March CPI came in at 0.4% MoM for both headline and core (versus 0.3% expectations for both), hotter than expected for the second month in a row. YoY headline registered at 3.5% versus expectations of 3.4% and 3.2% in February and core came in at 3.8% (unchanged from February) versus expectations of 3.7%.

As we expected, inflation continues to be buttressed by strong YoY energy, shelter and services prices. Our gas vs inflation model remains on track.

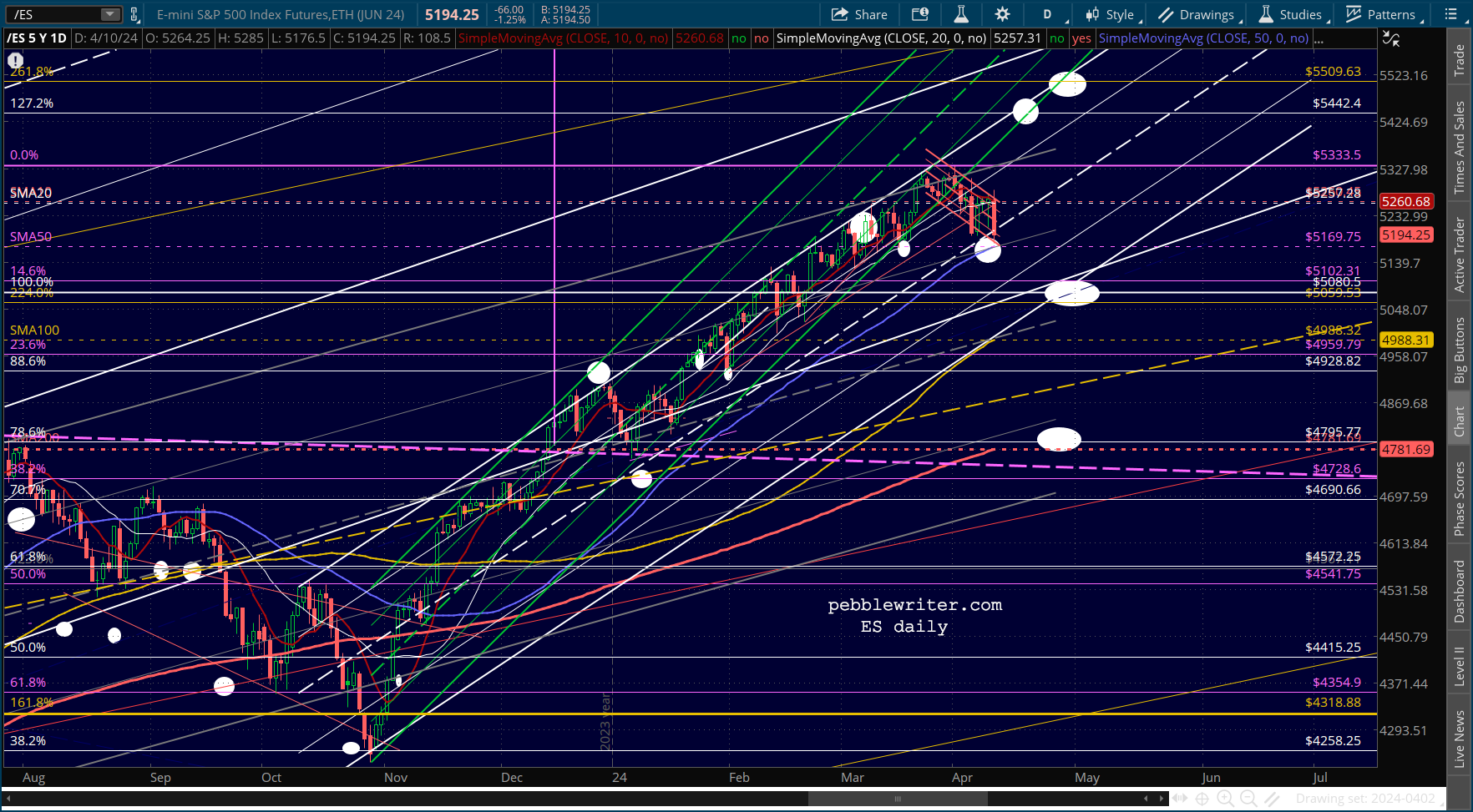

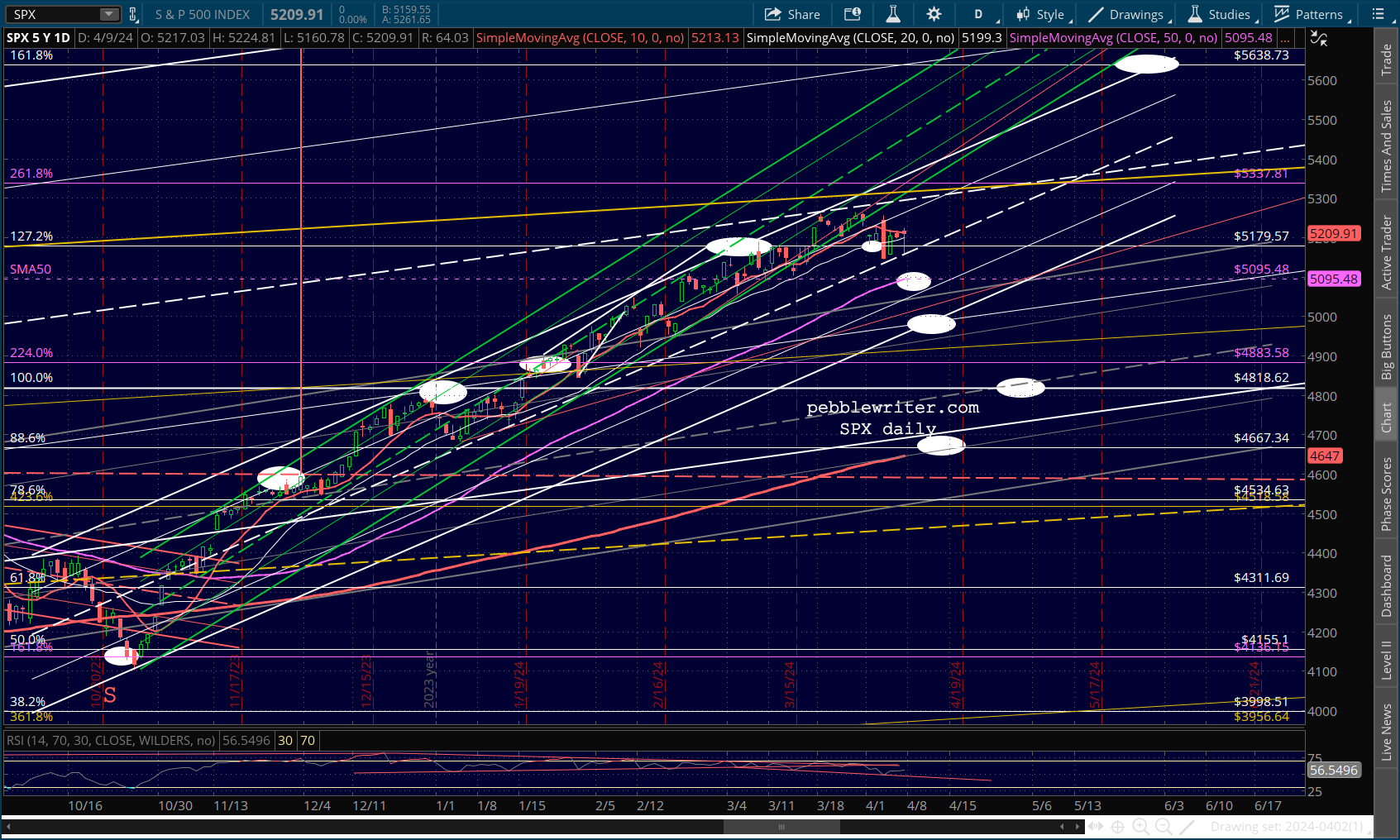

Futures came within a few points of our next downside target on the print.

Futures came within a few points of our next downside target on the print.

And, algos are finally recognizing that a string of 0.4% monthly prints can turn into an annual print much closer to 5% than 2%.

continued for members…

A bounce at SPX 5095 (ES 5170) would test not only the SMA50 but the rising white channel midline.

The BLS’ Table A shows how pervasive inflation has been in services, especially shelter, and energy.

The BLS’ Table A shows how pervasive inflation has been in services, especially shelter, and energy.

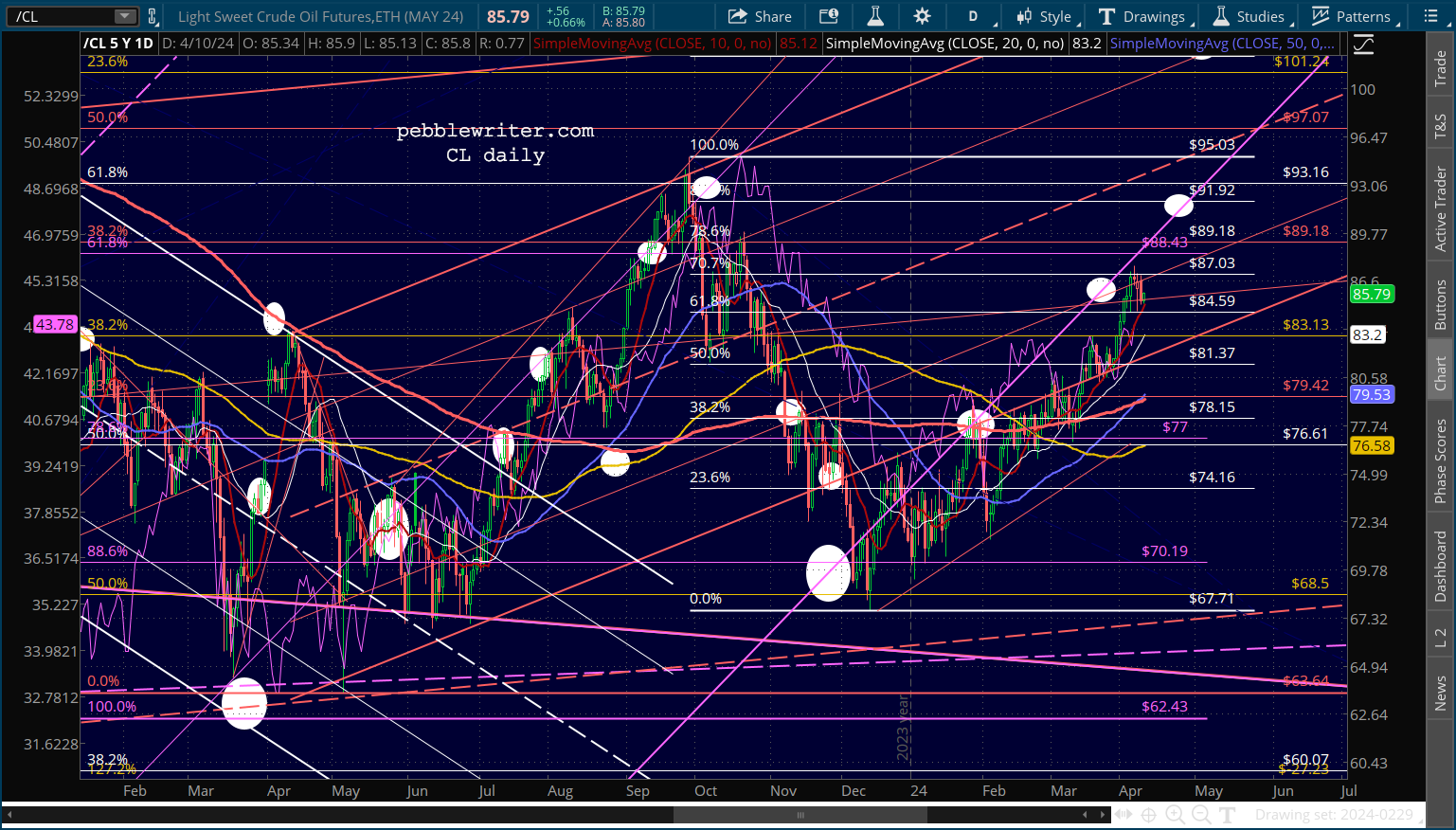

As we’ve discussed many times before, CPI will continue to disappoint as long as oil and gas prices continue to rise – setting up a major conflict between the Biden administration and OPEC+, which would love to see Trump back in office. The Israel-Hamas war complicated things, to say the least.

As we’ve discussed many times before, CPI will continue to disappoint as long as oil and gas prices continue to rise – setting up a major conflict between the Biden administration and OPEC+, which would love to see Trump back in office. The Israel-Hamas war complicated things, to say the least.

From an economic standpoint, the US needs a stronger DXY in order to reduce the cost of imports and, thus, inflation. We can see signs of this in the small drop in EURUSD and rise in USDJPY.

Note that USDJPY is topping 152 for the first time since April 1990.

Note that USDJPY is topping 152 for the first time since April 1990.

But, of course, this comes at a price: higher interest rates. Higher rates impair consumer and capital spending, which will help temper inflation. But, they are obviously not helpful for stock values. If the 10Y remains above 4.5%, those equity SMA50s are going to have a hard time holding.

But, of course, this comes at a price: higher interest rates. Higher rates impair consumer and capital spending, which will help temper inflation. But, they are obviously not helpful for stock values. If the 10Y remains above 4.5%, those equity SMA50s are going to have a hard time holding.

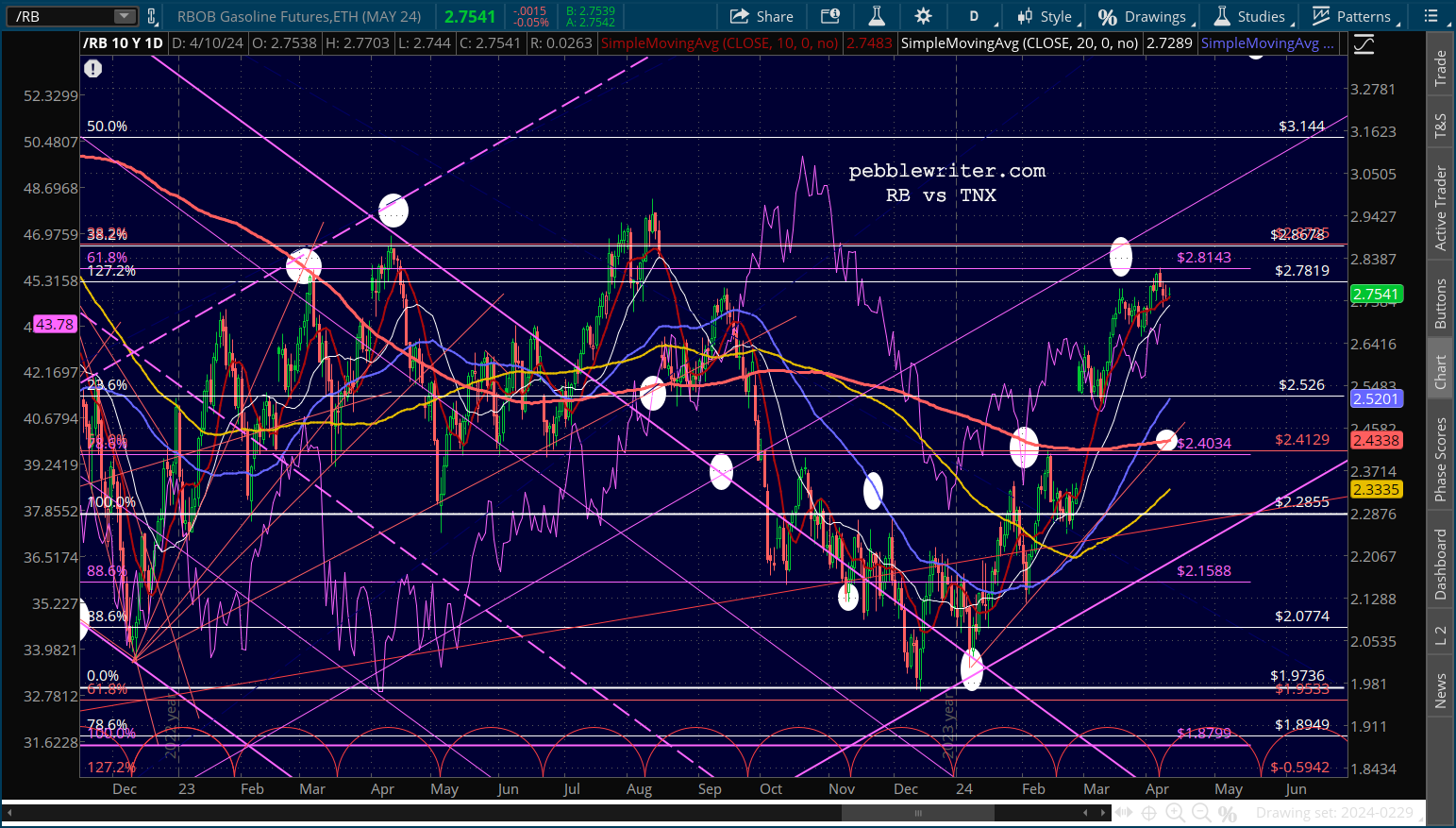

For now, oil and gas prices are fairly quiet.

For now, oil and gas prices are fairly quiet.

Stay tuned…

Stay tuned…