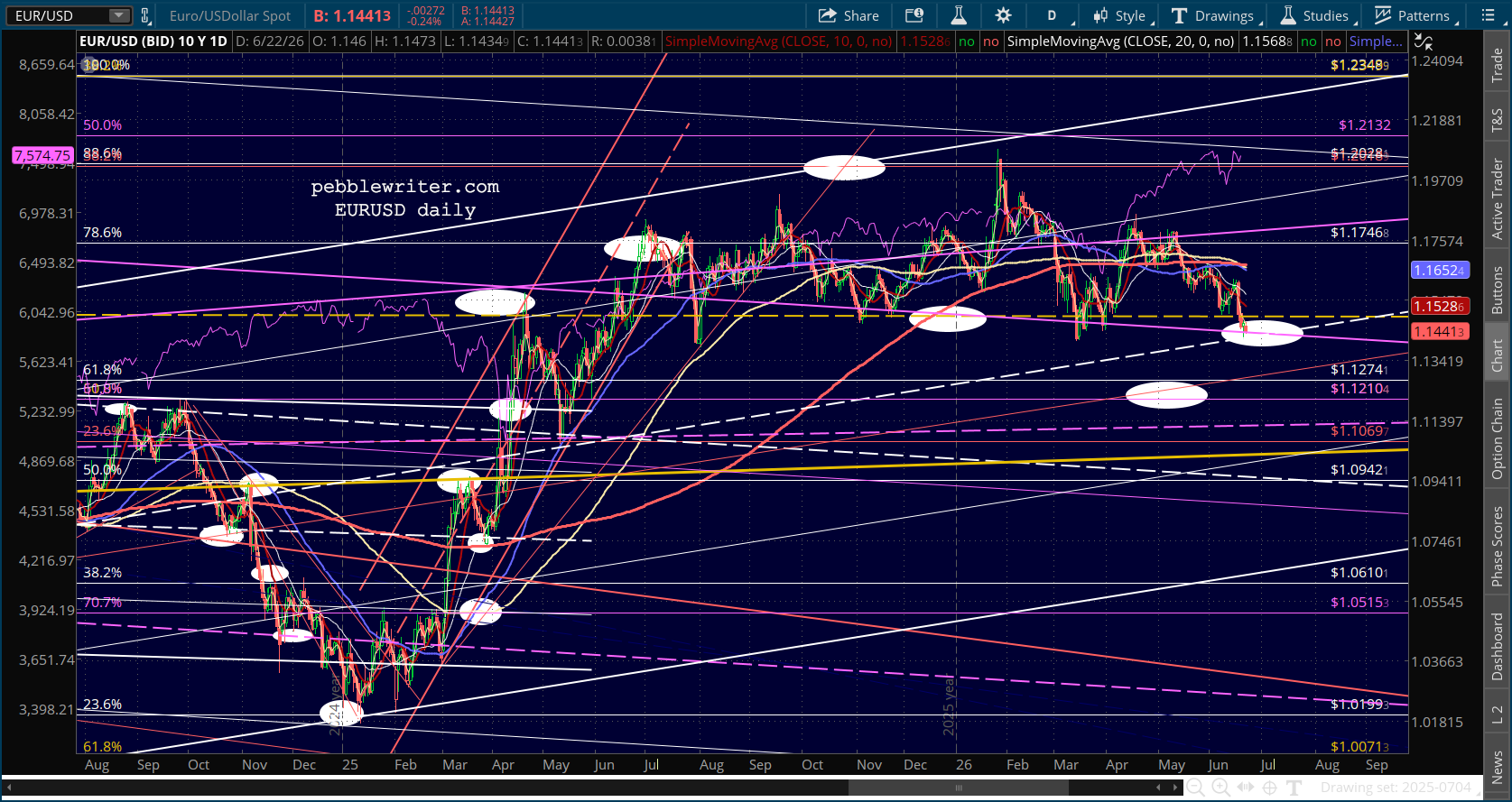

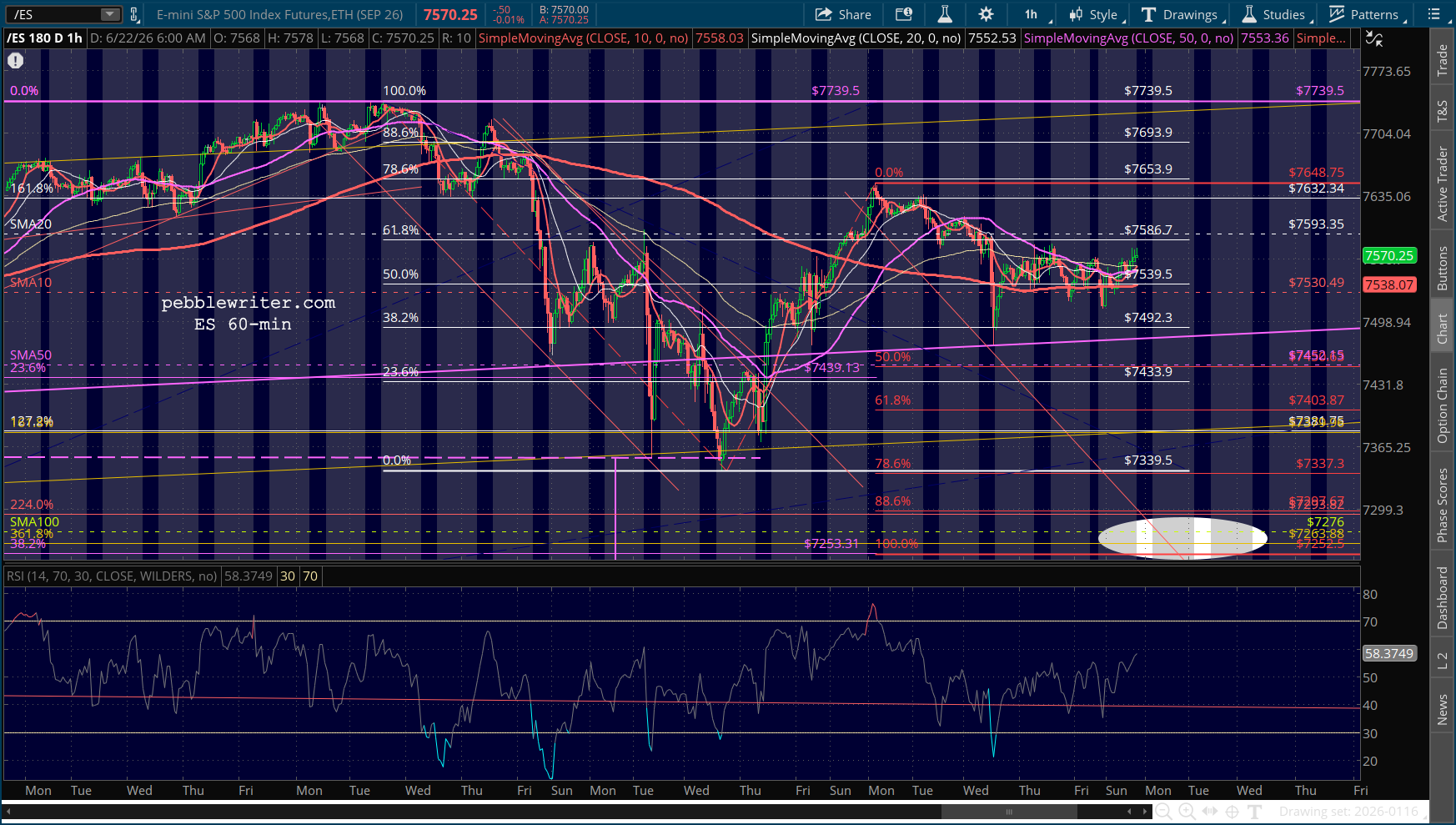

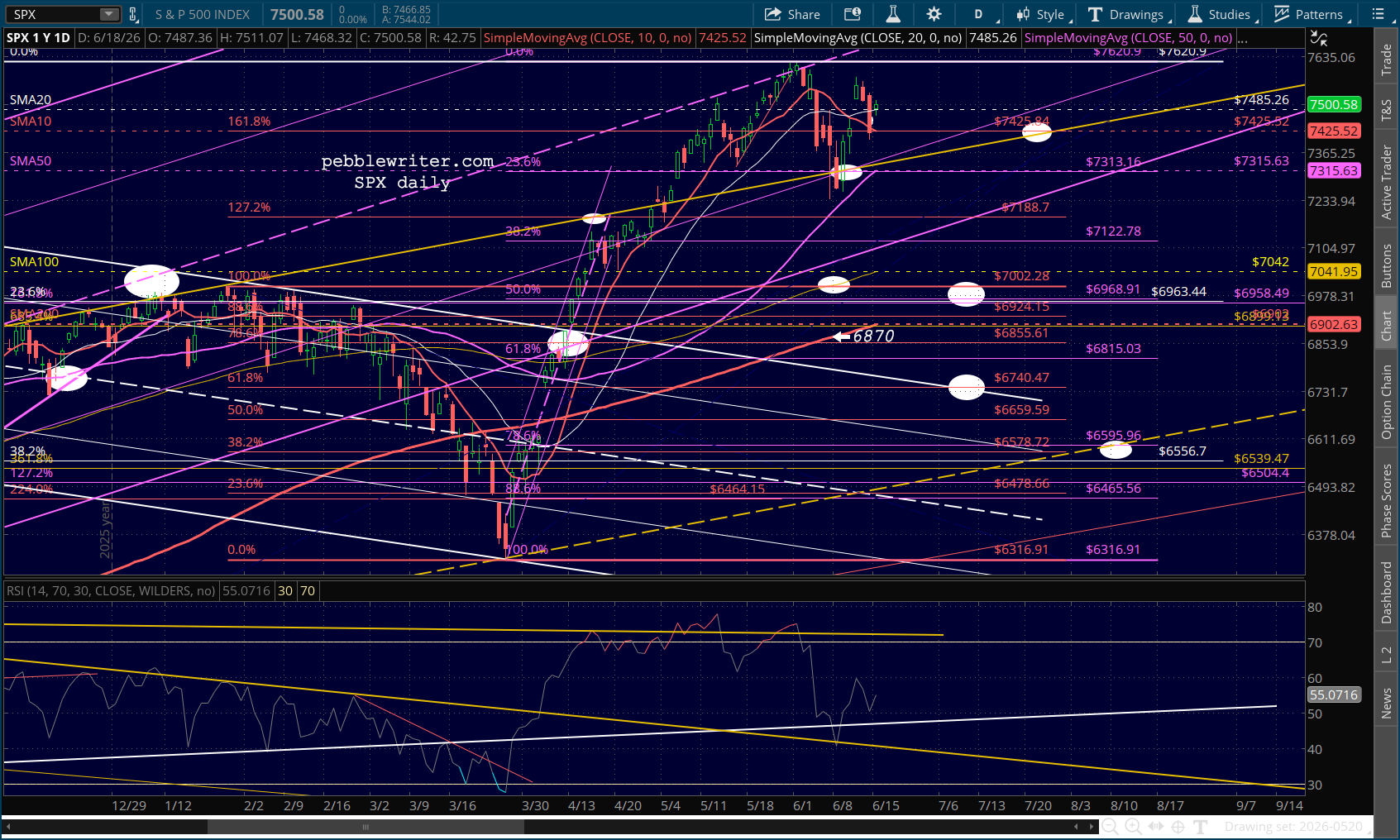

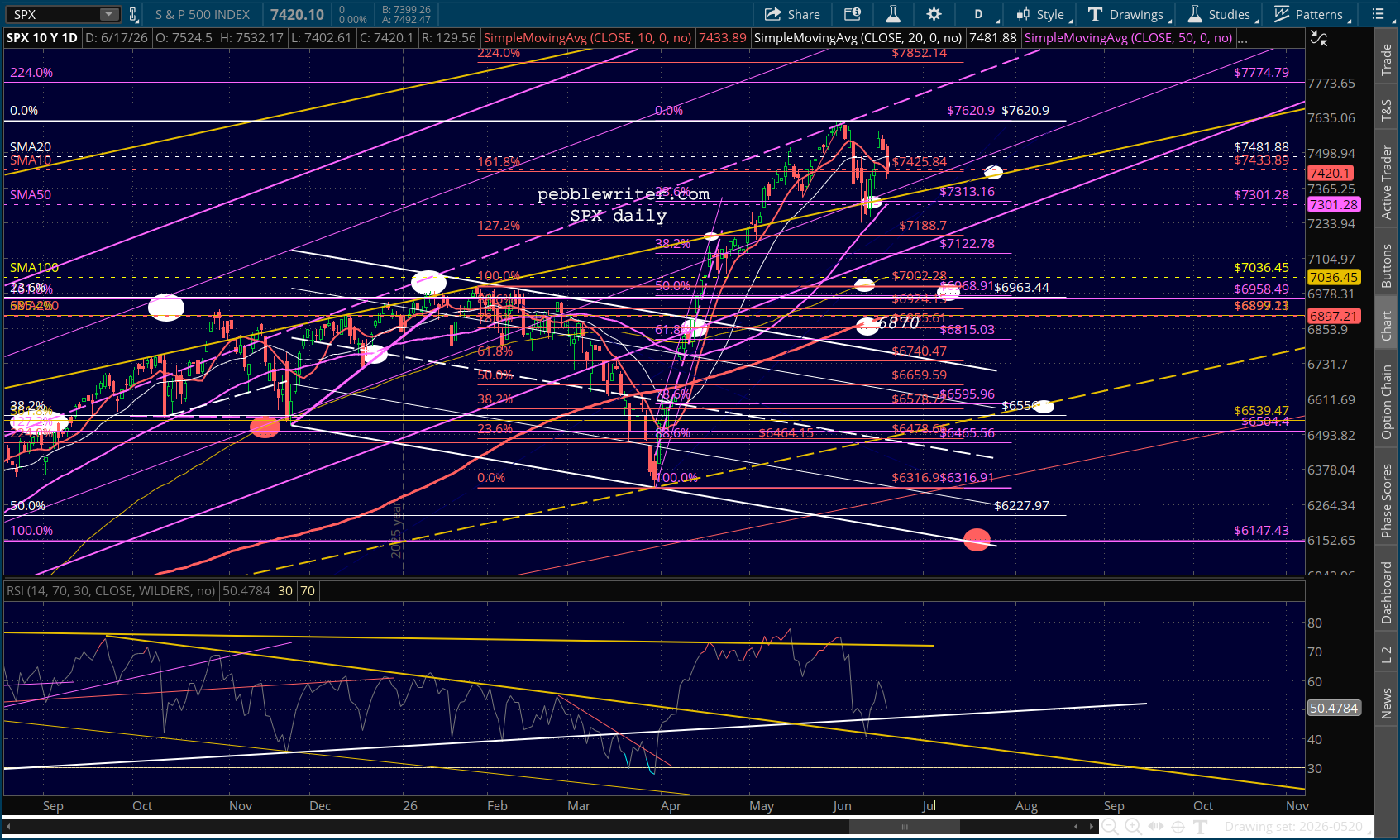

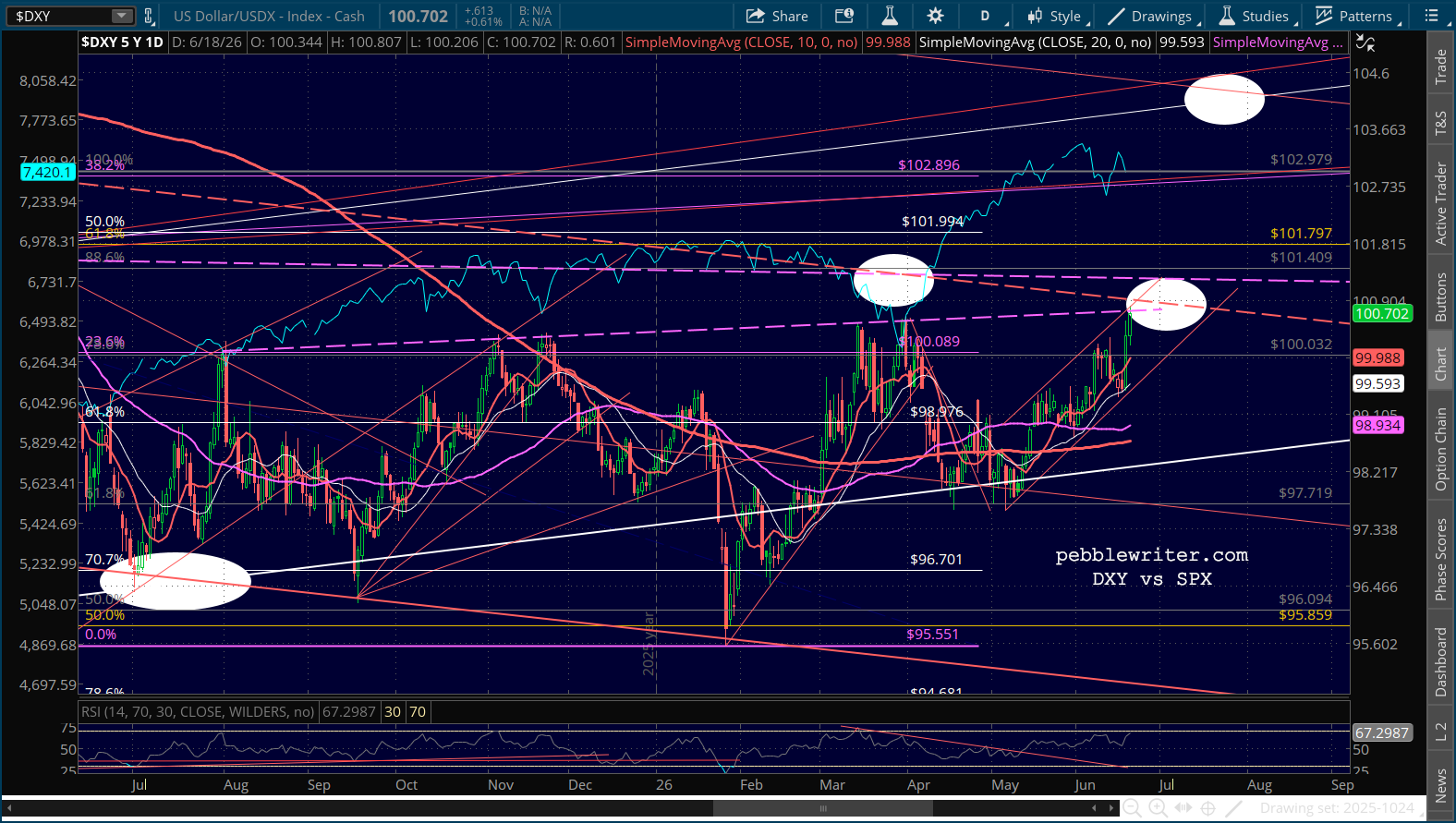

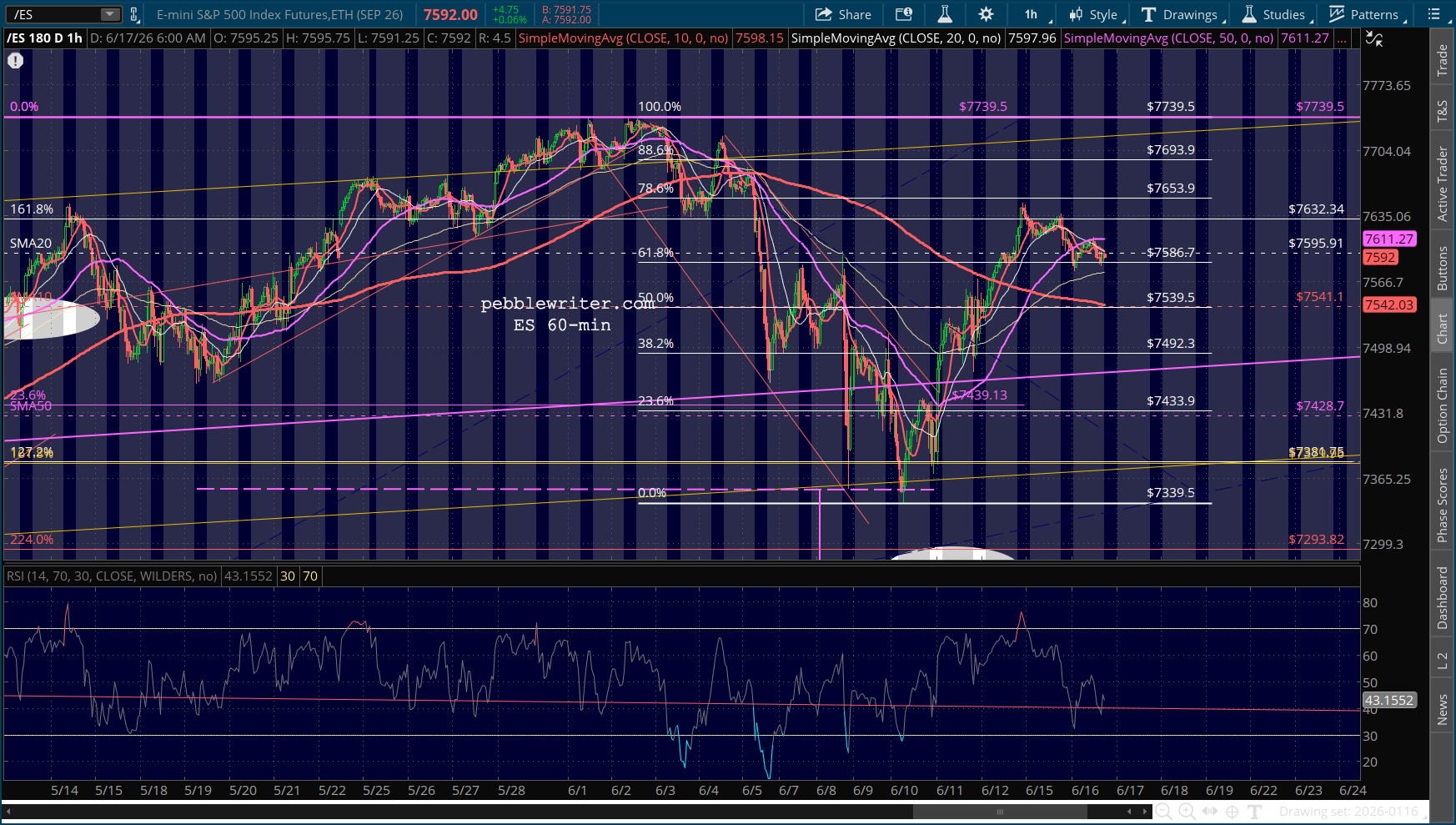

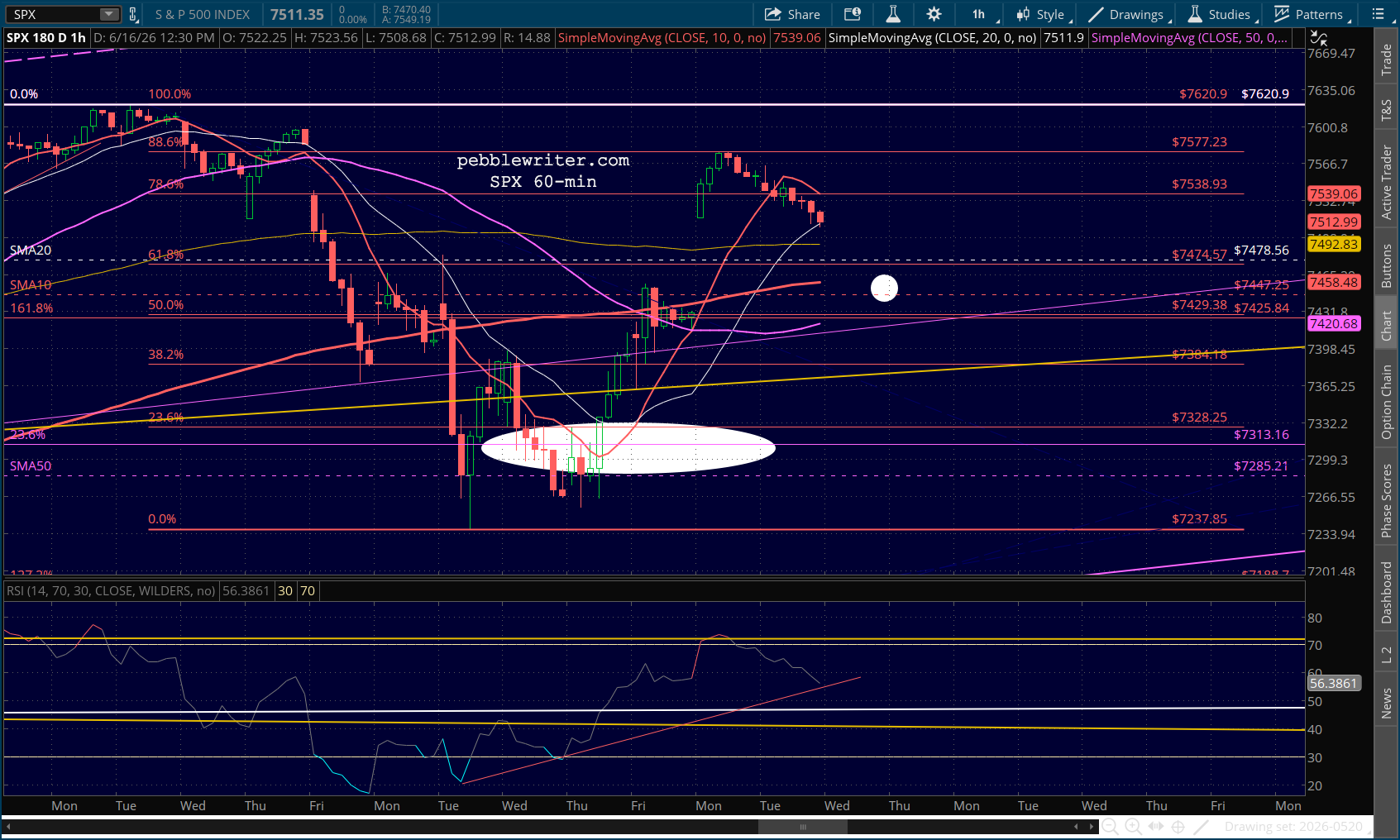

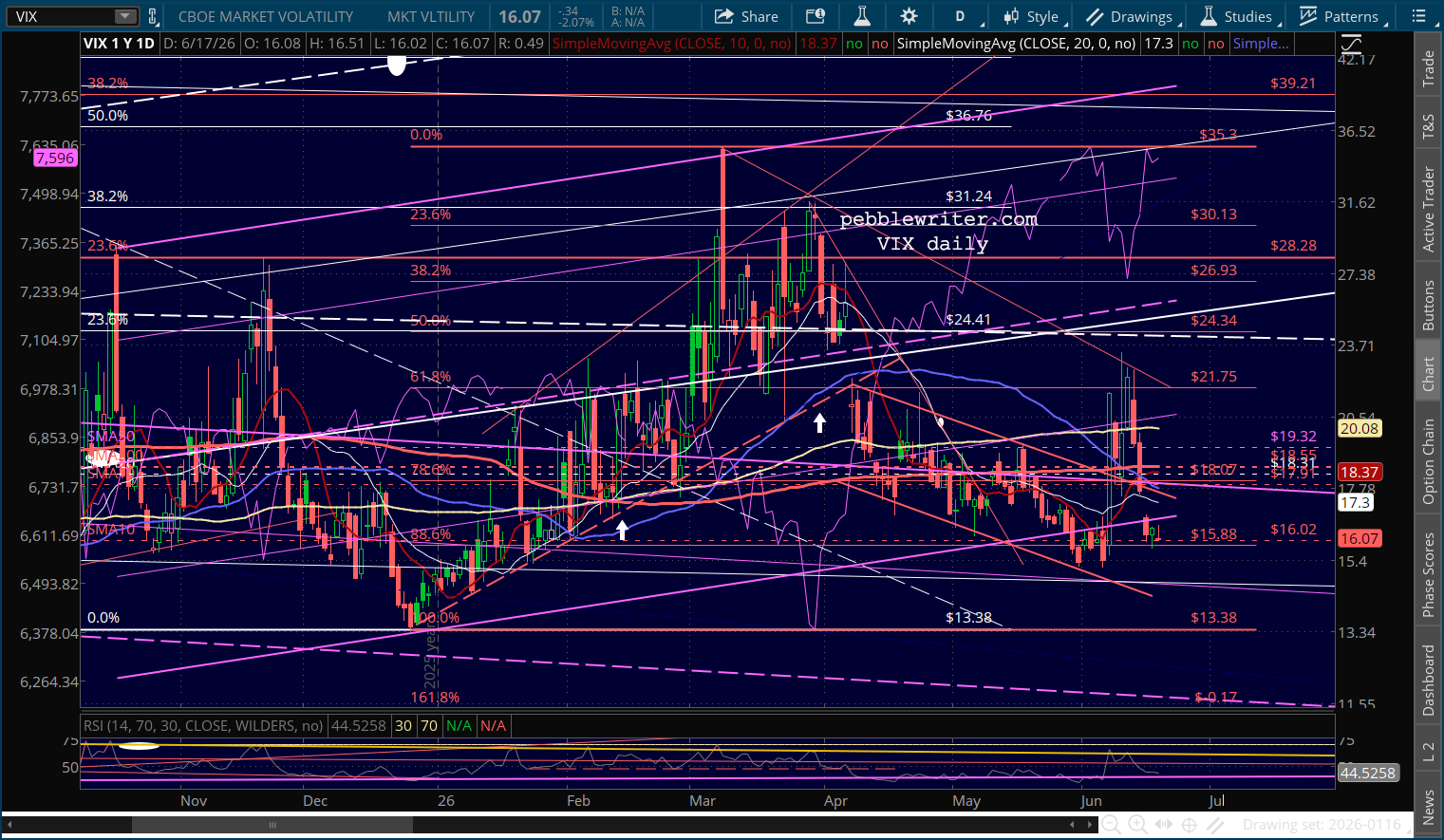

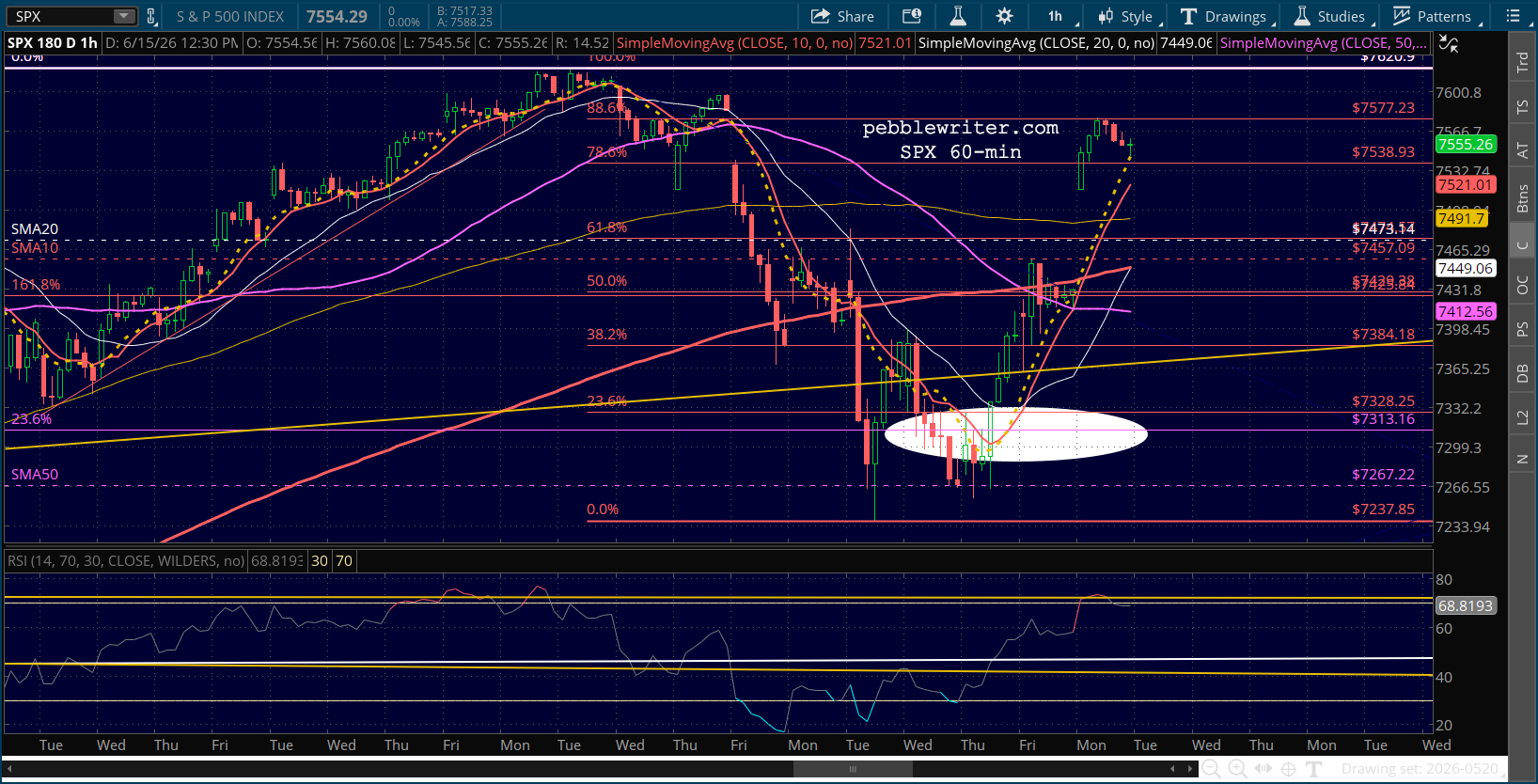

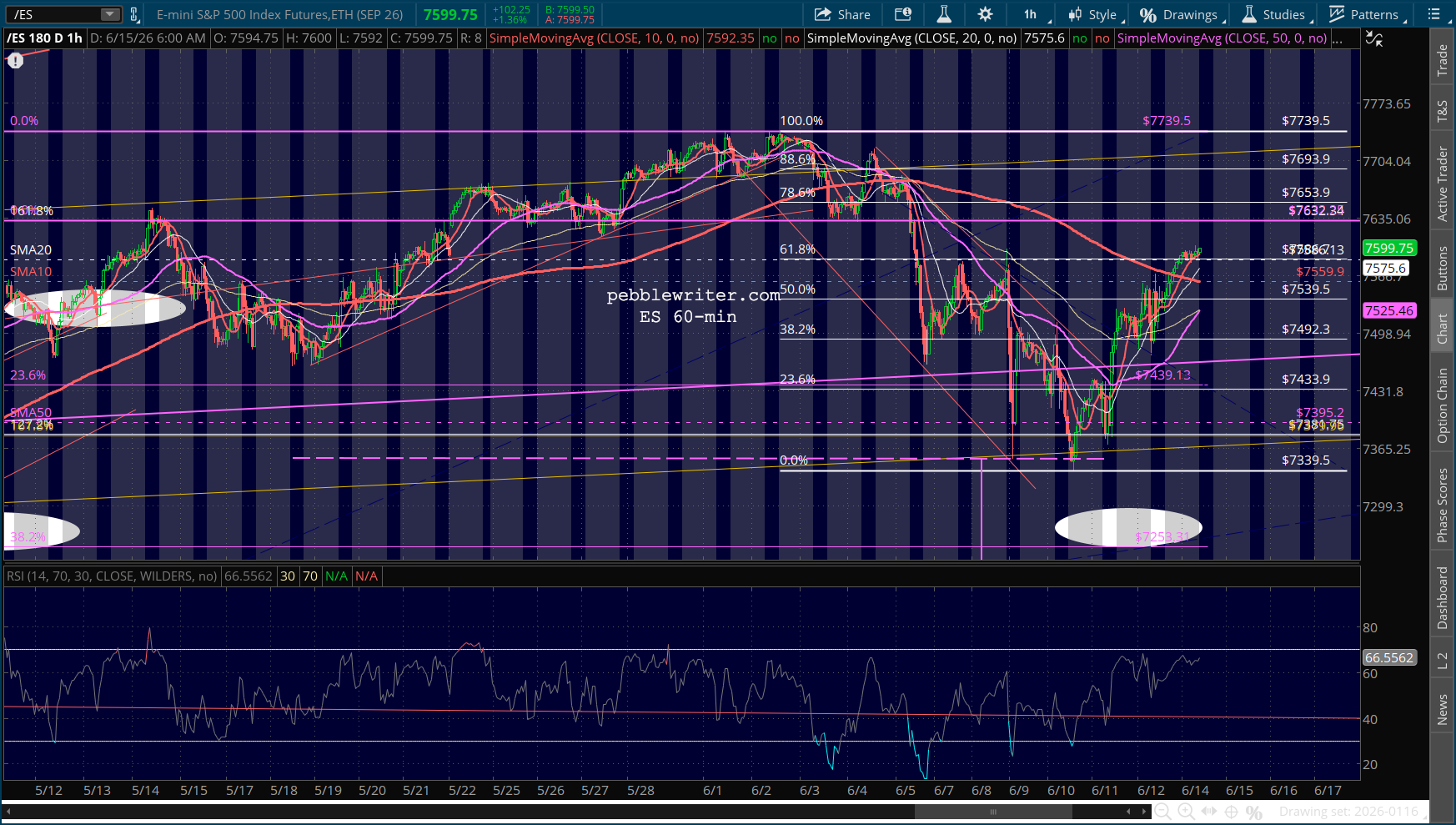

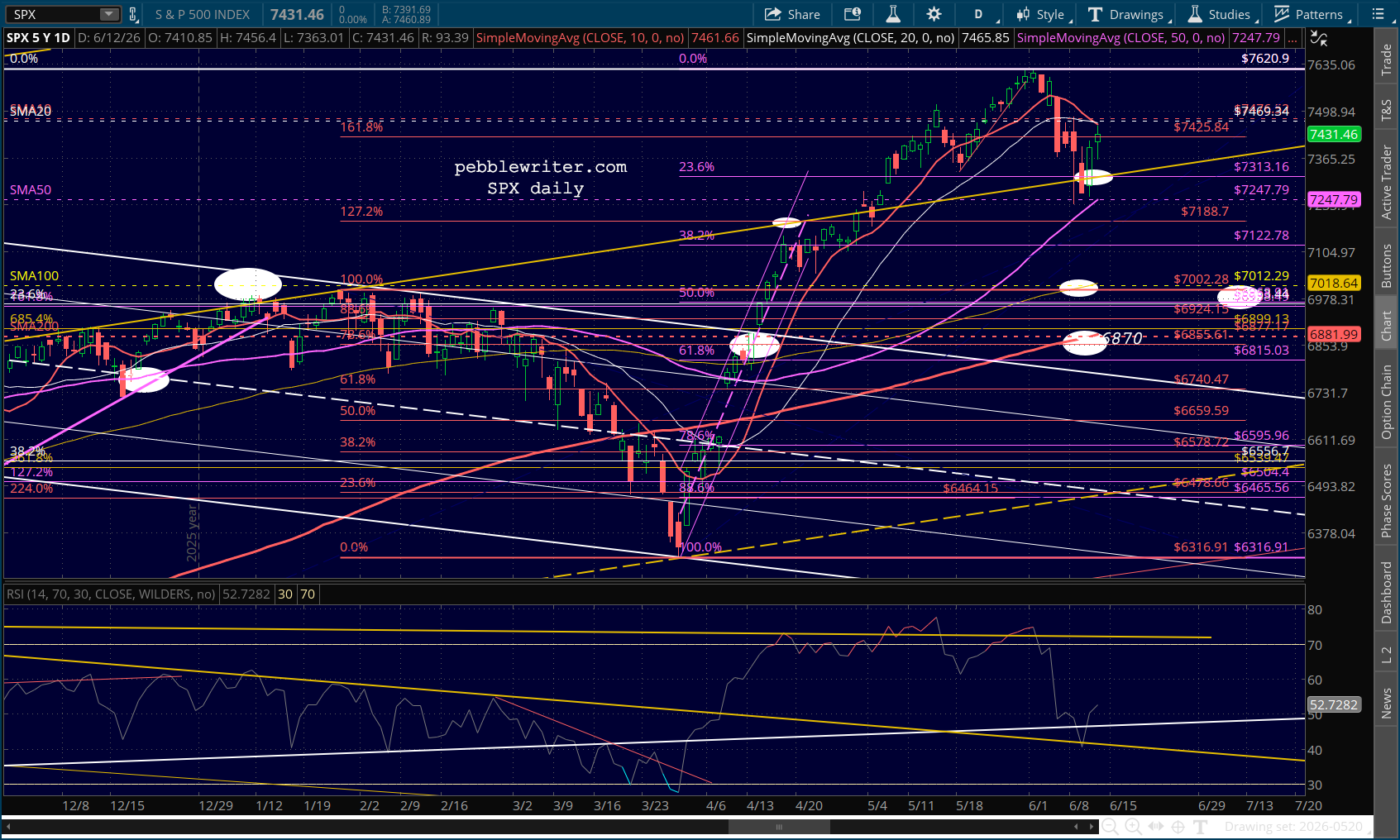

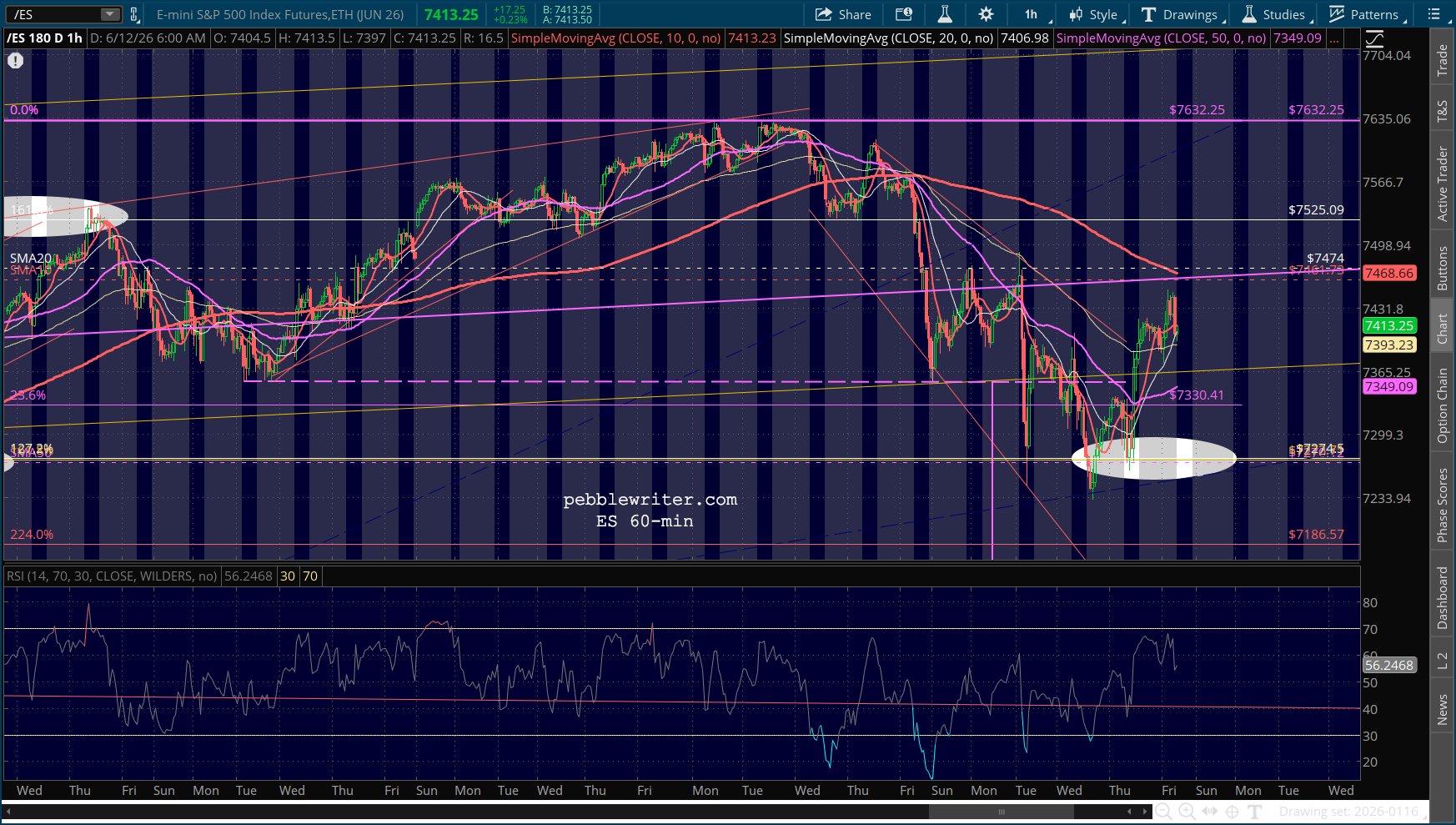

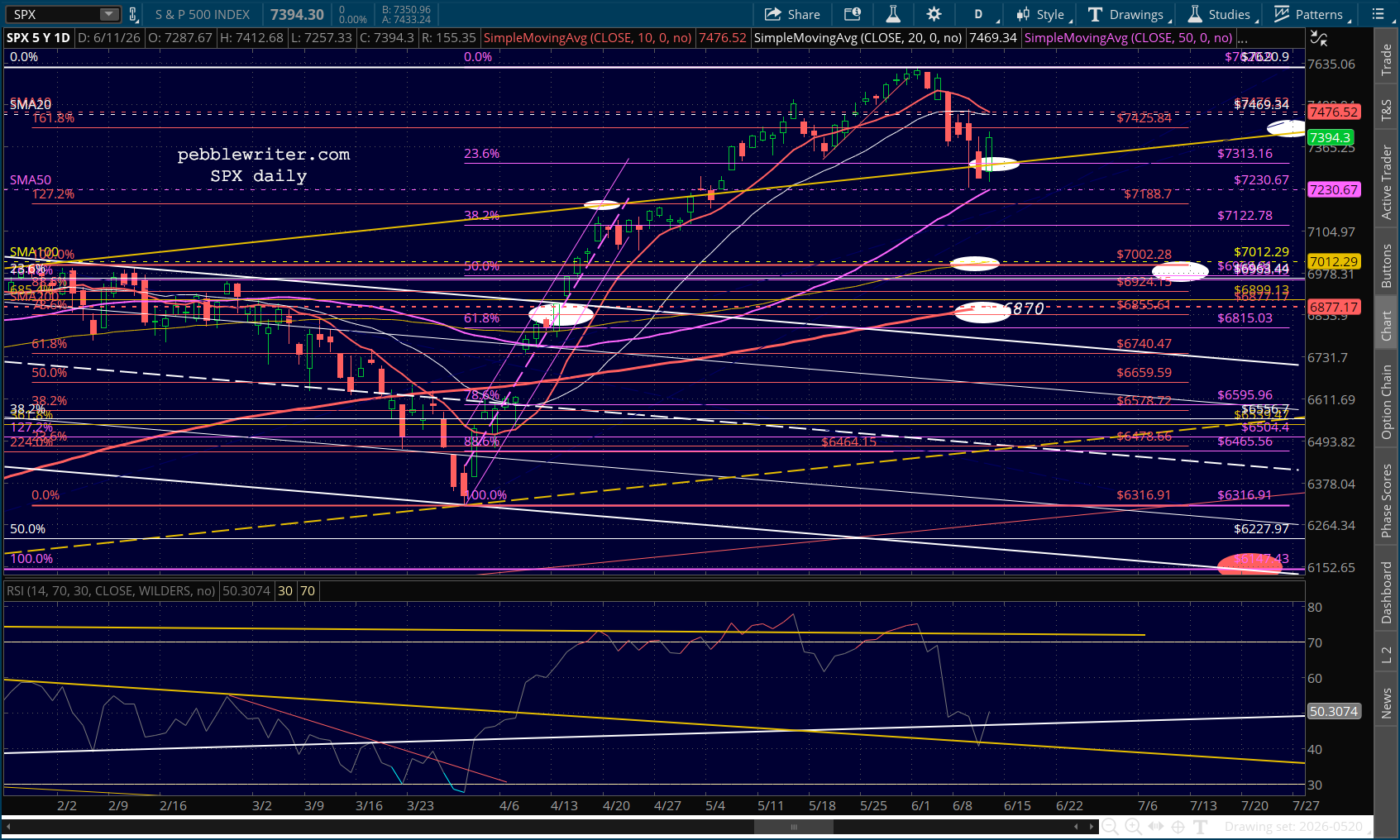

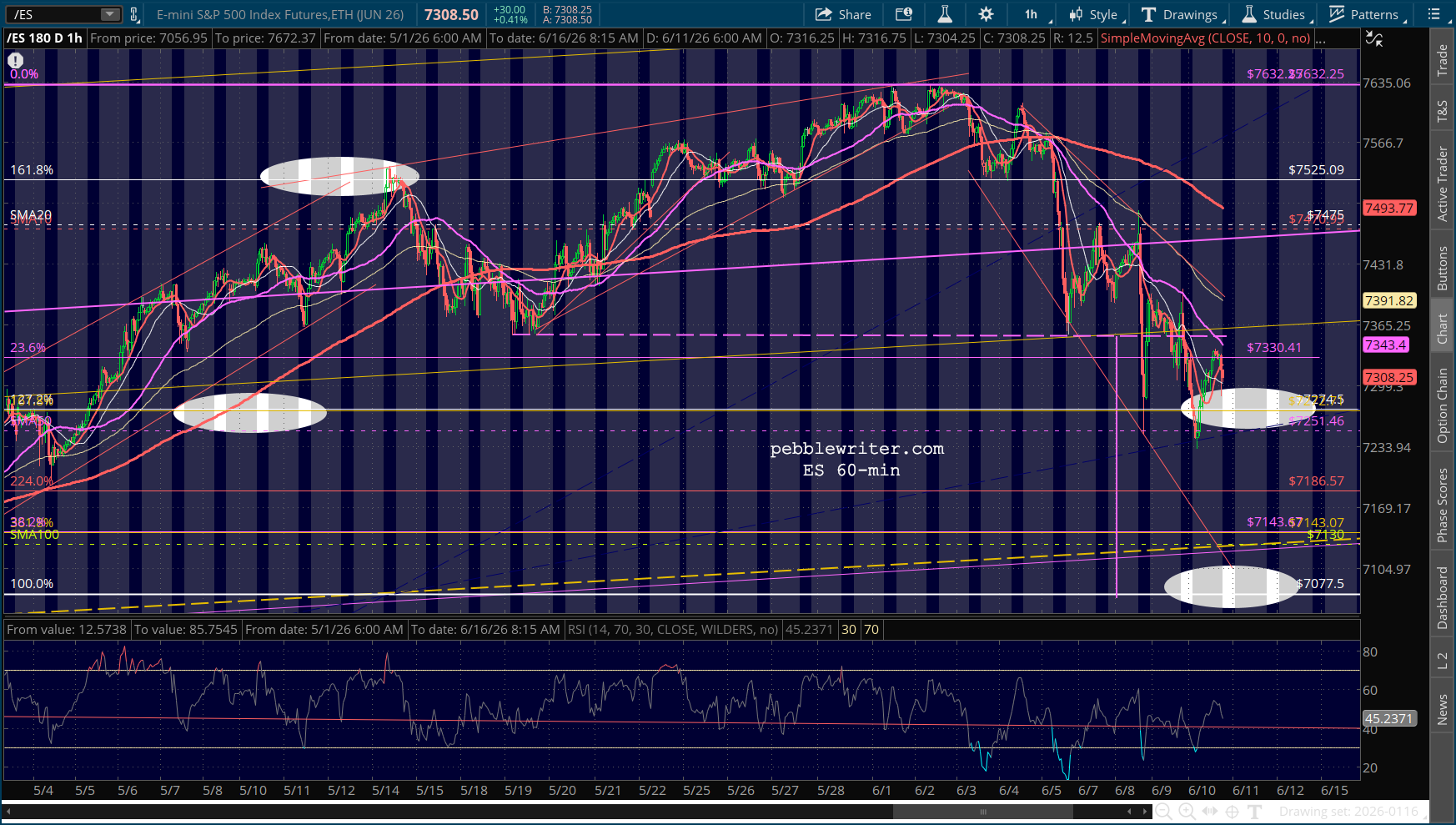

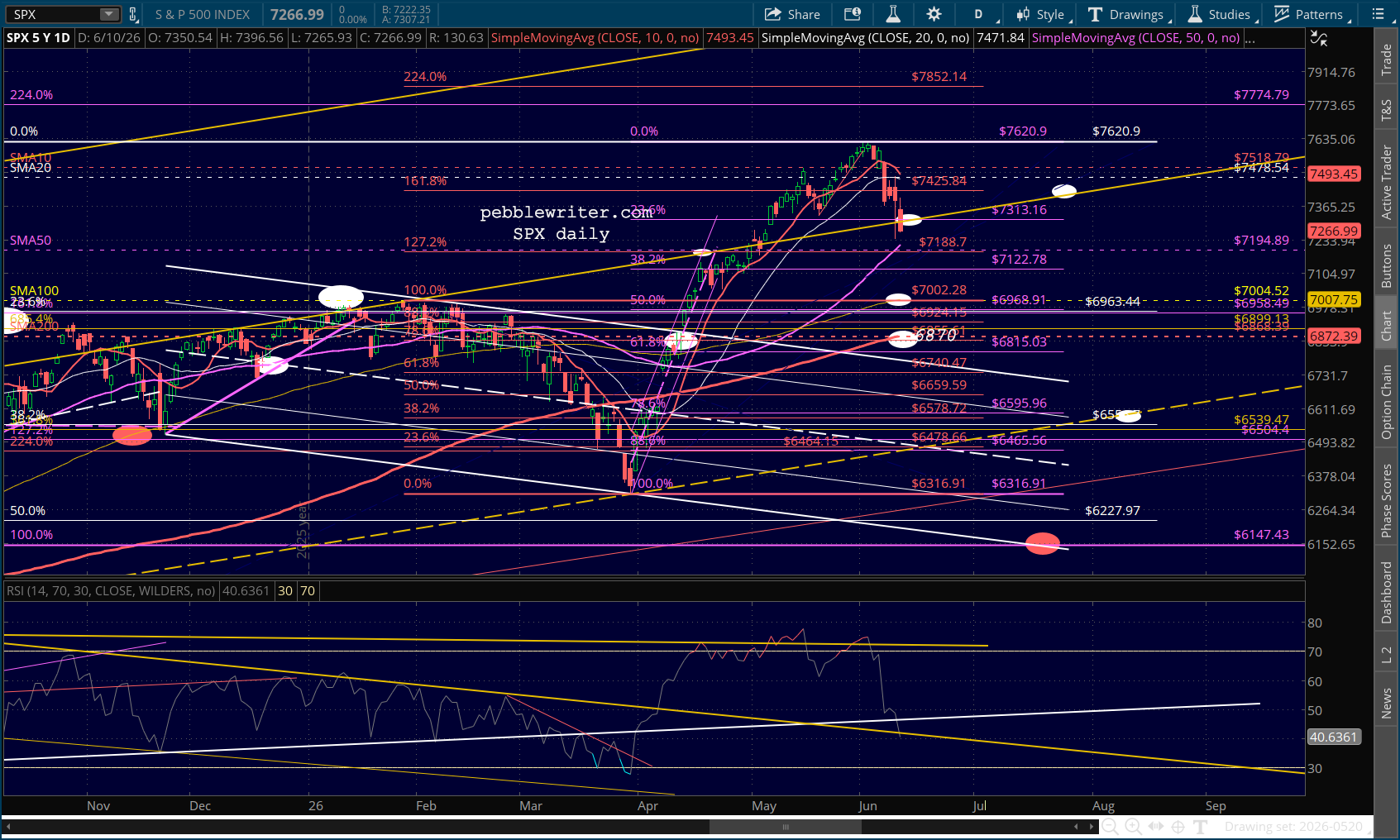

Yesterday’s gap higher put SPX right at the .886 Fib, where it’s likely to run out of steam unless the Fed gives the all-clear.

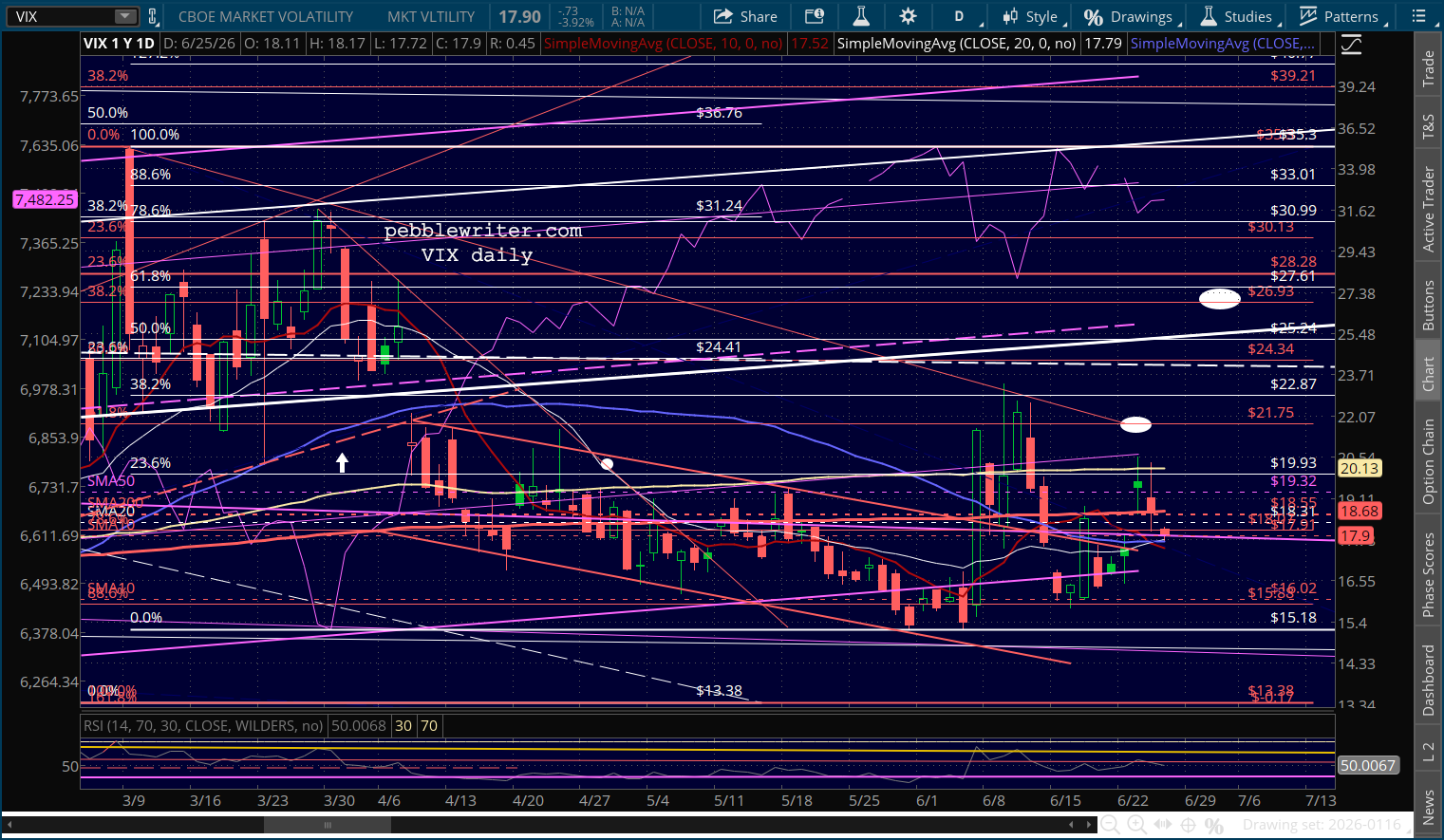

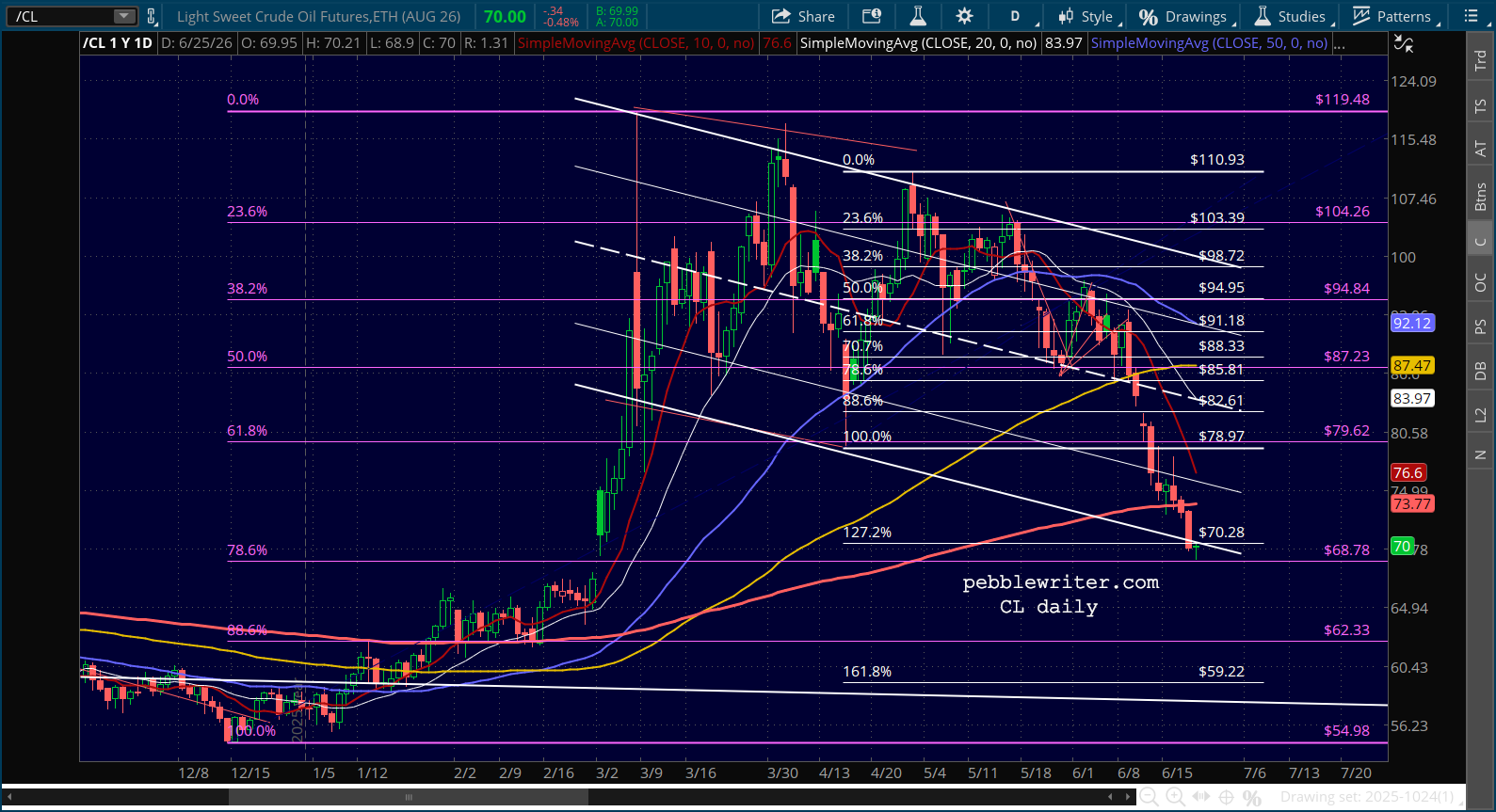

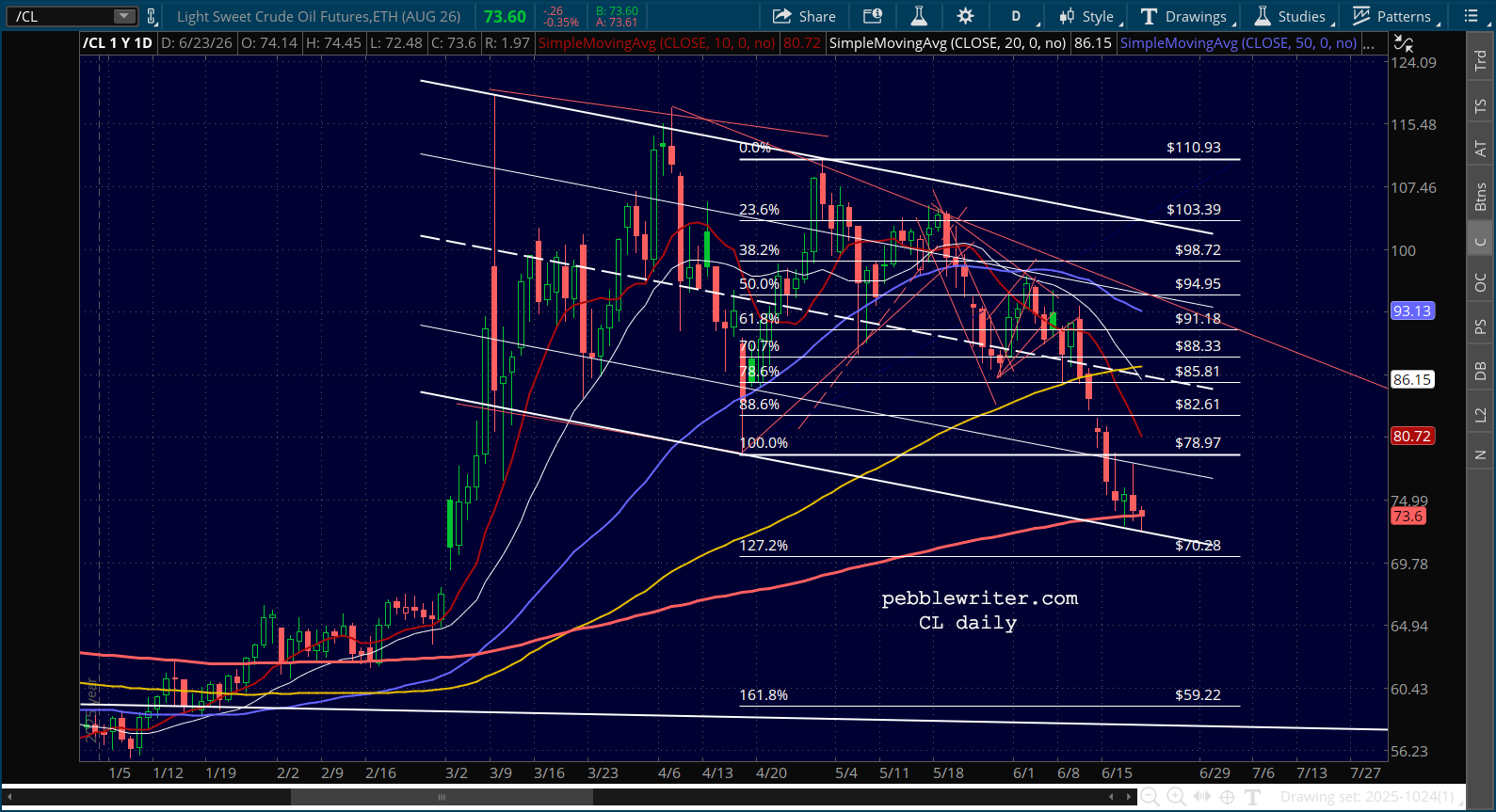

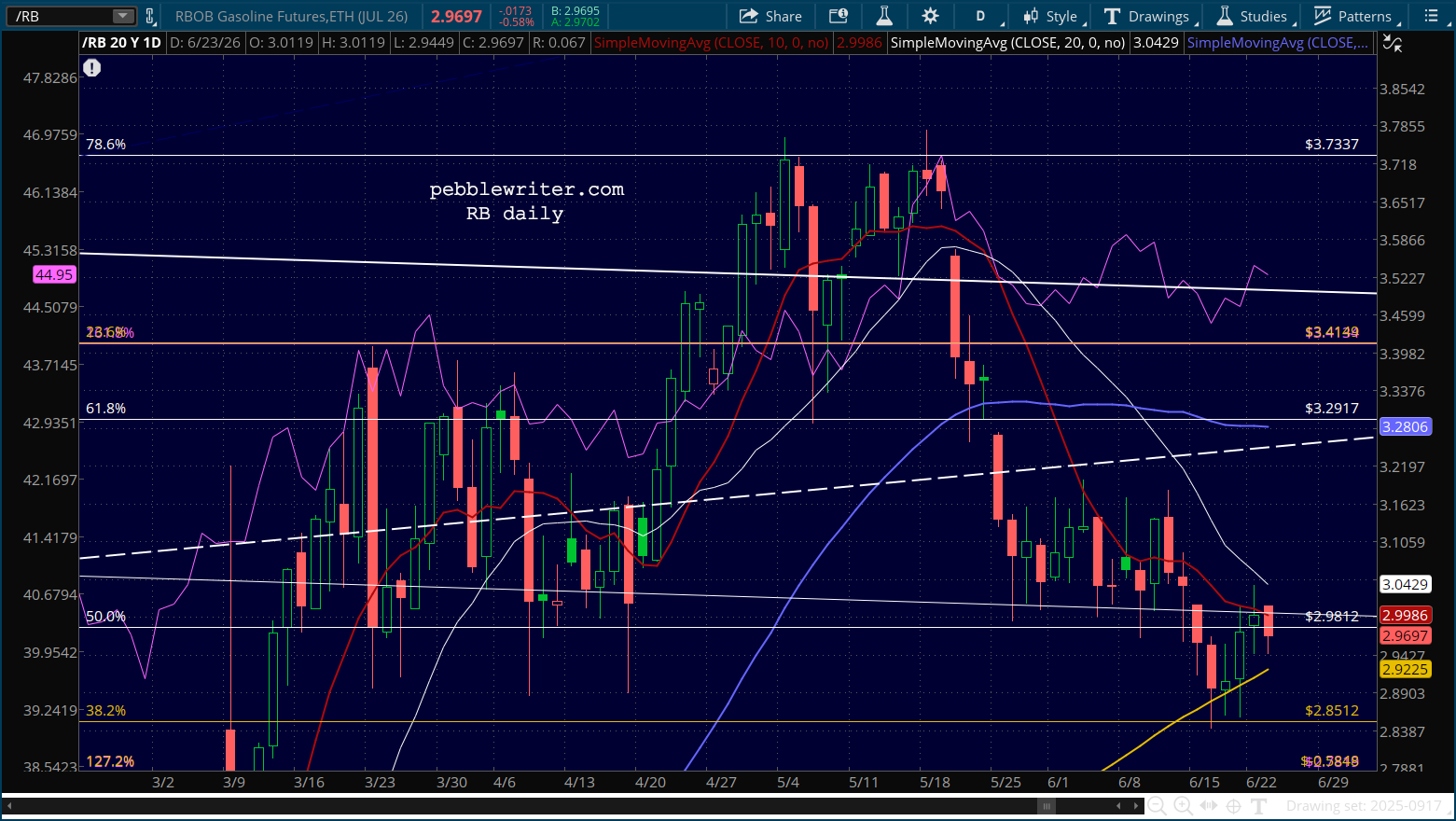

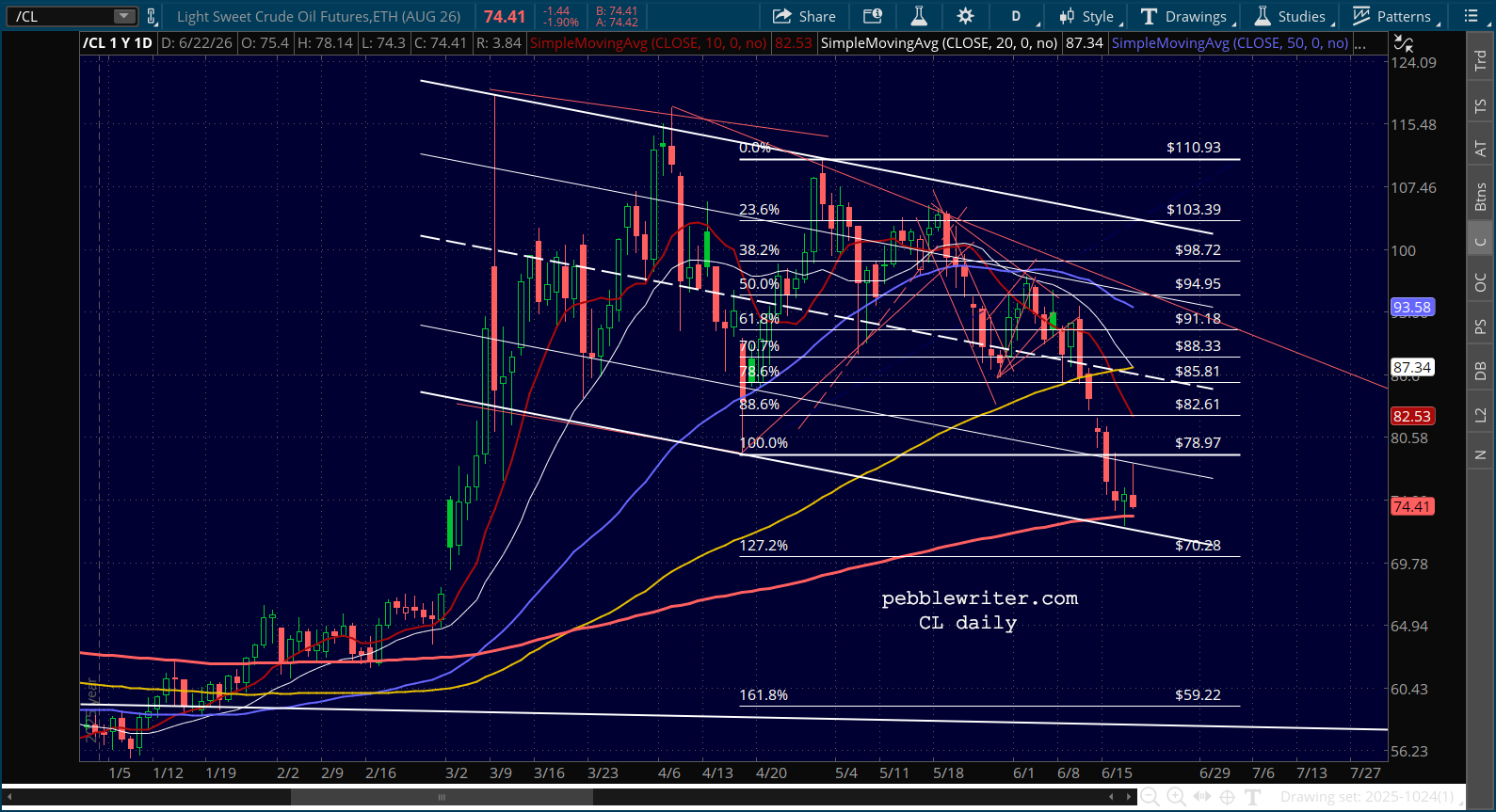

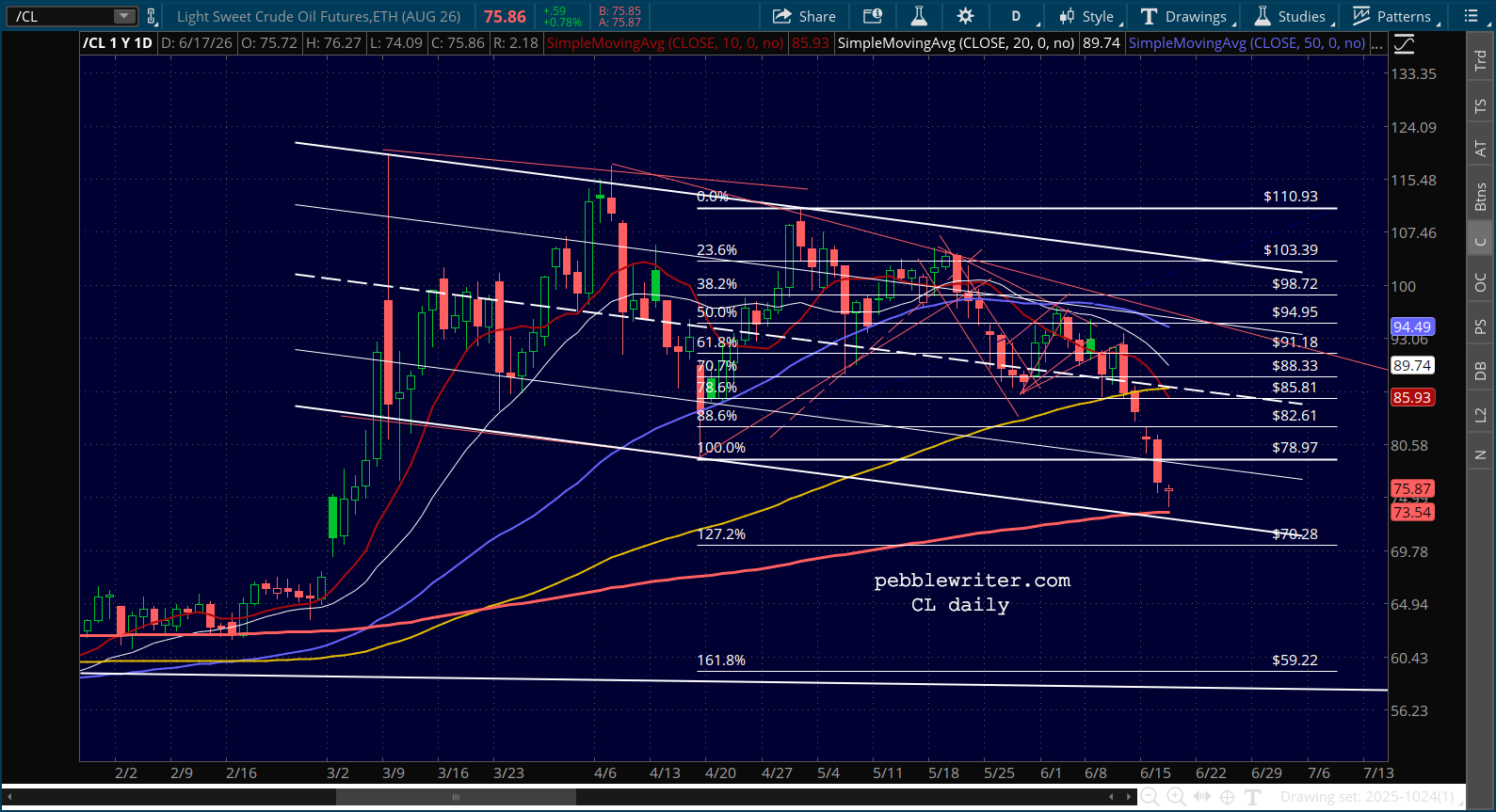

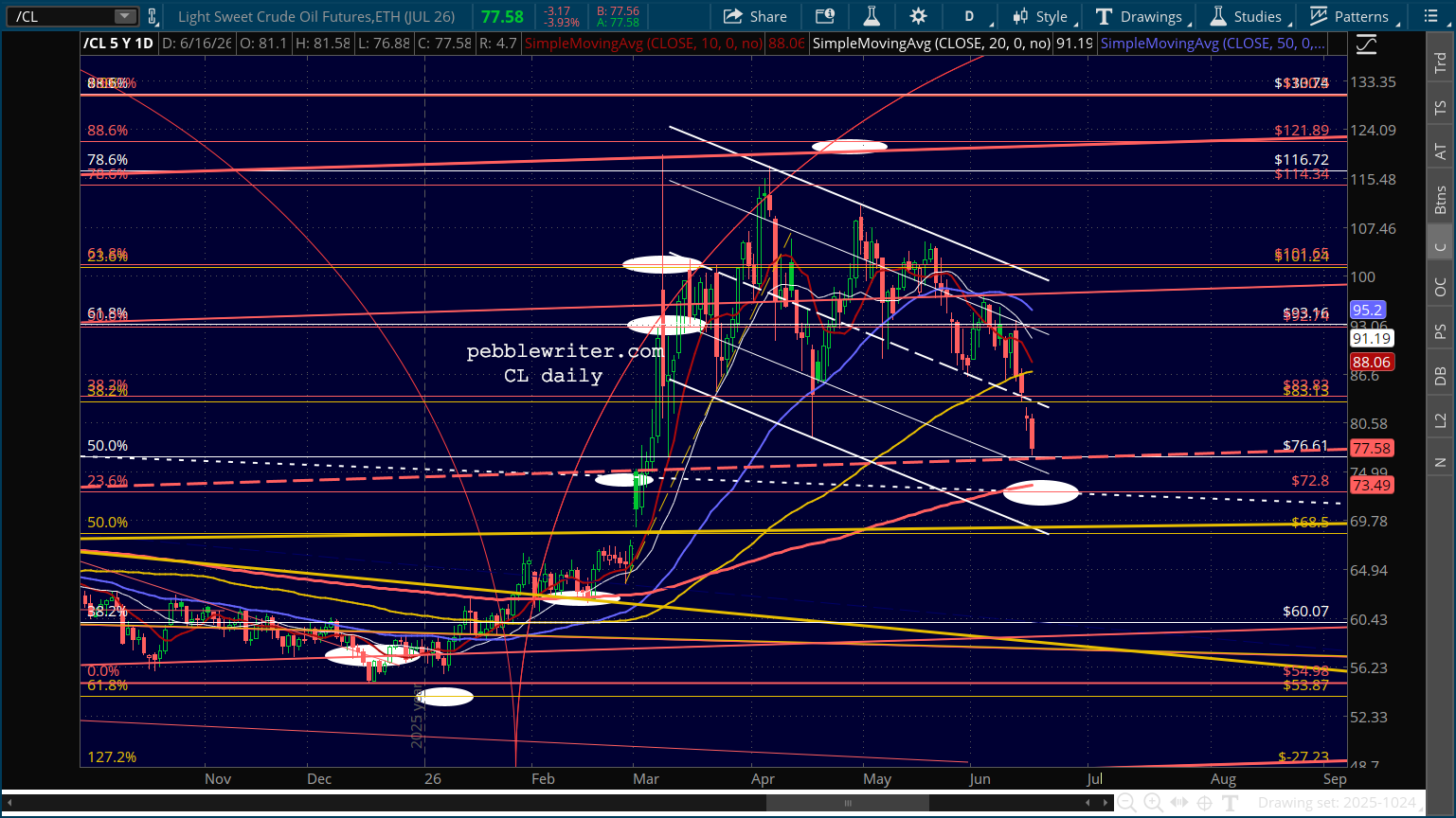

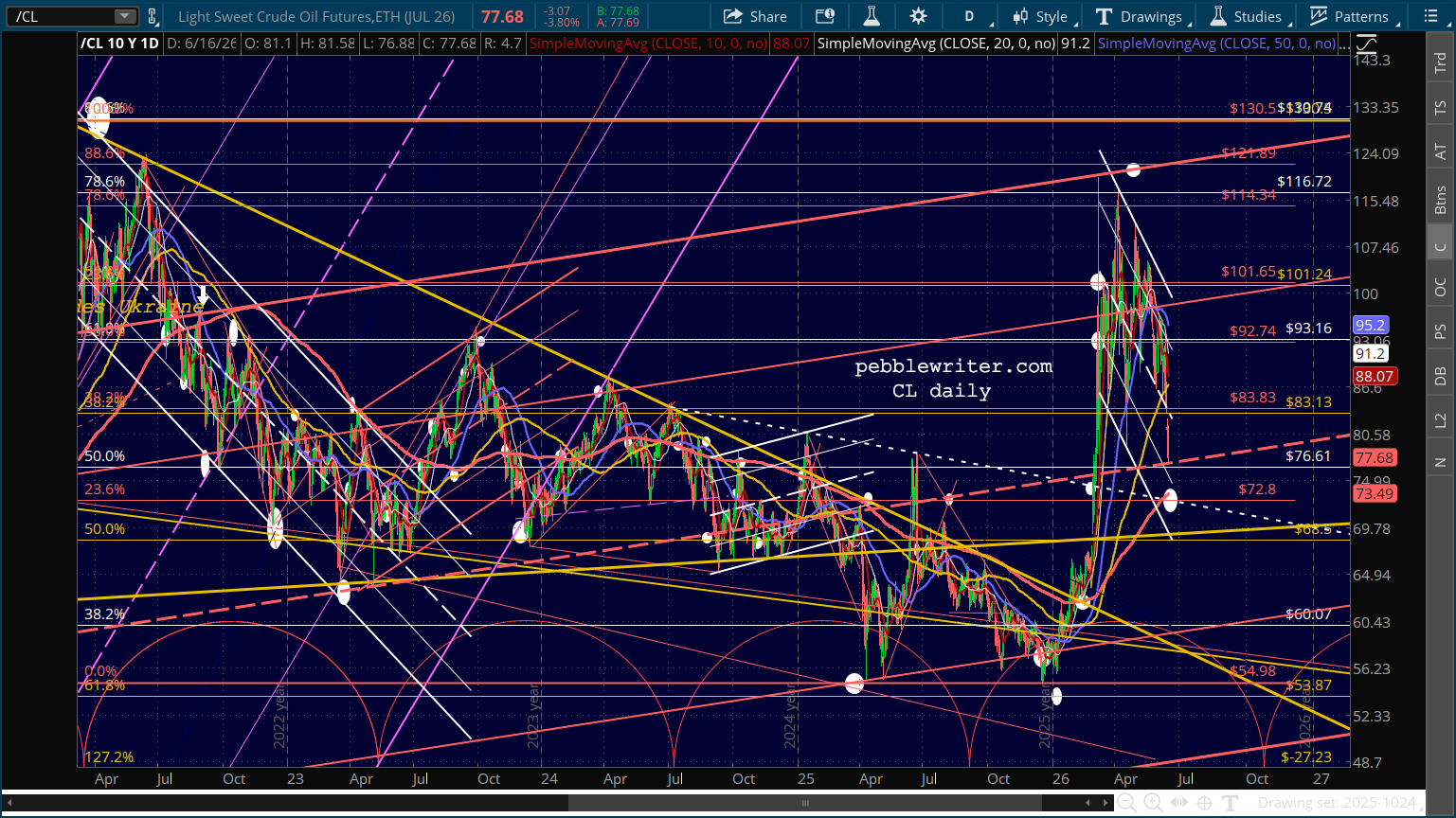

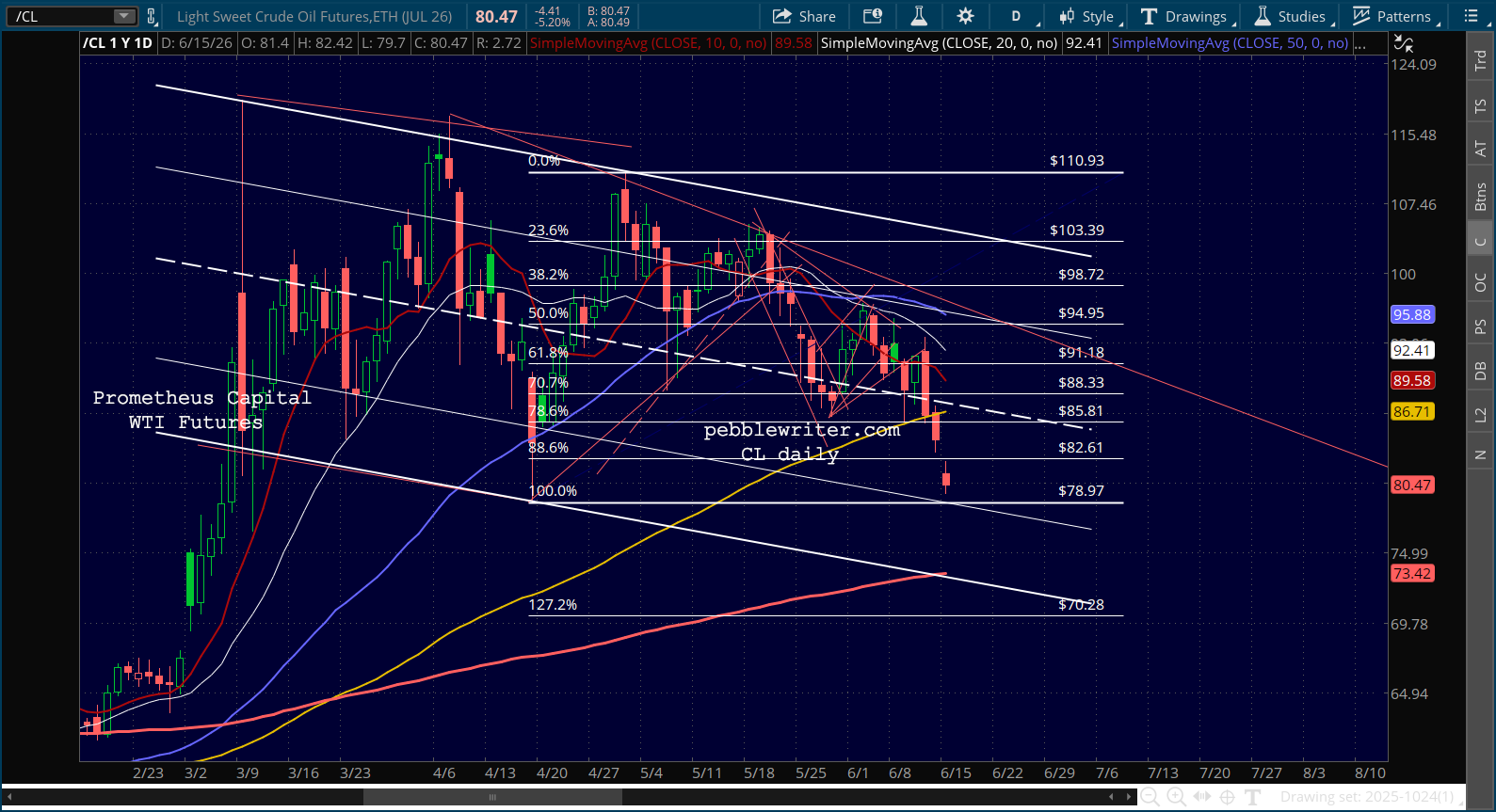

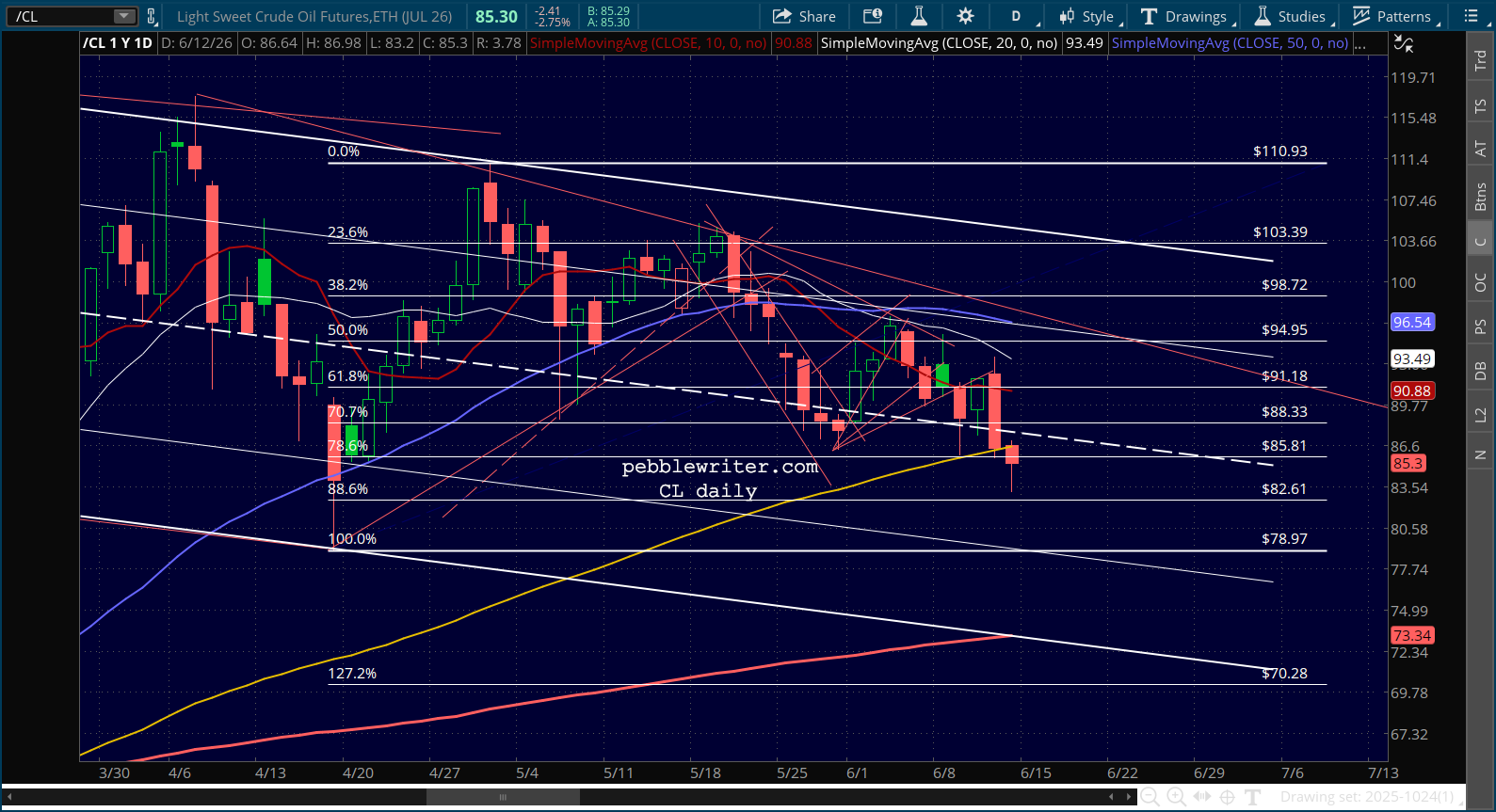

The markets are thrilled that the Iran War might actually be over. Oil prices are endorsing that view, though they are running into strong support in this price range: the 200-day moving average…

…and a combination of an important on top of a large channel midline. CL is backtesting both, with 72.80 a critical line in the sand.

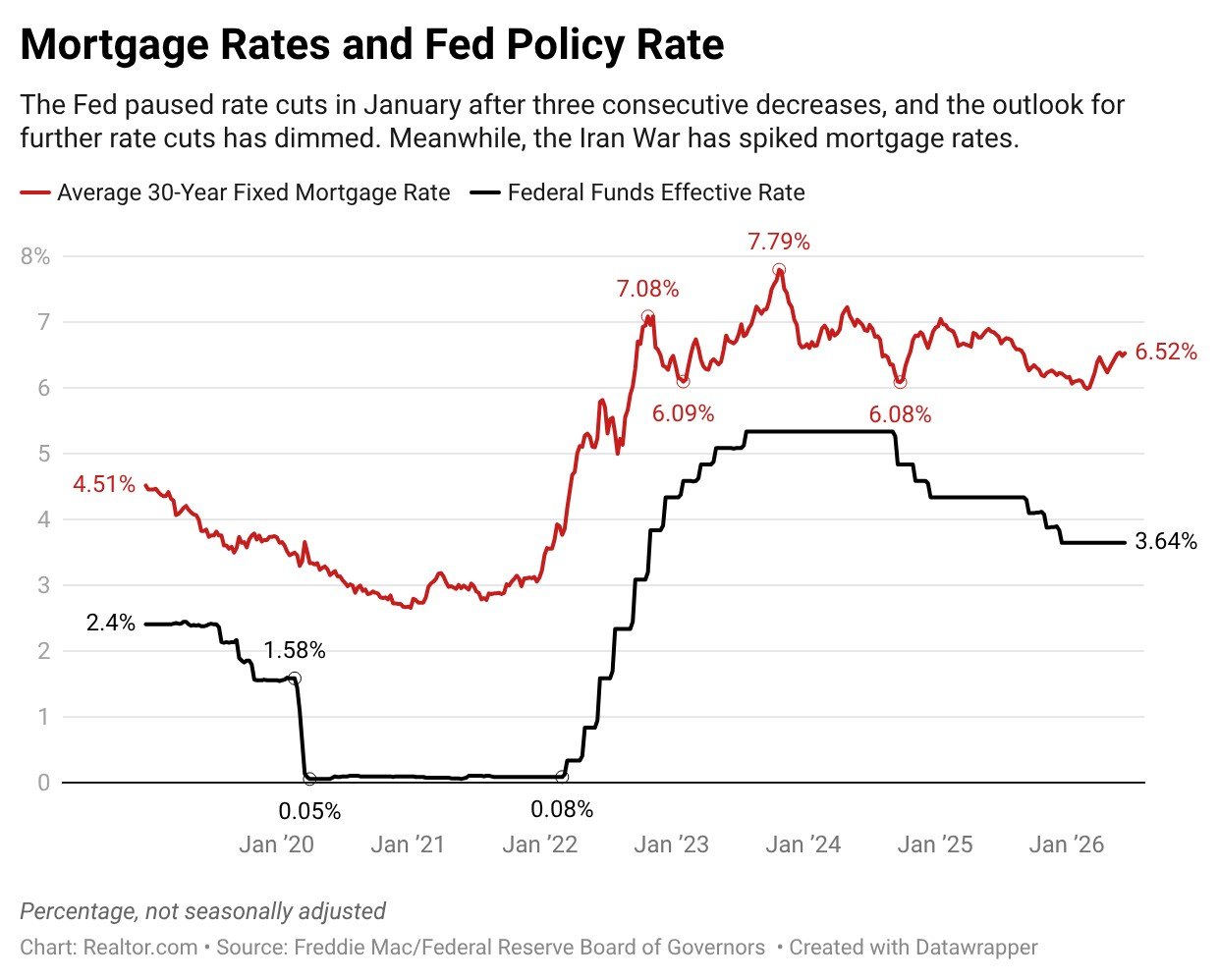

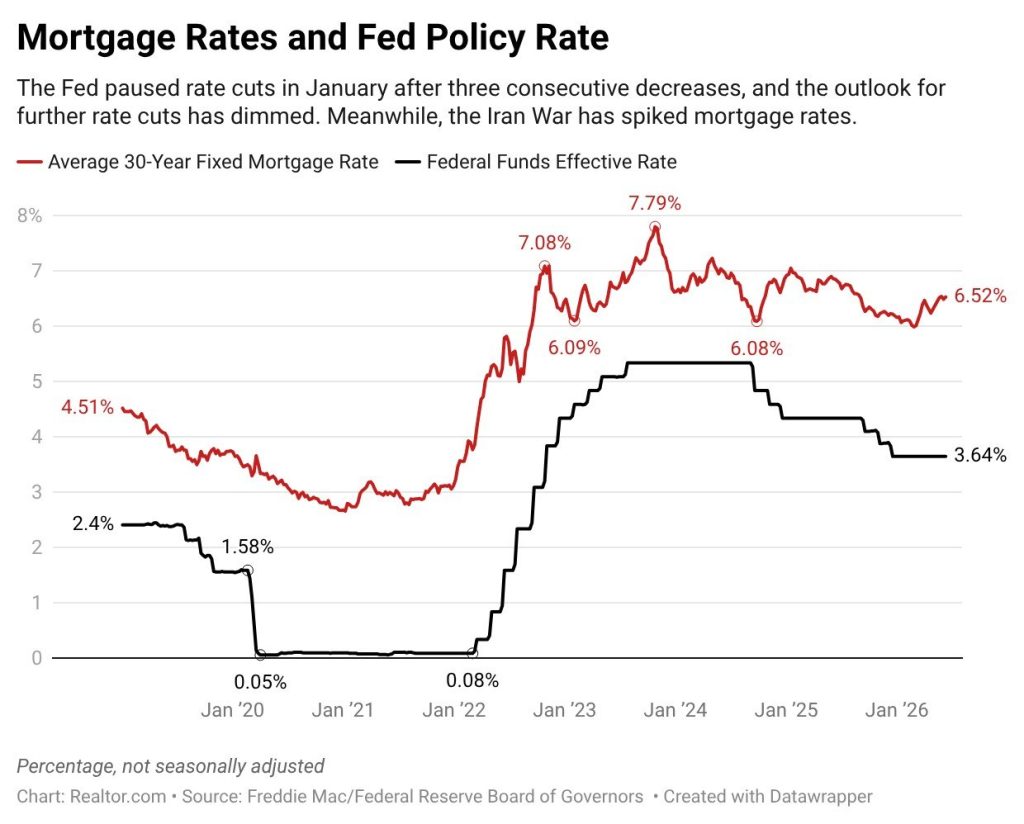

As mentioned before, housing is hung up on high mortgage rates. From the normally bullish realtor.com:

The 244 bps decline in Fed Funds from 6.08 helped keep mortgage rates in a very slight downturn, but obviously still elevated. If the Fed were to cut rates further — unlikely until we see a verified drop in inflation — it would help bring mortgage rates down, but with housing inventory being in short supply and most buyers basing their purchase decision on payment, not price, lower rates would simply prop up prices.

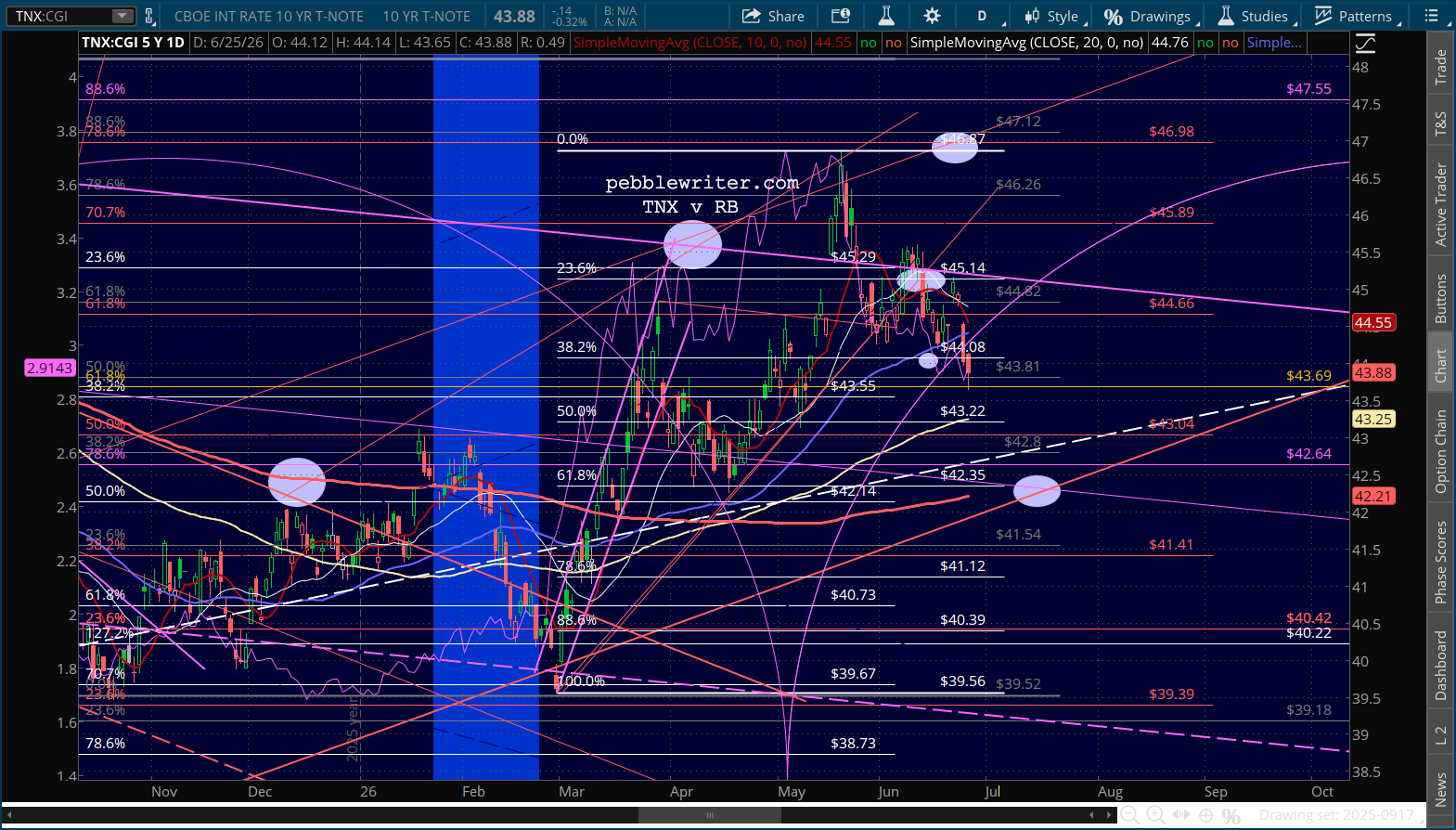

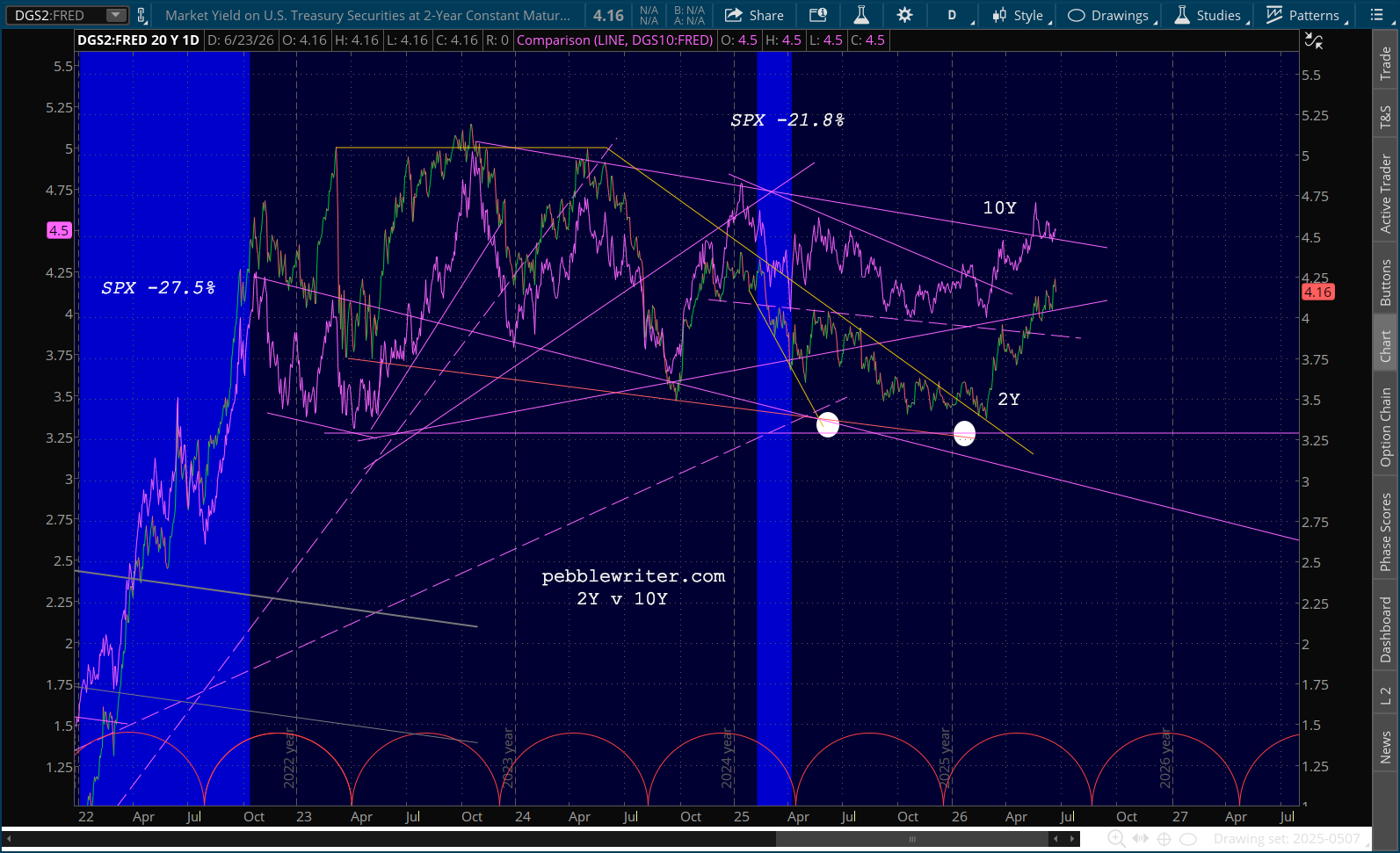

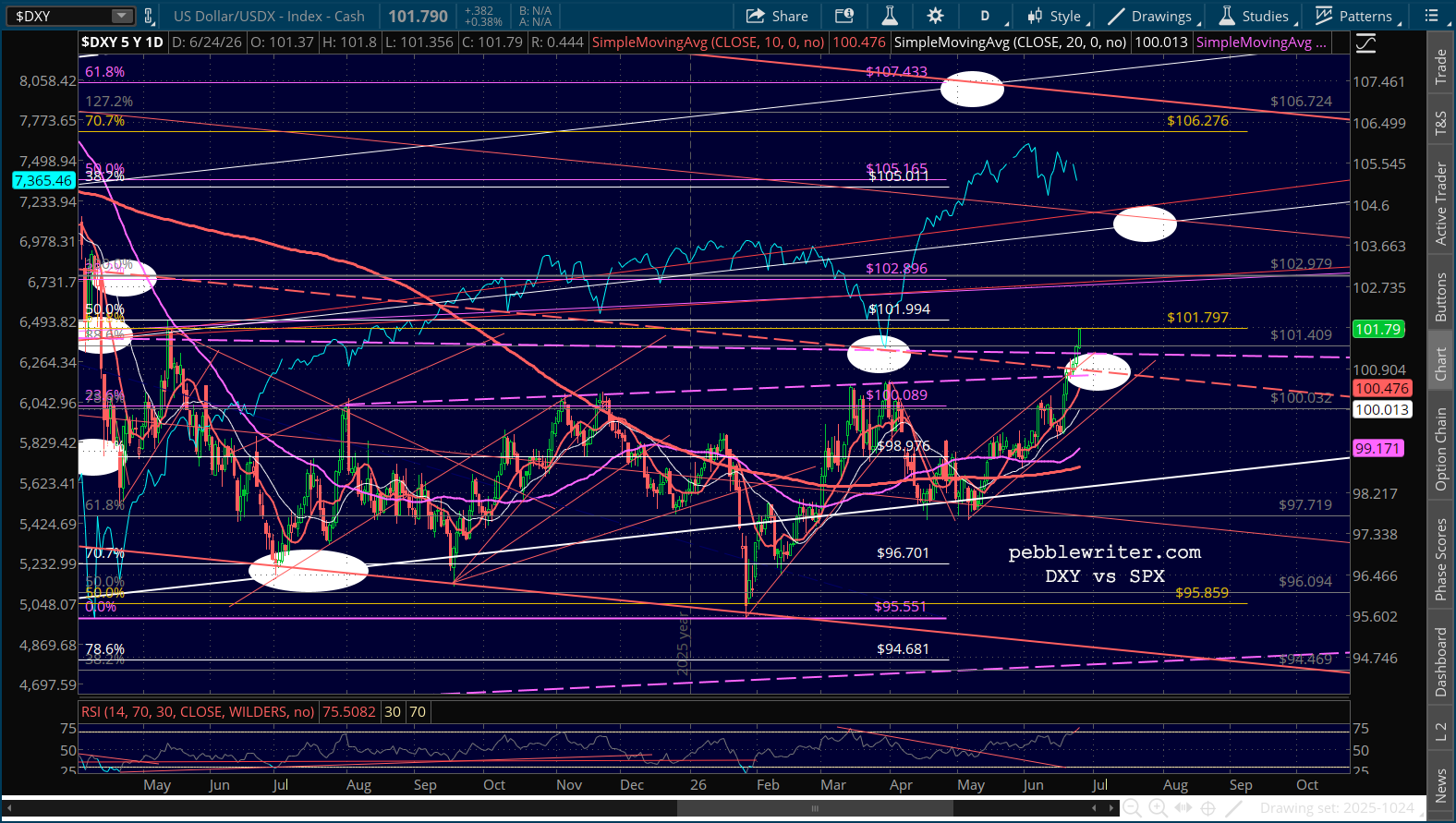

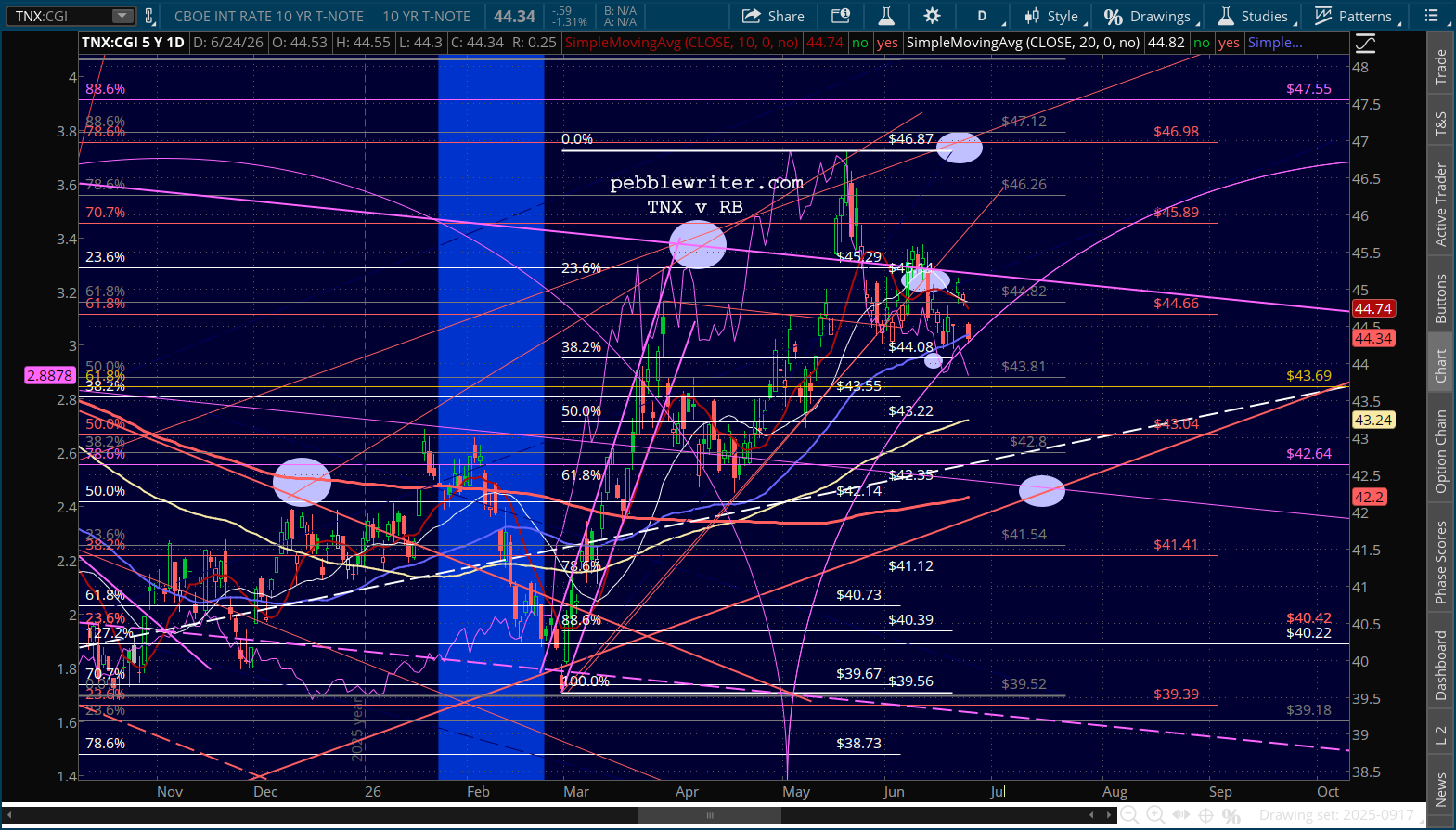

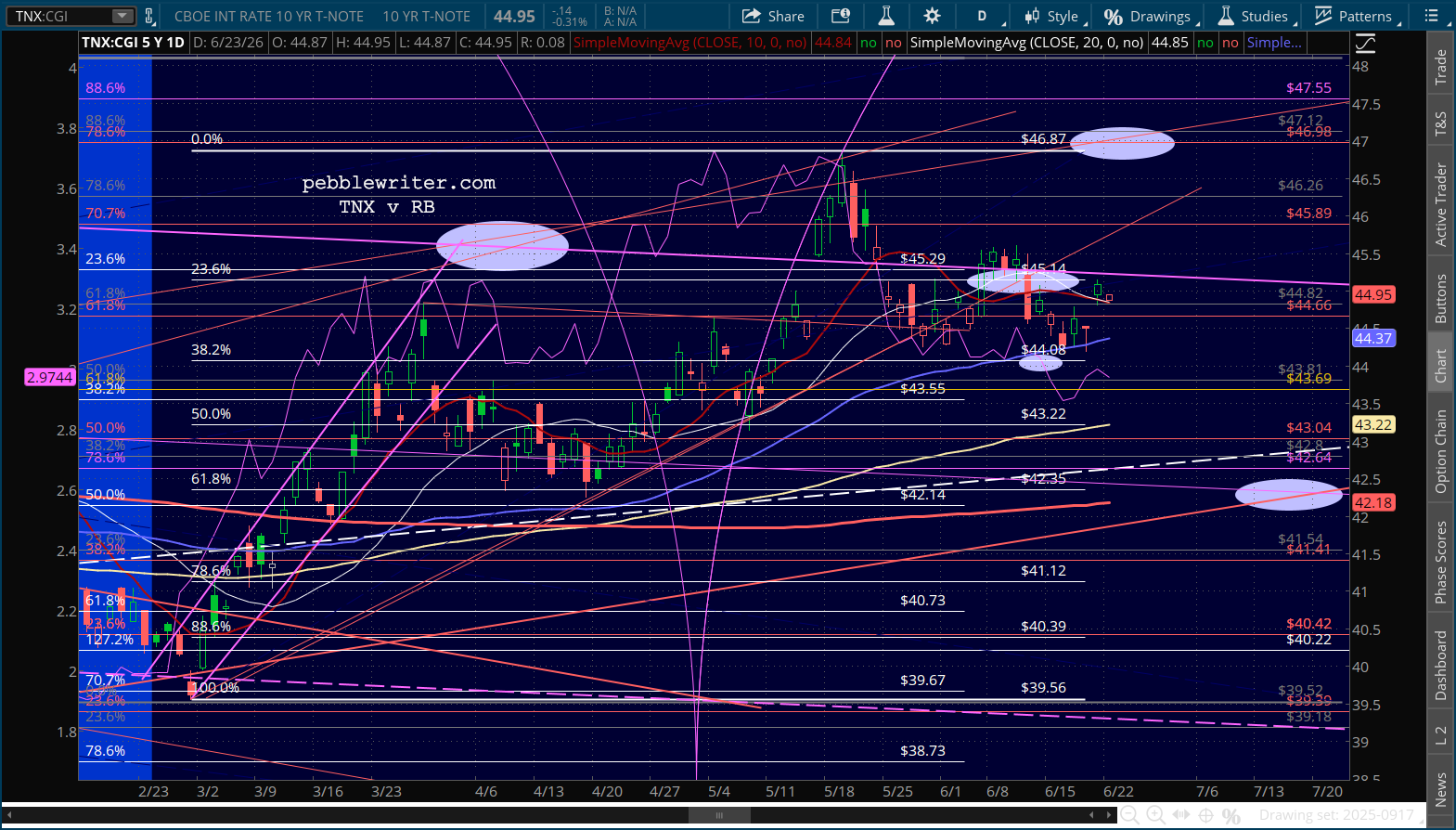

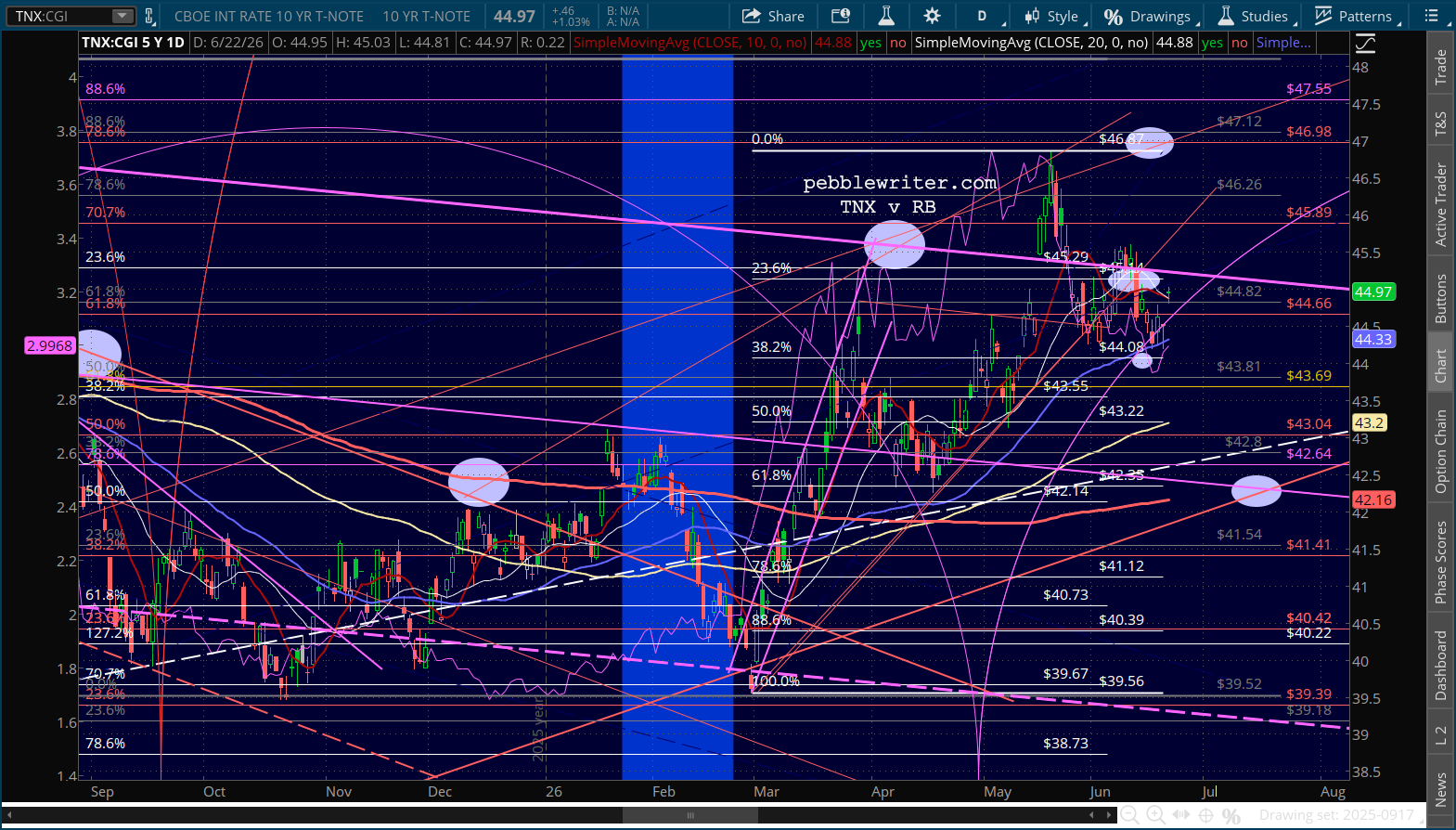

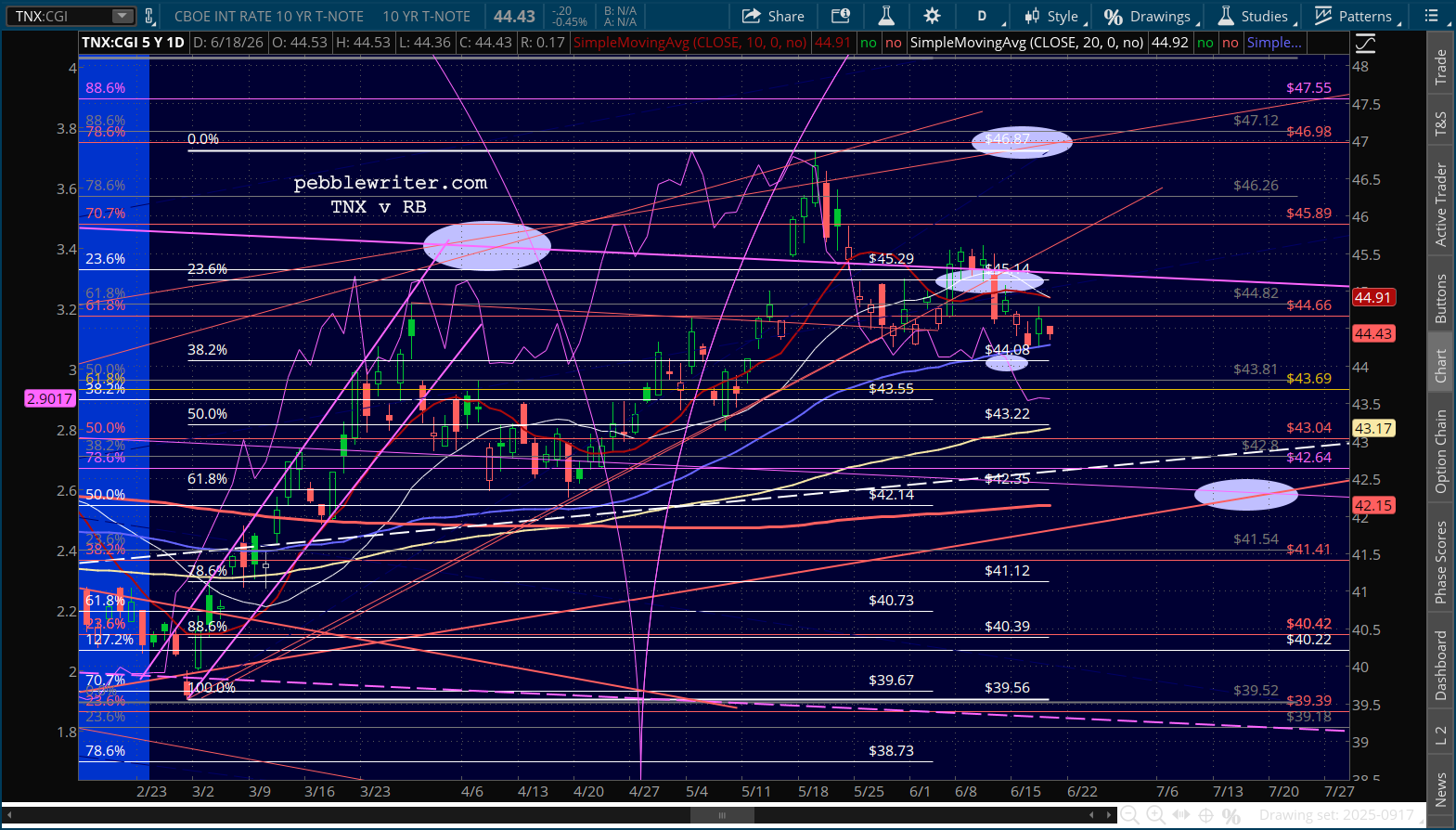

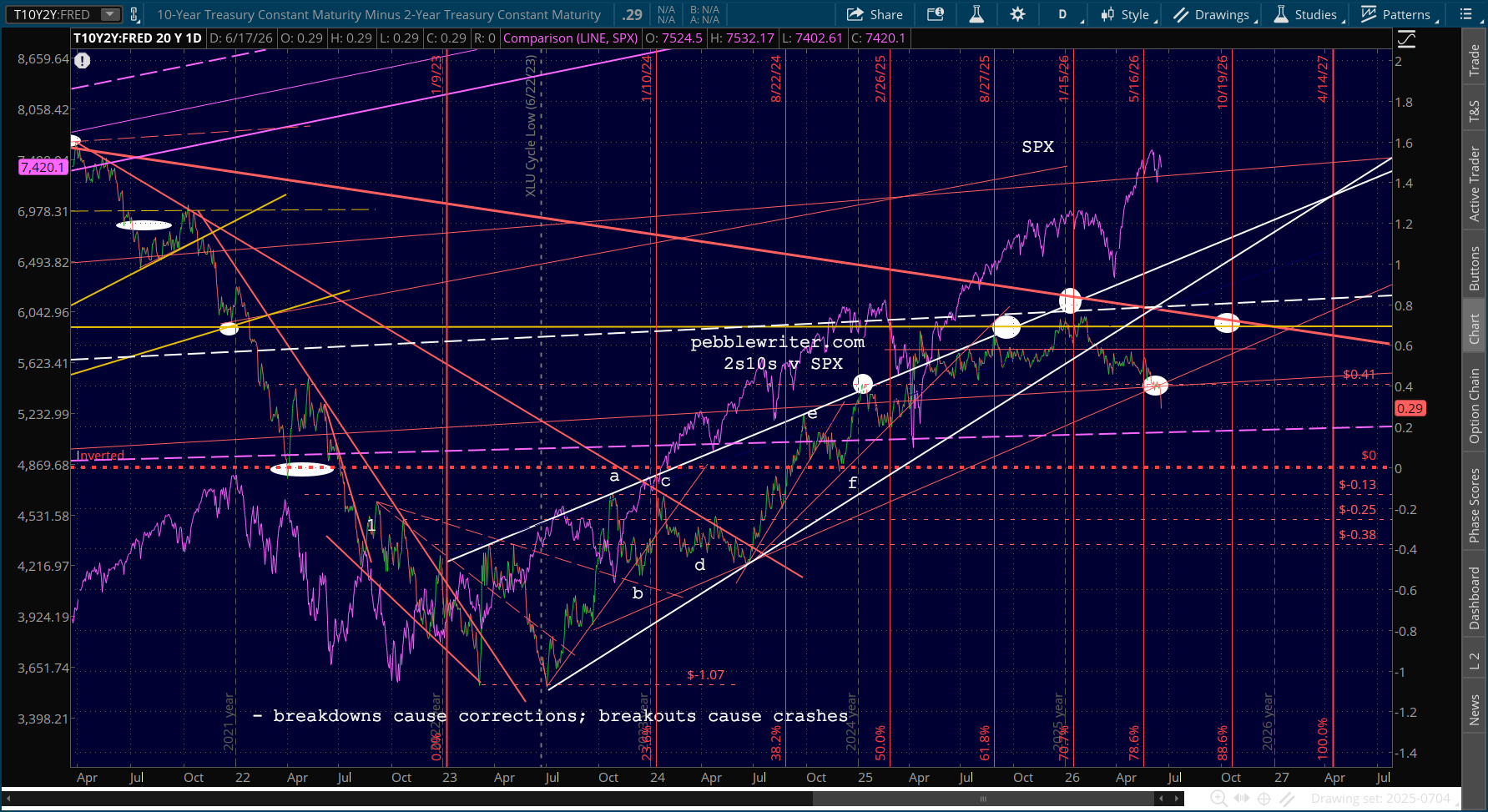

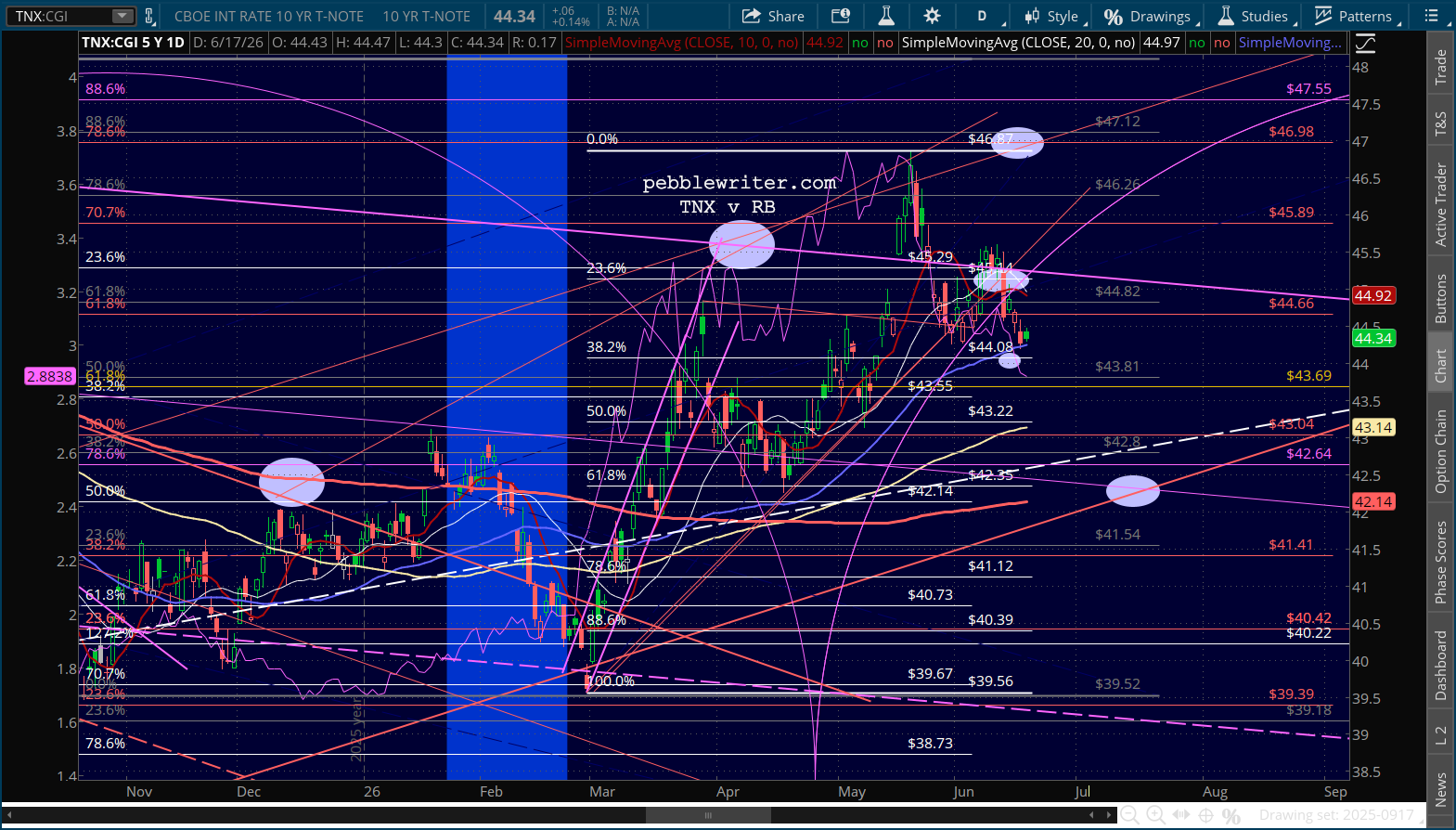

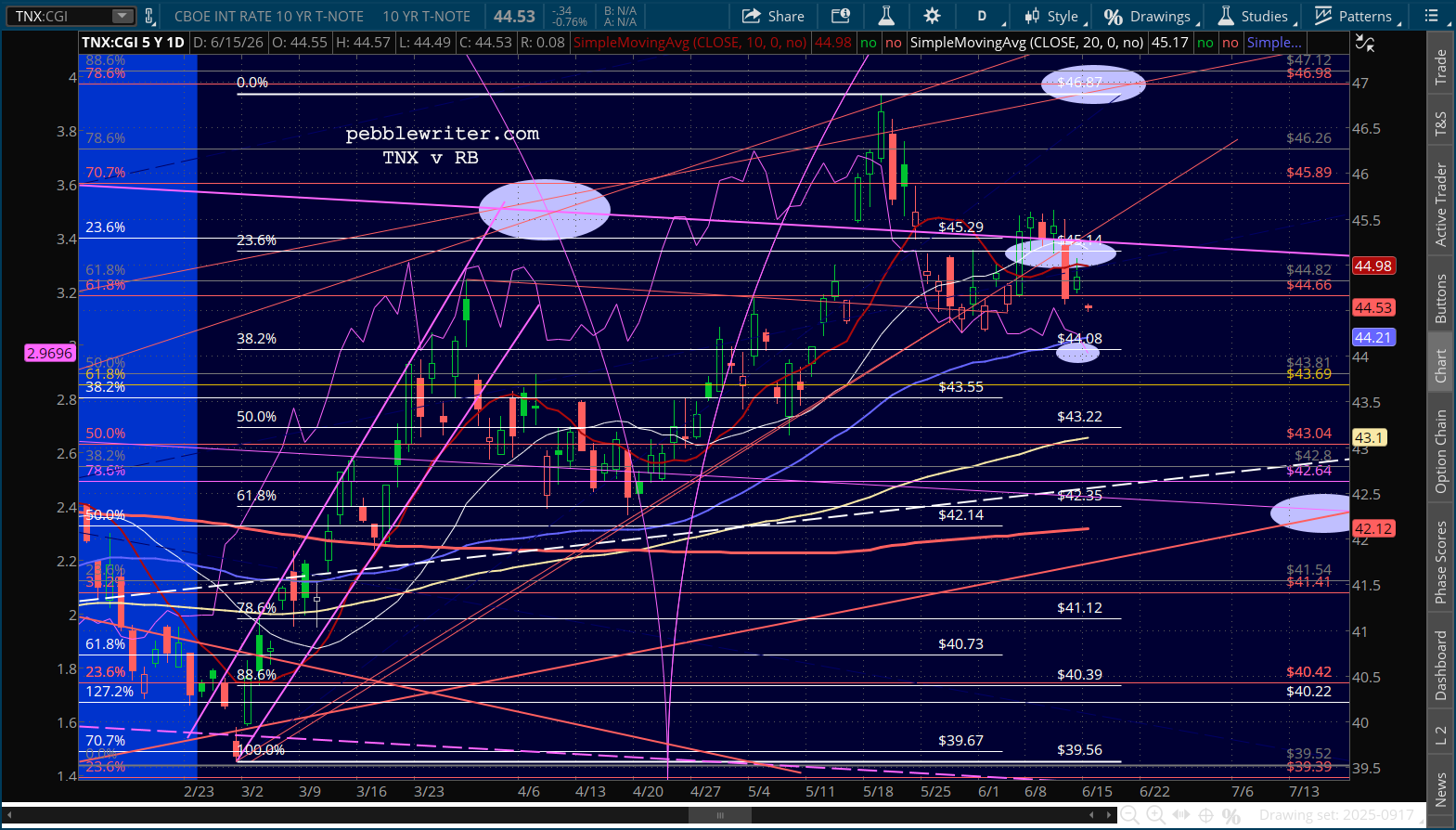

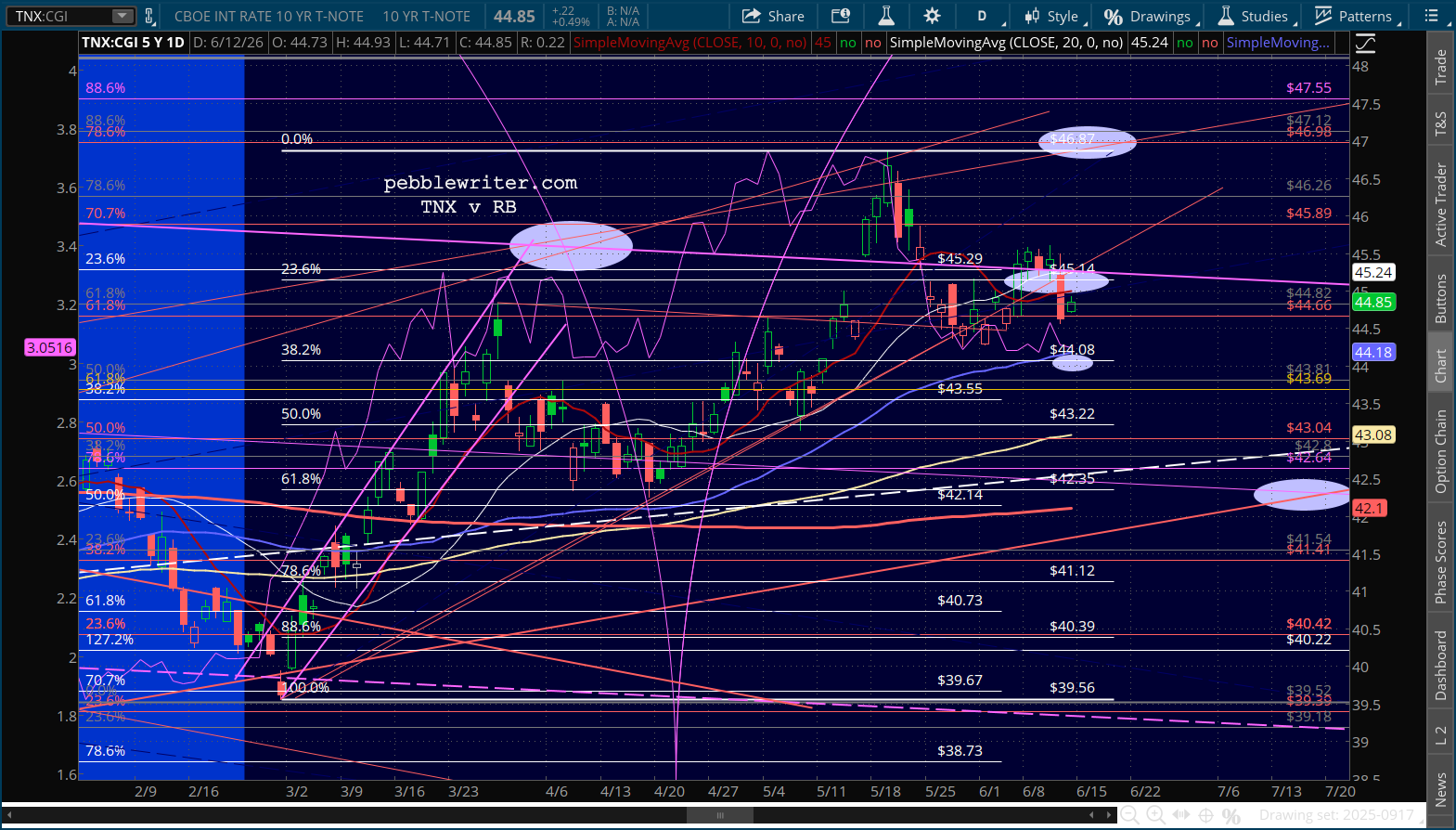

The 10Y, still elevated at 4.45%, would be at 3.25% if not for the war. We may yet get there, just out of sync with the cycle signal. But, it’s hard to imagine it happening in the absence of a nice little recession.

stay tuned…