ES has given back yesterday’s gains after bumping into the top of the rising channel which has guided it since late March. A large sell off would be unusual for the days leading into a Fed decision, let alone OPEX and the end of Q2. But, then again, there’s nothing normal about the market these days – which is why we need to keep a very close eye on VIX.

But, then again, there’s nothing normal about the market these days – which is why we need to keep a very close eye on VIX.

continued for members…

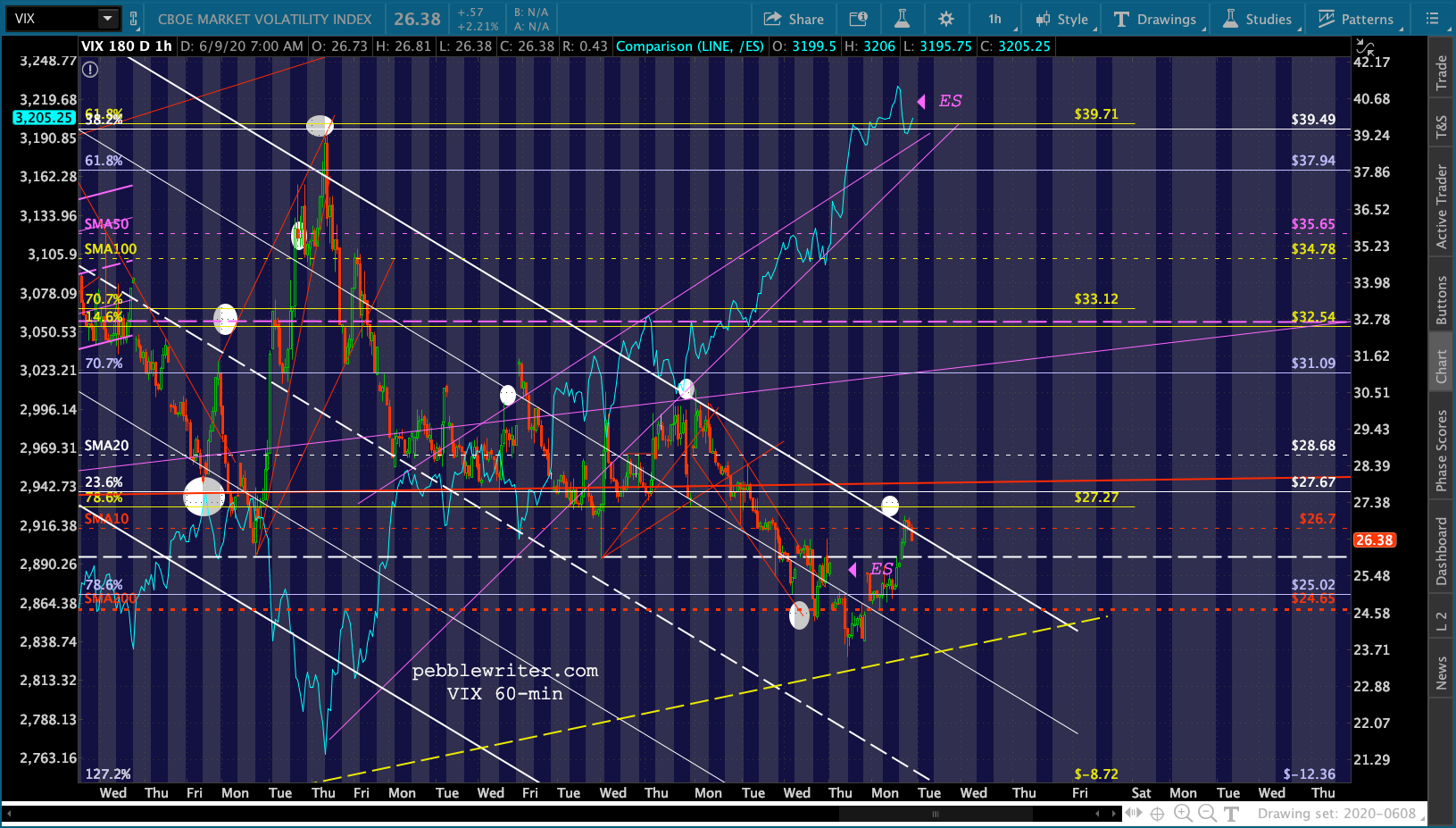

VIX faces another important test of its channel top as it’s about to be squeezed by the yellow TL from the January lows. A breakout here would presage more drops in stocks…

…while a reversal and breakdown of the TL would open up the .886 and potentially lower.

…while a reversal and breakdown of the TL would open up the .886 and potentially lower.  At this moment, ES is holding its SMA5 200, with the .886 just above at 3258 – about 28 points from yesterday’s highs.

At this moment, ES is holding its SMA5 200, with the .886 just above at 3258 – about 28 points from yesterday’s highs. SPX got even closer, about 23 points.

SPX got even closer, about 23 points. The most likely scenario is a stall, killing time until a final push up to (or topping) 3258 as the end of the month approaches. To reach it now would be counterproductive as it would suggest a reaction at a time when TPTB aren’t quite ready for one.

The most likely scenario is a stall, killing time until a final push up to (or topping) 3258 as the end of the month approaches. To reach it now would be counterproductive as it would suggest a reaction at a time when TPTB aren’t quite ready for one.

AAPL exemplifies the situation many stocks are in, with its recent breakout not quite to a point where it should reverse.

A stall would require one of the algo drivers to step up and whack stock prices.

A stall would require one of the algo drivers to step up and whack stock prices.

Right on schedule and as expected, USDJPY has given up on its “breakout.” This makes it much easier for stocks to slump…  …without actually breaking down…

…without actually breaking down…

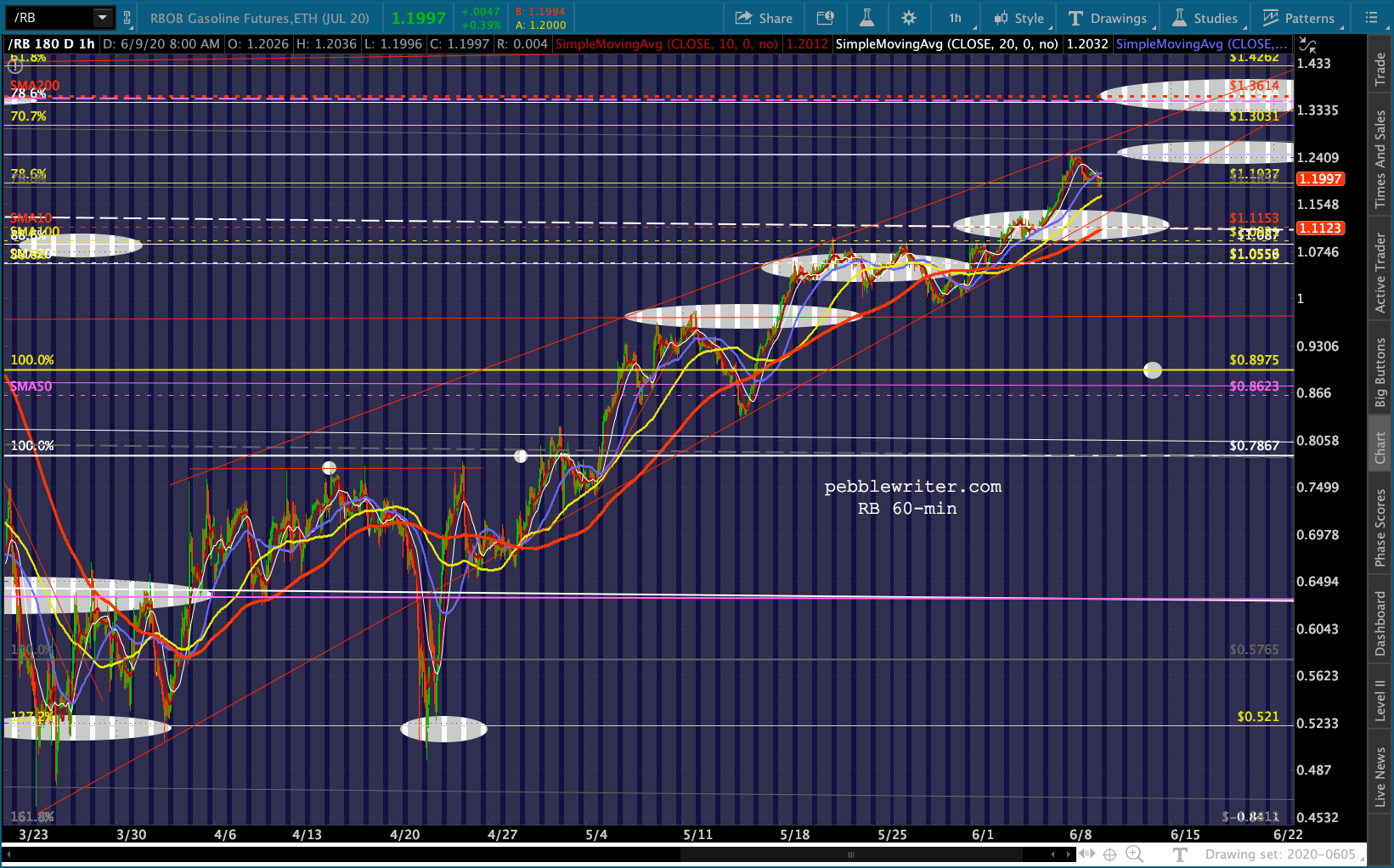

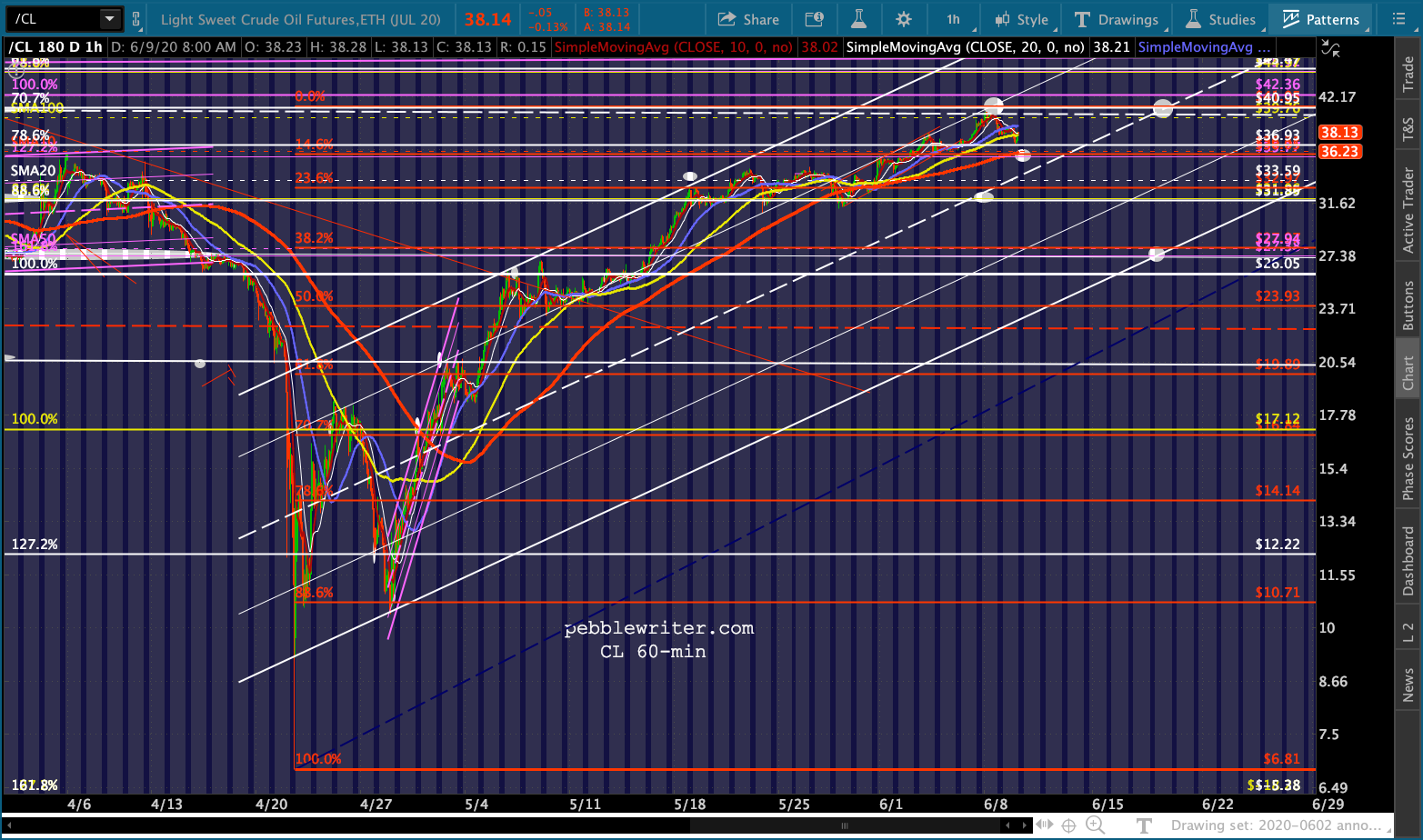

…especially since CL and RB are still hanging in there.

…especially since CL and RB are still hanging in there.

Note that CL didn’t quite reach its gap close at 41.05. It only reached 40.44, suggesting that it could hang around this price range for another few days of even the end of the quarter. I’d rather be short than long at this point, but we have to consider the possibility that it goes nowhere for a while.

Note that CL didn’t quite reach its gap close at 41.05. It only reached 40.44, suggesting that it could hang around this price range for another few days of even the end of the quarter. I’d rather be short than long at this point, but we have to consider the possibility that it goes nowhere for a while.

The wild card, of course, is the Fed announcement coming tomorrow. They can’t very well take back the trillions they’ve already thrown into the markets. But, they could put a damper on things by admitting that they over-reacted and that they’d look to pare back any further support.

The market expects the Fed to expand its accommodation. Note how DXY is still threatening new lows… …and EURUSD continues to bounce.

…and EURUSD continues to bounce. But, I consider this scenario unlikely, as the Fed knows that new all-time highs in SPX and DJIA would result in even more accusations of meddling. IMO, market integrity is at an all-time low. Once lost, it would be difficult to rekindle.

But, I consider this scenario unlikely, as the Fed knows that new all-time highs in SPX and DJIA would result in even more accusations of meddling. IMO, market integrity is at an all-time low. Once lost, it would be difficult to rekindle.

True, businesses are still in trouble, with bankruptcies on the rise. But, lower overall interest rates would do little to prop up zombie companies and would do nothing to boost consumer demand. I would expect any expansion of accommodation to be more targeted than past actions, such as increasing lending through the Main Street facility.

But, I fully recognize that most pundits are suggesting otherwise – which is why I’ve kept that 94.20 scenario for DXY in place. If the yen continues to strengthen, it would add to the USD’s troubles.

Bottom line, expectations are high for more aggressive Fed action. I think the risk is that they do less than expected, or at least hit pause, and that this will lead to a rebound for the dollar.

The 2s10s backed off its threatened breakout.

While the 2Y has held up nicely…

While the 2Y has held up nicely…  …10Y yields have fallen sharply from Friday’s highs – perhaps in anticipation of today’s 10Y auction.

…10Y yields have fallen sharply from Friday’s highs – perhaps in anticipation of today’s 10Y auction.