The OECD reports that global economic output will fall by 7.6% if another wave of coronavirus arrives in 2020, by 6% if not. US GDP will fall 8.5% if a second wave occurs, and 7.3% if a second wave is avoided. If Dr. Fauci is right, a second wave is likely. I’m almost certain of it.

Also out this morning, US CPI – which came in roughly in line with consensus and registered the third monthly drop in a row.

CPI fell 0.1% in May versus the 0.8% drop in April – the biggest since the GFC. YoY, CPI inched up 0.1% versus April’s 0.3% gain.

CPI fell 0.1% in May versus the 0.8% drop in April – the biggest since the GFC. YoY, CPI inched up 0.1% versus April’s 0.3% gain.

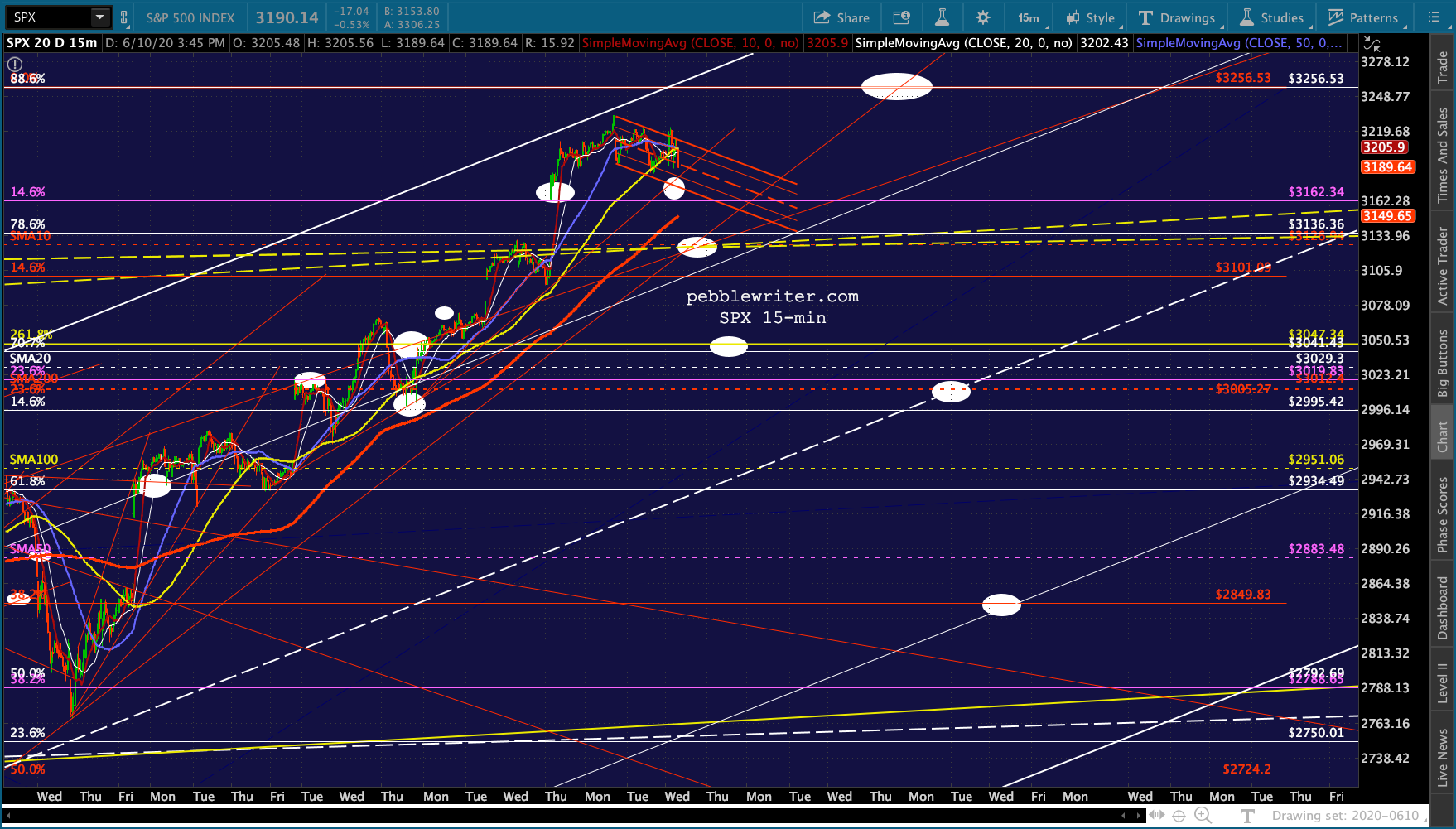

The SPX version:

The SPX version:

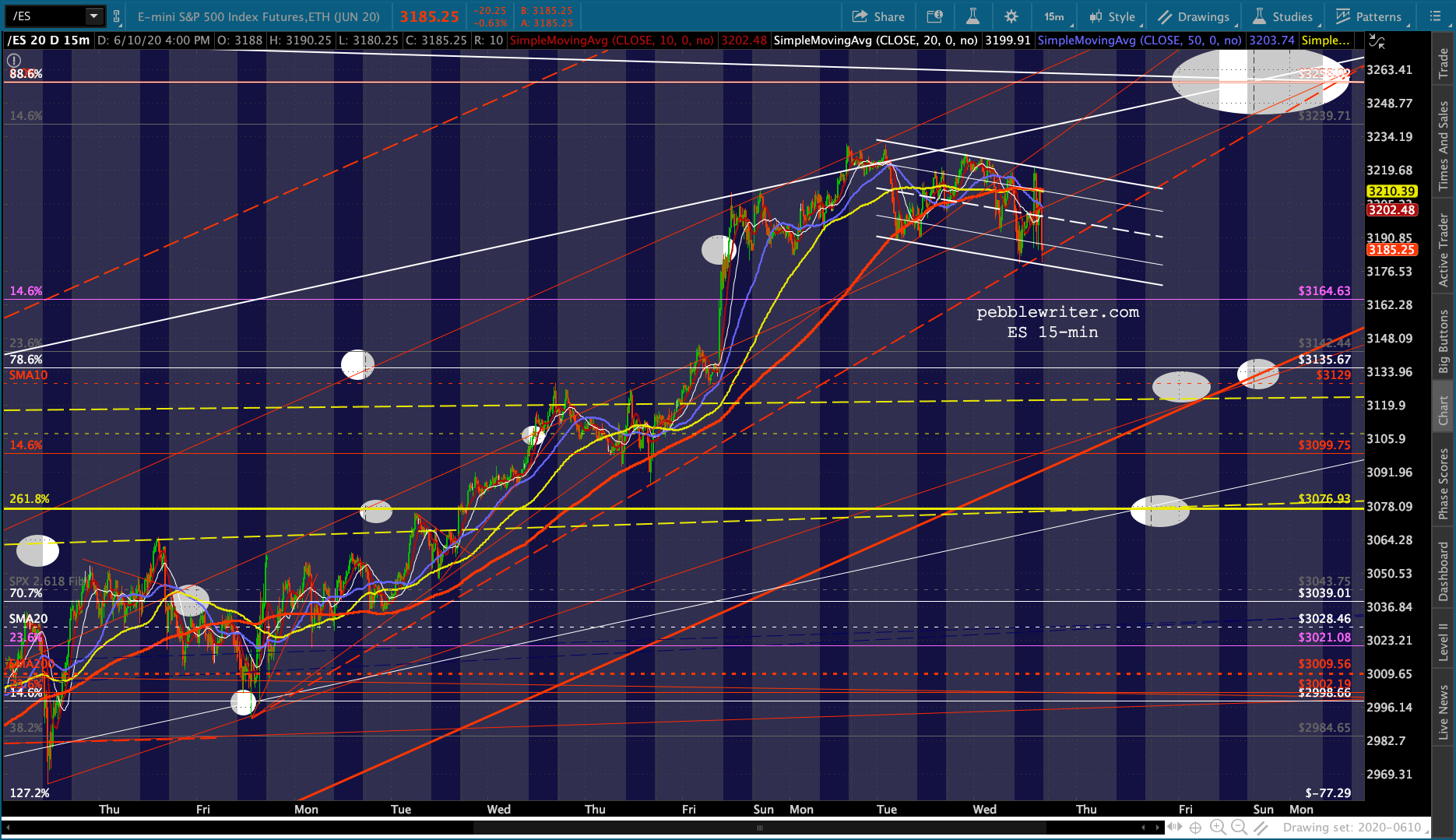

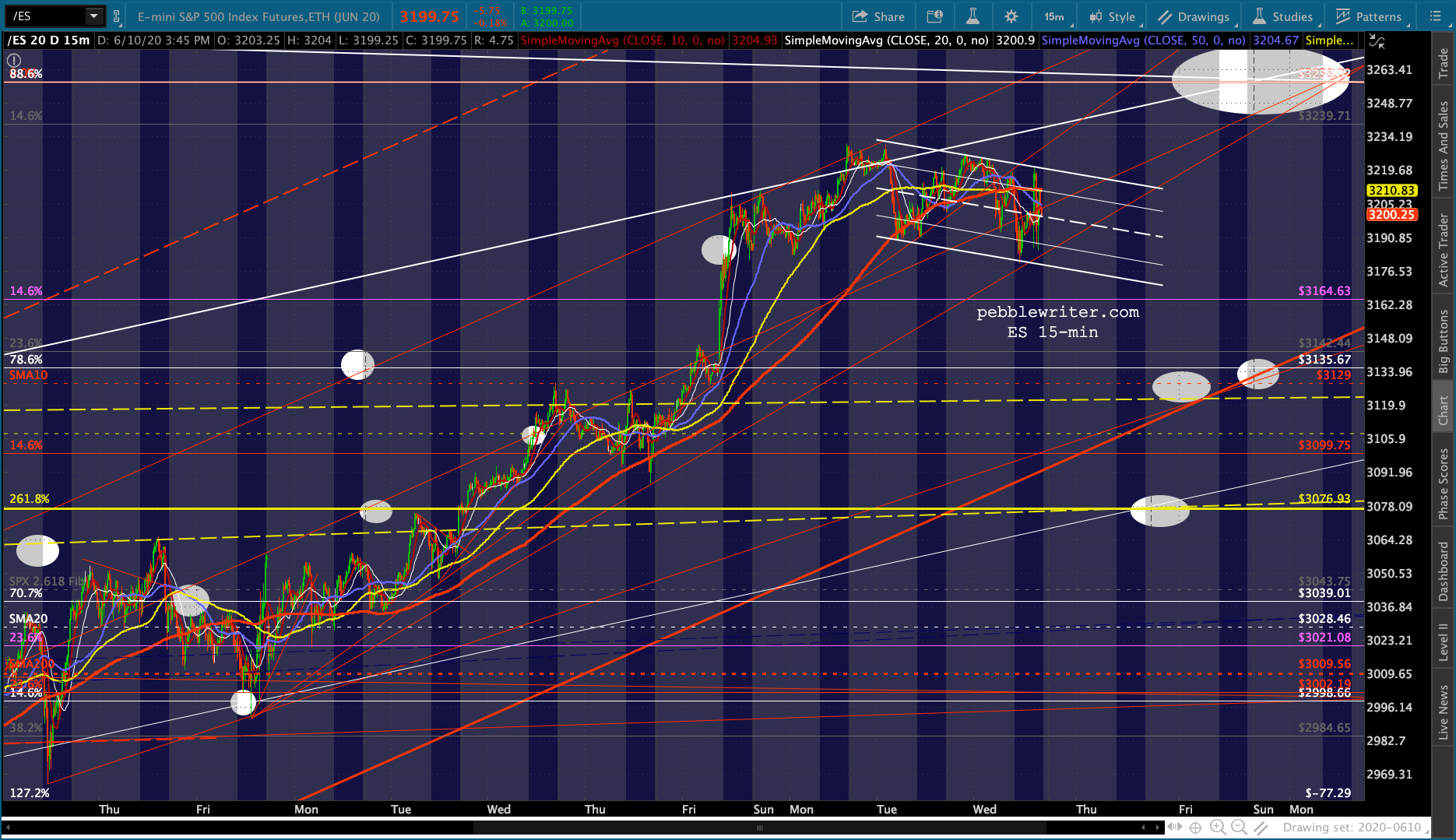

I see two bullish scenarios and one bearish. Bullish: we get a sell off (perhaps to the .786 at ES 3135) following today’s Fed action followed by a rebound into the end of the quarter; or, we see stocks continue to inch higher toward the .886 and then hang around for another two weeks until the end of Q2. Bearish: the market pukes here at or near the .886 and resumes a long, deep correction.

I see two bullish scenarios and one bearish. Bullish: we get a sell off (perhaps to the .786 at ES 3135) following today’s Fed action followed by a rebound into the end of the quarter; or, we see stocks continue to inch higher toward the .886 and then hang around for another two weeks until the end of Q2. Bearish: the market pukes here at or near the .886 and resumes a long, deep correction.

I’m leaning toward a correction beginning today, but am unsure whether the channel bottoms at ES 3076 and 3122-3135 will hold or not. It depends a great deal on what Powell says later today.

As discussed yesterday, I believe the Fed will pull its punches, shifting responsibility for the employment problem to the politicians. There is little that even lower interest rates or more printing can do to ameliorate the pandemic or reduce systemic unemployment which has been largely driven by the shutdown.

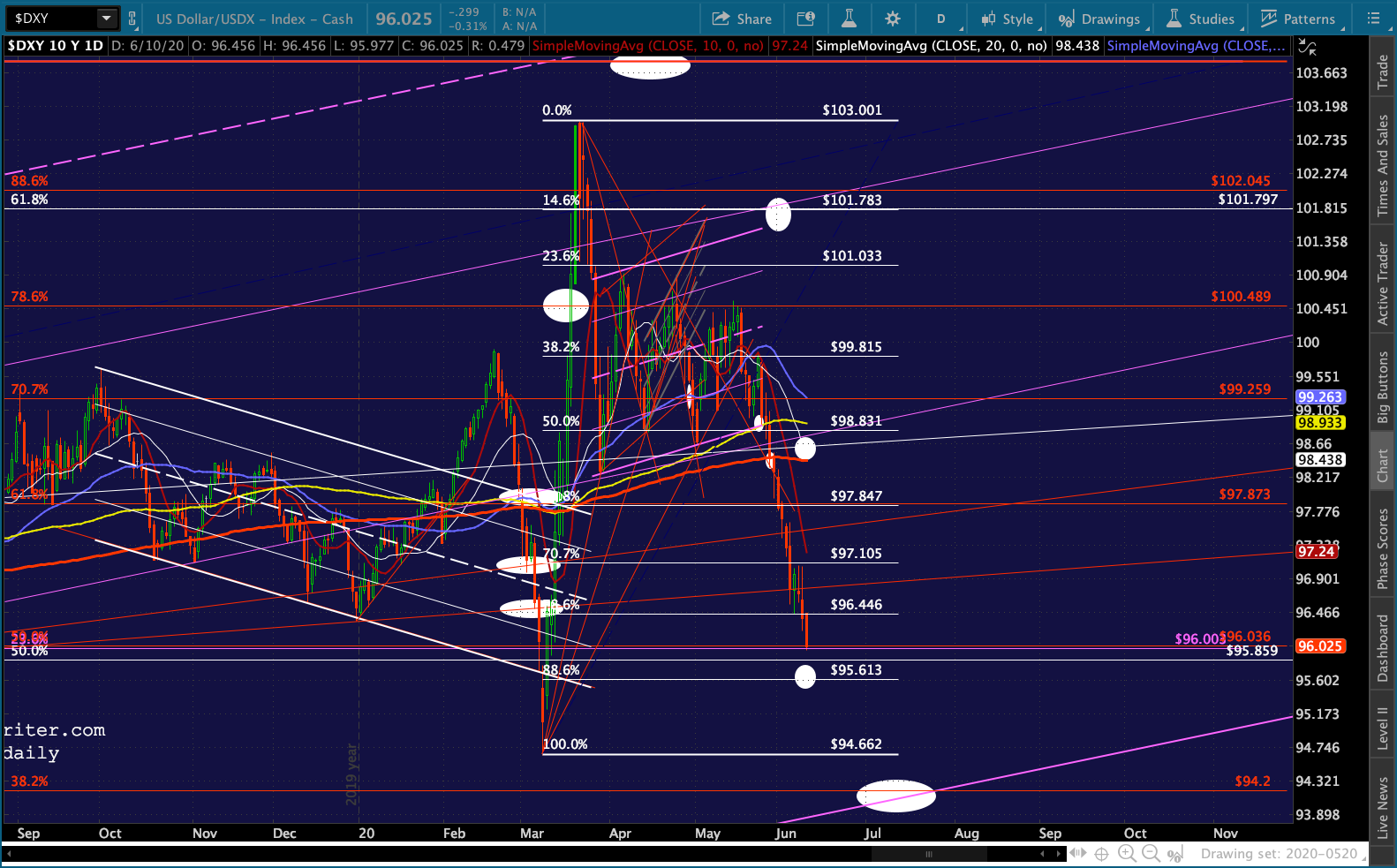

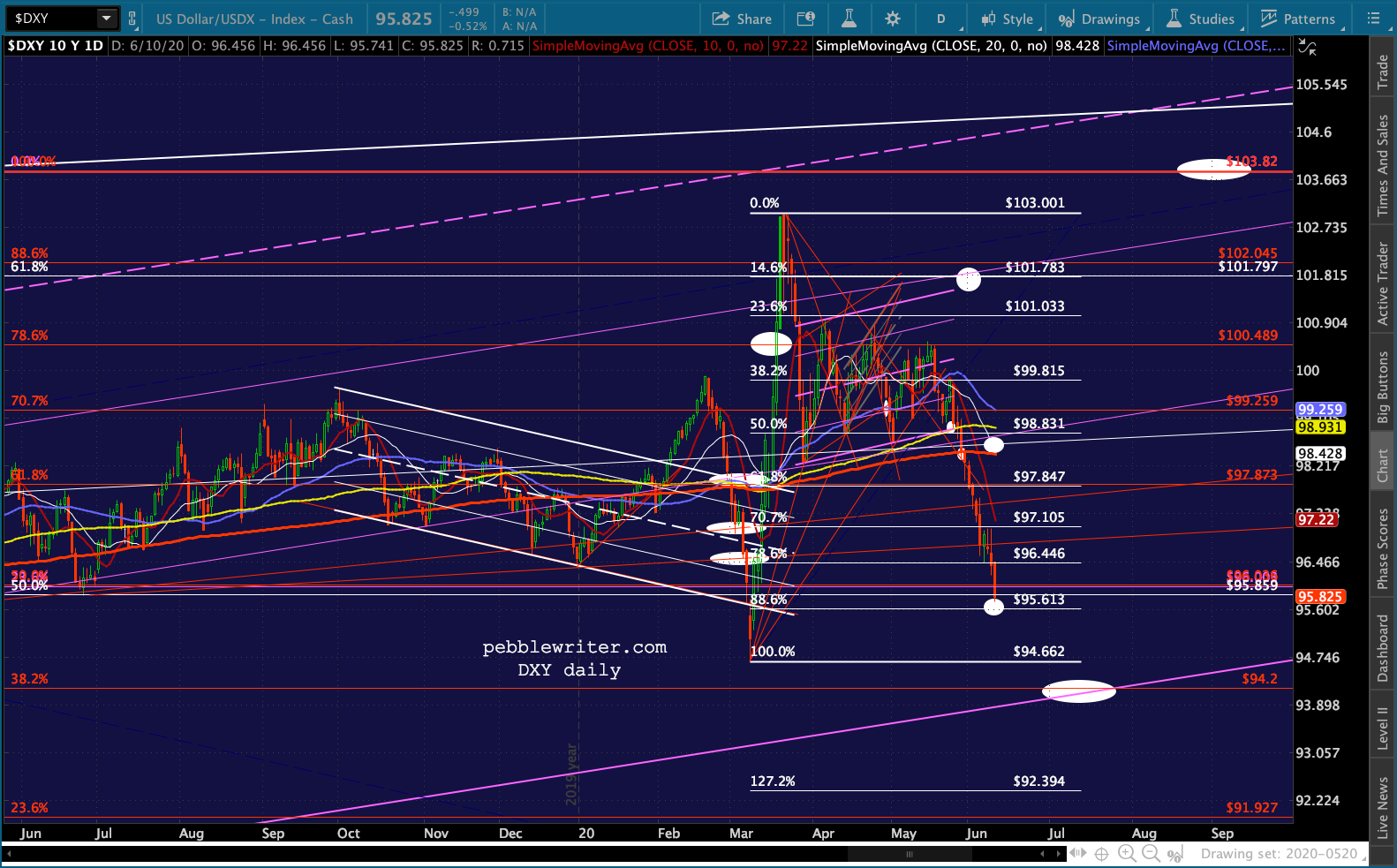

The market has disagreed with me for the past two weeks, with a weakening DXY reflecting more stimulus – or at least an expansion relative to the eurozone – which has its own problems but is, by and large, handling the pandemic better than the US.

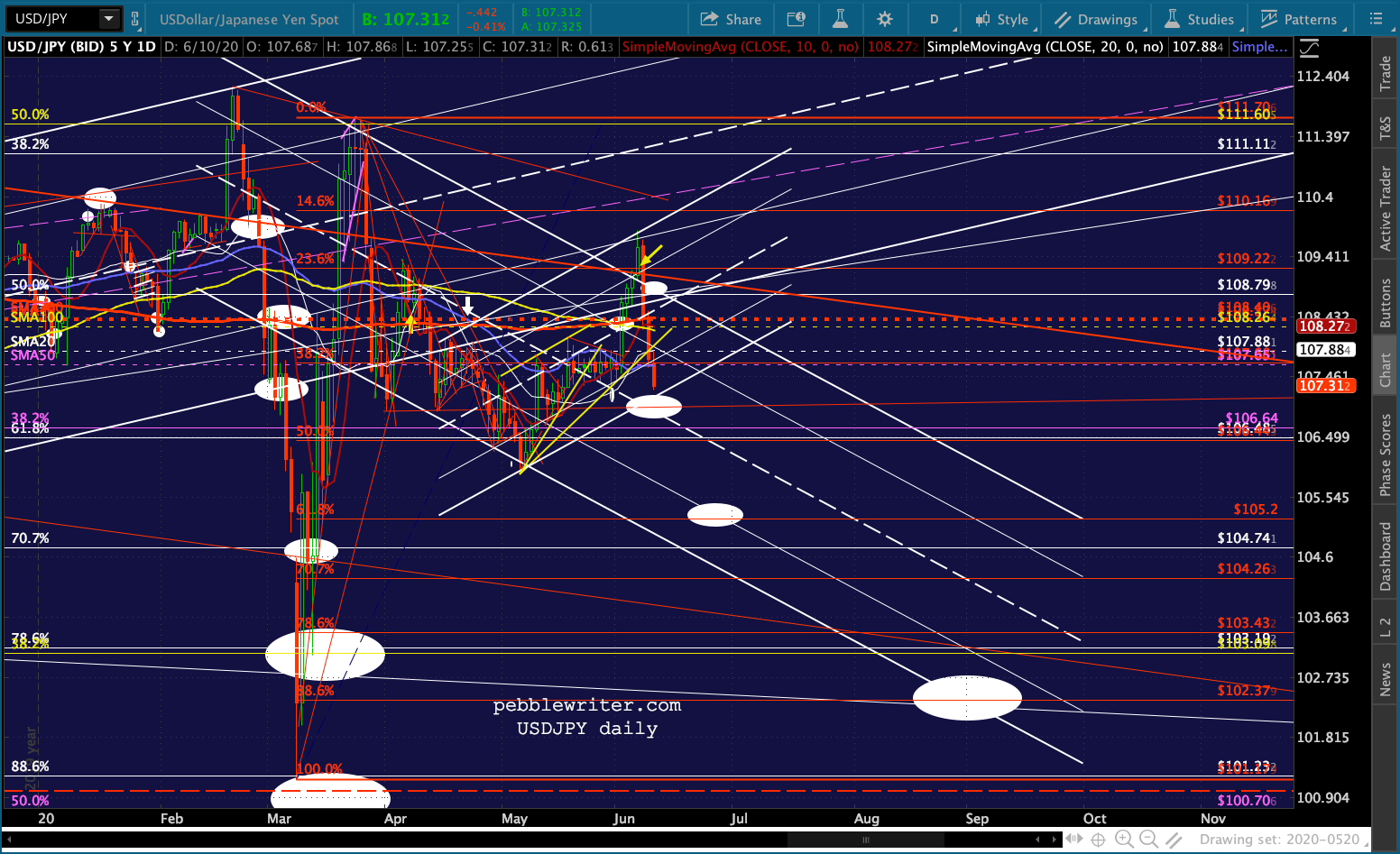

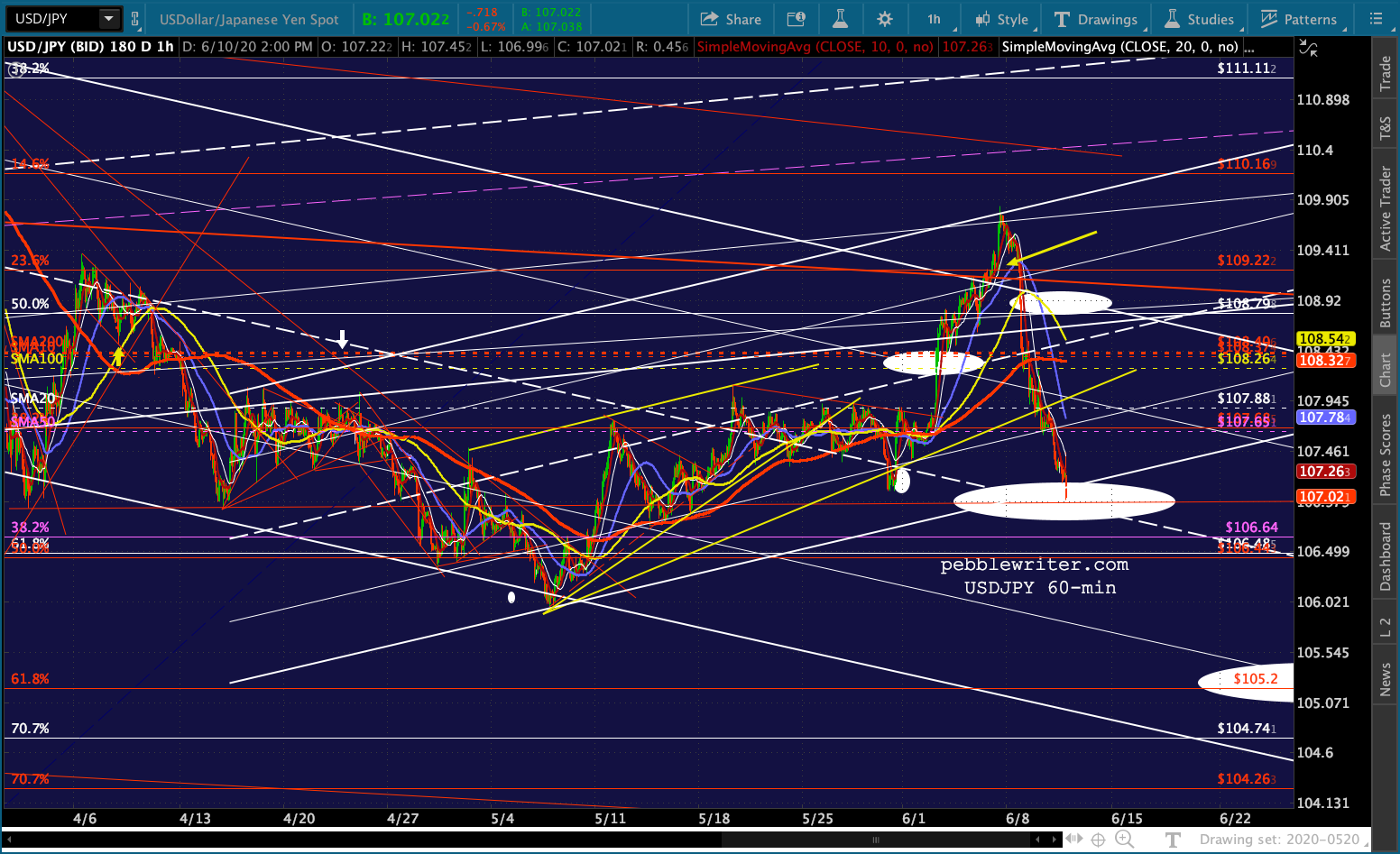

The dollar is even losing ground to the yen.

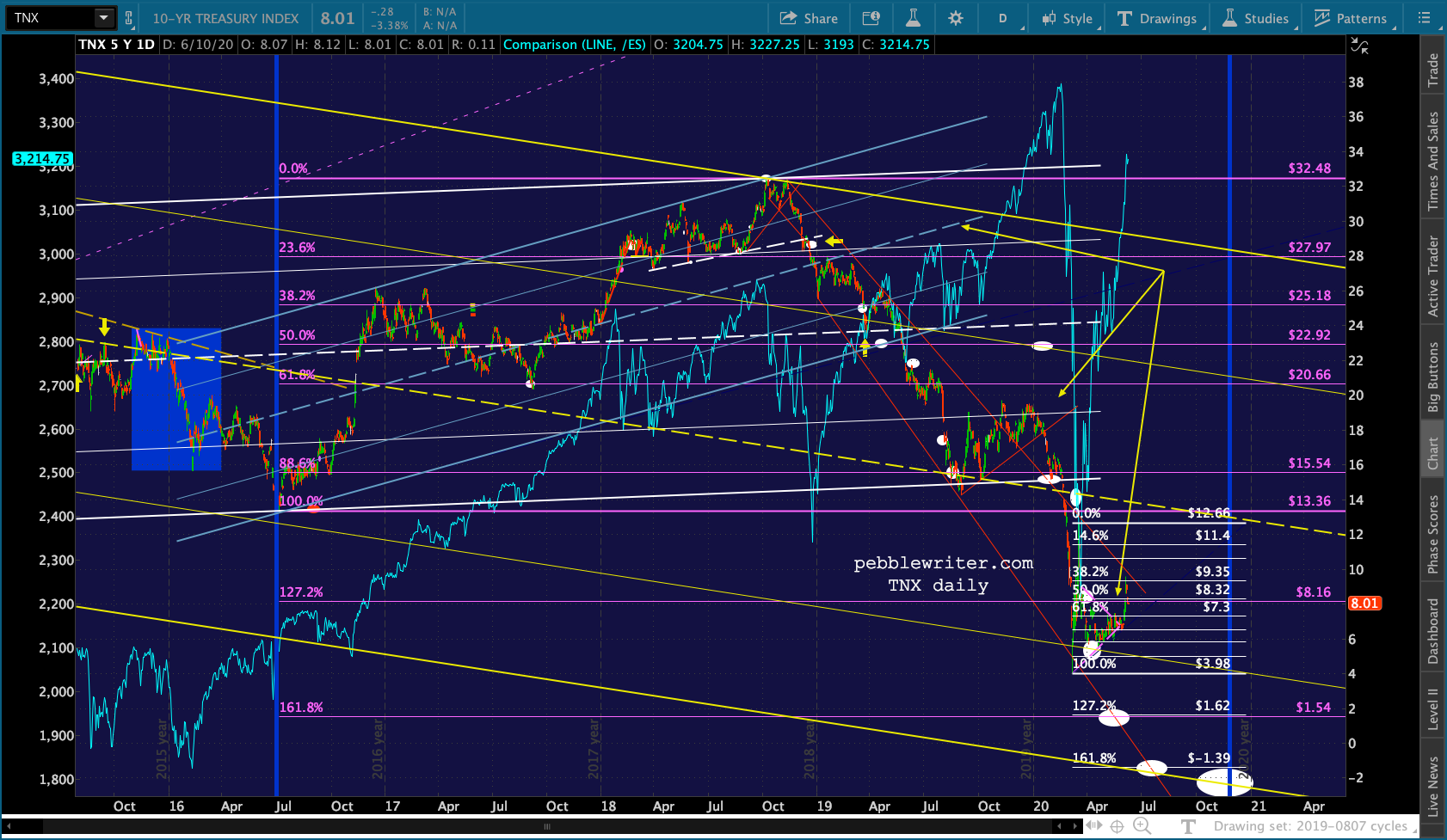

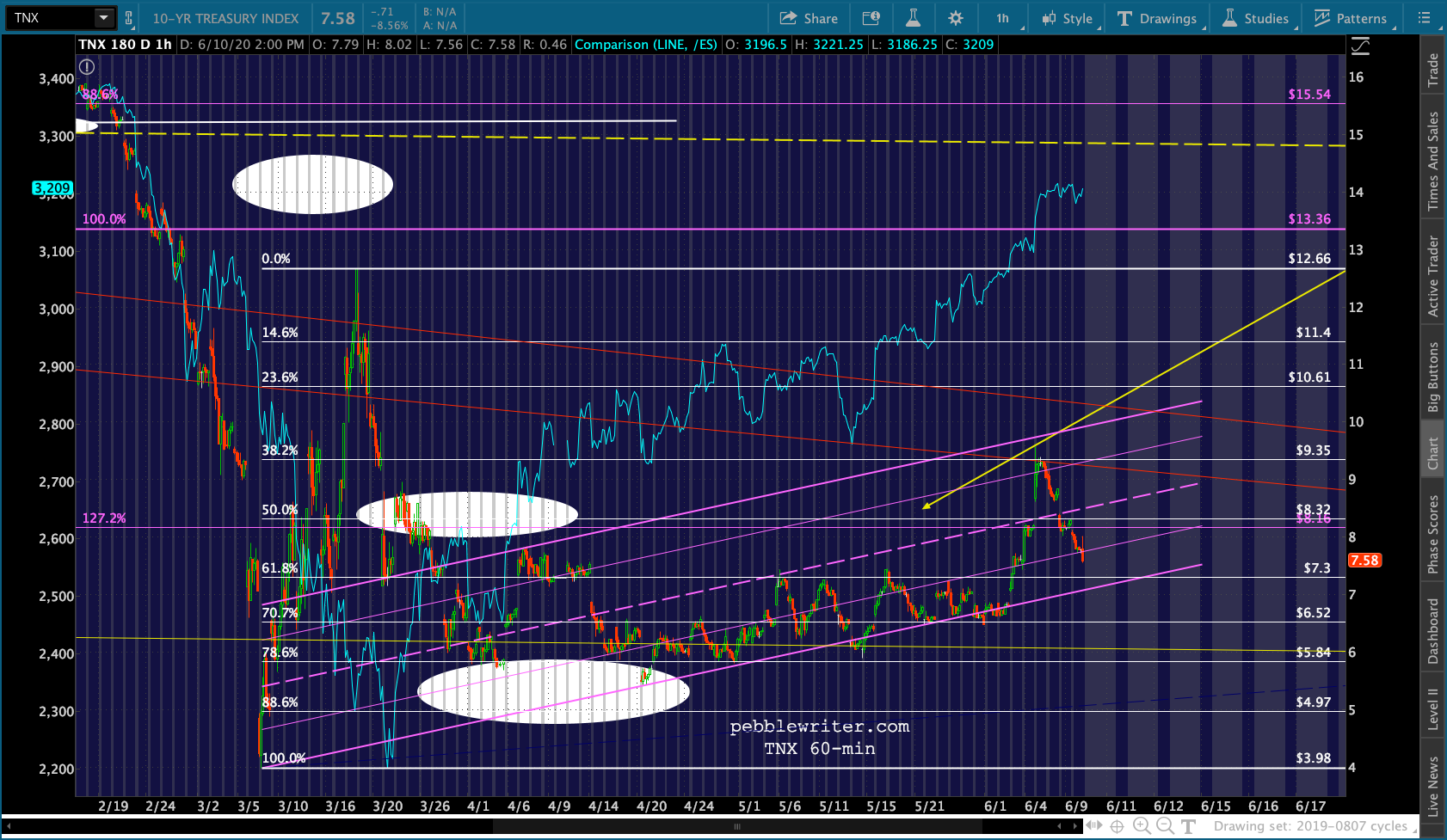

The dollar is even losing ground to the yen. The interest rate picture confuses things, as we recently saw the 10Y top 0.90%…

The interest rate picture confuses things, as we recently saw the 10Y top 0.90%…

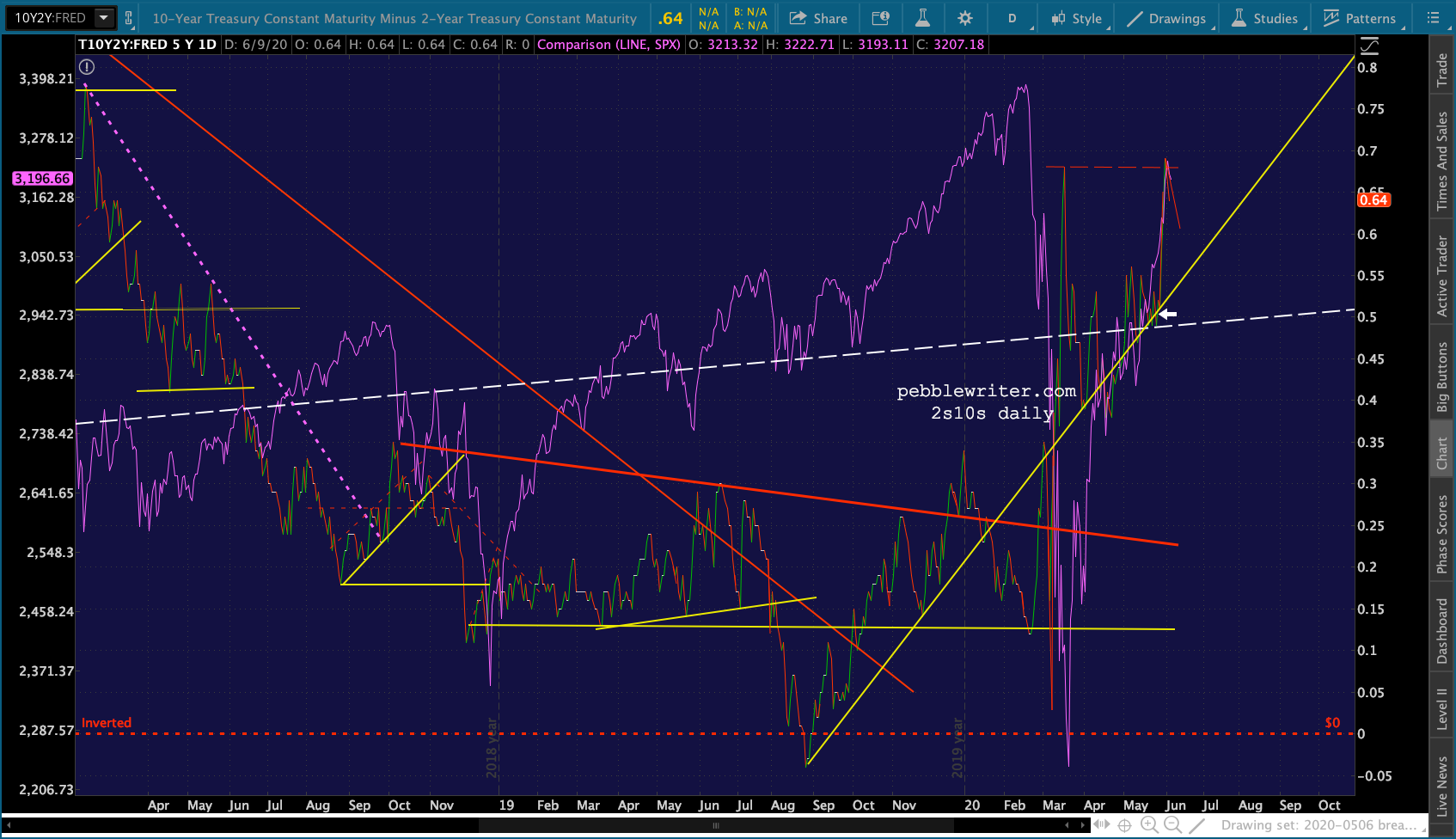

…and the 2s10s blow out to near March’s highs.

…and the 2s10s blow out to near March’s highs.

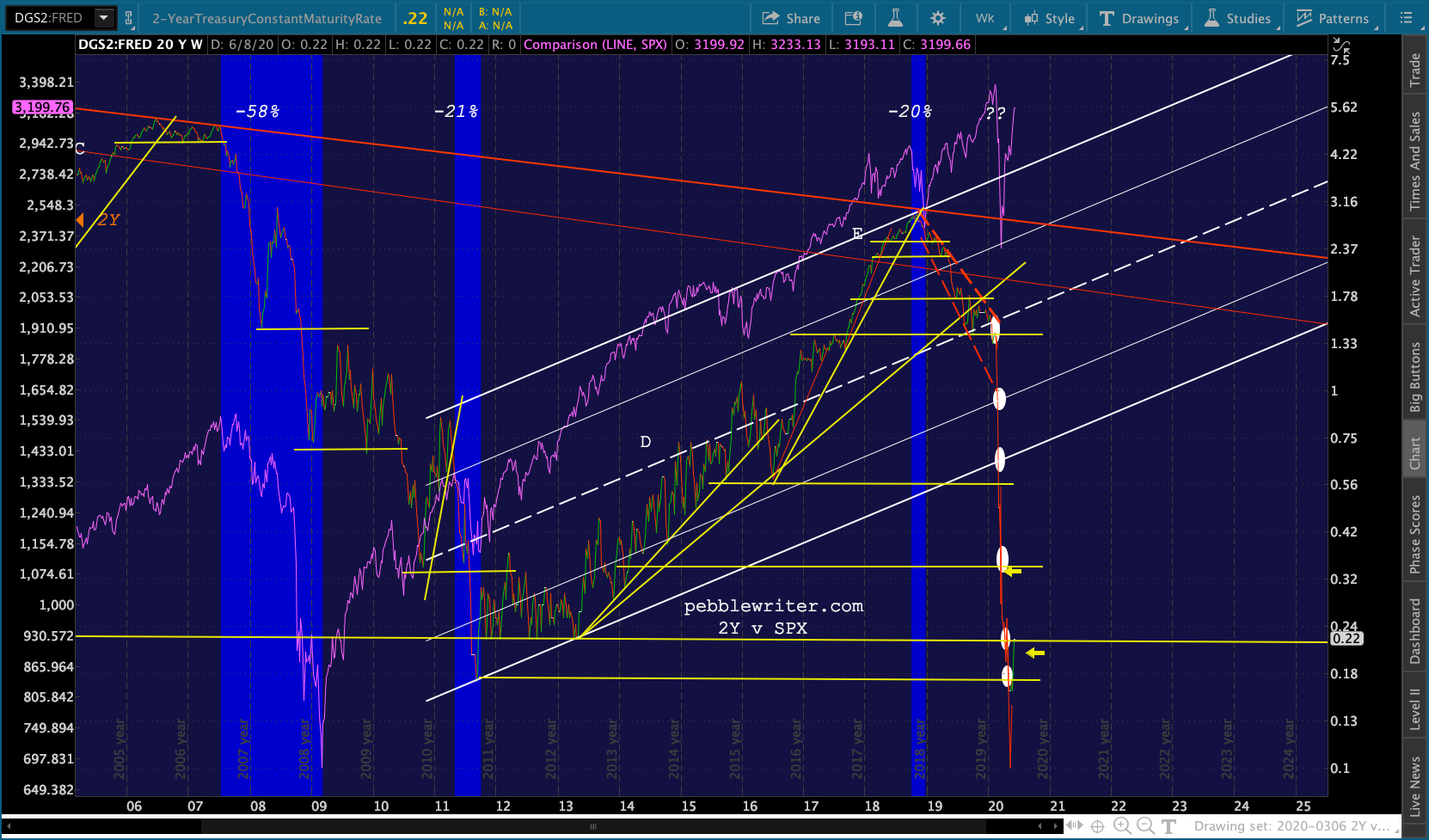

The 2Y has rebounded from May’s 0.10% intraday lows but has failed to retake the 0.22% resistance.

The 2Y has rebounded from May’s 0.10% intraday lows but has failed to retake the 0.22% resistance.

Higher rates might be consistent with increased economic activity. But, the one thing we know about the Fed is that they absolutely will not let interest rates rise substantially – not with the amount of debt that’s been taken on over the past few months. Given the sorry state of affairs with state and local government budgets, this problem will only get worse.

Higher rates might be consistent with increased economic activity. But, the one thing we know about the Fed is that they absolutely will not let interest rates rise substantially – not with the amount of debt that’s been taken on over the past few months. Given the sorry state of affairs with state and local government budgets, this problem will only get worse.

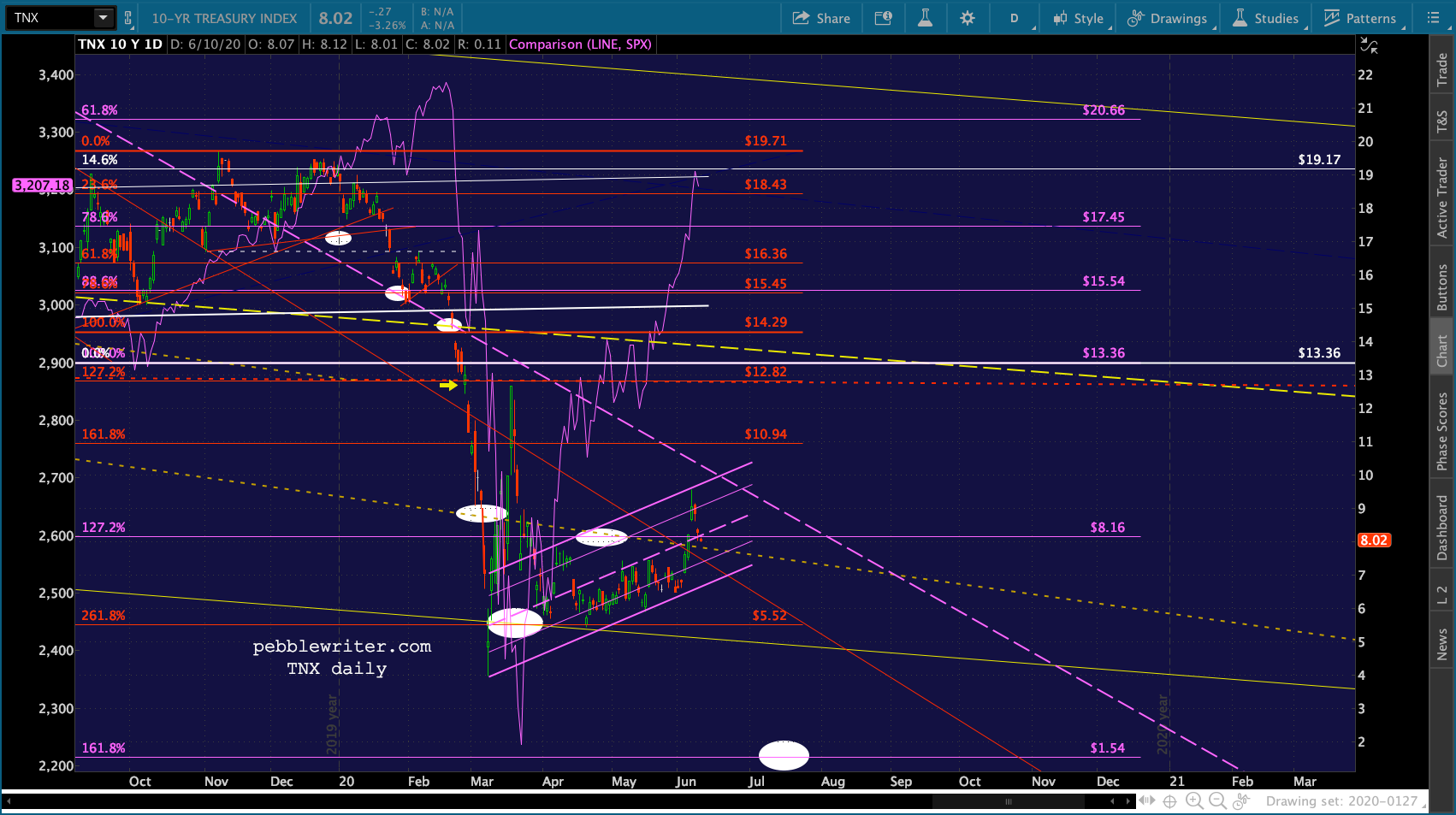

My charts still call for much lower rates which would presumably be driven by another equity shock rather than FOMC action. But, I would not put it past the Fed to do the math and see that negative rates will be required at some point – just to keep the house of cards from collapsing.

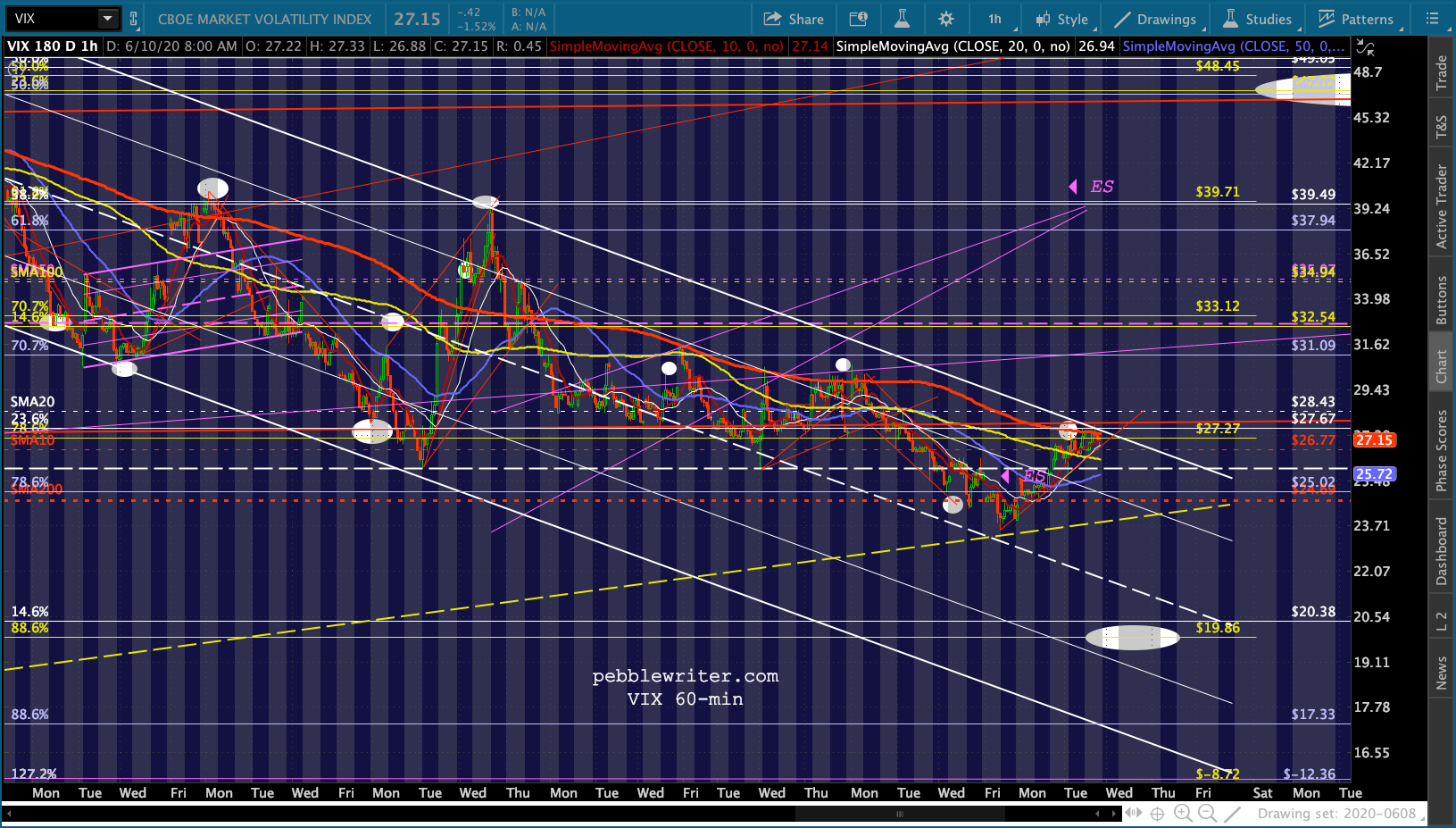

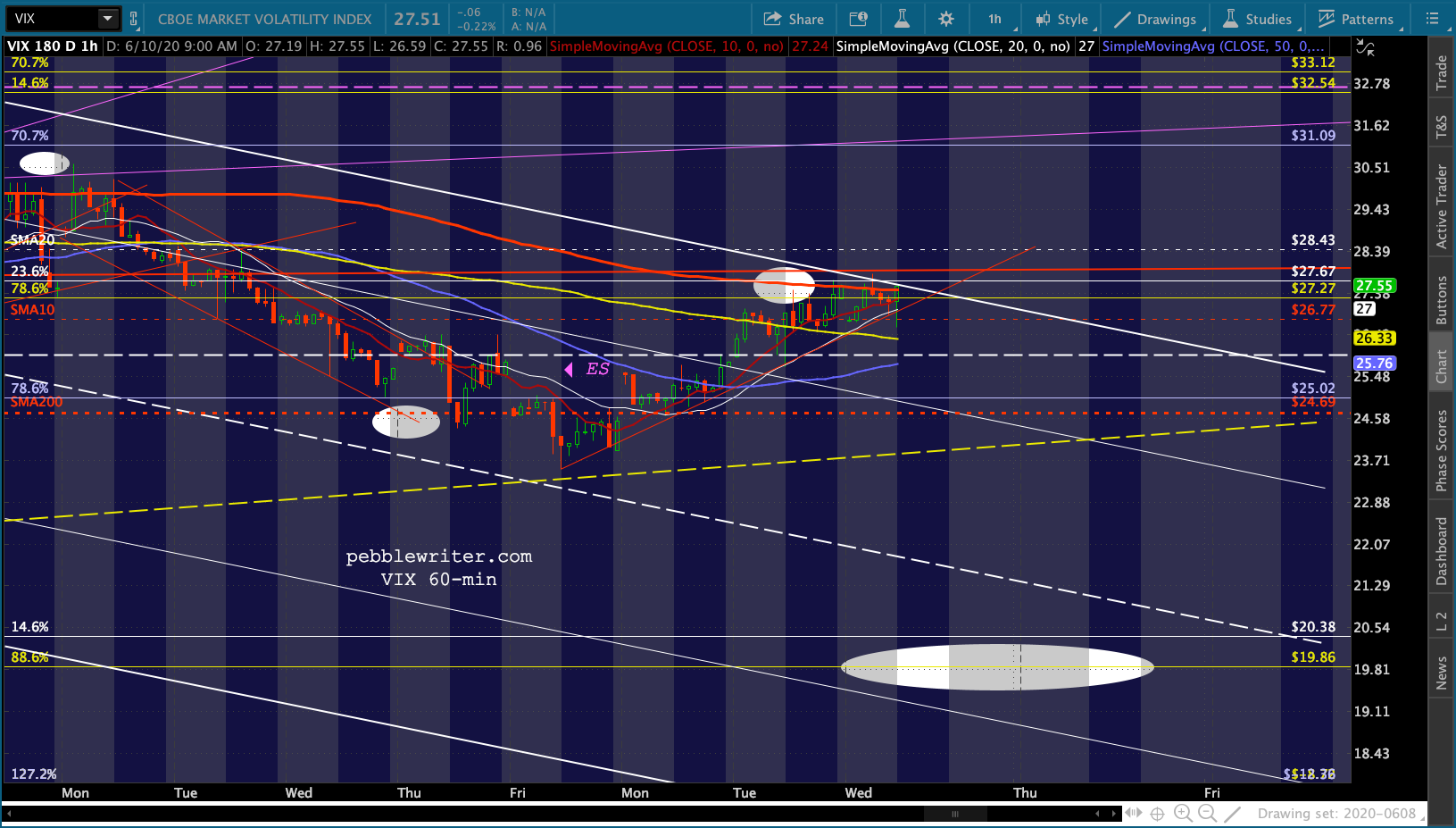

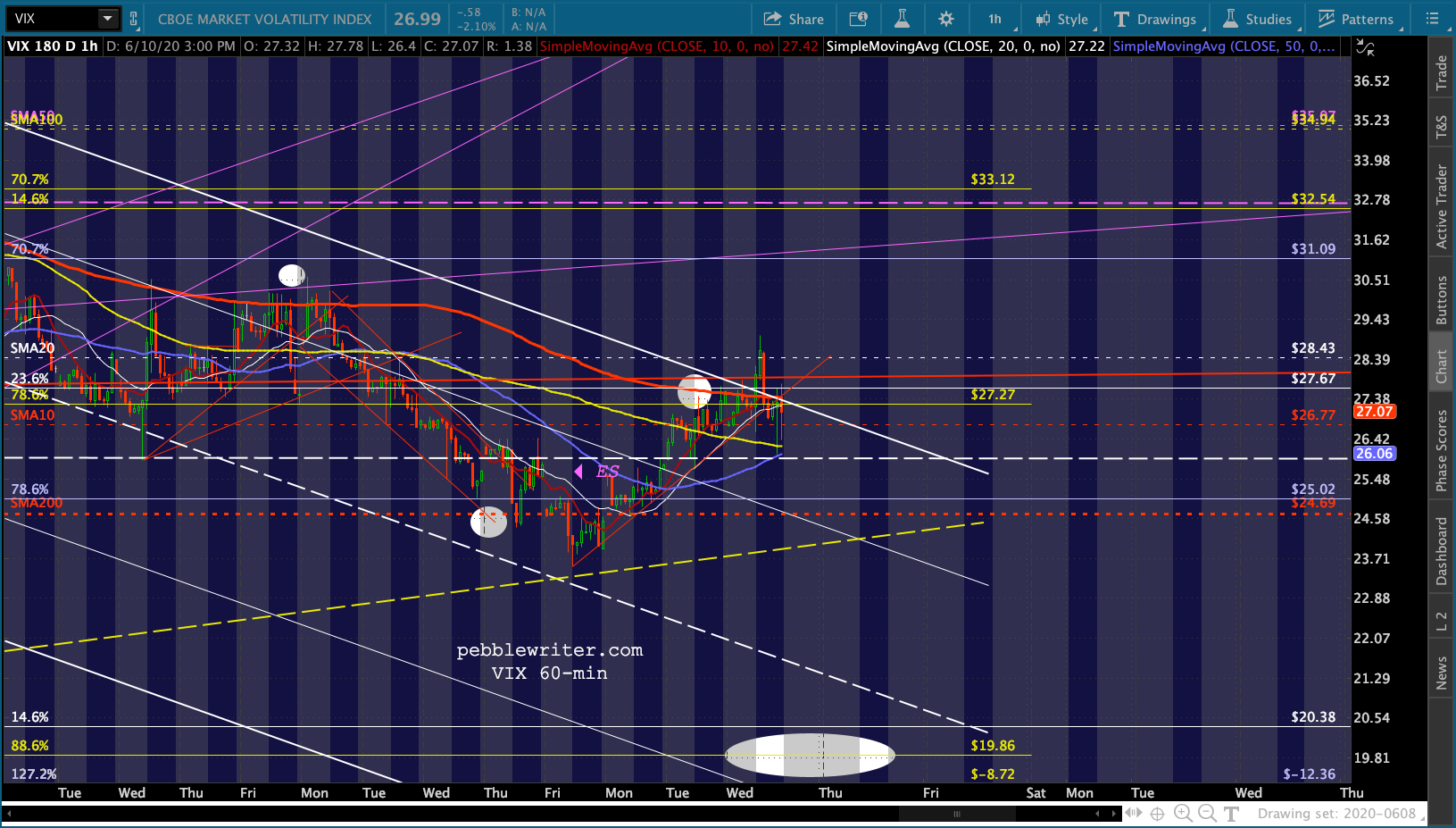

Just this morning, CNBC reported that two St. Louis Fed economists have put out additional research suggesting negative rates are in our future – something that would have been unthinkable before the Fed came unglued in March. In terms of managing the rally/breakdown, the usual suspects are in play. VIX will either break out of the falling white channel or break down below the little red TL, the SMA200 and, ultimately, the larger yellow TL.

In terms of managing the rally/breakdown, the usual suspects are in play. VIX will either break out of the falling white channel or break down below the little red TL, the SMA200 and, ultimately, the larger yellow TL.

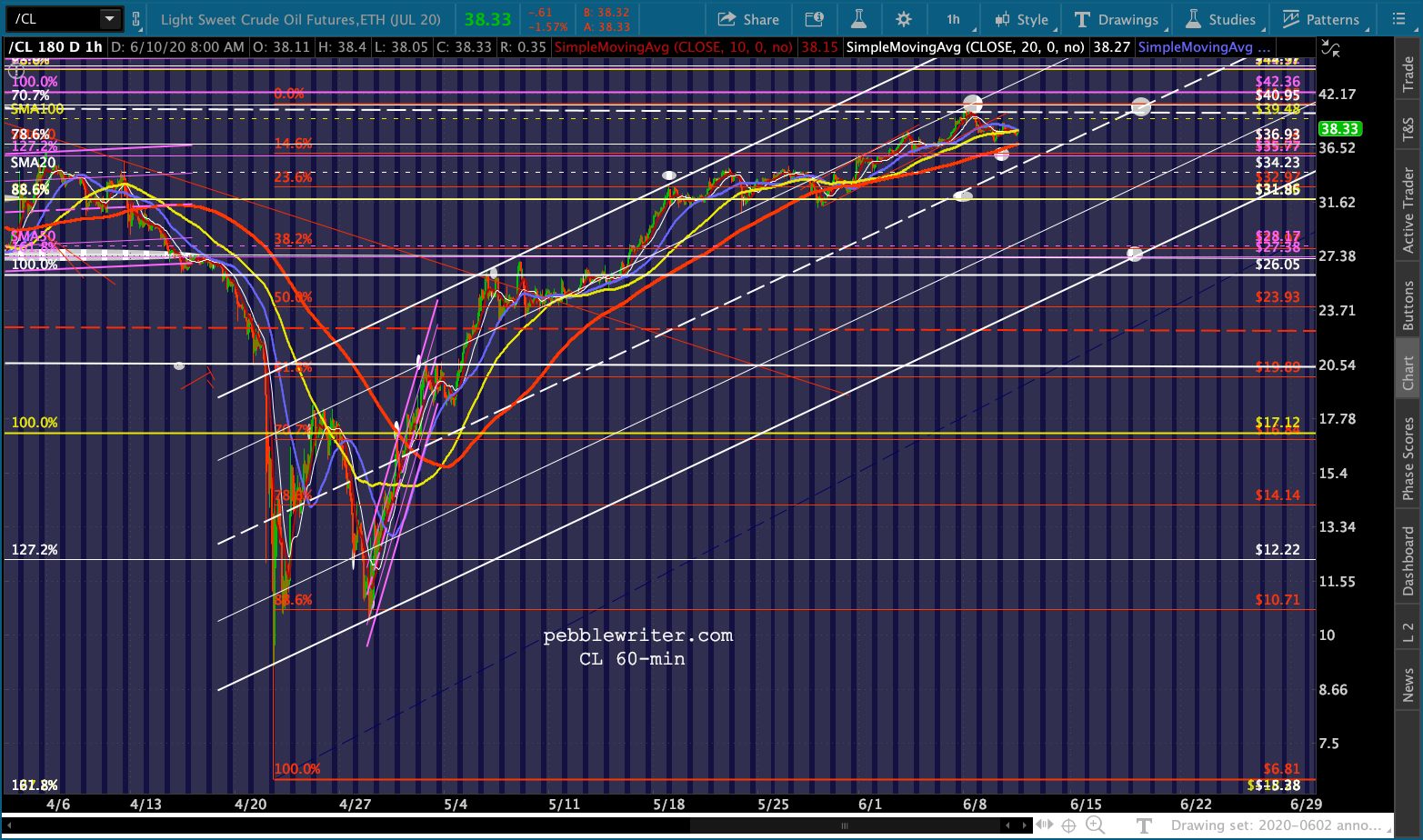

And, though IMO CL was a good short at 40.44 on Jun 7 (close enough to the gap close target at 41.05) it would shock no one if it remained in the current 37-41 range for a while longer, dropping enough in the after hours so that it has room to rally once stocks start trading.

And, though IMO CL was a good short at 40.44 on Jun 7 (close enough to the gap close target at 41.05) it would shock no one if it remained in the current 37-41 range for a while longer, dropping enough in the after hours so that it has room to rally once stocks start trading.

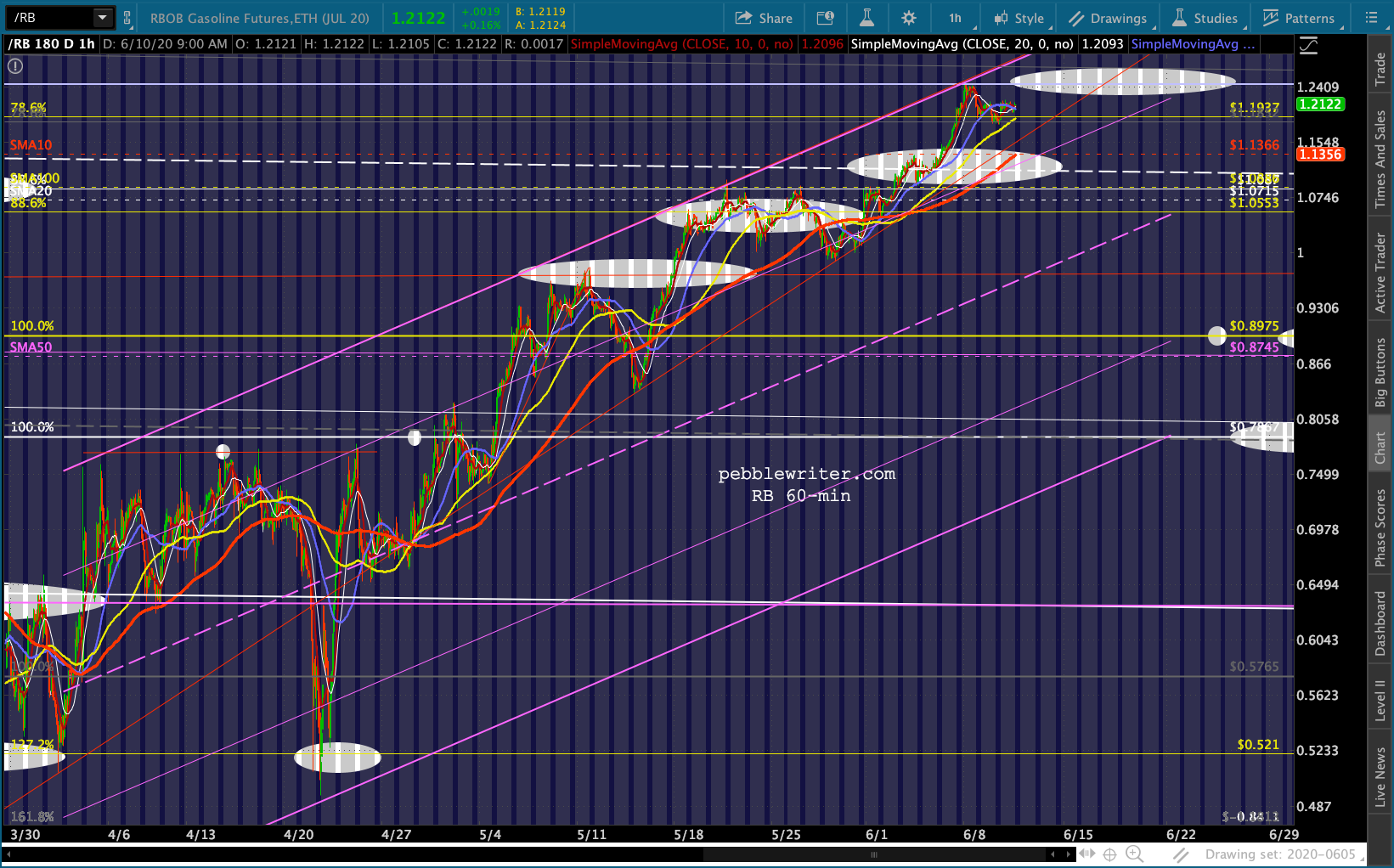

Ditto for RB, which reached 1.2443 on Jun 7 vs our 1.245 target. At some point, the rising wedge will break down and flesh out at least part of the channel below.

Ditto for RB, which reached 1.2443 on Jun 7 vs our 1.245 target. At some point, the rising wedge will break down and flesh out at least part of the channel below. UPDATE: 2:15 PM

UPDATE: 2:15 PM

Waiting on the press conference, but no real surprises in the statement or accompanying charts which can be found HERE.

Note that 10Y yields are continuing to slump…

Note that 10Y yields are continuing to slump… …contributing to a sharp drop in the 2s10s.

…contributing to a sharp drop in the 2s10s. more after Powell’s press conference…

more after Powell’s press conference…

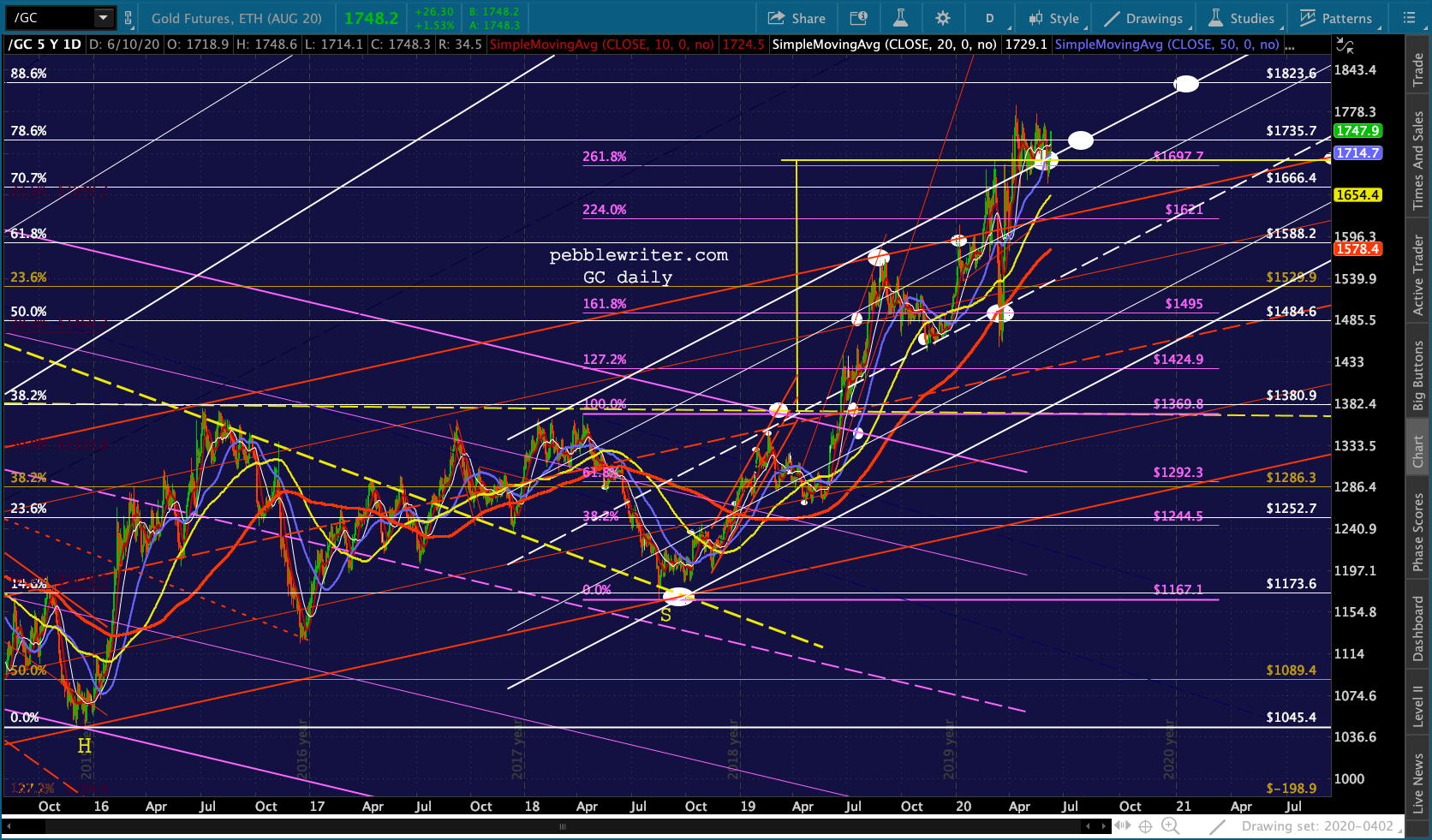

Gold is catching a bid today, but needs to break 1549 in order to have a crack at our 1823 target.

Gold is catching a bid today, but needs to break 1549 in order to have a crack at our 1823 target.

UPDATE: 4:20 PM

UPDATE: 4:20 PM