Today’s FOMC meeting is one of the most anticipated and consequential in years. It’s difficult to overstate its importance in terms of economic impact and, perhaps more importantly, Fed credibility.

Yes, we care about whether the Fed hikes 50 or 75 basis points – though either is unlikely to put a dent in inflation. The bigger question is what the Fed does with its $9 trillion balance sheet.

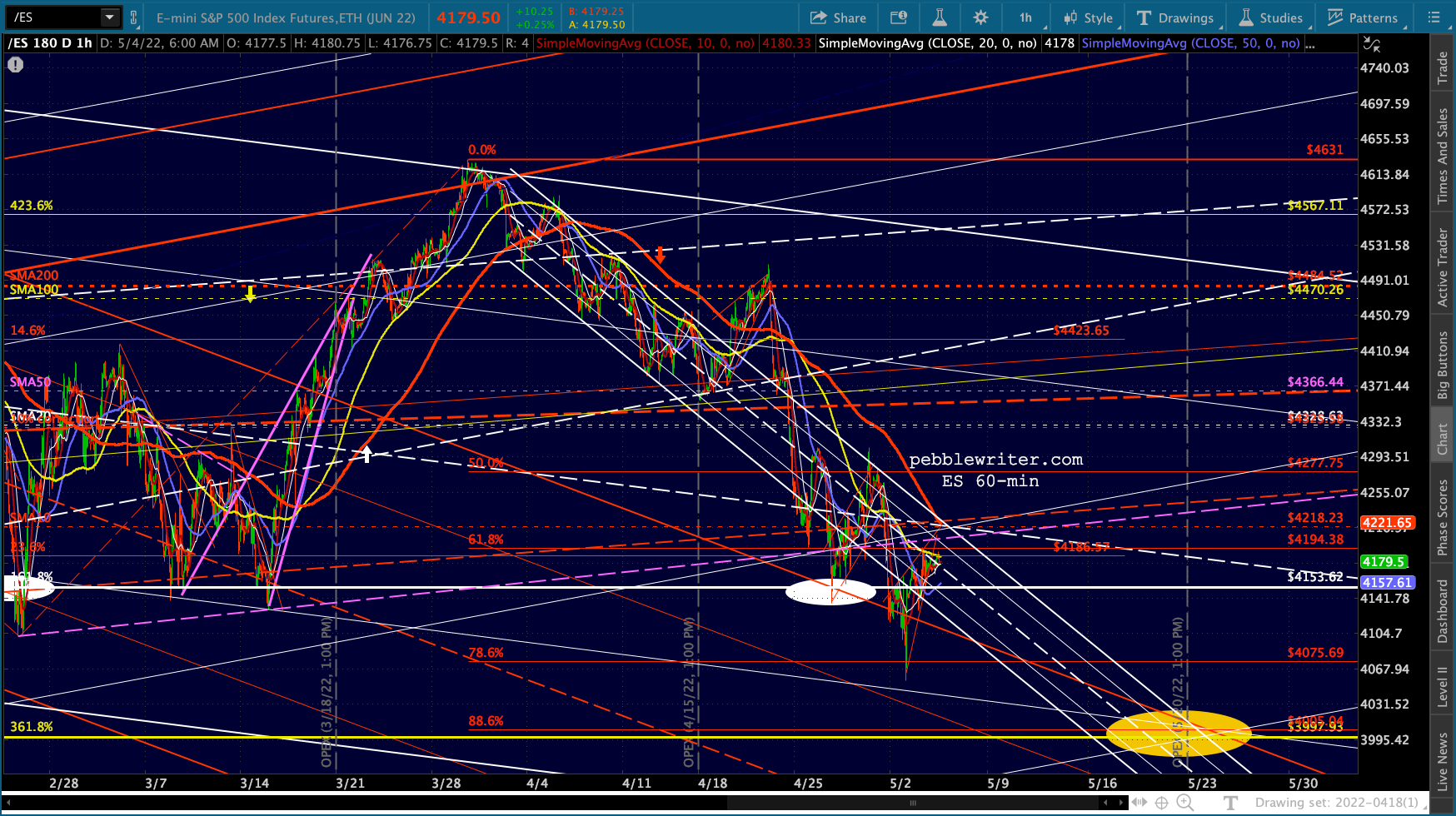

Futures are up modestly.

Futures are up modestly.

continued for members…

continued for members…

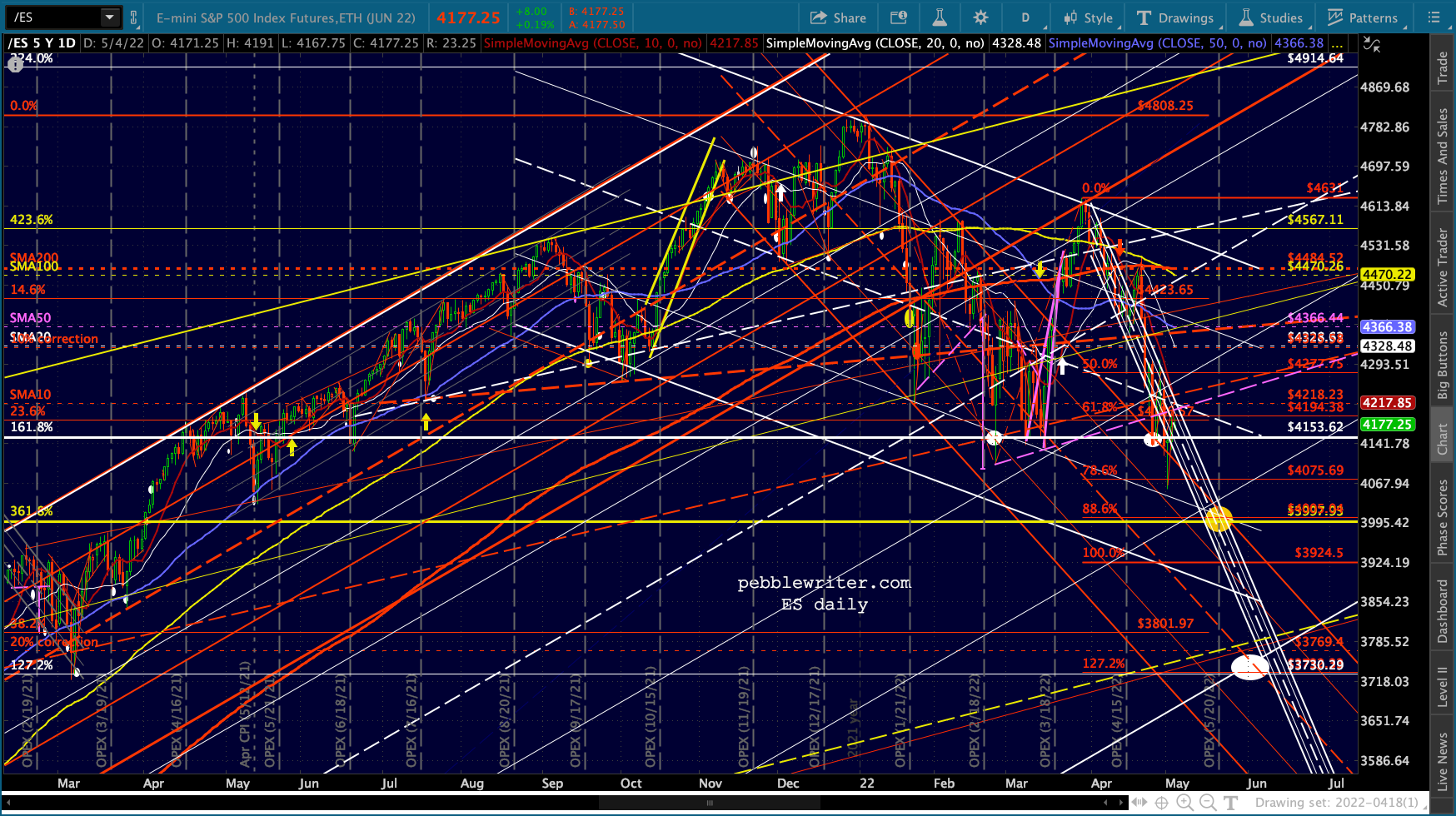

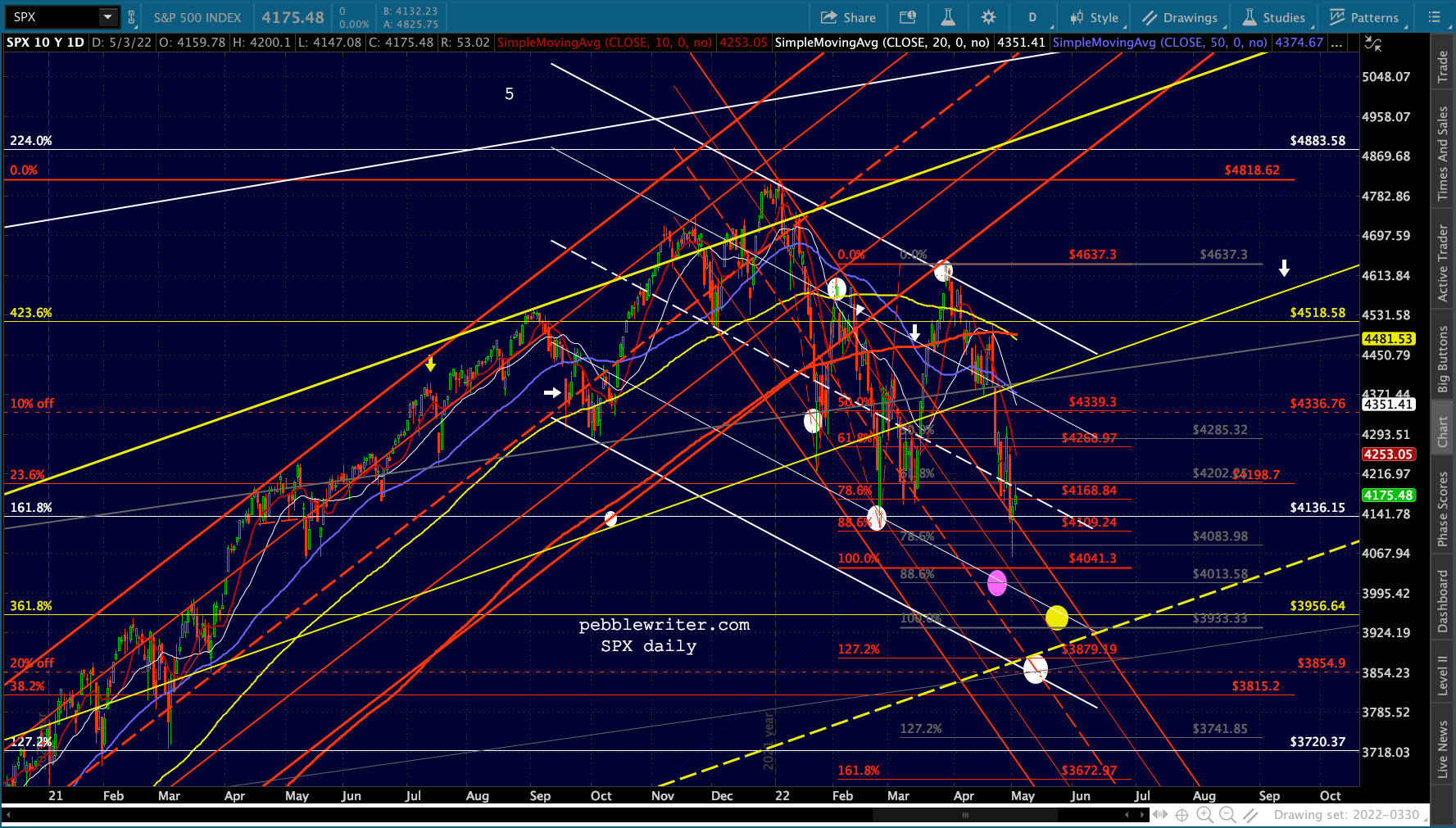

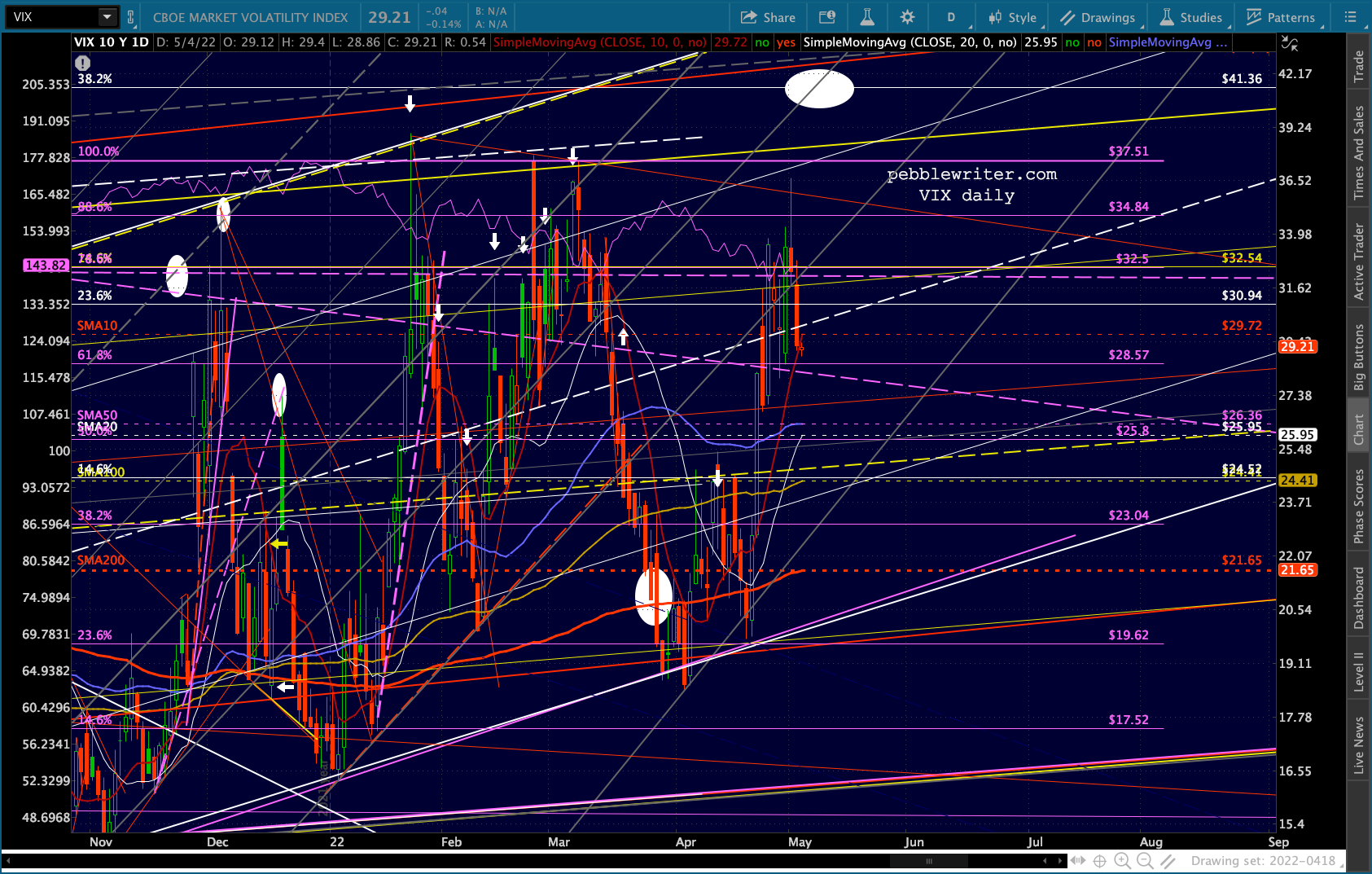

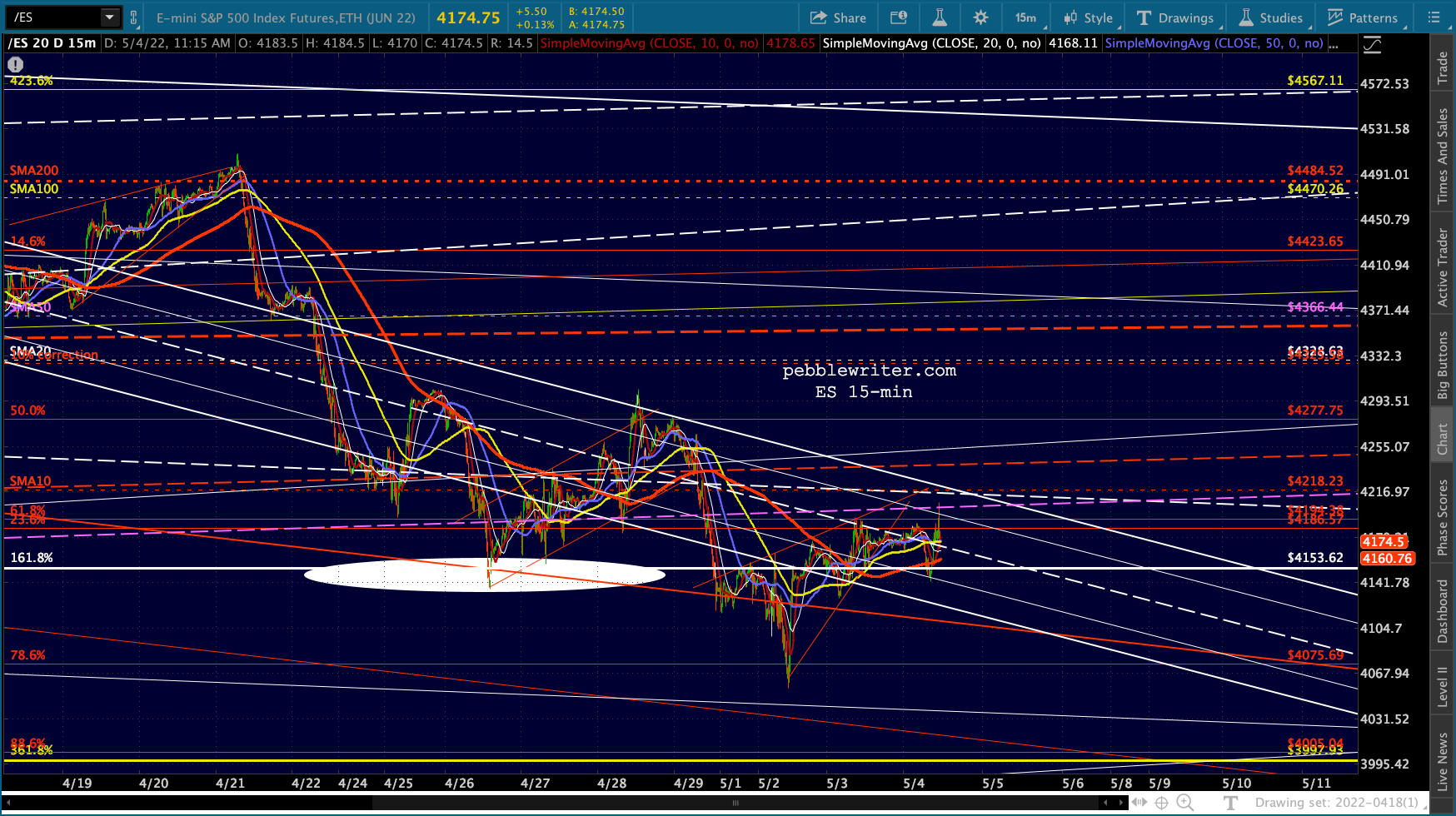

The equity picture remains unchanged, with scads of downside targets beginning with a backtest of the 3.618 extension at ES 3997 and SPX 3956.

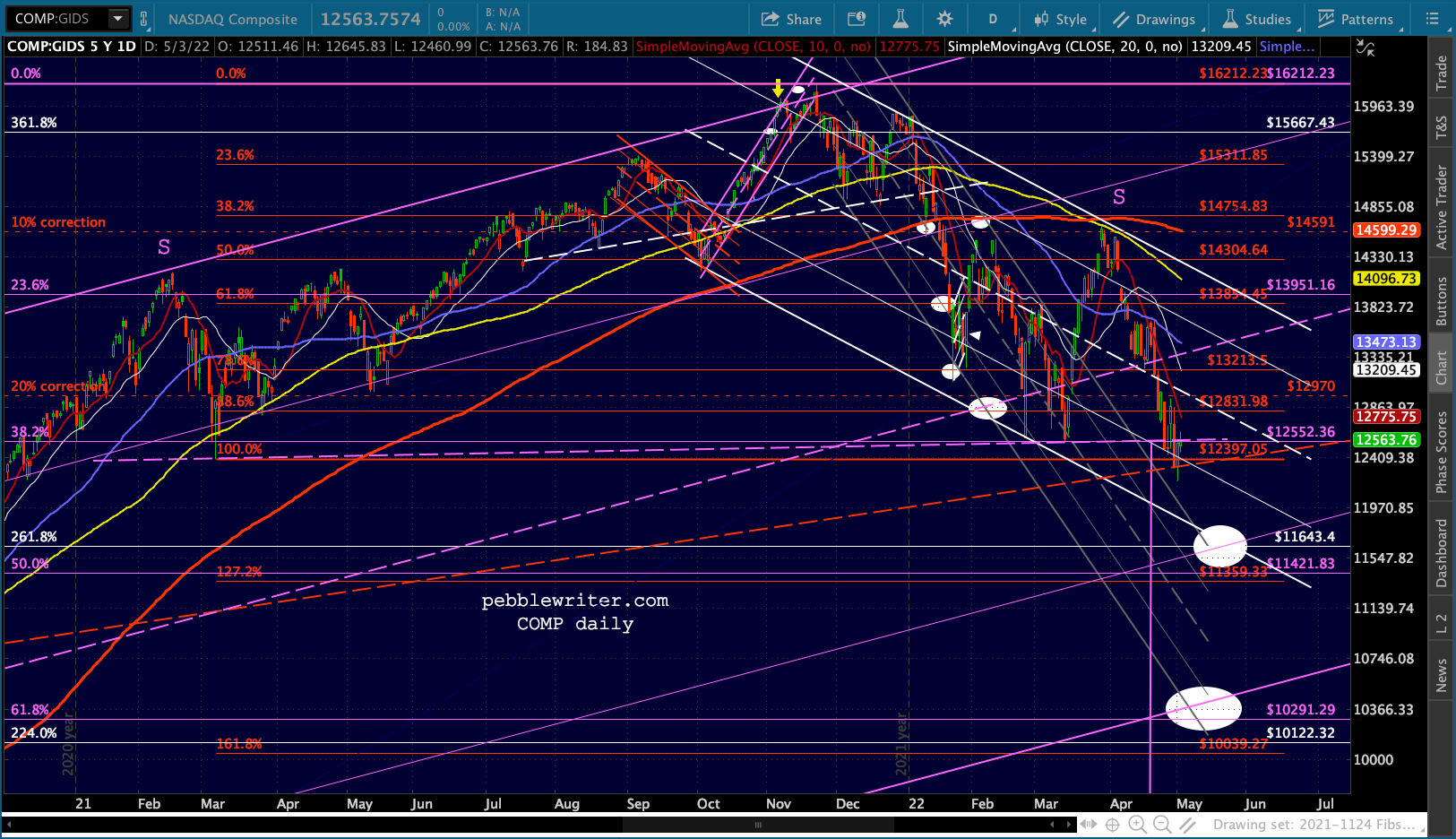

COMP’s clear, completed and backtested H&S Pattern suggests the downside could be much more severe.

COMP’s clear, completed and backtested H&S Pattern suggests the downside could be much more severe.

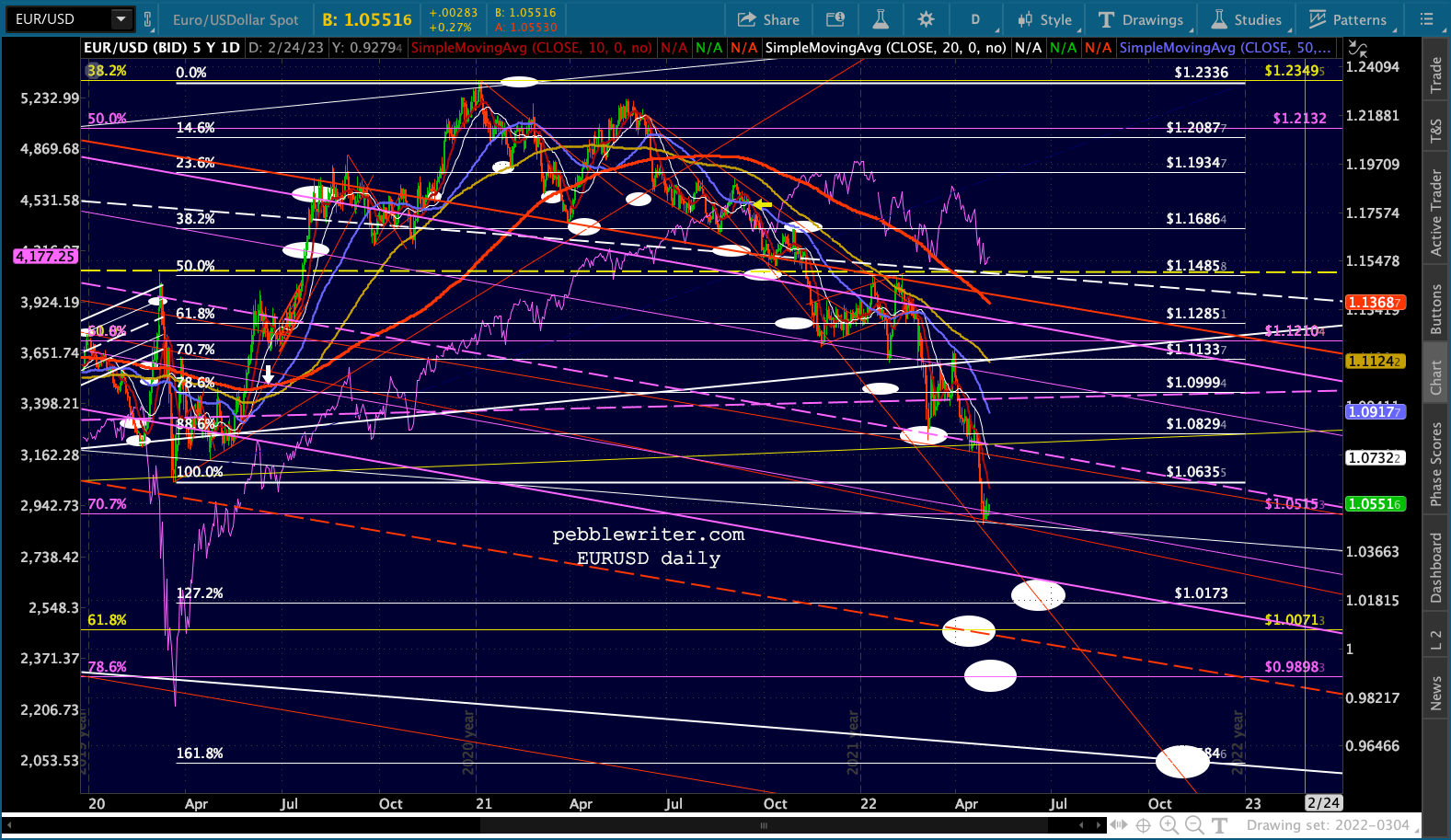

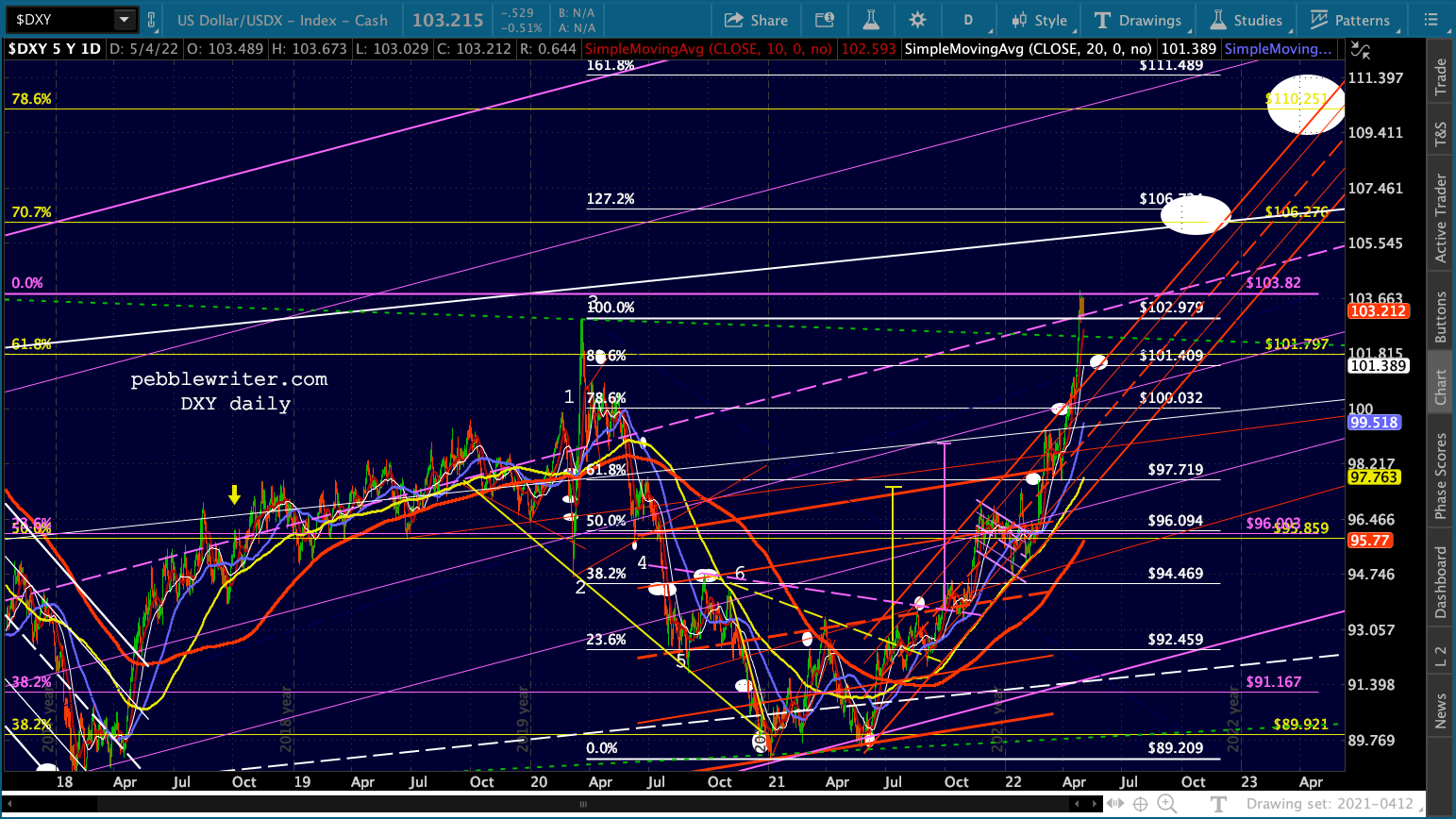

The currency picture still centers around a rising USD and DXY. A rate hike should do nothing to reverse this trend.

The currency picture still centers around a rising USD and DXY. A rate hike should do nothing to reverse this trend.

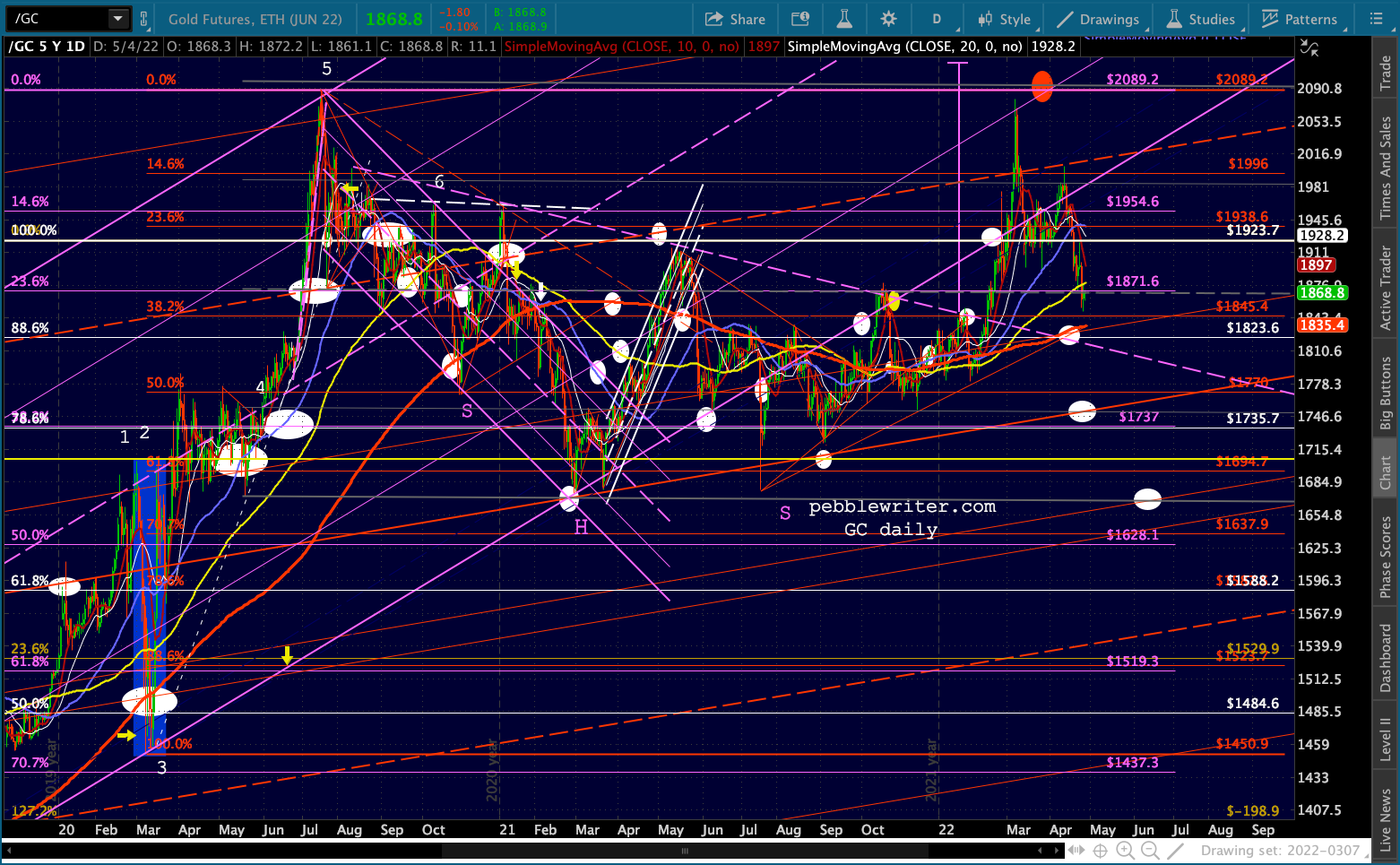

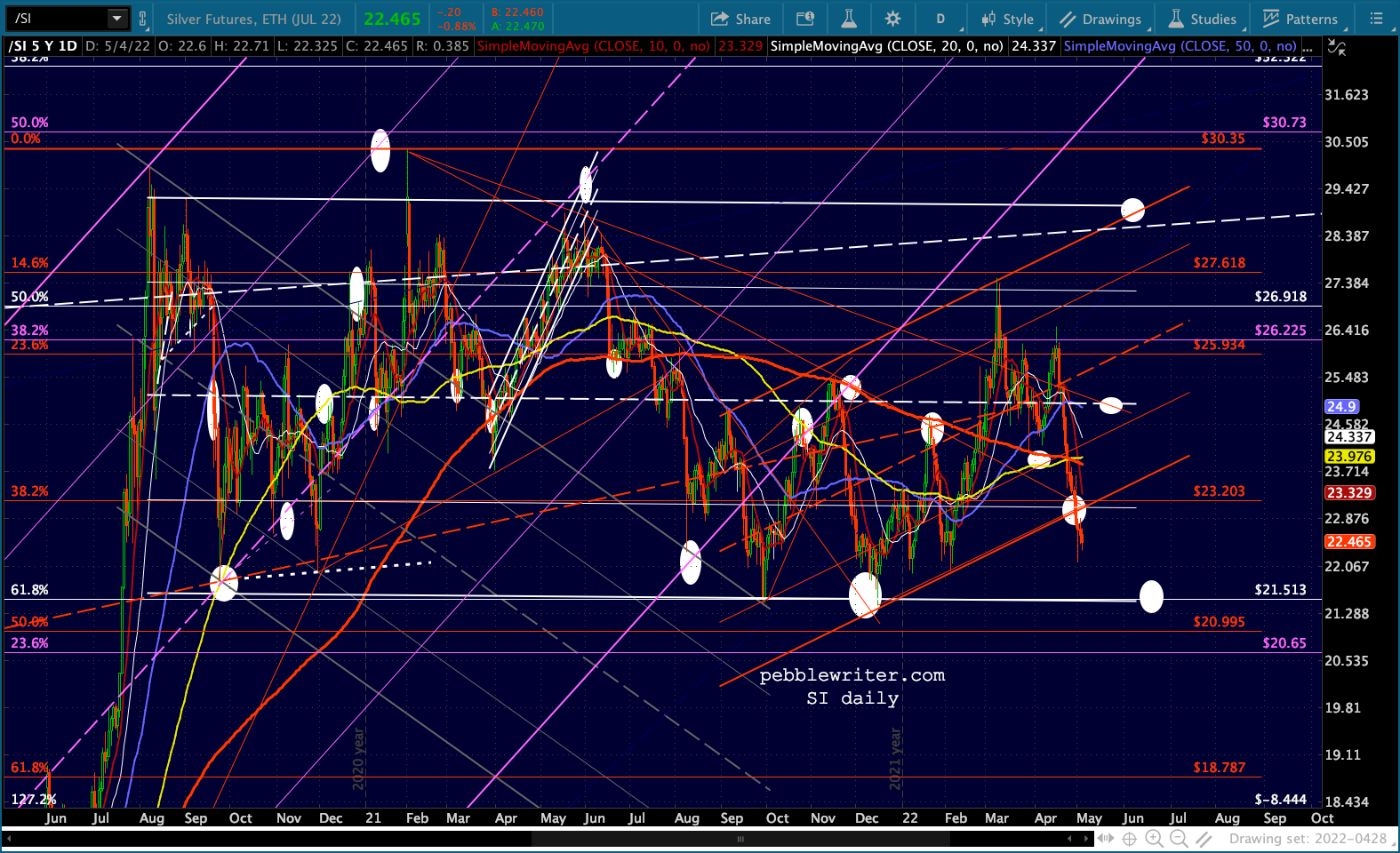

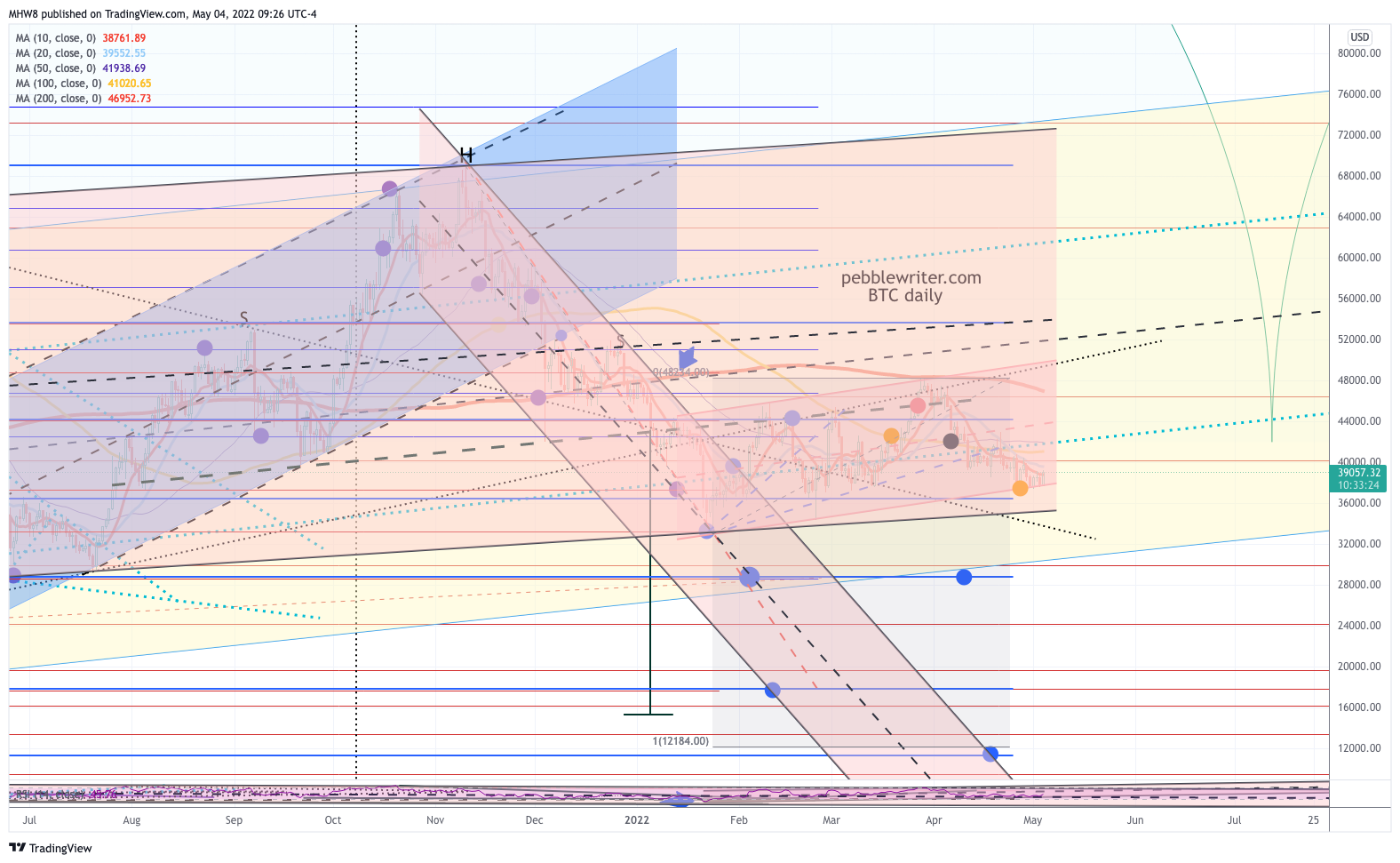

Gold, silver and bitcoin are still in a holding pattern with bearish leanings.

Gold, silver and bitcoin are still in a holding pattern with bearish leanings.

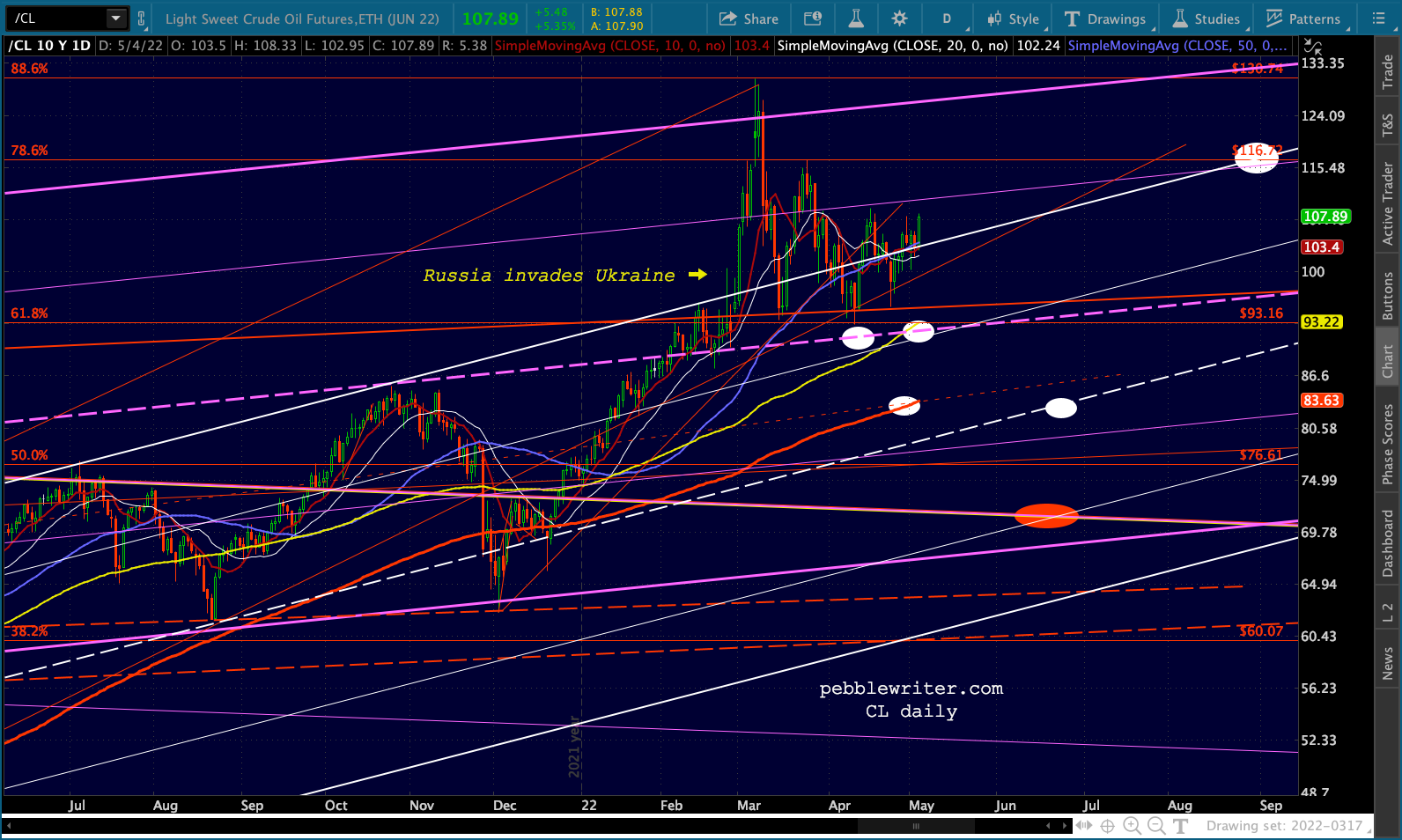

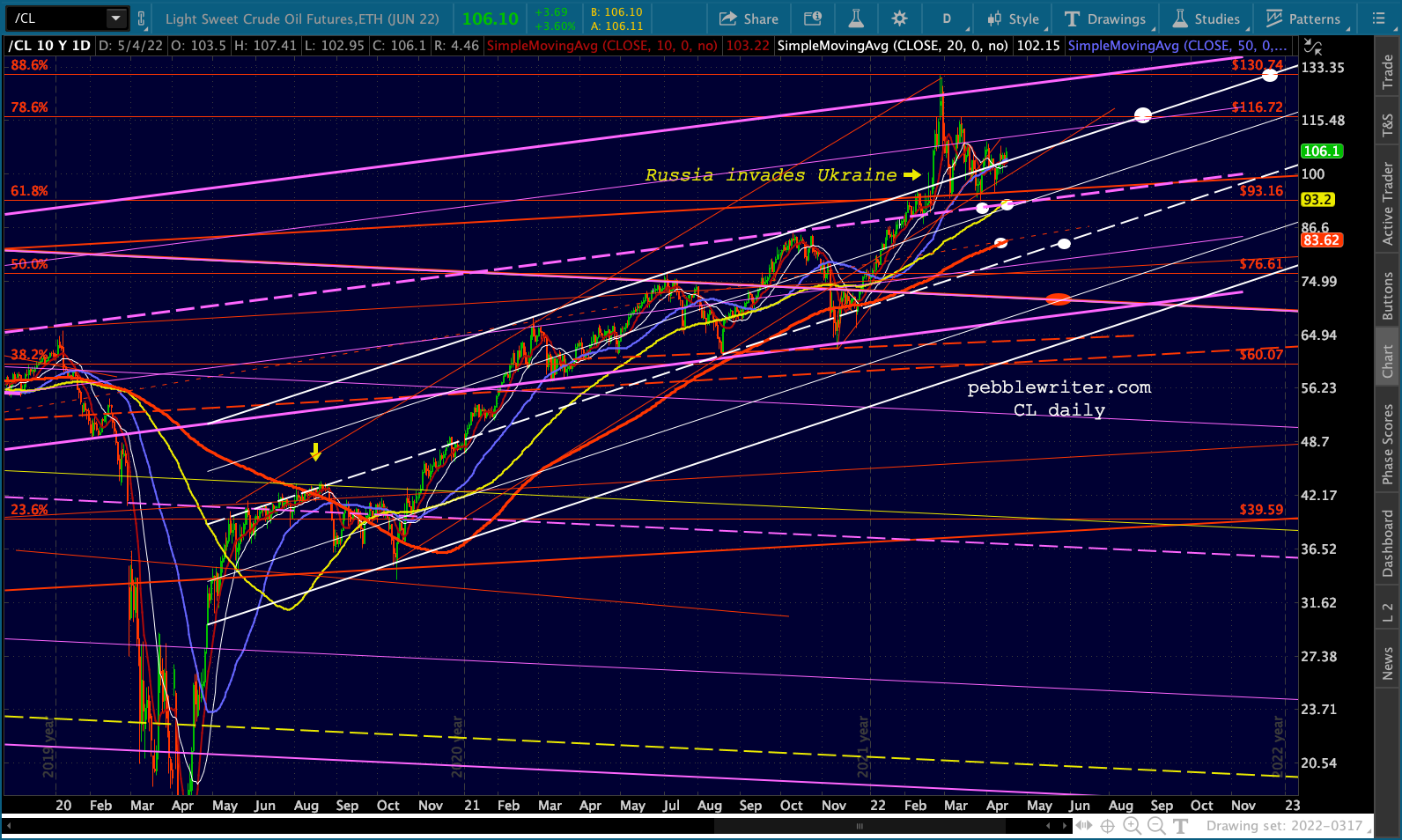

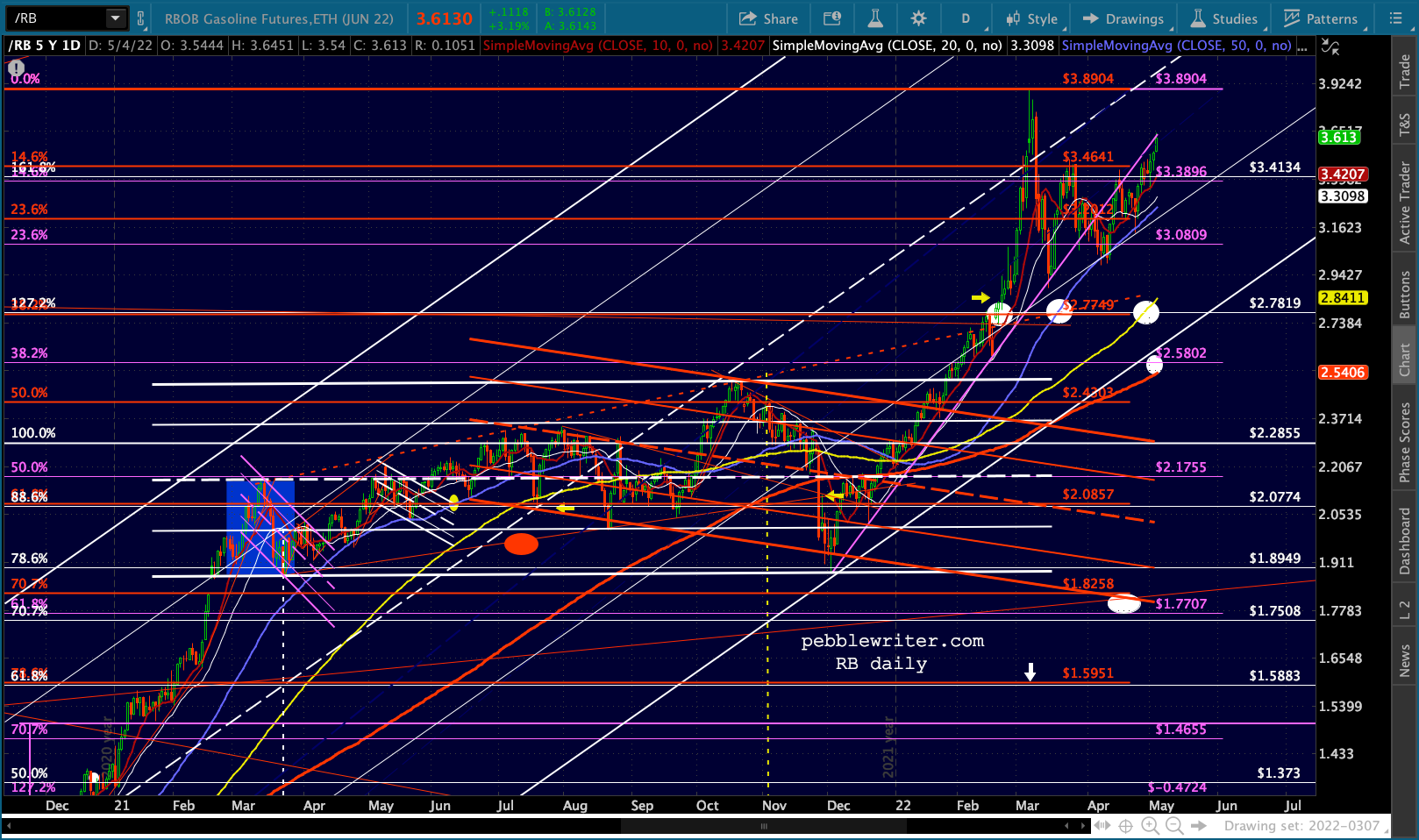

Saw an interesting news flash this morning that CIA director Bill Burns recently made an unscheduled trip to Saudi Arabia to meet with Crown Prince MBS – presumably to mend ties but obviously to coax/strong arm MBS into lowering oil prices. From the looks of the CL and RB charts, he was not successful.

Saw an interesting news flash this morning that CIA director Bill Burns recently made an unscheduled trip to Saudi Arabia to meet with Crown Prince MBS – presumably to mend ties but obviously to coax/strong arm MBS into lowering oil prices. From the looks of the CL and RB charts, he was not successful.

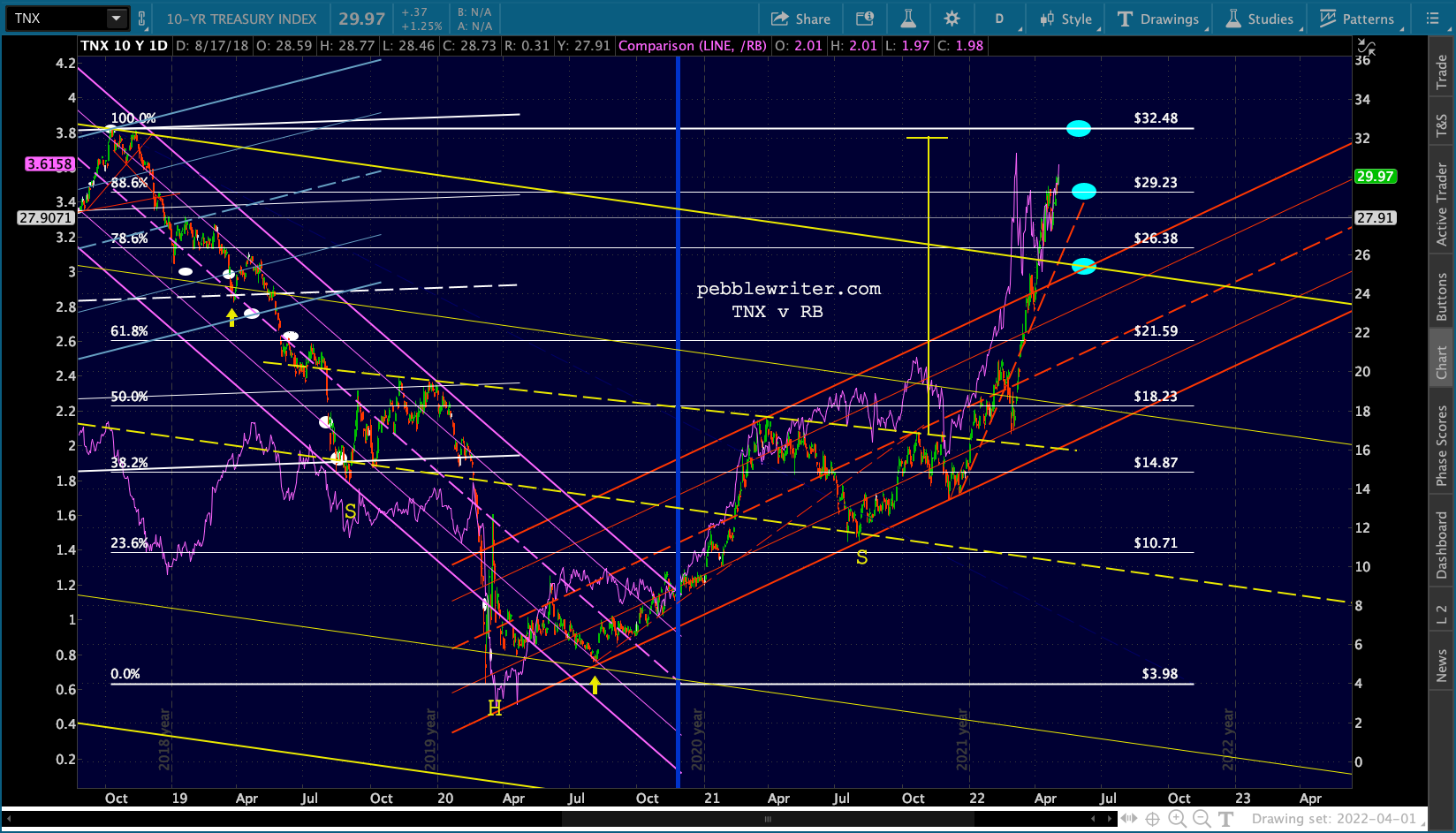

That leaves us with a 10Y which is now hovering right at 3% with our IH&S target at 3.20-3.25%.

That leaves us with a 10Y which is now hovering right at 3% with our IH&S target at 3.20-3.25%.

Before Russia invaded Ukraine, I reasoned that oil prices would fall or at least level off which would mitigate rising inflation. As long as Vladimir Putin is alive and kicking, it’s hard to envision that happening any time soon.

Before Russia invaded Ukraine, I reasoned that oil prices would fall or at least level off which would mitigate rising inflation. As long as Vladimir Putin is alive and kicking, it’s hard to envision that happening any time soon.

Without a viable means to halt inflation, and no longer able to suppress interest rates via massive monthly purchases, the Fed is left with the distasteful option of allowing a recession and/or market correction to do what’s necessary.

Stay tuned…

UPDATE: 2:00 PM

So, 50 bps and very timid QT starting in June. Not much movement in the bond market…

…but the pre-FOMC ramp job is faltering.

…but the pre-FOMC ramp job is faltering.

CL is up over 5%!

CL is up over 5%!