When it comes to retail, these are the best of times and the worst of times. Retail sales last month grew at a 5.8% annual rate — the best since March 2012. But, revolving credit (which recently hit new, all-time highs) has been growing at an annual rate of over 10%. And, delinquencies are on the rise.

But, revolving credit (which recently hit new, all-time highs) has been growing at an annual rate of over 10%. And, delinquencies are on the rise.

From a retailer’s standpoint, unless you’re Amazon (33% YoY revenue growth in Q3) you’re not loving the data at all.

From a retailer’s standpoint, unless you’re Amazon (33% YoY revenue growth in Q3) you’re not loving the data at all.

And, not even Amazon can be too excited about the lethargic pace of real income “growth.”

And, not even Amazon can be too excited about the lethargic pace of real income “growth.”

continued for members…

continued for members…

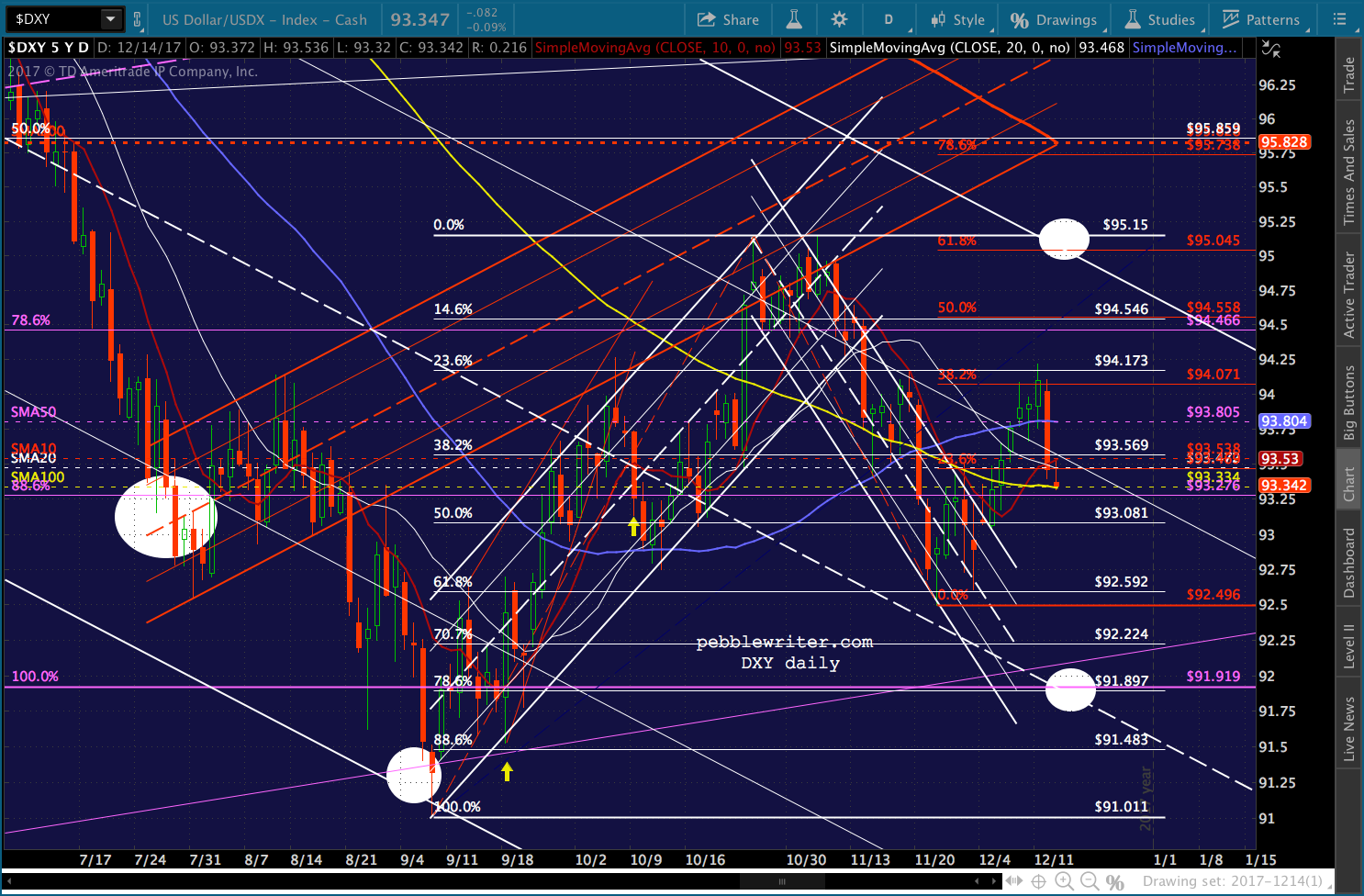

DXY slid through its shorter-term support this morning, but caught a bid at the SMA100 and looks likely to make a recovery. If it can push back through the .786 channel line (93.569) there’s still a chance it’ll test the former high and the channel top at around 95. If it can’t 91.897 is looking like the magic number.

If it can push back through the .786 channel line (93.569) there’s still a chance it’ll test the former high and the channel top at around 95. If it can’t 91.897 is looking like the magic number.

I’m partial to the under, here, as there simply wasn’t enough hawkishness in yesterday’s Fed show to justify further gains. But, in currencies, of course, everything’s relative. And, the BoJ and ECB have done nothing terribly hawkish either. TPTB could push the USD higher through the end of the year — but, there’s a bearish tint to the chart. And, RB/CL could drive the rally into year end.

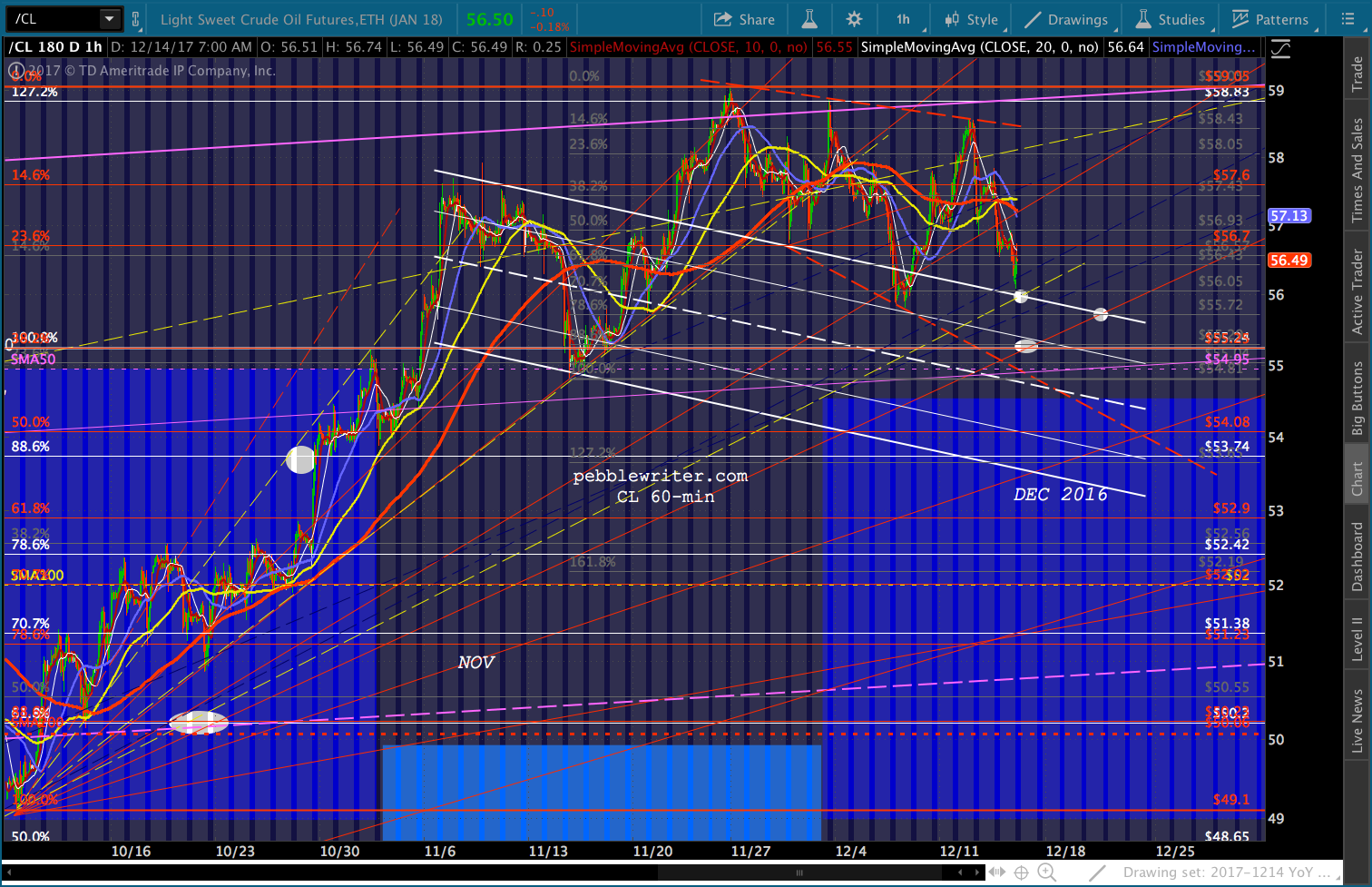

RB slightly overshot its .618, but is bouncing back above it anyway. At this point, we’ll look for resistance at the SMA100 at 1.6788, followed by the cloud bottom at 1.6884.

RB slightly overshot its .618, but is bouncing back above it anyway. At this point, we’ll look for resistance at the SMA100 at 1.6788, followed by the cloud bottom at 1.6884. CL just backtested the broken white channel and fan line at 56.09, which leaves it with a reason to bounce if it so chooses. A drop through 56 would open it up to 55.25, followed by 55, 52.9 and 51.23ish.

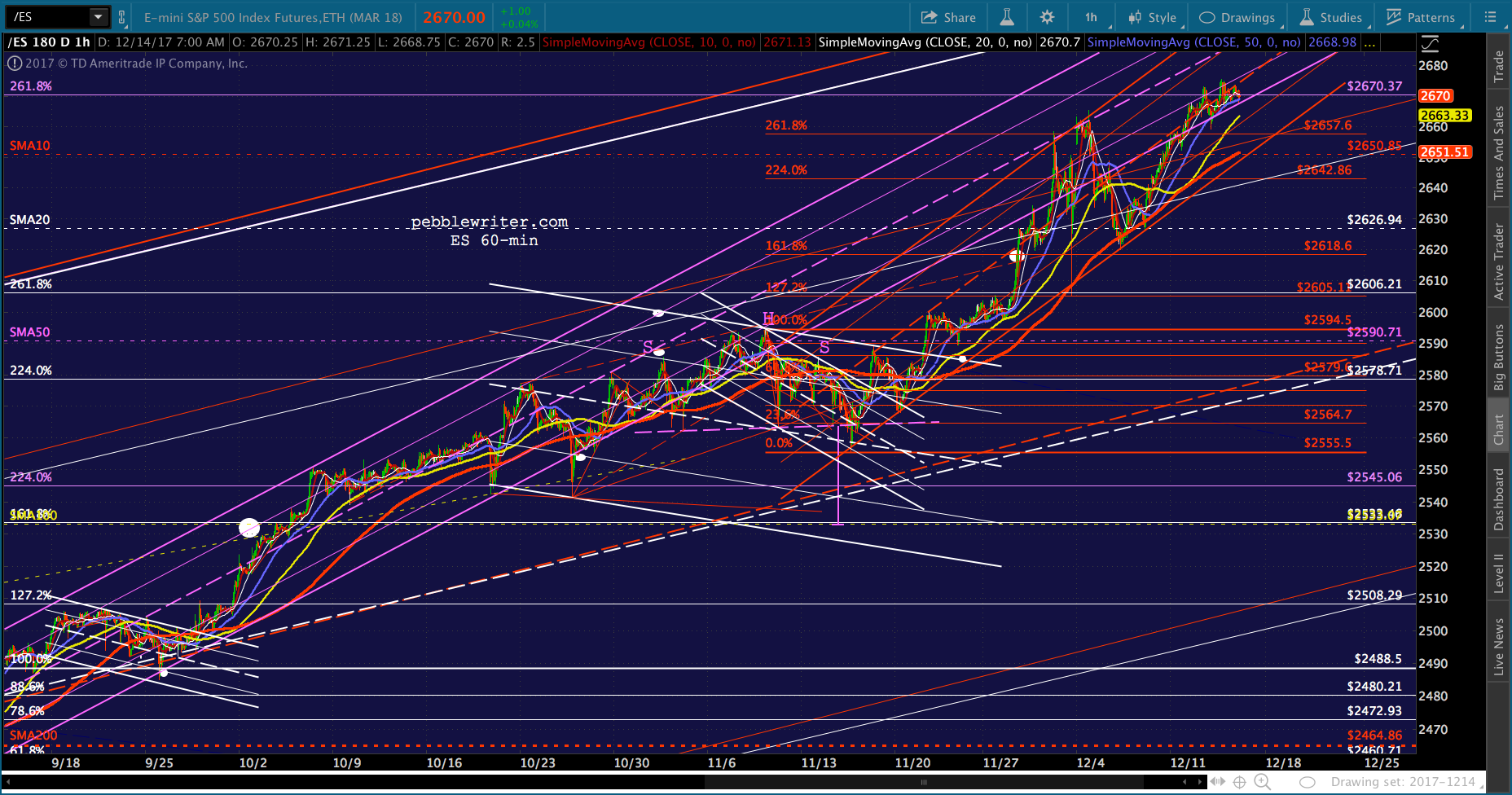

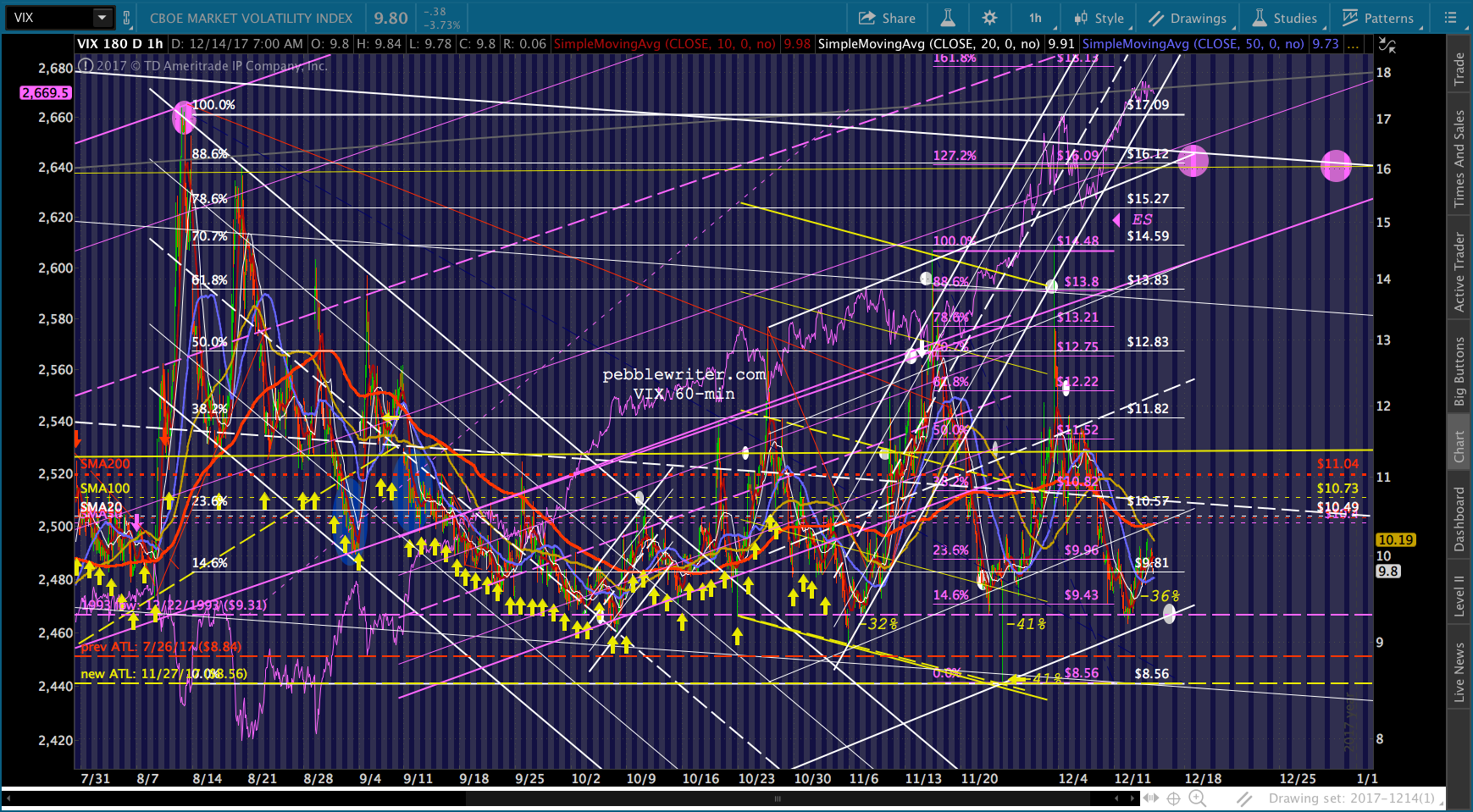

CL just backtested the broken white channel and fan line at 56.09, which leaves it with a reason to bounce if it so chooses. A drop through 56 would open it up to 55.25, followed by 55, 52.9 and 51.23ish. Futures are up 1 point courtesy of a 3% plunge in VIX. Funny how it’s taking more and more downside in VIX to produce a small increase in SPX. I suspect even the algos are tiring of this charade.

Futures are up 1 point courtesy of a 3% plunge in VIX. Funny how it’s taking more and more downside in VIX to produce a small increase in SPX. I suspect even the algos are tiring of this charade.

I’m off to the hospital, hopefully to bring my daughter home. I’ll check back in later in the session.

I’m off to the hospital, hopefully to bring my daughter home. I’ll check back in later in the session.

GLTA.