It clearly didn’t matter to stocks when 10Y futures broke down last month from the appreciation channel dating back to May 2018.  ZN’s decline was gentle, contained. And, weren’t higher rates a sign that the economy was recovering and inflation picking up as desired? Powell repeats this mantra every chance he gets. Besides, stocks have dutifully continued their “reflation” meltup.

ZN’s decline was gentle, contained. And, weren’t higher rates a sign that the economy was recovering and inflation picking up as desired? Powell repeats this mantra every chance he gets. Besides, stocks have dutifully continued their “reflation” meltup.

But, in the back of everyone’s mind: at what point would higher interest rates become a problem? With the national debt closing in on $30 trillion, higher rates would seem to be an important issue. Future earnings obviously aren’t worth as much when discounted at a higher rate. What would happen if market forces took over and rates shot up, out of control?

While breakdowns are cause for caution, breakdowns from breakdowns are often cause for alarm. That’s where we are today. And, yes, it could be a big problem.

continued for members…

continued for members…

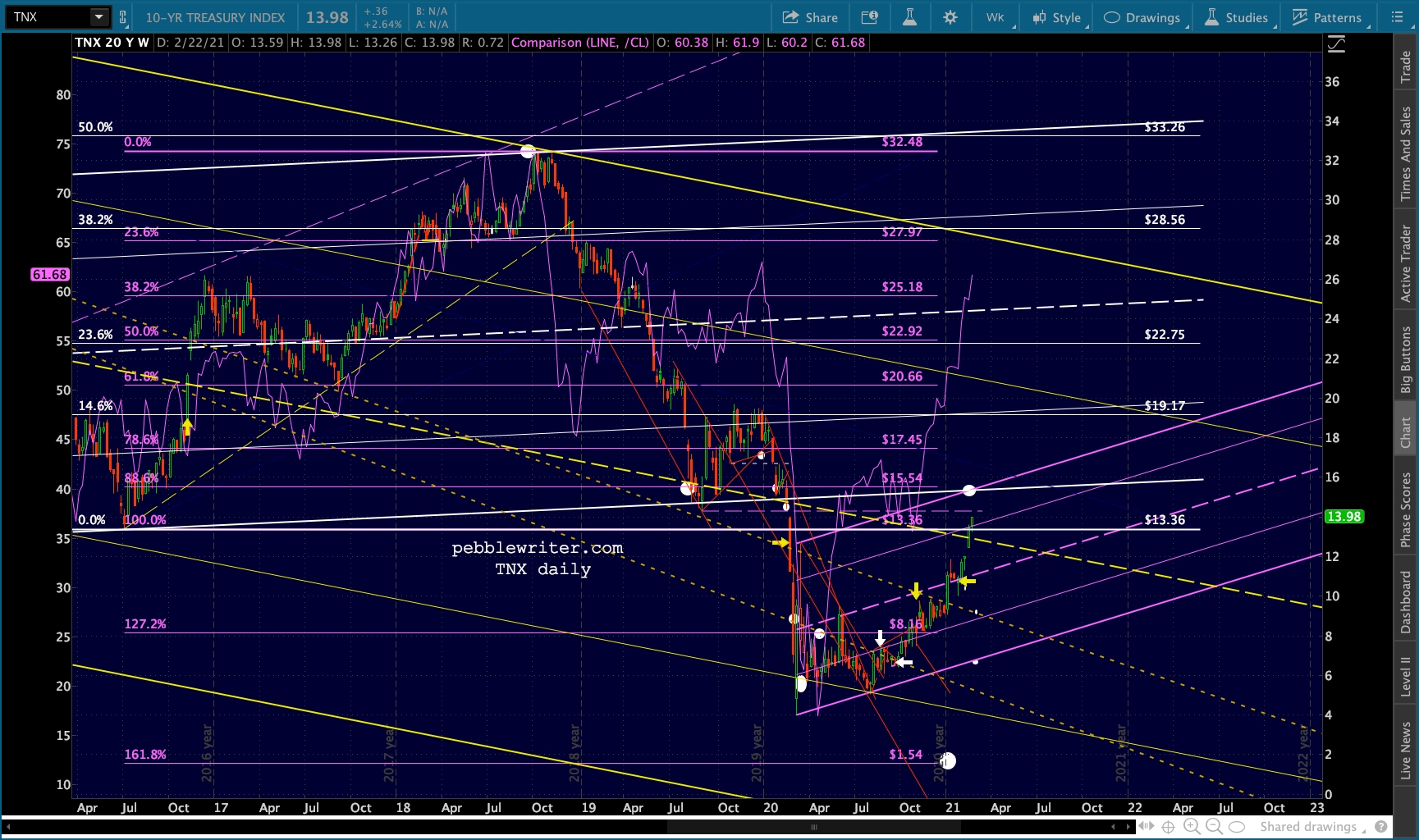

The bigger picture shows ZN likely to tag the rising white midline. Holding it will be critical. TNX’s version: note that the previous lows have been surpassed.

TNX’s version: note that the previous lows have been surpassed. While the falling yellow midline has been encroached on before, it’s important that it ultimately hold in order for rates not to get out of control.

While the falling yellow midline has been encroached on before, it’s important that it ultimately hold in order for rates not to get out of control.

ZN has also been a good predictor of gold prices.

ZN has also been a good predictor of gold prices.

And, the relationship is holding up this time as well.

And, the relationship is holding up this time as well.

BTC even managed a proper backtest of the last major Fib level, opening the door to the next upside target at the purple 3.618 extension at 62,977.

BTC even managed a proper backtest of the last major Fib level, opening the door to the next upside target at the purple 3.618 extension at 62,977.

Stocks might not be dinged too badly…

Stocks might not be dinged too badly…

…if the VIX smackdowns…

…if the VIX smackdowns…

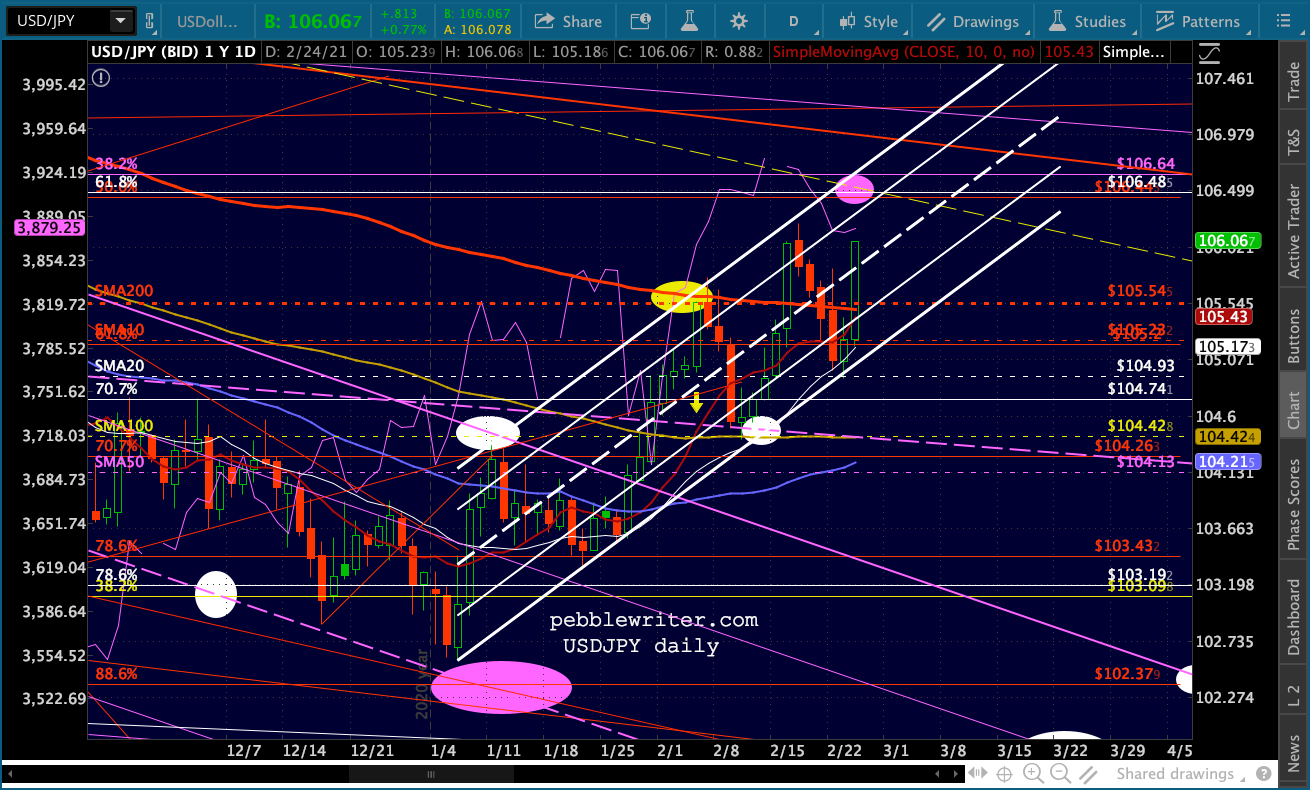

…and USDJPY ramps keep coming.

…and USDJPY ramps keep coming.

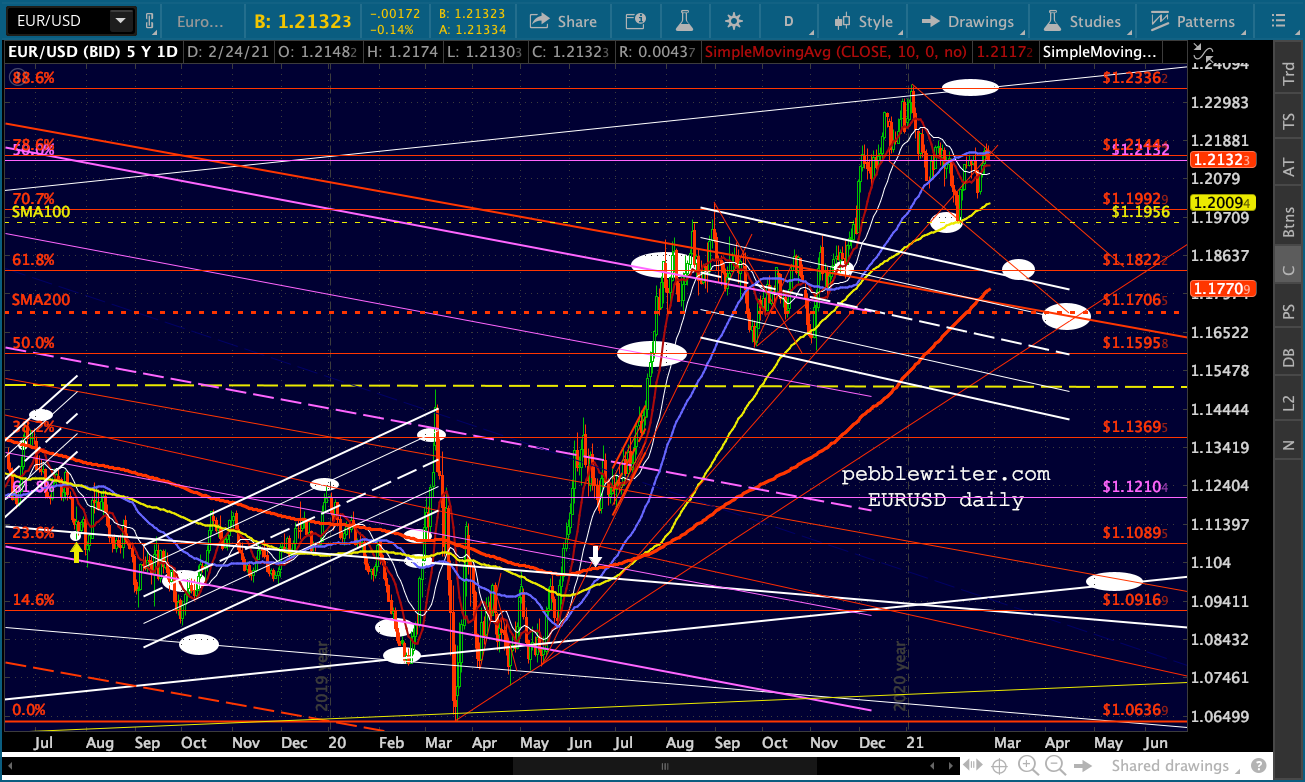

EURUSD looks ready to reverse…

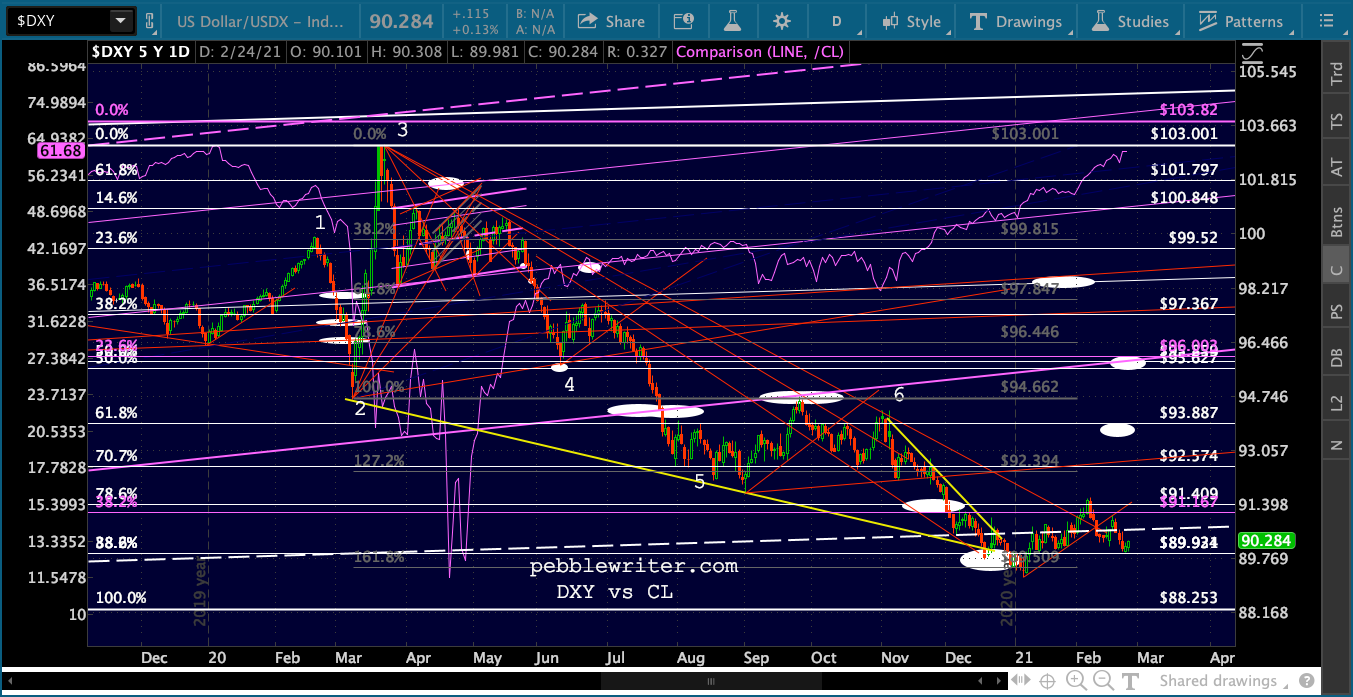

EURUSD looks ready to reverse… …which, depending on how the yen does, could give DXY a nice boost.

…which, depending on how the yen does, could give DXY a nice boost. But, remember, the BoJ won’t accept a perpetually lower yen as long as oil and gas prices remain elevated. We saw a big bump in Jan where CPI came in at -0.49% vs Dec’s -1.17%.

But, remember, the BoJ won’t accept a perpetually lower yen as long as oil and gas prices remain elevated. We saw a big bump in Jan where CPI came in at -0.49% vs Dec’s -1.17%.

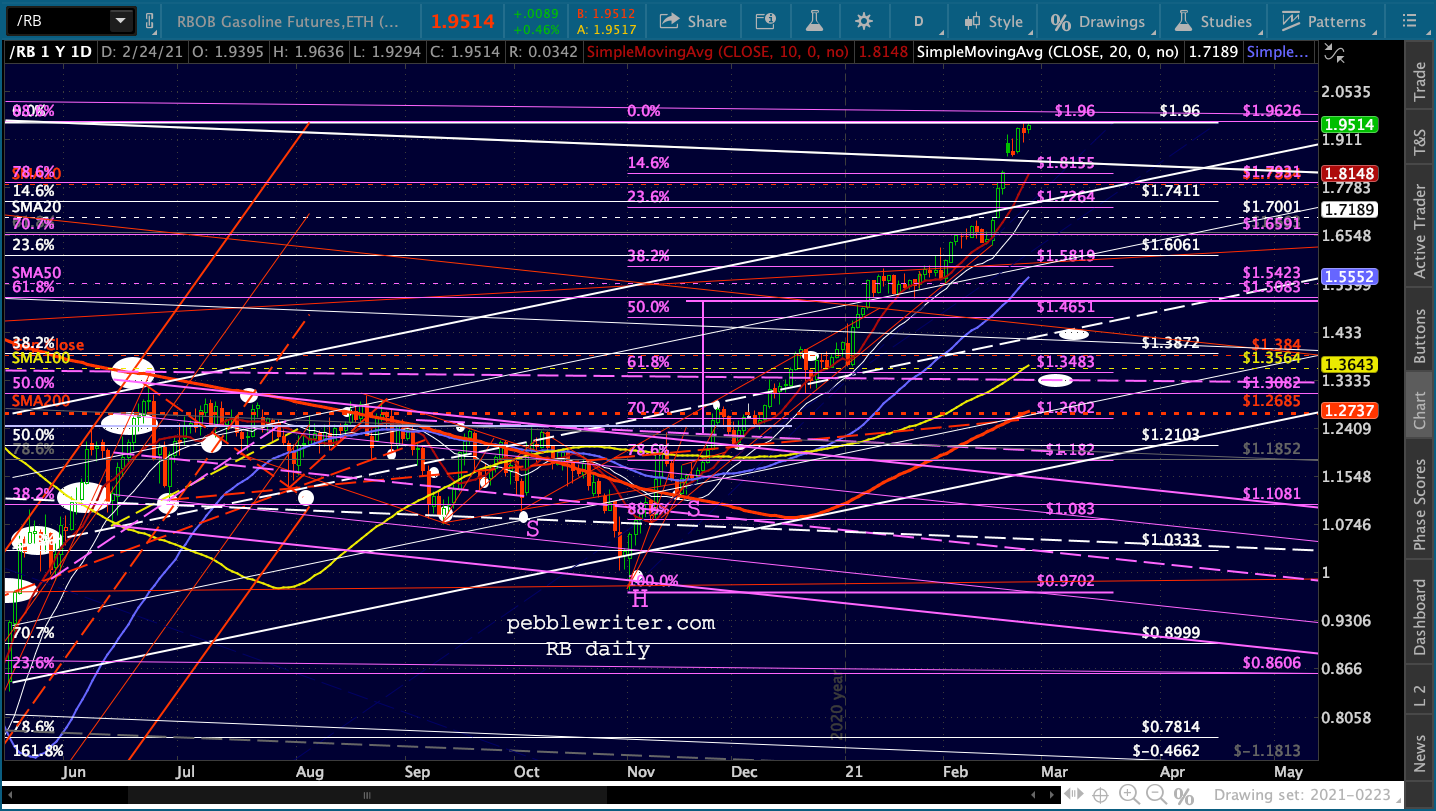

Remember what happened back in Oct 2018 when oil last peaked. The 10Y rallied to .139% as annual CPI tagged 1.39%. Japan cannot tolerate positive interest rates for very long. So, something has to give here. The obvious solution is to have oil/gas correct sharply.

So, something has to give here. The obvious solution is to have oil/gas correct sharply.

The final weekly read for Feb gas prices has already occurred. The monthly data will show a 2.7% increase versus the 8.7% decrease in Jan which produced a 1.40% CPI. This, alone, should nudge CPI pretty close to 2%. If prices don’t start declining right away, Mar will show a 13.5% increase and Apr will show a whopping 40.2% increase.

The final weekly read for Feb gas prices has already occurred. The monthly data will show a 2.7% increase versus the 8.7% decrease in Jan which produced a 1.40% CPI. This, alone, should nudge CPI pretty close to 2%. If prices don’t start declining right away, Mar will show a 13.5% increase and Apr will show a whopping 40.2% increase.

Surely the Fed has done the math and has a whole squad of PhD’s who have come up with the same conclusions. So, either they will proceed with what seems to be an attempt to divert attention from the problem, or they correct the problem while they can.

Stay tuned.

Comments

2 responses to “Bonds: Not Buying It”

Today, on the XLF I’m showing 720,000 calls vs 173,000 puts. Looks like extreme bullish sentiment. XLE is very close to filling some long term gaps I’ve been patiently waiting for. VIX is closer to filling the gap at 18.00.

Hello PW, a question on Oil and Bank stocks. I notice that oil stocks and bank stocks seem to go up and down together in similar scale. Since oil had been going up since last November, bank stocks are heading to the moon.

Some bank stocks are setting one year high today to “celebrate” the rise of oil.

If oil goes down hard, would bank stocks go down in similar fashion?

Thanks!